With Yellen suggesting the higher rates may be on the way to prevent the market from overheating, she created a nasty market whipsaw that produced some technical damage in the QQQ. On the other hand, the DIA bounced strongly enough to set up a new record high for the index if it can follow through today. Unfortunately, that’s been the problem for the last couple of weeks; inability to follow through! With a big day of earnings and private payroll number just around the corner, one has to wonder who it will inspire today? Bulls or Bear?

Overnight Asian markets closed in the red with modest declines across the board. However, European markets are decidedly bullish this morning, with the DAX up more than 1%. Ahead of earnings and jobs data, the Dow futures are trying to add to yesterday’s whipsaw rally, pointing to bullish open. Be careful rushing in until we see some actual follow-through buying. Remember, the pop and drops of late in this wide-ranging consolidation can be very punishing.

Economic Calendar

Earnings Calendar

The hump day earnings calendar is a busy one, with more than 200 companies scheduled to reveal quarterly results. Notable reports include GM, ALB, ABC, GOLD, BKNG, BWA, CERN, CF, CLH, CYBR, EMR, ETSY, FSLY, FOX, GDDY, HLT, HFC, HUBS, KTOS, LNC, LL, MTW, MRO, MET, NYT, NVO, NUS, PYPL, QRVO, QLYS, RLT, RGLD, SMG, SSYS, RGR, RUN, SKT, TRMB, TUP, HEAR, TWLO, UBER, WW, & ZNGA.

News & Technicals’

Janet Yellen spouted off about the need to raise rates to prevent the market from overheating, creating nasty whipsaw intraday. She later clarified that she is not predicting it will need to go up or as to when it will be necessary. Well, thank you very much! If the volatility created cost you some money yesterday, make sure to send her a thank you card. Yellen then said, “We propose to raise the global minimum tax and to close tax loopholes that allow American corporations to shift earnings abroad,” at the Wall Street Journal’s CEO Council Summit. Get ready for global taxation. President Joe Biden set the goal of getting 70% of U.S. adults to receive at least one dose of a Covid vaccine by July 4. The White House will also aim to have 160 million adults fully vaccinated by Independence Day, senior administration officials said. Treasury yields declined yesterday, but this morning ahead of the private payrolls, data have once again started to creep higher. The 10-year traded at 1.605% this morning, and the 30-year edged higher to 2.278%.

Yesterday’s price action produced some technical damage in the QQQ, with the index dropping through support levels of price and current trend. That left behind a somewhat significant price resistance level that the tech sector will now have to overcome. However, the DIA produced a strong bounce-off of price support to create possible new record highs if the index can find the energy to follow through today. The bounce in the SPY was also productive, but it also now has a price resistance level to deal with to move higher. One thing for sure this wide-ranging consolidation filled with chop and whipsaws is challenging and very frustrating. Be careful not to overtrade! Today begin to focus on jobs numbers, the private payrolls, jobless claim on Thursday, followed by the Employment Situation numbers Friday morning. Stay focused and flexible with more than 200 companies reporting and inflation worries and all the talk of higher rates and taxes; there is a lot for the investors to digest. Anything is possible.

Markets gapped down Tuesday and followed through to the downside in the morning, especially in the high-tech-heavy Nasdaq. From that point forward there was a very slow, gradual rally the rest of the day. This left us with gap-down Hammer-type candles in all 3 major indices. Both the large-cap indices remain in the recent range, but the QQQ gapped down below that range. On the day, SPY lost 0.59%, DIA gained 0.11%, and QQQ lost 1.80%. The VXX gained almost 3.8% to 40.21 and T2122 fell out of the overbought territory to 65.48. 10-year bond yields fell significantly to 1.582% and Oil (WTI) rose about 2% to $65.76/barrel.

During the day, Treasury Sec. Yellen told a conference that US interest rates may need to be raised modestly to keep economic growth from overheating after the trillions of dollars in stimulus. However, she followed up quickly by saying these were needed investments and will improve our competitiveness and economic growth in the longer run. Interestingly, while this news was widely publicized immediately, the market did not react strongly to the downside, despite the implied threat of inflation. Nonetheless, afterhours Yellen clarified her remarks saying she was not predicting or recommending a Fed rate hike. Instead, she said was just offering her opinion.

Crypto mania has hit again, this time in Doge as the currency rose 35% Tuesday and is up another 20% in premarket today. The surge in orders has crashed Robinhood crypto trading again this morning. Much of the enthusiasm comes from an Elon Musk tweet touting his appearance on Saturday Night Live on May 8, referring to himself as “The Dogefather.” So, speculators are hoping he will say something on the show that will bring in new buyers of Doge tokens.

Related to the virus, US infections are rising again after plateauing at a level above the fall level. The totals have risen to 33,274,659 confirmed cases and deaths are now at 592,409. The number of new cases has ticked lower again and are back down below the peak level from last summer to an average of 49,396 new cases per day. However, deaths have plateaued again, now at 718 per day. On Thursday, President Biden announced a new national goal that at least 70% of Americans have at least on vaccination shot by July 4 and also to have over half the population (160 million) fully vaccinated by then. This goal anticipates a drop-off in demand for vaccine. However, vaccine reluctance will still be a major hurdle with current vaccination rates down 50% from just 3 weeks ago.

