Friday brought a welcome relief raising hopes and leaving behind bullish engulfing patterns all over the place. Remember, hammer patterns must be validated with follow-through bullish price action. Soon money will begin to flow from the 1.9 trillion stimulus bill. Still, the question to be answered is can all the newly printed money overcome the consequences of rising inflation concerns as bond yields surge upward. Keep in mind the VIX remains elevated, so expect challenging price action so plan carefully.

Asian markets had a rough overnight session, with the HIS leading the declines closing down 1.92%. Across the pond, European markets trade modestly higher this morning, and the U.S. point to a flat open as investors monitor rising bond rates. Plan for choppy price action as the bulls and bears battle for control.

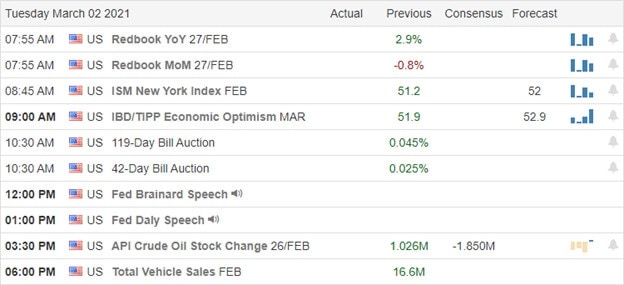

Economic Calendar

Earnings Calendar

On the Monday earnings calendar, we have 65 companies stepping up to report quarterly results. Notable reports include BNFT, CASY, TACO, NCMI, NIU, PVAC & SFIX.

News & Technicals’

Over the weekend, the Senate pass the 1.9 Trillion stimulus bills, and after another vote from the House, the money will begin to flow. While one would expect the market to celebrate, the newly printed money futures seem to be struggling a bit this morning. It turns out the massive printing continues to worry the market about inflation, with the 10-year Treasury yield topping 1.6%. Yemen’s Houthis attacked Saudi oil facilities this weekend, once again raising tensions in the region and pushing crude prices above $70 per barrel. The defense department stated the U.S. would hold accountable those responsible for the rocket attacks against the Iraqi base that hosts American troops.

On the technical front, last Friday’s relief rally left behind a lot of bullish hammer patterns lifting hopes that a market recovery had begun. Although buying the dip has been a good strategy in the past, I’m not sure it will work this time. Keep in mind a hammer pattern requires the price to follow-though to be valid. With rising bond rates spooking investors, can all the government stimulus still overcome the concerns of if it just made it worse? Then we still have the challenge of downtrends as well as overhead price resistance levels yet to overcome. With the VIX still elevated, I expect price action to remain challenging in the week ahead. Watch for overnight reversal and intraday whipsaws as the bulls and bears battle for control. Keep an eye on bonds, as I suspect it will be difficult for the tech sector to bounce back should they continue to rise.

Markets gapped up a percent Friday on a major beat by the Feb. Nonfarm Payrolls (379k vs 182k est.) while unemployment dipped to 6.2%. However, that gap was met with an immediate 2% selloff as fears of inflation resurfaced. Then about 11:30am, the bulls stepped in to defend the lows as bond yields lessened a touch from their highs. This led to a rally that lasted the rest of the day. This left all 3 major indices with long-wicked White-bodied Hammer type candles. On the day, the SPY gained 1.84%, the DIA gained 1.83%, and the QQQ gained 1.51%. The VXX fell 7% to 15.12 and T2122 rose back up to just outside the overbought territory at 77.18. 10-year bond yields spiked again to 1.577% and Oil (WTI) rose almost 4% to $66.28.

The Democratic relief bill hit a few snags on Friday. First, the President had to agree to a reduction from $400/week extended unemployment to $300/week. Then a WV Senator held the bill hostage for several hours related to various unemployment aspects. In the end, the Senate passed the bill Saturday in a 50-49 party-lines vote (one Republican was absent). The bill is now expected to be passed (as amended by the Senate) in the House on Tuesday before being signed by President Biden. The bill gives $1,400 direct checks to those making less than $80,000, extends unemployment at $300/week through September 6 and makes the first $10,200 of unemployment tax free for households making less than $150,000. Even with Senate passage, futures are pointing lower. So, apparently Mr. Market has already baked-in the stimulus and has moved on to other concerns.

