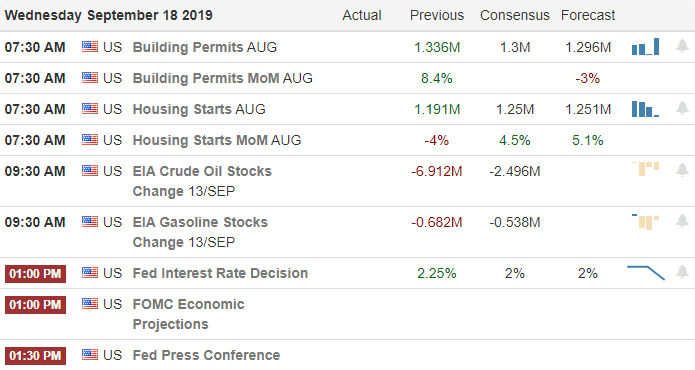

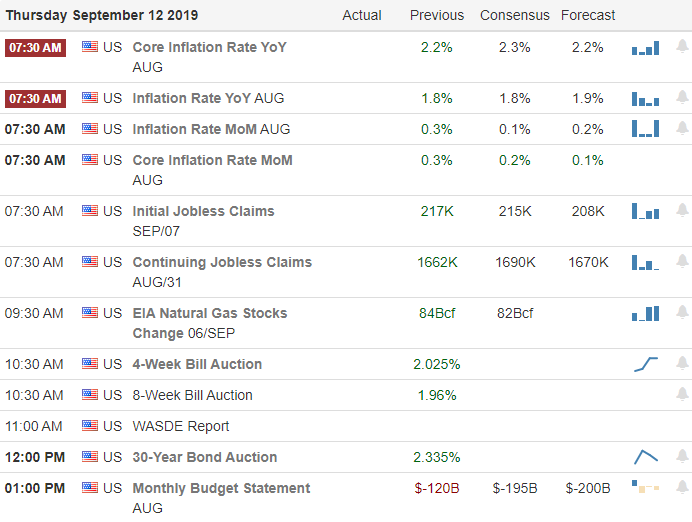

Jerome Powell is in the unenviable position of being criticized no matter what he does today as the entire world is focused on the Fed rate decision at 2:00 PM Eastern today. Choose to cut the rates a little and market could be disappointed, and Whitehouse tweet barrage will begin. There will likely be criticism within the committee as at least 2-dissenting votes expected to occur suggesting he has bowed to the market. As traders, no matter what the FOMC does, our job is to set aside the bias and trade the chart following our trading plan rules.

Overnight Asian markets closed mixed overall pretty flat on the day as they wait for the FOMC decision. European indexes are however seeing green across the board but only holding very modest gains as they wait. US Futures ahead Housing and Oil Supply numbers point to a flat to slightly bearish open. After the morning rush, I expect very slow and choppy price action until the Fed decision. After that anything is possible, so plan your risk very carefully.

On the Calendar

On the hump day earnings calendar, we have just 11 companies

reporting results. GIS is the notable

report on the day.

Action Plan

Oil prices moderated yesterday when Saudi Arabia said they have largely restored oil production and should be back to full capacity by the end of the month. Benjamin Netanyahu’s attempt at a 5th term as Prime Minister is struggling this morning as the election is said to be to close to call. It would seem political uncertainty is a worldwide theme these days. Today is all about the FOMC and whether they will or won’t or how much they choose to adjust the interest rates. No matter what Powell will have to face criticism. Cut the rates, and it’s likely there will be at least 2-dissenting votes cast on the committee. Don’t cut the rates enough and expect a barrage of disapproval tweets from the Whitehouse.

No matter what you think or want to happen; as traders, the best we can do is stick to our rules, set aside our bias and trade the chart. We will all know the answer at 2:00 PM Eastern and all the media spin before that is speculation and distracting noise. Currently, US Futures point to flat to slightly bearish open where we can expect choppy price action until the rate decision is released. After that, all bets are off, and anything is possible. If the market embraces the decision new, record market highs look possible. Disappoint the market, and the index charts could easily begin to show topping patterns. Hang on it could be a wild day!