Globally, the numbers rose to 155,061,321 confirmed cases and the confirmed deaths are now at 3,243,519 deaths. The trends have reversed and are now trending toward trouble again as we have seen significant upticks recently. The world’s average new cases continue to rise and is now at the all-time peak and with 805,993 new cases per day. Mortality, which lags, is also rising again at 13,192 new deaths per day. Although India remains the global epicenter, the entire Asian region is feeling the impact of the current surge from variants. In Osaka Japan, ICU beds are at 99% capacity as of Tuesday. Pakistan, Nepal, and Sri Lanka are all also implementing measures to get more oxygen as the wave spreads to their countries.

Overnight, Asian markets were mostly in the red. Thailand (-2.14%) was an outlier, but Japan (-0.83%), Shanghai (-0.81%), and Hong Kong (-0.49%) were typical of the region. However, in Europe, markets are strongly green across the board so far Wednesday. The FTSE (+1.17%), DAX (+1.33%), and CAC (+0.80%) are typical, but some of the smaller exchanges have rallied twice as hard as the majors. It appears the catalyst was business activity (Purchasing Manager’s Index) and good earnings. As of 7:30 am, US Futures are also pointing to the upside. The DIA is implying a +0.17% open, the SPY implying a +0.29% open, and the QQQ implying a +0.50% open.

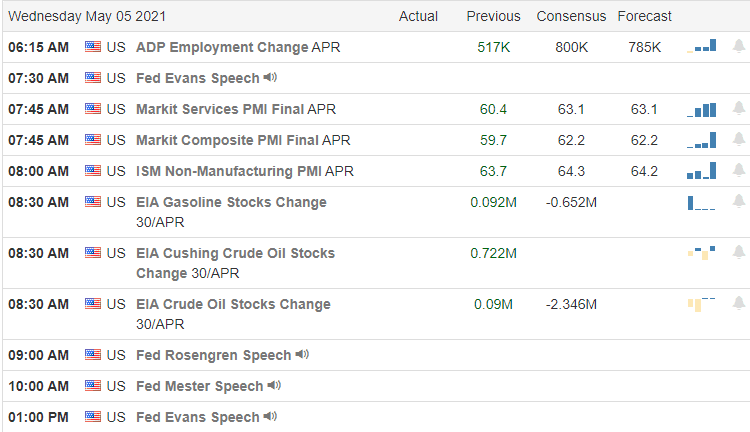

The major economic news scheduled for Wednesday includes ADP Employment report (8:15 am), Services PMI (9:45 am), ISM Non-Mfg. PMI (10 am), Crude Oil Inventories (10:30 am), and 3 Fed speakers (Evans at 9:30 am, Rosengren at 11 am, and Mester at noon). Major earnings reports on the day include ABC, AAQQ, GOLD, BDC, BWA, BRKR, CDW, CERN, CLH, CNHI, DNB, EMR, EXC, FLEX, FTS, GM, HLT, HFC, JLL, NI, ODP, OMI, PSN, PFGC, PNW, PEG, REYN, SMG, SRE, SBGI, SITE, SPR, SGRY, TT, VRTV, WAT, and WRK before the open. Then, after the close, ADT, ALB, APA, ATO, EQH, BKNG, CENTA, CENT, CF, CLW, CTSH, CNDT, CXW, CW, DCP, EC, NVST, EQT, WTRG, ETSY, FLT, FMC, FOXA, GIL, GDDY, HUBG, LHCG, LBTYA, LNC, LUMN, MRO, VAC, MELI, MET, NUS, PTVE, PARR, PYPL, PRI, PRIM, QRVO, RCII, RSG, RKT, RYI, SJI, STN, TRMB, TPC, TWLO, UBER, UGI, UNM, YELL, and ZNGA report.

The bears made a push Tuesday morning but never managed to move the large caps outside of their recent range. Then the bulls mounted a slow, but consistent, rally the rest of the day. This left us well up from the lows and (with the exception of the QQQ) back in the middle of that sideways range. With the way Tuesday ended and the way pre-markets are looking now, it appears the bulls will make the first move today. However, day-to-day chop is still the main characteristic of this market. So, continue to be careful.

Remember, you don’t have to trade every day or every week. Respect potential support and resistance levels. Stick with the trend (when you have one), but also avoid chasing trades you have missed and be nimble. Lock in your profits when you achieve your trade goals and maintain your discipline by following those trading rules. Don’t let your emotions get the better of you. Consistency is the key to long-term trading success.

Ed

Swing Trade Ideas for your consideration and watchlist: RHI, SYF, RIG, WETF, WFC, UEC, XOM, LPX, DHI, DISH. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Yesterday’s surge was a nice start to May, but the ability to follow through and break this choppy consolidation range continues to elude the bulls. With treasuries creeping higher this morning, the tech sector has topped earnings estimates by as much as 20% is struggling to hold price support and a possible double top failure in play. Be careful not to chase or overtrade a dull market because it can quickly chop up an account, leaving you bruised and battered before a direction manifests.

Overnight Asian markets closed mixed but mostly lower as the RBA holds steady on policy. European indexes trade mixed in a session muted with recovery worries. Facing a big day of earnings data as well as trade and factory numbers, U.S. futures currently point to a flat open with tech under slight pressure due to rising bonds. Could it be just another day of choppy consolidation as the market searches for some inspiration?

