All eyes will be on the CPI report coming out before the bell. Will it continue to inspire the bulls, or will it inspire the bears with worries of inflation? Ahead of the number, the 10-year treasuries rose to 1.69%, suggesting how critical this number could be in defining the path forward. The FDA came out this morning with a recommendation to pause the use of the J&J vaccine due to blood clotting worries. The futures markets have taken a turn for the worse as a result.

Overnight Asian markets traded mixed but mostly higher as Alibaba share surge for the second straight day. European markets trade with modest results this morning, with earnings and inflation data in focus. Ahead of the CPI report, U.S. futures point to a lower open on the eve of the 2nd quarter earnings kickoff.

Economic Calendar

Earnings Calendar

On the Tuesday earnings calendar, we have just 14 companies stepping up to report quarterly results. Notable reports include FAST & KRUS.

News & Technicals’

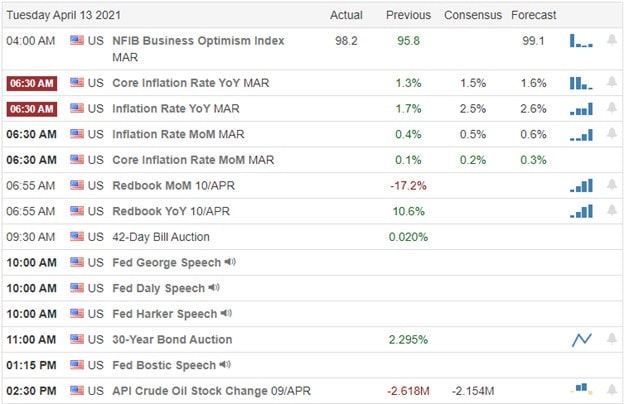

Critical economic data on the inflation front is on tap before the market opens with the CPI. The consensus projects the number to come in at 0.5%; however, markets could inspire the bears if it tops expectations. Conversely, should the number come in lower than the consensus, look for bullish inspiration to occur. Directly related to our possible inflation issues is the massive stimulus spending that pushed the U.S. budget deficit to a new record of $1.7 trillion this year. The 10-year Treasury yield moves back up this morning, topping 1.69% as we wait on the CPI numbers. On the pandemic front, the U.S. hit a new daily vaccination record, but unfortunately, infection rates are rising, with the country reporting 70,000 cases per day.

Yesterday proved to be a choppy sideways day for the indexes, and as we wait for the 2nd quarter earning kickoff, it’s very likely we could see more of the same assuming the CPI comes in as expected. Index trends remain very bullish even though the SPY and QQQ charts appear pretty extended in the short term. Plan your risk carefully as we head into earnings season. With all the big investment institutions singing in a chorus that a market boom is ready to begin, one has to wonder if they have factored in the possible inflation impacts that may result. Hmm? Stay with the trend but guard against complacency if the market should stumble for this very elevated position.

Markets opened just south of flat on Monday and then proceeded to grind sideways the rest of the day. This left us with inside day Doji across all 3 major indices. On the day, SPY gained 0.05% (to a new all-time high close), DIA lost 0.09%, and QQQ fell 0.13%. The VXX fell to 10.17 and T2122 fell outside of the overbought territory to 72.62. 10-year bond yields gained slightly to 1.671% and Oil (WTI) rose two-thirds of a percent to $59.71/barrel.

In Chip news, at the “Chip Summit” President Biden called for the chip, broadband, and battery technology portions of his Infrastructure plan to be approved. He read a letter from 23 senators and 42 House members expressing bipartisan support for $50 billion in government spending for semiconductor manufacturing and research. The 3 major US Auto-makers attended and all decried the loss of earnings and employee hours due to current chip shortages. For their part, the major chipmakers (TSM, INTC, Samsung, etc.) had all already announced tens of billions of dollars of investment (each, TSM having committed more than $100 billion) in new production capacity over the next 2-3 years. However, an Auto-Industry association called for new, immediate tax cuts to help automotive chip manufacturers add lines to existing plants now. In other chip news, NVDA announced it will begin making a server processor to compete with INTC and AMD in the highly-profitable data center market.

Less than a day ago, Fed Chair Powell told CBS 60 Minutes that it was “extremely unlikely” that the Fed consider raising rates this year. However, after-hours Monday, St. Louis Fed President Bullard told Bloomberg that as soon as the US reaches 75%-80% vaccinated, he believes the “tapering debate” will take place. This comes 12 hours before the CPI number and a slew of other Fed speakers weigh in. Elsewhere, Treasury Sec. Yellen announced that China will not be labeled a “Currency Manipulator” in her first semi-annual foreign exchange report to Congress.