One of the biggest one-day increase in oil prices in 30

years but the overall market seemed to take the blow in stride only losing

about half of one percent on the day. Rising

domestic production decreasing our dependence on foreign crude likely played a

significant role in the muted market reaction.

Another might be the no-rush response to retaliation of those

responsible for the attack. Last but not

least is the hopefulness that the FOMC will lower interest rates on Wednesday

afternoon. The question rattling around

in my head is what happens if the FOMC disappoints due to the rather strong US economic

data?

The rising geopolitical concerns and rising energy prices

led to Asian markets closed mixed with the Hong Kong exchange suffering the biggest

decline. Across the pond European are also

cautious this morning trading mixed but modestly lower overall. With the FOMC kicking of their 2-day meeting

today and ahead of Industrial Production number the US Futures points to a modestly

lower open and what could be another very choppy price action day as we wait

for the Fed decision.

On the Calendar

We have 22 companies stepping up to report today according to

the Earnings Calendar. Notable reports include

FDX, CHWY, ADBE, & CBRL.

Action Plan

Although the oil made it’s biggest one day spike in nearly

30 years, the overall market barely flinched only falling about half a percent

overall. While evidence mounts that the

oil field attacks came from Iran, the President is exercising patience on

retaliation as investigations continue. With

US energy production so high nowadays we have decreased dependence on Saudi oil,

but the other factor for a muted market reaction is the pending FOMC announcement

on Wednesday afternoon. Although fed

fund futures have recently decreased the odds of a rate cut slightly but as of

yesterday, the probability remains at 26% of an FOMC accommodation.

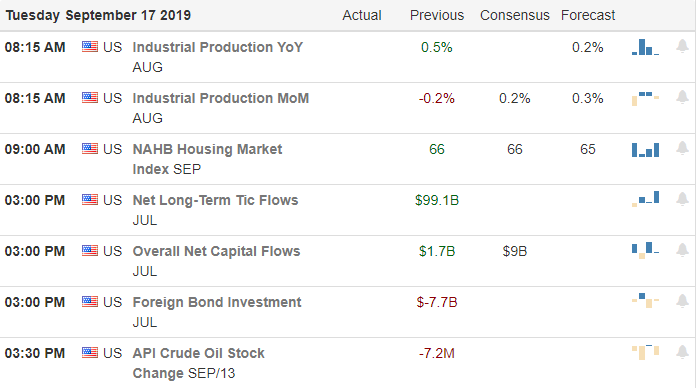

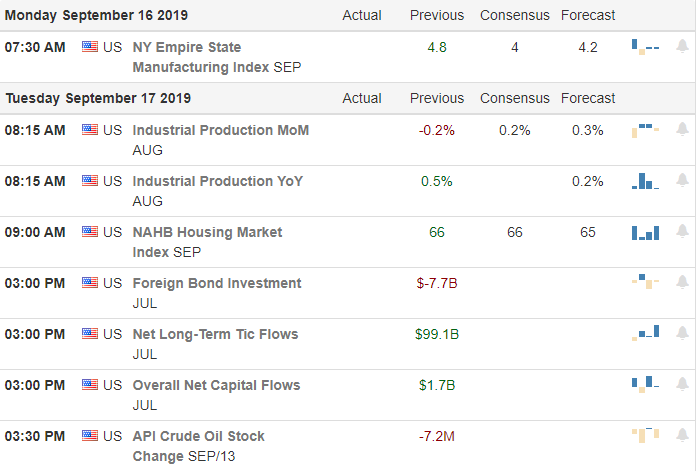

Ahead of the open US Futures are pointing to a modest decline

as the FOMC begins its 2-day meeting. We

have Industrial Production numbers at 9:15 and Housing Market Index reports on

the economic calendar and after the bell earings from FDX and ADBE that could

move the market. Although there could be

a news-driven event that creates some price volatility, I’m largely expected a

light and choppy day as the market waits on the Fed decision.

Crude prices rise sharply after Iranian attacks on Saudi oil fields forced the shut down of nearly 50% of their daily production. The President has authorized the opening of the US Strategic supplies in response. The UAW has officially placed 48,000 General Motors on strike, but negotiations are set to resume this week. What a difference a weekend can make! With the market hopeful of FOMC rate decision and forecasts on Wednesday afternoon and the weekend disruptions, we should prepare a bit more price volatility in the days ahead.