After the close Friday, the SEC charged T and 3 of its executives with selectively sharing non-public information about the company’s investments to certain stock analysts. In return, those analysts lowered their earnings estimates to just below the level the company then reported. In other words, the SEC is claiming that T bought an “earnings beat” by giving insider data to certain specific analysts. In other market news, Pot stocks slumped for the second straight week last week. This comes as the partisan nature of Washington is being seen by industry analysts as making it much harder to get national legalization (which many had expected from a Biden administration). And in commodity news, OPEC+ members unexpectedly agreed to keep output restrictions in place. This triggered another rally in oil which now has the price of oil above the balanced-budget required price of three large producing countries. This includes Saudi Arabia, Bahrain, and Oman, with UAE and Kuwait only about $3/barrel from their own break-even prices. This was before Brent topped $70/barrel over the weekend on the OPEC+ restriction extension news.

Related to the virus, US infections are starting to plateau at a level above the fall level after a month and a half of steep and steady decline in new cases. The totals have risen to 29,696,250 confirmed cases and deaths have now passed half a million at 537,838 deaths. As mentioned, the number of new cases fell again to an average of 59,777 new cases per day. Deaths, which have always lagged, also fell again to 1,725 per day. In good news, the US has now hit the milestone of doing over 2 million vaccinations per day. However, Health officials again warned over the weekend that it is too soon to ease social distancing and especially mask mandates.

Globally, the numbers rose to 117,509,784 confirmed cases and the confirmed deaths are now at 2,606,789 deaths. The trends have been good, but we saw a significant uptick today. The world’s average new cases have up-ticked again by 10,000 over the weekend to 399,523 per day. Mortality, which lags continued to tick down slowly, now at 8,715 new deaths per day. Among the places seeing a surge is Brazil, which reports it highest daily increase in new cases in over 2 months.

Overnight, Asian markets were mixed, but mostly red Monday. Shenzhen (-3.24%), Shanghai (-2.30%), and Hong Kong (-1.92%) led the move lower as China bore more most of the brunt of rising oil prices. However, Singapore (+1.90%) gained on that news. In Europe, stocks are green across the board so far today. The DAX (+1.38%) and CAC (+0.88%) are typical of the continent, but the FTSE (+0.21%) lags. As of 7:30 am, US Futures are mixed but generally down. The QQQ is implying a -1.32% open, the SPY implying a -0.49% open, but the DIA remains flat, implying a -0.01% open.

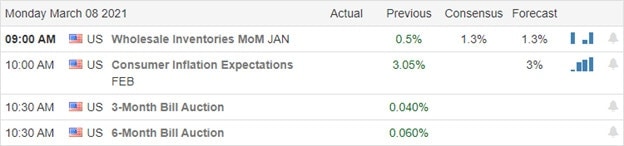

There is no major economic news on Monday. There are also no major earnings reports before the open. However, after the close, CASY and WISH report.

Inflation fears continue to grip Wall Street. Even clearing another major hurdle toward the $1.9 trillion stimulus bill has not helped the weekend mood. It looks as though Friday’s strong day is being answered by the bears pushing back today. The trend remains to the downside, but remember the bulls have recently defended a level not far below. So, volatility is to be expected.

As always, don’t try to predict, just follow the market. It’s the big money that makes the market move and we just need to tag along for the swings. Follow the trend, respect support and resistance, and don’t chase those moves that you miss. Another trade will come along any minute. Keep booking your trade goals when you can and stick with your discipline.

Ed

Swing Trade Ideas for your consideration and watchlist: DFS, DIS, F. XRT, MO, PFE, WMT, LUMN, NLSN, IVZ, MA. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Jerome Powell stepped on a landmine with his inflation comments that raised some uncertainty about future interest rates. Long-term bond yields surged bring out the bears and creating substantial technical damage to the SPY and QQQ index charts. Although it was painful, the DIA and IWM holding at their 50-day averages could be a silver lining, not to mention the massive stimulus bill that’s moving through the Senate. Expect price volatility to continue as we face potential market-moving reports before the bell.