Related to the virus, US infections are rising again after plateauing at a level above the fall level. The totals have risen to 31,990,143 confirmed cases and deaths are now at 576,298. The number of new cases has ticked higher again to an average of 69,926 cases per day. However, deaths are just starting to plateau again, now at 747 per day. Overnight, the FDA and CDC both called for a pause in the use of JNJ vaccine due to clotting issues. In addition, on Monday CDC Dir. Walensky said that MI should “shut things down” again because vaccinations alone will not stop the overwhelming surge in cases the state is seeing. On the plus side, the CDC also said that 50% of American adults will have at least one dose of vaccine by the end of this week.

Globally, the numbers rose to 137,340,422 confirmed cases and the confirmed deaths are now at 2,961,423 deaths. The trends have reversed and are now trending toward trouble again as we have seen significant upticks recently. The world’s average new cases are rising again (about 17,000 per day increase) and are now at 688,363 per day. Mortality, which lags, is rising again at 11,270 new deaths per day. The WHO said Monday that the world has seen a seventh straight week of increasing cases. Today, Germany reported an increase of almost 11,000 cases as the German Health Minister said the country had reached peak ICU capacity. On a brighter side, a new study published by the journal Lancet says the UK variant is much more transmissible but no more severe than the original virus.

Overnight, Asian markets were mixed. Thailand (-1.61%) led otherwise modest losses while India (+1.36%) and South Korea (+1.07%) led otherwise modest gainers. In Europe, markets are mixed on showing only small moves to either side so far Tuesday. The FTSE is down (-0.13%), DAX up (+0.12%), and CAC up (+0.28%) as of mid-day. As of 7:30 am, US Futures are all pointing to a modestly red open at this point (before CPI release). The DIA is implying a -0.38% open, the SPY implying a -0.30% open, and the QQQ implying a -0.11% open. Bond yields rose slightly overnight to 1.68% and Oil (WTI) is up half a percent to $60/barrel in premarket trading.

The major economic news scheduled for Tuesday is limited to Mar. CPI (8:30 am) and 4 Fed speakers (Daly at noon, George at noon, Harker at noon, and Bostic at 3:15 pm). Major earnings reports on the day are limited to FAST before the open. There are no major reports after the close.

The fear of inflation may be heightened today with Bullard’s less dovish note last night, CPI numbers this morning, and a slew of other Fed speakers later in the day. However, although we had indecisive moves on Monday, there is no doubting the trend is strongly bullish. With earnings season starting again on Wednesday, we may be in yet another “wait and see” environment.

Don’t predict moves or chase trades you have missed. Respect support and resistance as well as the trend. Keep taking your profits off the table when you can and maintain your discipline. Stay on the right side of the market trend and follow those trading rules. As we know, consistency is the key to long-term trading success.

Ed

Swing Trade Ideas for your consideration and watchlist: No trade ideas for Tuesday. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

In a Sunday interview, Jerome Powell said the extremely dovish policies would continue and that it is the Fed is highly unlikely to raise rates this year. With the last hour buying surge Friday, the DIA, SPY, and QQQ all set new closing records by the close. Last week was overall a frustratingly choppy price action punctuated by the Monday gap and Friday late-day surge. This week we kick off 2nd quarter earnings with the indexes in a short-term, very extended condition adding significant danger for retail traders. Anything is possible, so buckle up it could be a wild ride this week.

Overnight Asian markets saw red across the board even as shares of BABA rose 6.5% after being fined. European markets trade mixed but primarily flat this morning. With a light day of earnings and economic reports, U.S. futures have rallied well off overnight lows as the premarket pump begins. Prices could remain light and choppy until we get the big bank reports beginning on Wednesday. Plan your risk carefully.

Economic Calendar

Earnings Calendar

We have 12 companies listed on the Monday earnings calendar coming forward with their quarterly results. Notable reports include APHA & MIND.

News & Technicals’

On the news program 60 Minutes, Jerome Powell reaffirmed the Fed’s commitment to loose monetary policy. He went on to say, “it’s highly unlikely we would raise rates anything like this year.” According to reports, MSFT could announce a deal as early as today, the acquisition of NUAN. NUAN stock is indicated sharply higher this morning as a result. Despite a $2.8 billion anti-monopoly fine leveled by Chinese regulators, shares of BABA are popping 6% this morning following a 6.5% rally in Hong Kong overnight. On the pandemic front, Regeneron to request FDA clearance on an antibody-drug as a preventative treatment, Britain’s Pub drinkers return as lockdown eases, and Chinese vaccines don’t have very high protection, according to a top health official.