Overnight Asian markets closed mostly lower as higher oil

prices could pressure and the already challenged Chinese economy. European markets are seeing red across the

board in reaction to oil prices and the obvious geopolitical tensions it’s likely

to occur. US Futures had bounced slightly

off of overnight lows pointing to a gap down open. One has to wonder what comes next as a response

to the attack on world energy supplies?

On the Calendar

Although were nearing the end of the quarter we still have stragglers

yet to report. Today we have 21

companies expected to report but is see none that are particularly notable.

Action Plan

Iranian attacks on Saudi Arabian oil fields wiped out 5% of

the global supply and forced the shutdown of nearly 50% of their daily production. Not surprisingly crude price rose sharply as

futures markets reopened. What’s more,

unsettling is what comes next? Disrupt

the supply of energy, and a significant military response is not likely far

behind. Aerospace and Defense sector

stocks may join in the rally with oil prices.

Tuesday begins the 2-day FOMO meeting with their announcement on rates and

forecasts at 2:00 PM Eastern Wednesday.

Typically the market tends to chop with lighter than normal

volume ahead of an FOMC announcement but, normal may be difficult to achieve today

with the new uncertainty of energy. US

Futures have improved from overnight lows but continue to point lower this

morning with the Dow expected to gap down about 100 points. Keep in mind the 8-day rally has put the

indexes in a short-term overbought condition with 50-moving average support

significantly lower so we should not rule out the possibility of a test. However the hopefulness of lowered interest

rates could inspire the bull to hold firm.

The ECB delivered as expected, and the President said he is

willing to consider an interim trade deal adding rocket fuel an already extended

rally lifting the SPY temporarily to a new record high print. After 8-days up it hard to be a buyer but the

bulls are working hard this morning suggesting more than a 100 point Dow gap and

possibly secure more records before the weekend. With the FOMC expected to deliver even more

stimulus next Wednesday the momentum remains firmly with the bulls.

Overnight Asian markets closed with green across the board with

growing optimism of a trade deal. European

markets are mostly bullish this morning after the aggressive ECB move even as

worry of a German recession grows. The US

Futures point to another triple point gap up in the Dow on its 8th

day of rally that has recovered nearly 1400 points. Consider the risk carefully you carry into

the weekend as this rally become very extended.

On the Calendar

On the Friday Earnings Calendar, we have just 11 companies

reporting results. Looking through the

list I can find none that are particularly notable.

Action Plan

Although there was some light selling as we moved into yesterdays

close the bull, remain solidly in control with relentless upside pressure. Having said that with the indexes up 8-days

in a row and looking to extend that streak this morning, I don’t see this as a

buying opportunity. Heading into the

weekend with a gap up open on Friday seems more a profit-taking rather than a

day to add risk.

Our T2122 indicator is flashing an extreme over-bought short-term

condition, but I wouldn’t bet on a selloff until we see something in the price

action that suggests the bears are willing to fight back. That could begin today, but with the bullish

momentum and an FOMC expected to provide more stimulus I wouldn’t be surprised if

the bears have already taken the rest of week off. Have a wonderful weekend everyone!

The huge Institutional rotation into value plays created an amazing melt-up in index prices yesterday. Traders can witness this massive shift with a quick study of value ETF’s that have moved up so quickly they are nearly parabolic. Adding fuel to the fire is the expected ECB stimulus package and the likely accommodative FOMC decision next Wednesday. Toss in the Trump tariff delay from Oct. 1 to the 15 in what he called a goodwill gesture, and we have the recipe for new record highs in the indexes. I would be careful chasing this rally at this point considering the Dow has already rallied more than 1100 points in just 7-days of trading.

Asian markets mostly rallied on the Trump tariff delay news

but continue trouble in Hong Kong kept the HSI in the red at the close of

trading. European indexes have reversed

earlier gains on fears of a German recession even as the ECB is expected to

make an accommodative decision today.

Undeterred by European concerns the US Futures point to yet another gap

up open to challenge the all-time high resistance levels in the DIA, SPY, and

QQQ.

On the Calendar

The Thursday Earnings Calendar indicates that 25 companies are

confessing their quarterly results. Notable

reports include KR, AVGO & DLTH.