Economic Calendar

Earnings Calendar

Earnings ramp up this Tuesday with more than 200 companies listed on the calendar set to report quarterly results. Notable reports include UAA, ATVI, ALGT, ANDE, AKAM, ARNC, ANET, BHC, LNG, COP, CMI, CVS, DENN, DVN, D, DD, ETN, RACE, BEN, IT, HSIC, HST, H, IDXX, INCY, INFN, KKR, LPX, LYFT, MPC, MLM, MTCH, MCFE, MTOR, NXST, PFE, PXD, SEE, SU, SYY, TMUX, SPCE, VMC, WMG, WU, XLNX, & ZG.

News & Technicals’

It was a nice start to May with the indexes surging at the open, but sadly they lacked much energy to do much else, chopping sideways to down the remainder of the day. There are some starting to suggest that the market is topping due to the lack of momentum. However, the big instutions continue to sing in unison that this summer will see the indexes higher. Treasury yields advance this morning, with the 10-year at 1.61% and the 30-year moving up to 2.29%. Yesterday gold and silver surged after Warren Buffet said they see a significant rise in inflation as of late. As the CDC tells Americans, they can now freely resume travel around the country; India’s pandemic case total crossed 20 million with more than 345K infections reported yesterday. President Biden has set a deadline to reach an agreement on the infrastructure bill of May 31st as he travels around the country trying to sell the public on the multi-trillion deficit spending plan.

The bulls took a solid run at setting a new Dow record high yesterday but fell short as the tech sector found sellers damping the early enthusiasm. Interestingly the VIX crept slightly higher, and the Absolute Breadth Index moved lower despite the bullish effort. With earnings estimates topped by more than 20%, it makes me wonder what it’s going to take to break this choppy consolidation range. Trends remain bullish, with bonds moving slightly higher this morning, adding a little pressure to the tech sector struggling to hold onto its index price supports. As the morning earnings roll out, futures suggest a flat open with trade numbers and factory order numbers on the horizon. It looks as if the lackluster price action could continue this morning. Plan your risk carefully and avoid overtrading.

Markets gapped up about half a percent Monday to start the new month. However, that was it for the large-caps as they ground sideways in a tight range after the open. The QQQ faded the gap and then some before starting its own tight-range sideways grind about 11am. This left us with indecisive candles in the SPY and DIA and a small Bearish Engulfing candle in the QQQ. However, all 3 major indices remained inside the tight range of the last week. On the day, SPY gained 0.21%, DIA gained 0.64%, and QQQ lost 0.53%. The VXX fell 3.5% to 38.75 and T2122 climbed back to the edge of overbought territory at 80.65. After having climbed in premarket, 10-year bond yields fell during the day to 1.601% and Oil (WWTI) rose over 1% to $64.44/barrel.

After hours, US announced it will pay a $9 million fine to settle an accounting fraud charge. In other legal news, a trial began in WV with local authorities suing the 3 major drug distributors (MCK, ABC, and CAH) for failing to better monitor distribution of opioids as required by federal law. (The companies shipped 36 million doses to a community of 100,000 over an 8-year period.) Also, the AAPL vs Epic Games trial got underway with opening arguments from both sides on Monday. The trial will greatly impact whether AAPL can continue to prohibit alternatives to the AAPL App Store for devices in the APPL device userbase. Epic is arguing the 30% commission and arbitrary app approval process are wrong. AAPL is arguing it needs control because it does not want to devolve into being like the Android marketplace.

PFE reported beats on both the top and bottom lines this morning. The company said it will file for full (non-emergency) approval of its Covid vaccine by the end of the month. If approved, this would allow the company to market the vaccine directly to consumers. UA also posted beats on both lines and raised guidance for the full year. CVS joined the crowd, also beating on revenue and earnings as testing, vaccinations and prescriptions all outpaced forecast.

Related to the virus, US infections are rising again after plateauing at a level above the fall level. The totals have risen to 33,230,992 confirmed cases and deaths are now at 591,514. The number of new cases has ticked lower again and are back down below the peak level from last summer to an average of 50,665 new cases per day. However, deaths have plateaued again, now at 716 per day. In some good news, for perspective, US new cases and deaths are both less than 20% of their peak values in early January of this year. In addition, 40% of adults and 70% of all seniors are now fully-vaccinated. However, the CDC reports that demand for vaccine has also plummeted 27% and each day tens of thousands of available vaccination appointments are going unused daily in the US.

Globally, the numbers rose to 154,241,017 confirmed cases and the confirmed deaths are now at 3,228,632 deaths. The trends have reversed and are now trending toward trouble again as we have seen significant upticks recently. The world’s average new cases continue to rise and is now at the all-time peak and with 812,341 new cases per day. Mortality, which lags, is also rising sharply again at 13,336 new deaths per day. India continues to be the current epicenter of the pandemic with yet another Indian state entering lockdown. This comes as a new tragedy happened Monday, when another hospital ran out of oxygen, causing at least 20 deaths. However, international aid is now starting to arrive (though national logistics is very challenging in the country) and that includes a ramping up of India’s vaccination program which was expanded to everyone over age 18 yesterday.