Last week’s price action started with a considerable gap on Monday and ended with a buying surge in the last hour of trading on Friday. However, the price action between those sharp moves was frustratingly light and choppy. Although the DIA. SPY and IWM show extreme bullishness; the charts also display an extremely extended condition after nearly 2-weeks of buying, creating a parabolic move that’s a long way from good price support levels. That said, with the Fed standing on the gas peddle and the 2nd quarter earnings season kicking off on Wednesday, there is no reason to believe that the market will not continue to extend. Until then, choppy price action is likely to continue.

Markets opened flat on Friday and ground sideways for most of the day. Then the bulls stepped in to rally hard the last 45 minutes of the day, going out on the highs. All three major indices closed at new all-time high closes on strong white candles. On the day, the SPY closed up 0.73%, DIA closed up 0.81%, and QQ closed up 0.61%. The VXX was flat at 10.31 and T2122 remains in the overbought territory at 85.41. 10-year bond yields were flat after the pre-market surge at 1.662% and Oil (WTI) was off half a percent to $59.34/barrel.

In weekend news, after the close Friday, GM announced even more cuts to overtime and shifts at US truck plants due to the global chip shortage. This came after both F and GM announced plans to idle some plants for the same reason. However, GM announced the normal summer downtime weeks will be canceled, in hopes the shortage will be over and production those weeks can make up for shutdowns now. This is all backdrop to a Whitehouse Chip Summit today. However, this summit is not likely to have any short-term impacts. Producers are already selling every chip they can make and it takes years to add Fab capacity to any chip manufacturing company. On Saturday, BABA was fined $2.8 billion (US value) by Chinese regulators for antitrust activities. Sunday it was leaked that MSFT is in late-stage talks to buy AI-technology firm NUAN for a purported value of $16 billion (potentially $56/share).

In other news, Fed Chair Powell told 60 Minutes that the US economy is poised for explosive growth due to vaccines and stimulus. Specifically, he said projections are pointing to the largest increase in GDP since at least 1984. He also said it remains “highly unlikely” the Fed will raise rates this year but expects short-term inflation to be “moderately above the Fed’s 2% target.” In other news, Sunday France made climate change news, as the put forth rules that would ban short-haul commercial flights. The ban would prohibit any flights that cover less than the distance that can be travelled by train in less than 2.5 hours.

Related to the virus, US infections are rising again after plateauing at a level above the fall level. The totals have risen to 31,918,601 confirmed cases and deaths are now at 575,829. The number of new cases has ticked higher again to an average of 68,071 new cases per day. However, new deaths are trending down again, now at 755 per day. After another a week of a record number of vaccinations, including a record 4.6 million on Saturday alone, the country will have to deal with an 86% reduction in JNJ vaccine as the company has suffered manufacturing and regulatory clearance of their Baltimore facility. MI continues to be in crisis as the latest surge of cases and hospitalization caused by variants is hitting younger and healthier people in that state.

Globally, the numbers rose to 136,734,096 confirmed cases and the confirmed deaths are now at 2,951,407 deaths. The trends have reversed and are now trending toward trouble again as we have seen significant upticks recently. The world’s average new cases are rising again (about 17,000 per day increase) and are now at 668,744 per day. Mortality, which lags, is rising again at 11,54 new deaths per day. In India, things have gotten worse with a seventh straight day of record-high new cases. This comes as the government has outlawed the export of vaccine and treatment drug Remdesivir. India is the world’s largest producer of both. In the UK, more restrictions were lifted, allowing non-essential businesses to reopen. In China, the government admitted the country’s covid vaccines are “not highly effective” (contrary to their earlier reports) and that solutions would include more shots, increased dosages, or mixing those vaccines with others that are based on different technologies (such as PFE, MRNA, JNJ, or AZN vaccines).

Overnight, Asian markets were mostly solidly red. The flat exchanges South Korea (+0.12%) and Taiwan (+0.03%) were the lone green for the day. Shenzhen (-2.30%), India (-3.53%), and Shanghai (-1.09%) led the losses. In Europe, markets are mixed but lean to the red side so far today. The FTSE (-0.30%), DAX (+0.15%), and CAC (+0.14%) lead as usual midday based on their size. However, most smaller exchanges are following the FTSE lead. As of 7:30 am, US Futures are all on the red side of flat at this point. The DIA is implying a -0.12% open, the SPY implying a -0.10% open, and the QQQ implying a -0.21% open. Bond yields held steady overnight, but Oil (WTI) is up 1.33% in premarket trading.