Action Plan

An amazing rally yesterday as the indexes relentlessly marched

higher. To put this extraordinary rally

into perspective, the Dow has gained more than 1100 points in just 7-days or

trading. A big portion of the rally

seems have occurred in a huge institutional rotation into value plays that happen

to be heavier weighted in the indexes. Also,

there appears to be a substantial rotation out of safety plays, such as precious

metals and bonds into stock value plays.

One reason for this is the expectation that ECB and the FOMC

will both provide a monetary backstop to fears of slowing world economies. The president in what he called a goodwill

gesture in delayed the tariffs that were scheduled to increase on October 1 to

the 15th of the month. As a

result this short-term over-extended market is pointing to further extension

this morning. The tariff extension,

continued institutional rotation, and the likely ECB stimulus package expected

today could easily inspire the bulls to set new record highs in the

market. I would, however, caution traders

to be careful not to chase this rally after so many days up. Profit-taking could begin at any time so keep

a watchful eye on price signals.

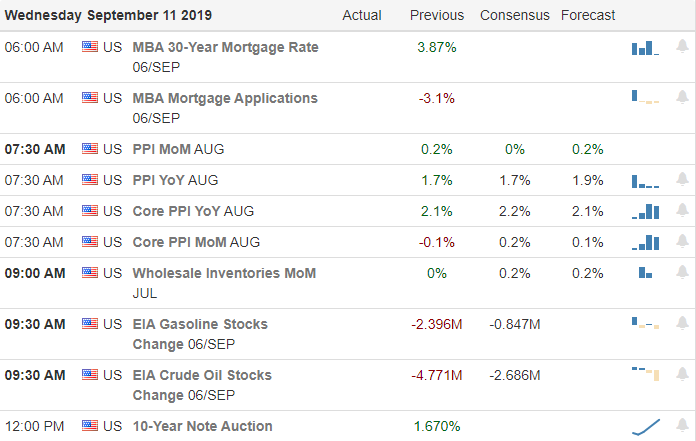

Today we remember one of the most tragic days in US history,

September 11th, 2001, where nearly 3000 fellow citizens died. First responders that give their lives that day

will be honored this morning at the market open with the ringing of the

bell. We are also waiting to see if the

ECB will provide a stimulus package and the latest reading of the Producer Price

Index. The bulls and bears continue to

battle in a very tight and challenging to trade chop. Perhaps the market can find some inspiration from

the ECB today, or perhaps we continue to chop as we wait on the FOMC next Wednesday.

Asian markets closed mixed waiting on the ECB, and Apple

suppliers rallied on the unveiling of their new product yesterday. European markets are green across the board

this morning in anticipation of their central bank decision. The US Futures point to a modestly higher

open waiting on the ECB. There is something

about the smell of freshly printed money that the bulls can’t get enough of and

just maybe the ECB will score them the fix they desire.

On the Calendar

The hump day Earnings Calendar has 24 companies expected to

report results. ACB & TRLD are among

the notable reports today.

Action Plan

As we remember and honor the nearly 3000 Americans that died

on September 11th 2001 we wait to hear from the ECB and a possible

stimulus package. There is not much that

the market loves more than the smell of freshly printed money. It’s a little like a heroin addict that knows

the drug is not good for them, but the immediate gratification of the next high

outweighs the long-term effects. The damaging

effects of debt no longer appears to matter as long as the market continues to

go up in the short-term. The President agrees

tweeting just a few minutes ago, “Fed boneheads’ should cut interest rates to

zero ‘or less,’ US should refinance debt.”

Wow!

US Futures point to a slightly higher open this morning as

we wait on the ECB and ahead of PPI numbers at 8:30 AM Eastern that is expected

to decline according to consensus estimates.

Although indexes continue to show signs of short-term overbought

conditions the bulls currently seem determined to attack all-time highs and a

stimulus package could be just the inspiration to get it done. However, we could also see more choppy price

action as we wait for the FOMC to chime in on interest rates next Wednesday. An institutional rotation seems to be underway

with risk coming out to defensive assets and rolling into value plays such as financials

and energy.