Asian markets had a rough night of volatility but ended the session only modestly lower. European market trade cautiously this morning as they monitor the inflation-sensitive long bonds. U.S. futures recovered from overnight losses, currently pointing to a flat or ever so slight bullish open ahead of the Employment Situation report. With the VIX elevated cinch up your big boy pants for another day of volatility.

Economic Calendar

Earnings Calendar

As we slide toward the weekend, we have a lighter day on the Friday earnings calendar with just 24 companies reporting. Notable reports include BIG, HIBB, & RUTH.

News & Technicals’

Reacting to Jerome Powells inflation comments where he stated the committee would ‘probably’ not raise interest rates, the market plunged sharply. The bears also gained energy as the longer-term treasuries rallied sharply as worried investors ran for the doors. The Senate cleared a hurdle yesterday, paving the way for the next round of stimulus. The hope is to have it completed by mid-March. Before the bell today, we will get the latest reading on the Employment Situation. Economists expect 210,000 jobs were created in February, up from the 49,000 last month but warn we have a long way to go before seeing a substantial employment recovery.

There is no doubt that yesterday’s price action was painful as it reacted to the Powell inflation comments. The majority of the technical damage focused on the tech sector, while the DIA and IWM managed to hold their 50-day averages. With the SPY so heavily weighted with tech giants, it also suffered substantial technical damage closing below its 50-average that now become overhead price resistance. With the VIX closing above 28 handles and turbulent overnight futures trading, expect another rough day price action. Keep an eye on the 10, 20, & 30-year treasury bonds. Should they continue to rise, the bears will likely remain in control. With market-moving economic news before the open, futures are trying to put on a positive face but stay on your toes and be ready for just about anything. Have a wonderful weekend, everyone!

Markets started off with an up-and-down first hour Thursday, but then the bulls rallied us back to the highs. Unfortunately, at noon, while he tried to be dovish, Fed Chair Powell indicated inflation lies ahead. This caused a massive and steep selloff that lasted 2 hours. Bulls were able to pull stocks up off the lows the last two hours, but much of the damage was done. This left all 3 major indices with big, ugly black albeit indecisive (large-wicks) candles. On the day, DIA lost 1.09%, SPY lost 1.23%, and QQQ lost 1.64% (turning negative for the year). The VXX rose over 4% to 16.26 and T2122 fell back into the oversold territory at 12.50. 10-year bond yields spiked on the inflation fears and closed at 1.545% as oil gained almost 5% to $64.24.

The Senate agreed to 20 hours of debate on the $1.9 trillion stimulus bill. However, that time does not start immediately as WI’s GOP Senator Johnson forced clerks to read aloud the entirety of the bill (which will take several hours of in-session time). As of now, the bill is still on track to be passed and then the reconciled bill to be passed in both houses of Congress just in time for a Wed. signature by president Biden. This is the deadline because the previous stimulus bill expires on that day. This said, it will be a razor-thin margin in the Senate and the GOP may have other procedural tricks in addition to Democrats playing hold-out to get favors and pet projects from their own leadership.

Potomac Economics (an independent watchdog group) found that the TX ERCOT power grid left its emergency price of $9,000/kwh in place for 2-3 days longer than their own metrics show it should have been in place. This means that ERCOT overbilled their customers (who passed the costs on to consumers) by as much as $16 billion during the winter freeze. This falls in line with the criticism of ERCOT’s power company customers, the largest of which has already filed for bankruptcy because the financial cost (and two others defaulted on the charges and have been banned from the grid). Since the CEO of the ERCOT grid has already been fired and most of the board has already resigned, it is unclear who will get blamed and how (if at all) things will be put right. However, this is sure to become a political football as soon as the Texas Energy Commission meeting today as politicians try to keep the blame for not adhereing to decades of advice squarely on ERCOT and not of themselves.