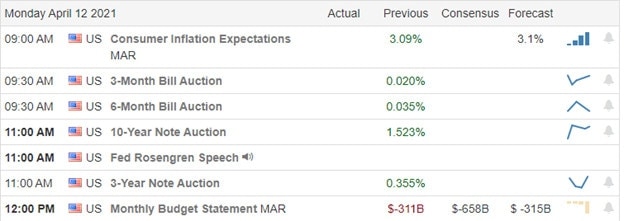

The major economic news scheduled for Monday is limited to the 10-year bond auction (1 pm) and Mar. Federal Budget Balance (2 pm). There are no major earnings reports on the day.

The trend remains bullish as of Monday morning, with all 3 major indices sitting at all-time highs, the Fed Chair predicting blowout economic growth, and no major news scheduled for the day. Yet the rest of the world and US premarkets are showing some concern. With earnings season starting again on Wednesday, we may be in a wait and see environment. So, it would not hard to imagine that markets may might drift today. However, that trend is clearly bullish and those bulls do love new highs.

Respect support and resistance as well as the trend. Don’t predict moves or chase trades you have missed. Keep taking your trade goals (profits) off the table when you can and maintain your discipline. Stay on the right side of the market trend and follow your trading rules. As we know, consistency is the key to long-term trading success.

Ed

Swing Trade Ideas for your consideration and watchlist: No trade ideas for Monday. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Chip shortages are forcing General Motors and Ford to temporarily shut down some American production plants ranging from weeks to several additional weeks in already idle facilities. The Amazon union vote at an Alabama warehouse looks as if it is failing as the vote count widened to deny unionization. Keep an eye on those Treasury yields that are once again pushing higher this morning as inflation worries linger.

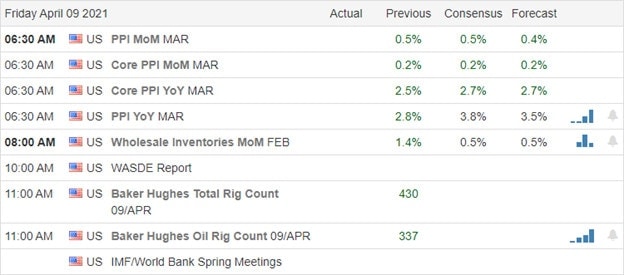

Overnight Asian closed the week mixed but mostly lower as the volatile whips continue in Hong Kong slipping more than 1%. European markets trade mixed with modest gains and loss with German health minister calling for a nationwide lockdown due to the third wave surge in infections. However, after a few days of choppy consolidation, U.S. futures currently point toward a bullish open and more record highs ahead of PPI numbers.

Economic Calendar

Earnings Calendar

We have a very light day as we wrap up the 1st quarter earnings with just 12-companies listed on the calendar with most unconfirmed. The only notable report I see is JKS.

News & Technicals’

Due to chip shortages, GM and F are cutting production at several American plants. The temporary plant closures range from a week to several additional weeks for plants currently idled. In Germany, the health minister is calling for a nationwide lockdown after reporting over 30,000 new infections on Wednesday and 26,000 on Thursday. According to reports, Biden’s China policy is tougher on financial firms than President Trump’s policies. The Cowen Washington Research Group analyst Haret Seiberg says delisting of Chinese companies will happen because Beijing is unwilling to allow the U.S. to inspect company audits. Treasury Yields are bumping higher this morning to 1.666% on the 10-year, with the 30-year rising to 2.343 as inflation concerns linger.

The index charts remain very bullish with no clues in the price action that the bears have any teeth at all. However, traders should note the very extended condition of the current rally and the possible danger if the market were to stumble. That said, it seems every big institution is singing in a chorus that the market boom will continue despite the incredibly high P/E ratios. As for me, I will stay with the trend, but I will also guard myself against complacency and avoid the urge to overtrade due to this very extended market condition. Let’s enjoy the ride while it lasts, but always remember what goes up will eventually come down and likely in a swift and very painful correction. Have a fantastic weekend, everyone!

Markets started the day Thursday in a divergent situation. The QQQ gapped higher by nine-tenths of a percent, with the SPY gapped up a third of a percent, and the DIA opened down just a fraction. From there all three ground sideways with a slight bullish slant the rest of the day. This left all three closing very near the highs and left the SPY as a potential Hanging Man candle at an all-time high close. On the day, the DIA closed up 0.23%, the SPY closed up 0.47%, and the QQQ closed up 1.04%. VXX closed down again to 10.33 and T2122 rose back into the overbought territory at 86.05. 10-year bond yields fell to 1.628% and Oil (WTI) gained slightly to $59.89/barrel.