Overnight, Asian markets were mixed. New Zealand (+1.12%) was an outlier to the upside, with South Korea (+0.64%) and Hong Kong (+0.70%) being more typical of gainers. Taiwan (-1.68%), India (-0.94%), and Japan (-0.83%) paced the losers on the day. In Europe, markets are also mixed so far today. The FTSE (+0.83%) and CAC (+0.75%) are leading the gainers, but the DAX (-0.10%) and a number of the smaller exchanges remain on the red side of flat. Denmark (-0.88%) is an outlier to the downside. As of 7:30 am, US Futures are pointing toward a flat and mixed open. The DIA is implying a +0.05% open, while the SPY is implying a -0.11% open and the QQQ is implying a -0.35% open at this point.

The major economic news scheduled for Tuesday is limited to Mar. Imports/Exports and Mar. Trade Balance (both at 8:30 am), Mar., Factory Orders (10 am), and a Fed speaker (Daly at 1 pm). Major earnings reports on the day include AME, APO, ARCB, ARNC, BHC, BERY, BR, BEP, BG, CWH, CTLT, CRL, CQP, LNG, COP, CMI, CVS, D, DD, ETN, EXPD, RACE, BEN, IT, GPN, HSC, HSIC, IDXX, INCY, INGR, KKR, LCII, LDOS, LGIH, LPX, MPC, MLM, NXST, PFE, SEE, SYY, TRI, UA, UAA, VIRT, VSH, VMC, WMG, WLK, XYL, ZBRA, and ZBH before the open. Then, after the close, ATVI, AKAM, ALC, AMCR, AFG, ANDE, ANET, AIZ, BKH, CZR, CTVA, DK, DVN, ENLC, PEAK, HLF, HI, JAZZ, KAR, LYFT, MANT, DOOR, MTCH, MCFE, MCY, PKI, PXD, PAA, PRU, RYAM, SMCI, TMUS, TTEC, VRSK, WU, XLNX, and ZG report.

Markets continue to feel as if the bulls have run out of energy to push higher. However, the bears have no traction either. This leaves us in a tight-range sideways grind. This is a very difficult market to trade as the day-to-day chop crushes traders, even as the indices go nowhere. Even with blowout earnings and generally raised outlooks, the bulls have not been able to run lately. So, be careful on the long side. Still, the trend has not changed direction. We do not have a bearish trend. So, also don’t be too quick to take shorts either. Stuck between the trend and the chop is a tough place to make money.

Remember, you don’t have to trade every day or every week. Respect potential support and resistance levels. Stick with the trend (when you have one), but also avoid chasing trades you have missed and be nimble. Lock in your profits when you achieve your trade goals and maintain your discipline by following those trading rules. Don’t let your emotions get the better of you. Consistency is the key to long-term trading success.

Ed

Swing Trade Ideas for your consideration and watchlist: SHIP, BIG, MDLZ, JNJ, FAST, DHI, NOK. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Though we had a week of blowout earnings, the price action that followed made for a very frustrating week as it chopped sideways with little to no momentum. With the futures once again pushing hard in the pre-market, the question is will this time be different, or will it turn out to be just another pop and drop that we experienced several times over the last couple of weeks? Overall index trends are still bullish but stay focused and flexible with a busy week of earnings ahead.

Asian markets closed in the red across the board overnight with Twain tensions rising and India reeling from pandemic infection rates. However, European indexes trade higher this morning, with the U.K. closed to celebrate their May Day holiday. Here in the U.S., the pre-market pump has begun ahead of a busy day of earnings as well as manufacturing data. Will there be some follow-through or another frustrating whipsaw? Plan your risk carefully.

Economic Calendar

Earnings Calendar

Kicking off the first week of May, we have more than 100 companies reporting quarterly results. Notable reports include AMG, ALK, WEK, APO, CAR, CBT, CHGG, CC, FANG, EL, FN, GPP, IRBT, L, MOS, RMBS, ON, PETS, RBC, RIG, & XPO.

News & Technicals’

Warren Buffett announced his successor, CEO Greg ABEL when he would be no longer man the helm of Berkshire Hathaway. Treasury yields dipped slightly this morning ahead of the manufacturing data, with the 10-year coming in at 1.625% and the 30-year traded flat at 2.298%. The Phillippine secretary of foreign affairs accused Beijing of strainings its friendship with the Philippines. In a Twitter post, Locsin asked China to “get the f— out!” Keep a close eye on this as the war of words escalates with Taiwan clearly in China’s crosshairs. The president will out touring the country trying to sell the infrastructure bill to the public as Congress continues to wangle over the size and scope. As India’s pandemic numbers spike, the U.S. discusses a more comprehensive licensing of vaccines that may waive patent protections. Over the weekend, India reported more than 400,000 daily cases bringing the countries total to nearly 20 million. On Friday, the White House announced that it would restrict travel from India.

There’s no doubt that last week was a confusing and frustrating week of price action as companies report blowout results while the market showed little to no interest. Technically speaking, the bullish trend remains intact though the price action has lingered in a wide-ranging consolidation. For some reason, the pre-market futures appear inspired to get moving this morning, but once again, I feel it’s necessary to suggest caution in case of another pop and drop. Don’t case, instead let’s wait to make sure there is some actual buying after the open with enough momentum to last more than a few minutes. With a big week of earnings and news, stay focused and flexible.