Related to the virus, US infections are starting to plateau at a level above the fall level after a month and a half of steep and steady decline in new cases. The totals have risen to 29,526,086 confirmed cases and deaths have now passed half a million at 533,636 deaths. As mentioned, the number of new cases fell slightly again to an average of 64,110 new cases per day. Deaths, which have always lagged, also fell slightly to 1,854 per day. Yet more states are ignoring health experts and loosening their pandemic restrictions. This cuts across party lines as CT is among the latest.

Globally, the numbers rose to 116,322,289 confirmed cases and the confirmed deaths are now at 2,583,546 deaths. The trends have been good, but we saw a significant uptick today. The world’s average new cases has up-ticked again to 388,894 per day. Mortality, which lags continued to tick down slowly, now at 8,853 new deaths per day. In Europe Germany says they are seeing a rise in cases and that 40% are of the UK strain. Italy banned shipping vaccine out of their country and France is considering following suit. In Asia, Japan extended the state of emergency in Tokyo for another 3 weeks. In better news, Australia announced that it has enough AZN vaccine to cover them until domestic production can get ramped up.

Overnight, Asian markets were slightly mixed, but mostly red in modest trading. Malaysia (+1.19%) and Thailand (+0.65%) led to the upside while Australian (-0.74%) and South Korea (-0.57%) led to the downside. In Europe, we see a similar picture so far today. The DAX (-0.59%) and CAC (-0.31%) lead to the downside while the FTSE (+0.38%) and some of the smaller exchanges lead on the green side. As of 7:30 am, US Futures are pointing to a flat open. The DIA and SPY are just on the green side of flat, while the QQQ is just to the red side of break-even. This comes as markets wait for the data dump at 8:30 am.

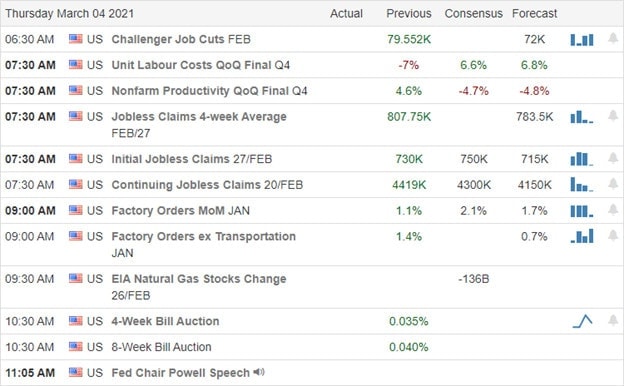

The major economic news for Friday includes Feb. Avg. Hourly Earnings, Imports/Exports, Feb. Nonfarm Payrolls, Feb. Participation Rate, Jan. Trade Bal., and Feb Unemployment Rate (all at 8:30 am), US Federal Budget (2 pm), and a Fed speaker (Bostic at 3 pm). Major earnings reports on the day include BIG and GLP before the open. There are no major earnings reports after the close.

Inflation fear remains in charge on Wall Street. After the ADP miss earlier in the week, look for all eyes to be on the Feb. Employment Report as traders look for any sign of overheating in the economy. That said, the bulls did push us up off the lows late Thursday, so they may be looking to defend a potential support level below. Volatility seems to be the only thing assured in the market now. So, preparedness is the key here.

As always, don’t try to predict, just follow the market. It’s the big money that makes the market move and we just need to tag along for the swings. Follow the trend, respect support and resistance, and don’t chase those moves that you miss. Another trade will come along any minute. Keep booking your trade goals when you can and stick with your discipline. And don’t forget it’s Friday…so take a paycheck off the board too.

Ed

Swing Trade Ideas for your consideration and watchlist: No trade ideas for today. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Although the bulls tried to in the premarket to lift bullish spirits, they ran into a roadblock with declining mortgage applications and a substantial miss on Private Payroll’s. Also, those pesky long-term bonds seem to hang in there stubbornly, adding uncertainty. The tech sector suffered the most significant technical damage failing its 50-day average and closing with a lower low that signals a downtrend. With the VIX rising sharply into yesterday’s close, expect price action to remain quite challenging.

Overnight Asian markets sold off strongly across the board, with tech leading the way. European market trade in the red this morning as they closely monitor the long-term bonds. Ahead of more jobless data, the U.S. futures currently suggest a lower open. Still, as we have seen, anything is possible depending on the investor’s reaction as they digest new data. Hold on tight it could be a wild ride.