After hours Fed member Brainard followed the suit of her peers saying that the economy is improving, but is still far from where it needs to be. This echoes the sentiments of discussion that were seen in the March FOMC minutes released earlier in the afternoon. The point repeatedly made is that the Fed will not tighten regardless of short-term inflation, as long as we are not at “full employment.”

In the AMZN union vote in AL, it turns out that the company spent just under $330 million to fight against unionization and only 55% of eligible workers voted (3215 of 5,800). In counting so far, AMZN is winning 1,100 votes to 463, with 500 votes not declared because AMZN has challenged the legitimacy of those votes. The counting process is very slow because each vote is counted by the National Labor Relations Board and can be challenged for everything from whether the person is still employed, if the form was filled correctly, to whether the signature matches company records. In other business news, GM and F both announced more production cuts overnight as the global chip shortage continues to bite manufacturing industries. F says the shortages are likely to cost the company $1.5-$2 billion this year. GM echoed the sentiment, saying their earnings should be off about the same amount due to lost sales.

Related to the virus, US infections are rising again after plateauing at a level above the fall level. The totals have risen to 31,717,404 confirmed cases and deaths are now at 573,856. The number of new cases has ticked higher again to an average of 66,677 new cases per day. However, new deaths are trending down again, now at 775 per day. CA has found 5 more cases of the so-called “double mutant” variant of the virus. This extremely contagious strain is the cause for the recent 55% spike in one province of India (where Mumbai Is located). This strain is less susceptible to antibodies (as generated by previously having the virus or from having a vaccine). So, these cases are a major concern in the San Francisco bay area where the infections have been found. FL also filed a lawsuit against the CDC trying to force the resumption of cruises.

Globally, the numbers rose to 134,641,198 confirmed cases and the confirmed deaths are now at 2,917,995 deaths. The trends have reversed and are now trending toward trouble again as we have seen significant upticks recently. The world’s average new cases are rising again (about 17,000 per day increase) and are now at 618,021 per day. Mortality, which lags, held roughly steady at 10,376 new deaths per day. The EU’s vaccine chief told reporters on Thursday that the EU is on track to achieve herd immunity (70% of the population vaccinated) by mid-July. However, Germany is edging closer to another lockdown as the Chancellor and most state Premiers have called for another one. In Asia, India had another record number of new cases. Japan also exceeded its self-set warning level and has not declared a fourth wave, but PM Suga did say extra precautions are warranted as the country continues to prepare to host the Olympics in late July.

Overnight, Asian markets were mostly red. Shenzhen (-1.26%) and Hong Kong (-1.07%) led the losses with only Malaysia (+0.61%) and Thailand (+0.48%) managing to stay in the green. In Europe, markets are mixed on very modest moves so far today. The FTSE (-0.11%), DAX (+0.06%), and CAC (+0.25%) are typical of the continent at midday. As of 7:30 am, US Futures are also mixed and flat. The DIA is implying a +0.22% open, the SPY implying a +0.14% open, and the QQQ implying a -0.04% open. Bond yields did rise overnight (currently 1.664%) and Oil is flat.

The major economic news scheduled for Friday is limited to Mar. PPI (8:30 am). However, the preliminary result (lawsuits are likely to follow) of the AMZN union vote is also likely to be announced. The only major earnings report on the day is JKS before the open.

The bulls took control again Thursday, especially in the tech-heavy QQQ. However, both the QQQ and DIA have some resistance close overhead. With earnings season starting again next week and the weekend ahead, it is not hard to imagine that markets might drift sideways today. However, the trend is clearly bullish and the big concern (inflation causing Fed action) seems to have been addressed again by Fed voters themselves.

So, don’t predict or chase trades you have missed. Respect support and resistance as well as the trend. As always, keep taking trade goals (profits) off the table when you can and maintain your discipline. Remember that successful traders are the ones that keep hitting singles and doubles. They are not the traders that are looking to hit a grand slam every time at-bat. So, take your profits when trade goals are met, stay on the right side of the market trend. Be sure to follow your trading rules, because consistency is the key to long-term trading success.