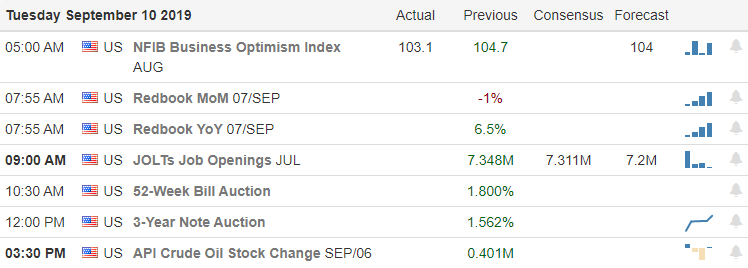

Are you frustrated with the current price action, overnight

gaps and go nowhere choppy days? Do you

feel as if your missing out and feeling the pressure to trade not wanting to

miss out on your share? Believe me; you

are not alone! I speak with may traders

every day that share the same frustration with this uncertain news-driven market. Those that succumb to the emotion of missing

out have and continue to suffer significant losses while traders standing aside

waiting for their edge to return are equally frustrated by the market condition

but retain their capital as they wait.

Are you holding onto an edge, or are you trading on emotion and

finding your account suffering as a result?

The choice is yours. You are the

CEO of your trading business. The buck

stops with you! It’s perfectly okay to

feel frustrated with the current condition of the market and the wild price action. That’s normal, but if you’re giving up your

trading edge and allowing your emotion or sheer boredom to guide your trading

your capital and your confidence will both disappear very quickly. Make your choice!

On the Calendar

We have just 14 companies on the Earnings Calendar to fess

up to quarterly results. Notable reports

today include GME, PLAY, RH & ZS.

Action Plan

Choppy consolidation consumed the vast majority of yesterdays

price action. However, it would seem there

is an institutional rotation underway selling-off market leaders and picking up

value plays. The rotation also appears

very targeted into heavily weighted index names that have significant impacts on

overall index valuation. Overnight Britain’s

Prime Minister failed in his attempt to force a new vote on Brexit creating a

stalemate with Parliament as the deadline nears. Forty-Eight states have joined an antitrust

investigation into GOOG while 11 states have joined in antitrust investigations

into FB. Big Tech is also under federal antitrust

scrutiny as AAPL, FB, GOOG & AMZN come under fire.

US Futures rallied off overnight lows currently pointing to

modestly lower open. We have the APPL

dog and pony show this morning as they unveil there new iPhone line up so

expect some volatility in the stock. I

would not be surprised to see continued choppy price action as the market waits

and hopes on as ECB stimulus package later this week and the FOMC decision Wednesday

the 16th. Of course, any is

possible in this emotional and news-driven market, so plan your risk carefully.

Hong Kong citizens ask for US help to gain their freedom while

China directly accuses members of Congress of inciting new violent riots that

resumed last night. How will this affect

the scheduled US/China trade talks next month?

The Taliban issued a direct threat to US lives after the President

abruptly canceled peace talks, and Afghanistan is said to be bracing for

violence. The British Prime Minister is

once again attempting to force a vote on Brexit today while at the same time a

new Parliamentary bill to block the action is supposed to go into effect today

as well. With all this in play the bulls

are pushing for another gap up open continuing to stretch toward all-time highs.

Overnight Asian markets closed mixed but mostly higher as

Hong Kong protests flair up and Chinese exports unexpectedly decline. European markets are also mixed but mostly

lower at this hour as the Brexit battle continues and hoping for an ECB stimulus

action. US Futures point to another gap

up open ahead of a light day of earnings reports and a quiet economic calendar. I would not rule out the possible pop and

drop, and I would also not be surprised to see the bulls try very hard to keep

the momentum marching higher.

On the Calendar

The Monday Earnings Calendar expects 25 companies to fess up

to quarterly results today. The notable

report of the day is CTRP.

Action Plan

The US pulls out of peace talks with the Taliban this

weekend and violent protests once again break out in the streets of Hong Kong. While Hong Kong asks for US help to gain

freedom, China is directly accusing members of Congress for encouraging the

riots. One would rationally assume that could

be a major stumbling block to the scheduled trade talks scheduled next month.