Economic Calendar

Earnings Calendar

As usual, the number of earning reports ramp-up on Thursday, with a total of more than 100 companies revealing quarterly results. Notable reports include COST, BALY, BJ, AVGO, BURL, CNQ, CHUY, CIEN, FRGI, GPS, GWRE, KR, MIK, SDC, SWBI, & TTC.

News & Technicals’

Yesterday’s premarket bullish ran into a roadblock after learning that mortgage applications stalled and Private Payrolls registered a substantial decline. We spent the rest of the day with whipsawing price action that ultimately left behind bearish price patterns. The biggest concern is the QQQ failure of its day moving average and making a lower low, signaling a downtrend. Apple is now the target of a government antitrust probe in the U.K., adding to the suffering tech sector’s woes. SpaceX made headlines yesterday after a successful rocket landing of a high-altitude test flight. However, after landing, the rocket exploded.

The technical troubles we now see in the tech sector could make it very difficult for the DIA and SPY to gain headway due to the massive weighting that these tech giants hold in the indexes. While the SPY managed to hold at price support, if the QQQ remains under pressure, the big tech has the weight to pull it under. After failing the 50-day average, we can’t rule out the possibility of a 200-day average could be tested, which means another 10% could be shaved off of the QQQ. Today we face another job number with the Weekly Jobless claims and will follow that up with the Employment Situation number before the bell on Friday. With VIX elevated above 26 handles, be prepared for more gaps and whipsaws to challenge a trader’s skill.

Markets made a small gap-down to open the session Wednesday. However, the bears had the whip in hand all day as inflation fears loomed. Bond yields rose over 8 basis points before settling back. This left us with big, ugly black candles that have either are forming (DIA), have formed (SPY), or have broken out of (QQQ) a Dreaded-h pattern. All 3 major indices closed on the lows. On the day the DIA (buoyed by BA and JOM) lost 0.38%, the SPY lost 1.32%, and the QQQ lost 2.88%. The VXX rose 4.28% and T2122 rose a bit to 39.01, but remains on the lower side of mid-range. 10-year bond yield closed up significantly to 1.469% and Oil (WTI) jumped 2.5% to $61.25/barrel.

After the close, DIS said they are closing 20% of their brick-and-mortar stores in order to shift more focus to e-commerce. President Biden made a concession Wednesday by announcing his support for a reduction in the earnings cap qualification for direct payments. The new number will be $80,000, down from the original $100,000. This would disqualify about 12 million people. This comes as the Senate began debating the bill on Wednesday evening.

AAPL is now facing a new antitrust probe in the UK. This is based on app developer complaints about the Apple app store. Specifically, the 30% fee and long approval process are being challenged. AMZN also made news in the UK, though for better reasons. AMZN opened its first cashier-less retail shop, where customers just pick out their items and leave. The system works on smartphones and an AMZN phone app. An AMZN-backed food delivery service (Deliveroo) also chose London as the location of its first operation.

Related to the virus, US infections have plateaued (after almost 2 months of fall) at a level above the fall level after a month and a half of steep and steady decline in new cases. The totals have risen to 29,456,377 confirmed cases and deaths have now passed half a million at 531,652 deaths. As mentioned, the number of new cases fell just slightly again to an average of 65,322 new cases per day. Deaths, which have always lagged, also fell very slightly to 1,922 per day. President Biden, the CDC, and Dr. Fauci (NIH) all derided states who are lifting restrictions now before the virus and its variants are fully beaten. In the Senate, GOP members are planning “made for TV” testimony sessions that will likely delay a Senate vote until next Wednesday.

Globally, the numbers rose to 115,869,639 confirmed cases and the confirmed deaths are now at 2,573,690 deaths. The trends have been good, but we saw a significant uptick today. The world’s average new cases has up-ticked again to 388,447 per day. Mortality also ticked up again, now at 8,955 new deaths per day. The WHO weighed in to say that after many weeks of falling, the number of cases is ticking up and that variants are to blame. In better news, the UK has now said that like the US, they will fast-track modified versions of vaccines to deal with variants rather than require the full 3-phase trial process. In Germany, the governement finally approved the AZN vaccine for people over 65. And in India, an Indian vaccine (Covaxin) has been found to be 81% effective in trials on almost 26,000 people, based on results from 43 patients. (36 who had gotten the placebo contracted Covid while only 7 who had gotten the real vaccine also contracted Covid).