Markets gapped down on Friday. The large-caps then ground sideways in a tight range the rest of the day. Meanwhile, the QQQ faded the gap and then slowly sold off back to the gap price again. This left us with gap-down Doji in the large-caps and a gap-down Inverted Hammer type candle in the QQQ to end the month. On the day, SPY and QQQ both lost 0.66% and the DIA lost 0.48%. The VXX gained 4% to 40.16 and T2122 fell out of the overbought territory back into mid-range at 49.03. 10-year bond yields fell to 1.626% and Oil (WTI) dropped 2.34% to $63.49/barrel.

A few tidbits came out of the Berkshire Woodstock annual meeting. Warren Buffett announced a 20% increase in BRK operating profit while announcing the company share buybacks have and will continue. He also said that stock prices are too high and decried Robinhood as being an enabler of the public’s gambling habits. He says that has led to far too many “short-term bets” and has hurt BRK (such as the way short-term option activity in AAPL hurt the BRK position). He also said when he retires, Greg Abel will succeed him as CEO. Meanwhile, Charlie Munger (Buffett’s number two) decried Bitcoin as “disgusting” and a bane to society.

In misc. news, overnight and in pre-market activity, bond prices rose again. The 10-year yield is up to 1.642%. VZ is considering selling the dog entity it created by merging AOL and Yahoo Finance. Finally, over the weekend GOP Senators said an infrastructure deal is possible and the President seemed to embrace that sentiment although the sides are well over $1 trillion apart.

Related to the virus, US infections are rising again after plateauing at a level above the fall level. The totals have risen to 33,180,441 confirmed cases and deaths are now at 591,062. The number of new cases has ticked lower again and are back down below the peak level from last summer to an average of 50,251 new cases per day. The same is true of deaths, which are trending down again, now at 719 per day. This has led to the lowest weekly aggregate number of deaths so far this year. In great news, new cases have dropped dramatically (17% week-on-week). However, the CDC has reported that vaccinations rates have also plummeted since the JNJ vaccine pause last month and are raising real concern over whether the US will reach herd immunity later than projected or even at all.

Globally, the numbers rose to 153,565,250 confirmed cases and the confirmed deaths are now at 3,218,006 deaths. The trends have reversed and are now trending toward trouble again as we have seen significant upticks recently. The world’s average new cases continue to rise and is now at the all-time peak and with 809,729 new cases per day. Mortality, which lags, is also rising sharply again at 13,366 new deaths per day. India has been reporting more than 400,000 new cases per day (one-third of the global new cases) as of the weekend. Foreign aid (especially oxygen and related equipment) has started arriving, but deaths remain at the highs and one state of the country (the one encompassing New Delhi) has announced a 1-week total lockdown.

Overnight, Asian markets leaned heavily to the red side with just 3 exchanges staying just on the green side of flat. Taiwan (-1.96%), Hong Kong (-1.28%), and Singapore (-1.04%) led the losses. In Europe, just the opposite is true so far today as markets are mostly green. Russia (-0.76%) is the exception to the rule. The FTSE (+0.12%), DAX (+0.61%), and CAC (+0.50%) are typical of the continent. As of 7:30 am, US Futures are pointing to a green open. The DIA is implying a +0.62% gap, the SPY implying a +0.52% gap, and the QQQ implying a +0.29% open.

There is no major economic news scheduled for Monday. Major earnings reports on the day include AMG, CAN, ENBL, EPD, EL, GPRE, ITRI, LDI, ON, and WEC before the open. Then after the close, AWK, AGR, CAR, BWXT, CC, CR, CVI, FANG, FLS, NSP, LEG, MOS, NTR, OGS, QGEN, RBC, REGI, SANM, SCI, RIG, TA, WMB, WWD, and XPO report.

Markets seem poised to start May on a higher open. However, the short-term trend is clearly an indecisive sideways grind for the last couple of weeks. Even with blowout earnings and generally raised outlooks for the coming quarter, the bulls have not been able to run lately. On the other hand, the bears have also been unable to make any headway without bad earnings or a major story to hang their hats on. So, for now, it seems the market is undecided and hard to trade with no trend in place.

Remember that you don’t have to trade every day or every week. That is one of the great benefits of trading as a career. Respect potential support and resistance levels, but don’t just assume they will hold either. Predicting is a sucker’s game. So, stick with the trend, but also avoid chasing trades you have missed and be nimble. Lock in your profits when you achieve your trade goals and maintain your discipline by following those trading rules. Don’t let your emotions get the better of you. Consistency is the key to long-term trading success.

Ed

Swing Trade Ideas for your consideration and watchlist: No trade ideas for Monday. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

As big tech produces historic earning numbers, it has been a puzzling week of lackluster price action. Could the rising bonds and concerns of inflation causing the lack of momentum, or perhaps the significantly elevated P/E ratios causing the problem? Whatever the cause, the price action continues to chop up accounts as it whipsaws in a better than 500-point consolidation range in the Dow. As we enter the last trading day of the month and slid into the weekend, consider your risk carefully.

Asian markets traded lower across the board overnight, with the HSI falling nearly 2%. European indexes trade mainly lower this morning as the Eurozone deals with another pandemic-related recession. After the blowout earnings in AMZN, the U.S. point to a lower open ahead of personal income numbers. Get ready for another day of choppy uncertainty.