Whether focused on the hopefulness of a future rate cut or

the sheer momentum of the current rally, the US Futures point to a bullish open. In the UK, Prime Minister Boris Johnson is

once again trying to force a vote for a no-deal Brexit while at the same time Parliament’s

new bill to block such an action goes into effect today. How all the uncertainty warrants the US markets

rallying toward record highs in the light of declining job increases makes little

sense. T2122 suggest we are at or very

near a short-term overbought condition, so watch the possible pop and drop but

don’t ignore the bullish momentum as this all or nothing emotional trading

continues.

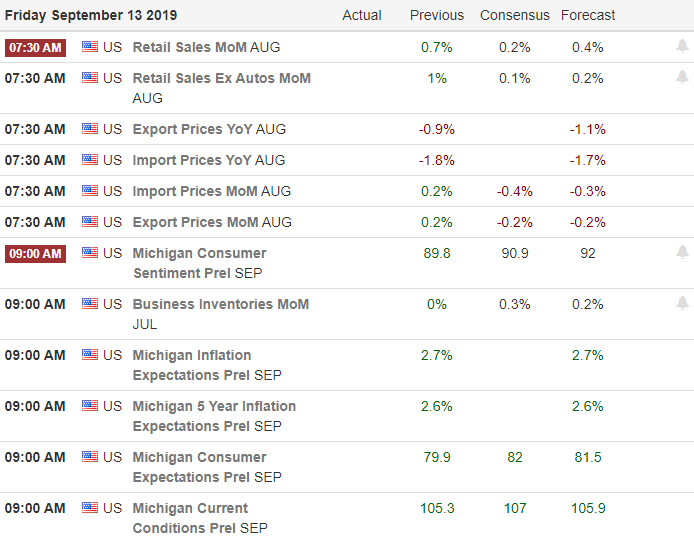

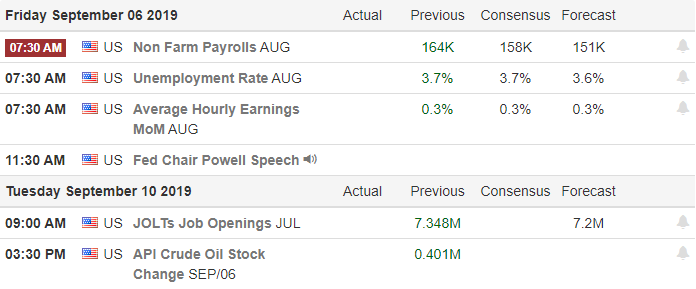

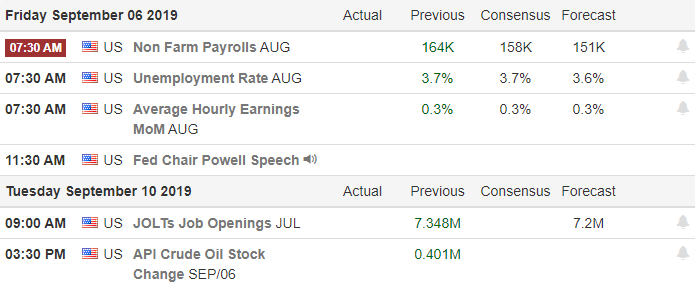

After gaping up triggering a brief short squeeze, the market

chose to chop sideways the rest of the day once again leaving the biggest price

action of the day in the gap. The question

for today is whether the Employment number and the Powell speech will inspire

for the bulls to push higher or if the bears will get the energy to attack backfilling

the gap below. After rallying nearly 850

Dow points in just 3-day on nothing more than a commitment to talk about trade

in month one has to wonder if emotion got way too far ahead of common sense?

Overnight Asian markets closed the week with green across

the board as Hong Kong protest subside.

European markets appear tentative and mixed this morning with the swirling

uncertainty of Brexit as they head into the weekend. Ahead of the Employment Situation Report, the

bulls are pushing for another gap up open but how the market actually opens

will greatly depend on the reaction the 8:30 AM report. Get ready for a wild day as we close out this

gap a day week and head into the uncertainty of the weekend.

On the Calendar

On the Friday Earnings Calendar, we have just 10 companies

reporting results. About the only somewhat

notable report is GCO.