Ed

Swing Trade Ideas for your consideration and watchlist: No trade ideas for Friday. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

According to President Biden, he is now willing to negotiate the corporate tax increase that funds the $2.3 trillion infrastructure bill as the battle in Congress heats up. The IMF is at the same time trying to praise the U.S. for the stimulus spending while also warning the massive debit overhang threatens economic recovery. However, the FED appears unconcerned as they stand fast on their extremely dovish QE policies. As the market searches for inspiration, keep in mind we might have to wait until the kickoff of earnings next Wednesday to break this resting consolidation.

Asian markets mostly rallied overnight, with Hong Kong continuing its volatile swings, closing up more than 1% reversing the day before. European markets are mostly higher this morning, but the gains are pretty modest. Ahead of earnings, Jobless Claims, and another Jerome Powell speech, the U.S. futures currently suggest a flat to modestly bullish open.

Economic Calendar

Earnings Calendar

The Thursday earnings calendar has just ten companies stepping up to report quarterly results. Notable reports include CAG, STZ, LEVI, PSMT, & WDFC.

News & Technicals’

As the battle for the $2.3 trillion infrastructure bill, President Biden says he is now willing to negotiate on the corporate tax increase. The CDC is tracking a Covid variant that is spiking severe cases in younger adults. There are now 52 jurisdictions across the country with and more than 16,000 of the B1.1.7 variant. Fed officials are willing to stand fast on their extremely dovish policies, according to the minutes of the last FOMC committee meeting. Officials indicated that the unemployment rate could fall to 2.2% by year-end, and inflation could run to 2.2% in the process. That said, the ECB says it may begin to reduce its bond-buying in the third quarter of this year. The IMF is now warning the U.S. that the debit overhang and financial vulnerabilities pose a significant threat to the economic recovery while at the same time trying to praise the stimulus efforts. Hmm?

Another day of choppy price action as the market seems to be waiting for some inspiration. I suspect we could have to wait until next Wednesday and the official kickoff of 2nd quarter earnings. However, with Jermone Powell speaking today, it is possible he could get things moving. The question is in which direction? The index trends remain bullish, and there is the apparent desire of the FED and the federal government to keep the new record highs coming. The problem traders face is the challenging price volatility that accompanies these all-or-nothing price swings. Remain vigilant to your trading rules, don’t chase or overtrade but stay with the bullish trend as long as it continues.

Markets were essentially flat on the day as traders continue to rest after the recent strong run. All 3 major indices printed indecisive white candles (Doji or Spinning Top). On the day SPY was up 0.12%, DIA up 0.01%, and QQQ up 0.24%. The VXX fell to 10.49 and T2122 dropped just below the overbought territory at 76.29. The 10-year bond yield climbed to 1.679% and Oil (WTI) fell half a percent to $59.50/barrel.

After hours Fed member Brainard followed the suit of her peers saying that the economy is improving, but is still far from where it needs to be. This echoes the sentiments of discussion that were seen in the March FOMC minutes released earlier in the afternoon. The point repeatedly made is that the Fed will not tighten regardless of short-term inflation, as long as we are not at “full employment.”

Related to the infrastructure bill, Republicans continue to fight anything beyond roads, bridges, and railways being called infrastructure (perhaps oddly, missing was the electricity grid, water systems, and telecom/Internet). Meanwhile, some Democrats are saying they are against raising the corporate tax as far as 28%. The President said Wednesday he isn’t married to 28% and is open to negotiation. Meanwhile, the Treasury Dept. (and Sec. Yellen) says the tax policy that is part of this Infrastructure bill would repatriate $2 trillion in corporate profits currently being hidden abroad. In a related story, Sec. Yellen told the press she believes that the vast majority of developed nations (including the G20) will go along with the idea of a “global minimum corporate tax” that she has proposed. Separately, the Wharton school has said the infrastructure plan (as proposed, not as finalized) would have little if any impact on business investments.

Related to the virus, US infections are rising again after plateauing at a level above the fall level. The totals have risen to 31,637,243 confirmed cases and deaths are now at 572,849. The number of new cases has ticked higher again to an average of 66,271 new cases per day. However, new deaths are trending down again, now at 771 per day. The CDC (and Dr. Fauci, NIH) announced that more and more new cases and hospitalizations are coming from younger demographics and that the main cause appears to be the increase in travel, reduction of restrictions, and the public abandonment of mitigation (masking).