Economic Calendar

Earnings Calendar

On the Friday Earnings calendar, reports lighten up, giving us a little break after such a big week of data. Notable reports include ABBV, BCS, CHTR, CVX, CLX, CL, E, XOM, GT, HP, ITW, NWL, PSX, PBI, QSR, GWW, & WY.

News & Technicals’

It’s been a puzzling week with massive earnings beats but a market devoid of the momentum to react to the historic results. Make a person wonder if the saying, sell in May and stay away, will merit this year? According to the European Commission, Apple has abused its dominant position in the distribution of music streaming apps. The stock is indicated lower this morning. Unfortunately, the Eurozone economy has once again slipped into another recession as they deal with the 3rd wave of pandemic lockdowns. Inda reported another new record with over 386,000 new infections in a single day. In April alone, the county has had to deal with 6.6 million new cases, bringing more than 18.76 million cases in total. As the market digests the blowout earnings reports, the 10-year treasury pushed higher to 1.647% with only a slight movement in the 30-year, moving up to 2.31%.

On the index technical front, the SPY managed to set a new record high, but the day’s price action was not exactly confidence building leaving behind a possible hanging man candle pattern on the chart. Overall the trends remain bullish even as the price action continues in a choppy consolidation zone. , With the price action lacking directional momentum and chop zone of more than 500 points in the Dow, it has been a challenging and punishing time for swing traders. Holding longer-term positions in trend stocks have rewarded trader with discipline to hold through the uncomfortable chop. However, the quick, experienced day traders seem to have the upper hand. With the bulk of earnings inspiration behind us, significantly elevated P/E ratios, and the summer doldrums just around the corner, traders should be cautious of overtrading.

Markets gapped higher Thursday on the prior night’s earnings beats from AAPL and FB. Stocks the proceeded to fade the gap and spent the rest of the day working back toward to gap open. This left us with Hanging Man candles in all 3 major indices (white body on DIA and the other two black bodies). However, the SPY was at another all-time high close. On the day, SPY gained 0.62%, DIA gained 0.66%, and QQQ gained 0.36%. The VXX was essentially flat at 38.58 and T2122 fell ever so slightly to 91.05. 10-year bond yields rose to 1.636% and Oil (WTI) rose 1.69% to $64.92/barrel. Copper also reached a 10-year high.

After the close AMZN continued the trend for big tech by smashing expectations with a 44% sales increase for the quarter and earnings that beat estimates by 65% ($15.79 vs $9.54 est. per share). The online retail giant also said they forecast no fall-off in the pandemic-driven surge in sales. However, while TWTR did post slight beats on both lines, they rained on the parade somewhat by posting a miss on user numbers and lower than hoped forward guidance as well as not beating as big as the other big tech names.

Early Friday, the executive arm of the EU opened a new antitrust investigation of the AAPL App Store. This one is based on music platform SPOT complaining about the AAPL license agreements. The EU announced that “the mandatory use of Apple’s own in-app purchase mechanism for apps distributed through the store likely violates EU antitrust regulations.” This adds to AAPL’s antitrust problems with Epic Games having filed suit on the same grounds in the US.

Related to the virus, US infections are rising again after plateauing at a level above the fall level. The totals have risen to 32,983,695 confirmed cases and deaths are now at 588,337. The number of new cases has ticked lower again and are back down below the peak level from last summer to an average of 55,773 new cases per day. The same is true of deaths, which are trending down again, now at 727 per day. This has led to the lowest weekly aggregate number of deaths so far this year.

Globally, the numbers rose to 151,240,576 confirmed cases and the confirmed deaths are now at 3,182,092 deaths. The trends have reversed and are now trending toward trouble again as we have seen significant upticks recently. The world’s average new cases continue to rise and is now at the all-time peak and with 829,052 new cases per day. Mortality, which lags, is also rising sharply again at 13,448 new deaths per day. France announced a 4-step process to end its lockdown with the first step starting on May 19 with a goal of the final lifting happening June 30. Japan reported its highest number of new cases since January as the country tries to prepare for the delayed Olympic games. Following in the steps of PFE, MRNA president said patients using their vaccine will also likely need a booster 9-12mo after completing the second dose. However, in more hopeful news, in India, the first shipments of foreign oxygen-related aid have arrived.

Overnight, Asian markets were red across the board. Hong Kong (-1.97%) and India (-1.77%) paced the losses. The same story seems to be taking shape in Europe so far today. Moves are generally modest, with the smallest moves coming from two of the big 3 exchanges with the FTSE (-0.17%) and DAX (+0.04%), which is the only green on the continent. The CAC (-0.35%) is closer to typical of all the other exchanges. As of 7:30am, US Futures are also pointing to a gap lower. The DIA is implying a -0.49% open, the SPY implying a -0.59% open, and the QQQ implying a -0.75% gap-down open.

The major economic news scheduled for Friday includes Mar. PCE Price Index, Q1 Employment Cost Index, and Mar. Personal Spending (all at 8:30 am), Chicago PMI (9:45 am), and Michigan Consumer Sentiment (10 am). Major earnings reports on the day include ABBV, ALXN, AON, AZN, AVNT, CRI, CHTR, CVX, CLX, CL, XOM, FNMA, GT, HRC, HUN, ITW, IMO, JELD, JCI, LHX, LAZ, LYB, NWL, PSX, PBI, POR, QSR, GWW, and before the open. Then after the close, WES reports.