Action Plan

A day after a short squeeze triggered on news that the US

and Chian will return to the negotiations table traders are now holding there

breath hoping the employment numbers will allow the bullishness to continue. The ADP report and the consensus estimates

suggest the economy created more than 160K jobs last month and that the unemployment

rate will remain flat. Currently the US

Futures, suggest a desire to extend the short squeeze into the weekend. However, a surprise miss would likely quickly

reverse that sentiment, and if the number were to come in better than expected

what would that mean for the hoped-for interest rate cut?

Technically speaking yesterday’s gap and go nowhere price

action saw key resistance levels broken and the DIA, SPY, and QQQ closed above

their respective 50-day averages for the first time in more than a month. Unfortunately, the 3-day gap riddled rally

has moved the indexes from a short-term oversold condition to a short-term

overbought condition according to the T2122 indicator. So the question is can the bulls hold on to this

big bullish reversal or will the bear’s attack and fill the big gap below? That leaves some tough choices for traders as

we head into the weekend.

High emotion continues to govern the market price action

this morning with yet another large news-driven morning gap. China and the US have agreed to hold

ministerial-level talks one month from now with deputy-level talk not expected

until mid-September. While it is very

good news that we will return to the negotiations table, a lot can happen during

that month of waiting as the uncertainty swirls around the market. I guess what I’m saying is that the All-Clear

is a long way off so expect volatility to continue and carefully plan your risk

as we navigate through this new-driven minefield.

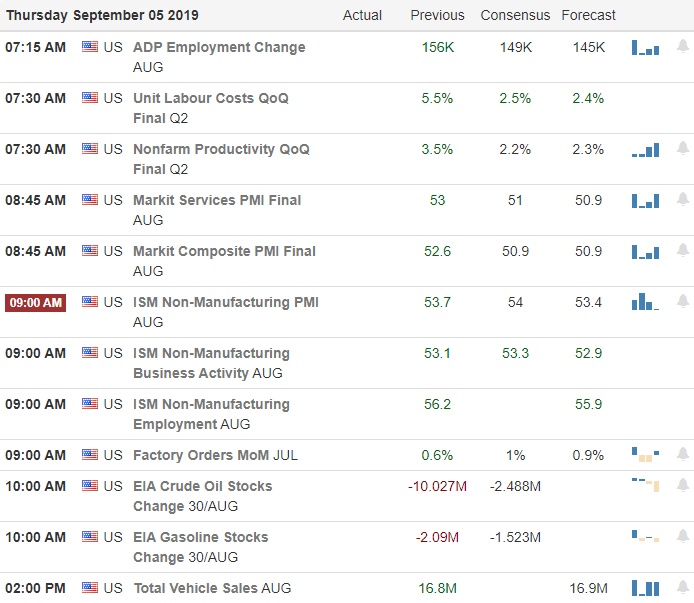

Overnight Asian markets Asina markets closed mixed but

mostly higher as traders closely monitored the developments in Hong Kong. Currently, European markets have mixed

results but mostly modestly higher, reacting to UK developments and China-US

news. US Futures are very happy this morning

ahead of a big day of economic reports and earnings. The Dow points to gap up of nearly 250 points

as it waits for the data dump.

On the Calendar

The Thursday Earnings Calendar is the biggest day of reports

this week with more than 40 companies reporting. Notable reports include LULU, ZM, CIEN, DOCU,

GIII, LE, MDLA, FIZZ, SIG, and ZUMZ.

Action Plan

US and China have agreed to hold ministerial-level trade

talks in early next month with the deputy-level meetings not taking place until

mid-September. British Prime Minister

Boris Johnson has now failed in his attempt to force a no-deal Brexit by the

end of October stabilizing the Sterling and kicking the can further down the

road. US Futures are bullish on this

news ahead of busy morning on the Economic Calendar as well our biggest day of

the week for earnings reports.

So once again the market is expected to significantly gap

this morning, but at least it’s in the same direction as yesterday’s gap up and

chop price action. Honestly, I have a

hard time understanding agreeing to talk about trade one month from now warrants

a gap of more than 200 points. However,

I also have to say that I’m not all that surprised considering how erratic and

emotional the price action has been over the last month. The question now is, can it hold as the

uncertainty swirls around us for another month.