Globally, the numbers rose to 133,830,978 confirmed cases and the confirmed deaths are now at 2,904,226 deaths. The trends have reversed and are now trending toward trouble again as we have seen significant upticks recently. The world’s average new cases are rising again and are now at 600,875 per day. Mortality, which lags, held roughly steady at 10,074 new deaths per day. The Canadian province of Ontario went into lockdown for at least the next 4 weeks as cases and hospitalizations have spiked. In the middle-east, Iran has seen the average number of new cases double in the last week. In Asia, India reported another record number of new cases today. And related to vaccines, several countries announced new restrictions or new pauses in the use of the AZN vaccine, including Australia, Spain, Belgium, and even the UK.

Overnight, Asian markets were mostly green on modest moves. Hong Kong (+1.16%), Australia (+1.02%), and New Zealand (+1.16%) were the biggest winners by far on the day. Only Japan (-0.07%) and Singapore (-0.29%) were in the red. The other exchanges all saw modest moves to the upside. In Europe, a similar story is taking shape as of midday. Denmark (+1.46%) is a dramatic outlier, but the FTSE (+0.38%), DAX (-0.12%), and CAC (+0.42%) are much more typical of the continent. As of 7:30 am, US Futures are mixed. The DIA is implying a flat (unchanged) open, the SPY implying a +0.34% open, and the QQQ implying a +0.90% gap higher.

The major economic news scheduled for Thursday is limited to Weekly Jobless Claims (8:30 am) and Fed Chair Powell speaks at noon. Major earnings reports on the day include CAG and STZ before the open. Then after the close LEVI reports.

Bond yields are down very slightly and Oil is off about 1% overnight. So, the inflation story is in check at least prior to the Jobless Claims number (which is expected to be down significantly). With markets having rested the last couple of days and extension having been relieved to some extent, the bulls may have the wind at their back again today. Regardless, do not fight the tide whether that means picking a reversal or not following the trend.

As always, keep taking trade goals (profits) off the table when you can. Stick with your discipline. Successful traders over the long run are the ones that keep hitting singles and doubles. They are not the traders that are looking to hit a grand slam every time at-bat. So, take your profits when trade goals are met, stay on the right side of the market trend, respect both support and resistance, and don’t chase the moves you missed. Be sure to follow your trading rules, because consistency is the key to long-term trading success.

Ed

Swing Trade Ideas for your consideration and watchlist: ALLY, DRI, ORCL, MRVL, INTC, LB. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

After Monday’s big jobs pop and waiting on the FOMC minutes, the bulls took a siesta yesterday, largely chopping sideways. Though we are likely not learn anything new in the minutes of the last Fed meeting, all eyes will be looking for clues for changes in their extremely dovish stance coming under fire due to inflation worries. With the 2nd quarter earnings season set to begin next week, don’t be surprised to see the choppy price action continue.

Asian markets closed mixed overnight, with the HIS slipping nearly 1%. European markets trade mixed with mostly modest price action across the board. After a decline of 20% in mortgage refinance demand, the U.S. has softened from early morning highs, currently suggesting a flat to modestly bullish open as we wait for the Fed minutes.

Economic Calendar

Earnings Calendar

On the Wednesday earnings calendar, we have just ten companies listed, though several are unconfirmed. Notable reports include LW, MSM, & SCHN.

News & Technicals’

Markets took a siesta yesterday, waiting on the FOMC minutes. According to reports, second-quarter numbers will likely surge, and many believe the Fed will come under considerable pressure for maintaining its extremely dovish stance. Economists expect a 9% growth in the second quarter that could trigger strong inflation concerns. Though I doubt we learn much more than we already know, all eyes will be on the FOMC minutes looking for clues later this afternoon. Jamie Dimon chimed in to let us know that the expected economic boom is fueled by deficit spending. Thank you very much, captain obvious! Jeff Besos says he supports a hike to the corporate tax rate even though Amazon has come under fire for paying very little in taxes over the past years.

Technically speaking, the indexes are in good shape though perhaps a bit dangerous because of the overstretched condition. The QQQ has rallied sharply up more than 8% in just 9-trading days yet still has overhead resistance to overcome. With the softness experienced in the financial sector and energy sector yesterday, the IWM seemed to struggle and now shows us a possible head and shoulder pattern to keep an eye on. Ahead of the FOMC minutes, the 10-year treasuries continue to moderate, but this could be a temporary situation should the second-quarter numbers confirm inflation concerns. Keep in mind with the kick-off of earnings season just a week away, it could be possible to see choppy consolidation price action in the indexes as we wait for the inspiration.

Markets opened flat on Tuesday and then ground sideways the rest of the day with a slight bearish direction. This left all 3 major indices in Doji-type candles. On the day the SPY lost 0.06%, DIA lost 0.25%, and QQQ lost 0.07%. The VXX was flat at 10.77 and T2122 also held ground deep in the overbought territory at 95.57. 10-year bond yields fell significantly to 1.658% during the day and Oil (WTI) gained almost 1.5% to $59.46/barrel.