Despite continued blowout earnings reports from the massive FAANG names, markets seem poised to follow the rest of the world lower on Friday. Maybe this is related to the month-end or weekend news cycle that both are nearly at hand. Regardless, this just reinforces the bulls have had breaking through the recent highs and running free. Yet, the bears still have no shock or major story to hand their hats on. With blowout earnings and increasing forecasts, future inflation seems to be their storyline…and history shows markets rising in infationary times. So, for now, the bears best case would seem to be for a pullback.

Respect those potential support and resistance levels, but don’t just assume they will hold either. Predicting is a sucker’s game. So, stick with the trend, but also avoid chasing trades you have missed and be nimble. Lock in your profits when you achieve your trade goals and maintain your discipline by following those trading rules. Don’t let your emotions get the better of you. Consistency is the key to long-term trading success.

Ed

Swing Trade Ideas for your consideration and watchlist: PM, XLE, AAPL, JPM, MDLZ, JNPR, AA. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Big tech delivers blowout reports as AAPL and FB surge in after-hours trading. Today we will hear from AMZN and TWTR as we roll into the biggest day of earnings so far this quarter. The FED will keep rates low and plans to buy $120 billion in bonds a month, keeping pedal to the metal for the foreseeable future with little to no concern about inflation. The President rolled out plans for nearly $4 Trillion government spending last night, so let’s party like it’s 1999 as long as it lasts.

Asian markets saw bullish gains overnight led by the HIS rising 0.80%, reacting to the FED policy. European markets are mixed but mostly higher as Nokia surges 16%. Ahead of a massive day of earnings and an economic calendar that includes GDP & Jobless Claims, futures point to a substantial gap open. Buckle up it could be a wild day of price action!

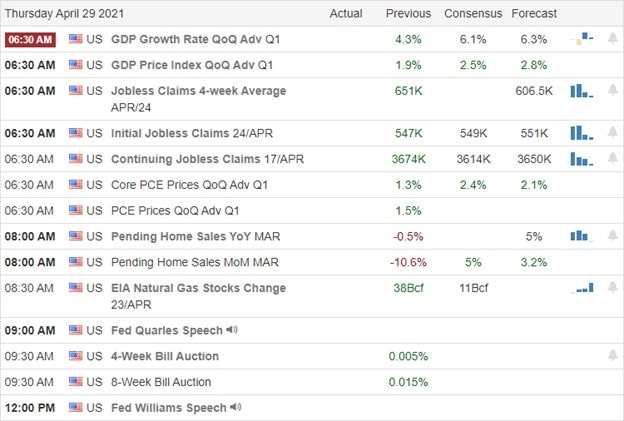

Economic Calendar

Earnings Calendar

Today will be the biggest day of earnings so far this quarter. Notable reports include MCD, AOS, AEM, MO, AMZN, AMT, BAX, BLUM, COG, CARR, CAT, CHD, CRUS, CTXS, CMCSA, CUBE, DVA, DLR, DPZ, ERJ, FSLR, GLPI, GILD, HSY, IP, KDP, KIM, KHC, TREE, LOGI, MMP, MA, TAP, NEM, NIO, NOK, NOC, PFPT, RCL, SWKS, SO, TROW, TXRH, TW, TWTR, X & XEN.

New & Technicals’

Blowout reports from big tech companies AAPL & FB appear to have finally broken the earnings doldrums of the last couple of weeks, with the bulls pushing hard in the future. However, looking forward, AAPL is warning the chip shortages may slow growth looking forward. The President rolled out a massive plan with $2 Trillion on infrastructure and another $1.8 Trillion for families, children, and students! Under his proposal, workers would get 12 weeks of family and medical leave up to $4000 a month. The 10-year treasuries are back up again this morning, climbing to 1.65%, and the 30-year rose to 2.318%. Gerome Powel and the FOMC kept the pedal to the metal, keeping rates near zero with plans to buy $120 Billion in bonds each month.

With futures on the rise this morning, the SPY and QQQ may open at new record highs. Let’s watch carefully to make sure there is some follow-through buying after the open. We don’t want to rush into a pop and drop! The Fed, massive government spending, and big tech earings certainly favor the bulls, and the overall bullish trends with blue skies above show no signs of stopping just yet. Stay with the trend as long as it lasts but let’s not become complacent as P/E ratios continue to stretch to remarkable levels. AMZN and TWTR report after the bell today, so prepare for more price volatility and possible gapping open on Friday.

Markets basically treaded water all day in a tight range. There was a little volatility around the time of the Fed announcement but that quickly faded back to where it was beforehand. It seems like traders were more concerned about the post-market AAPL and FB reports than the foregone conclusion that the Fed would not change rates or their stance. The SPY closed as a Doji again very near all-time highs with the DIA and QQQ putting in small black candles. On the say, SPY gained 0.01%, DIA lost 0.39%, and QQQ lost 0.34%. The VXX was also flat at 38.88 and T2122 remains well into the overbought territory at 92.07. 10-year bond yields fell to 1.611% and Oil (WTI) rose 1.3% to $63.76/barrel.

After the close, FB beat on both the top and bottom line with a 48% rise in revenue but slightly fewer active users than expected. AAPL also announced another blowout quarter with a 54% increase in sales, a 42% profit margin, and in addition authorized a $90 billion share buyback plan. QCOM and F also both announced beats, with QCOM raising guidance on strong smartphone demand. However, F said the global chip shortage and a fire at a Japanese chip supplier will reduce the carmaker’s Q2 production by 50% and also expects that shortage to reduce earnings for the year by about $2.5 billion.

During the afternoon, the Fed raised their outlook for the economy and said inflation will pick up, but they remain unconcerned. However, they did not change rates, reiterated they have no plans to do so and said they will also not stop bond purchases at this time. In the evening, the President spoke before Congress, calling for passage of the Infrastructure plan and unveiling a new $1.8 trillion plan aimed at families, children and students. While neither is likely to pass as proposed, there is no way to look at trillions of dollars of spending that doesn’t consider it fiscal stimulus.

Related to the virus, US infections are rising again after plateauing at a level above the fall level. The totals have risen to 32,983,695 confirmed cases and deaths are now at 588,337. The number of new cases has ticked lower again and are back down below the peak level from last summer to an average of 55,773 new cases per day. The same is true of deaths, which are trending down again, now at 727 per day. In an ominous sign, many parts of the country are now in an urgent rush to find patients for the vaccine they have to deliver. This has been true across the South for some time, but Philadelphia had to plead for patients Wednesday to avoid throwing away unused PFE vaccine and in Detroit the city has resorted to going door-to-door trying to get vaccine used before it expires. That “two alternate universes” point of reference seems as strong as ever (regardless of which one you reside in).

Globally, the numbers rose to 150,341,231 confirmed cases and the confirmed deaths are now at 3,166,947 deaths. The trends have reversed and are now trending toward trouble again as we have seen significant upticks recently. The world’s average new cases continue to rise and is now at the all-time peak and with 827,154 new cases per day. Mortality, which lags, is also rising sharply again at 13,200 new deaths per day. Turkey is starting a national lockdown today amidst a spike in infection rates. In the Philippines, Manilla extended their lockdown through mid-May. However, India remains the center of the pandemic storm with an eighth straight day of over 300,000 reported new cases…reported being the key word. Testing positivity rates are suggesting India may have over 500 million cases at the moment with the majority of hospitals in the country turning away patients for a lack of oxygen, beds, and medical staff.

Overnight, Asian markets were mostly green with South Korea (-0.23%) being the only red on the board. Hong Kong (+0.80%) and Thailand (+0.87%) led the gains on modest moves. In Europe, a similar situation is taking shape. Only the DAX (-0.50%) is in the red with the FTSE (+0.68%) and CAC (+0.43%) being more typical of the continent. As of 7:30 am, US Futures are pointing to a gap higher at the open. The DIA is implying a +0.37% open, the SPY implying a +0.68% open, and the QQQ implying a +1.04% gap higher at this point.

The major economic news scheduled for Thursday includes Q1 GDP and Weekly Jobless Claims (both at 8:30 am), Mar. Pending Home Sales (10 am), and 2 Fed speakers (Quarles at 11 am and Williams at 2 pm). Major earnings reports on the day include AOS, AGCO, ATI, ADS, AB, MO, AMT, AIT, BAX, BCE, BGCP, BLMN, BMY, BC, CG, CARR, CAT, CBRE, CHD, CTXS, CMS, CFX, CMCSA, COWN, DISH, DPZ, ERJ, EME, EEFT, FMX, FMCC, FCN, GNRC, GPI, HSY, ICE, IP, JHG, KBR, KDP, KHC, LH, LKQ, MDC, MMP, MKL, MA, MCD, MRK, MDP, TIGO, TAP, COOP, NEM, NOK, NOC, NVT, PH, PATK, PBF, PCG, PPC, PRG, RLGY, SPGI, SPGI, SNDR, SAH, SO, STM, SYNH, TROW, TMHC, TFX, TPX, TXT, TMO, VC, WAB, WST, WLTW, and XEL before the open. Then after the close, ACHC, AMZN, ATR, AJC, TEAM, BZH, BIO, BKCC, COLM, DVA, DLR, EMN, ENSG, ERIE, FSLR, FTNT, FTV, FBHS, GILD, GFF, THG, KMPR, KLAC, LPLA, MHK, NIO, RMD, SKYW, SWKS, SWN, TEX, TXRH, TWTR, X, VRTX, WDC, and INT report.

The flood of blowout results, and more suggested spending are giving the bulls a tailwind so far today. However, the GDP number may raise the fear of inflation later this morning. So, beware of volatility, but stay on the right side of the trend. There has been a ton of good news for bulls lately, even if markets remain extremely high (frothy to use Chair Powell’s word). There certainly has not been a shock or strong case for the bears lately for anything but a pullback at best.

As I’ve said before, predicting reversals is a game that few traders play successfully…and none of them do it successfully for long. So, stick with the trend, but also avoid chasing trades you have missed. Respect those potential support and resistance levels, but that doesn’t mean assuming they will hold. Just lock in your profits or be prepared to watch closely at those levels. As always, keep taking your goals off the table when you achieve them and maintain your discipline by following those trading rules. Don’t let your emotions get the better of you. Consistency is the key to long-term trading success.

Ed

Swing Trade Ideas for your consideration and watchlist: SENS, TLRY, RIDE, NKLA, QS, CRSP, SLV, NUE, VIAC, XLE, AI. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service