After hours, LUV called back pilots to prepare for what they expect to be a very busy summer travel schedule. AMZN CEO Jeff Bezos also released a statement saying that he supports a bold infrastructure investment and the raising of the corporate tax rate. However, he stopped short of endorsing President Biden’s specific infrastructure plan or Biden’s proposed corporate tax hike to pay for the plan. (It is worth noting that AMZN paid zero in federal income taxes for 2 years and then only paid $162 million last year on $386 billion in revenue…four one-hundredths of a single percent.)

Bloomberg reported that commodity shipping rates have jumped over 50% so far this year. This includes shipping for various grains, steel, coal, and other dry goods. As of a couple weeks ago, prices were nearing the all-time highs that preceded the pandemic crash in March of 2020. In other strong economic news, JPM Chair Dimon issued a shareholder letter this morning that said he expects strong economic growth to easily continue into 2023. He also said that while stock valuations are quite high, the multi-year boom we are entering may justify those stock prices.

Related to the virus, US infections are rising again after plateauing at a level above the fall level. The totals have risen to 31,560,438 confirmed cases and deaths are now at 570,260. The number of new cases has ticked higher again to an average of 65,582 new cases per day. However, new deaths are trending down again, now at 820 per day. The CDC announced that at least 80% of teachers, school staff, and childcare workers have now gotten at least one dose of vaccine. This came the same day the White House announced that 150 million vaccine doses have been dispensed in the first 75 days of the administration. In addition, as mentioned yesterday, President Biden has moved the deadline forward by two weeks, requiring states to offer vaccine to all US adults by April 19.

Globally, the numbers rose to 133,136,691 confirmed cases and the confirmed deaths are now at 2,889,245 deaths. The trends have reversed and are now trending toward trouble again as we have seen significant upticks recently. The world’s average new cases are rising again (about 10,000 per day) and are now at 599,421 per day. Mortality, which lags, held roughly steady at 9,988 new deaths per day. In South America, Brazil recorded its deadliest day of the pandemic on Tuesday, with 4,195 deaths. Argentina also recorded the highest number of new cases since the pandemic started. Elsewhere, there is better news as Sough Korea approved the JNJ vaccine, Russia gave Pakistan 150,000 doses of the Sputnik V vaccine, and the first patients in the UK have started to receive the newly approved MRNA vaccine.

Overnight, Asian markets were mixed again. Thailand (-1.46%), Hong Kong (-0.91%), and Shenzhen (-0.74%) were the major losers on the day. Meanwhile, Malaysia (+1.37%), India (+0.92%), and New Zealand (+0.70%) led gainers. The rest of the region put in modest moves in either direction. In Europe, we see a similar picture at this point in the day, again on modest moves. The FTSE (+0.80%) is an outlier to the upside, with the DAX (-0.05%) and CAC (+0.10%) being much more typical of the continent. As of 7:30 am, US Futures are pointing to a flat open. The DIA is implying a +0.03% open, the SPY implying a +0.04% open, and the QQQ implying a +0.03% open at this hour.

The major economic news scheduled for Wednesday is limited to Imports / Exports and Fed. Trade Balance (both at 8am), Crude Oil Inventories (10:30 am), and FOMC Meeting Minutes (2 pm). Major earnings reports are limited to LW, MSM, RPM, and SCHN before the open. There are no major reports scheduled after the close.

Overnight trading was mixed and flat following Tuesday (which was the least volatile day so far this year). Bond yield rose slightly (10-year up to 1.66%) and Oil gained a percent again overnight, implying slightly more inflation expectation. However, there was no major move that would signal strength from the bulls or bears. It may just be that Mr. Market needs to catch his breath after running “too far too fast.” Or maybe traders are just waiting for the next reason to run. Regardless, we remain extended, but in a strong bullish trend. So, keep an eye on volatility and don’t fight the tide.

As always, keep taking trade goals (profits) off the table when you can. Stick to your trading rules, and maintain that discipline. Traders that are successful in the long run do it by continually hitting singles and doubles…not by looking to hit a grand slam every time at-bat. So, take your profits when trade goals are met, stay on the right side of the market trend, respect both support and resistance, and don’t chase the moves you missed. Be sure to follow your trading rules, because consistency is the key to long-term trading success.

Ed

Swing Trade Ideas for your consideration and watchlist: No trade ideas today. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service