Overnight, Asian markets were red across the board. Hong Kong (-2.15%), Japan (-2.13%), and Shenzhen (-2.90%) highlighted the losses, but the red was widespread and strong everywhere. In Europe, markets are also in the read all across the continent so far today. Smaller exchanges like Finland (-1.36%) and Belgium (-1.21%) are leading the losses. However, the FTSE (-0.86%), DAX (-0.38%), and CAC (-0.22%) are all headed lower as well at this point in their day. As of 7:30 am, US Futures are pointing to a very modestly red open. The DIA is now implying a -0.14% open, the SPY implying a -0.23% open, and the QQQ implying a -0.23% open.

The major economic news for Thursday includes Weekly Initial Jobless Claims, Q4 Productivity, and Q4 Unit Labor Costs (all at 8:30 am), Jan. Factory Orders (10 am), and Fed Chair Powell speaks (noon). Major earnings reports on the day include BJ, BURL, CNQ, CIEN, GMS, KR, MIK, SRLP, and TTC before the open. Then after the close, AVGO, COO, COST, and GPS report.

Inflation fear still grips Wall Street. While pre-market futures are just shy of flat, we still have a shot of data coming before the open. Also, with Fed Chair Powell speaking again today (I don’t know if he will be taking questions), markets may be waiting on more reassurance that inflations will be ignored the rest of the year. All we know for sure is that despite a pullback of late, we are still not far from all-time highs and the market is seriously worried about the Fed maybe changing course later this year. So, preparedness is the key here.

Follow the trend, respect support and resistance, and don’t chase those moves that you miss. Another trade will come along any minute. So, forget about predicting reversals or breakouts. Just book your trade goals when you can and stick with your discipline. Achieve your ambitions in the long-run by taking short-term trade gains off the board consistantly as they are met, over and over again.

Ed

Swing Trade Ideas for your consideration and watchlist: SQQQ, BIDU, HON, EMR, KHC, KEYS, PFE, EEM. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

The bears found the energy to defend overhead resistance yesterday, leaving behind some dark cloud cover and bearish engulfing patterns overnight. That said, it now looks as if the institutions were setting a bear trap as they began pumping up the futures moments after the closing bell rang. Unfortunately those pesky bond rates are not retreating this morning, and the mortgage applications have stalled as a result. Perhaps like the 21 million unemployed, higher long-term rates no longer matter as long as the government continues to flood the economy with newly printed money.

Asian markets surged higher overnight, with Hong Kong leading the way closing up 2.70%. European markets also have on their bullish caps this morning as they await U.K. budget plans. U.S. futures point to a strong overnight reversal that could create another short squeeze with ADP numbers just around the corner.

Economic Calendar

Earnings Calendar

The number of earnings reports bump up slightly today, with 59 companies expected to fess up to quarterly results. Notable reports include AEO, DLTR, MRVL, OKTA, PDCO, RRGB, SNOW, SPLK, & TCOM, WEN.

News & Technicals’

Although the bulls made several attempts to break overhead resistance levels in the index charts, the bears sustained enough energy to defend and repel each push. However, almost immediately after the close, institutions went to work pumping the futures to trap remaining short sellers this morning with a substantial gap up in play this morning. Twenty and thirty-year bonds retreated ever so slightly yesterday, but this morning yields don’t appear to be cooperating with the bullish sentiment tenaciously holding strong. Perhaps, like the 21 million Americans unemployed, we can add the rising bond rate to the list of things we can ignore and no longer matter as long the government continues to flood the economy with money skyrocketing the debt. The White House says the U.S. will have enough vaccine for all adults by the end of May and has ordered all educators to receive at least one shot by the end of March to get schools reopened.

ON the technical front, resistance levels held yesterday, leaving behind concerning darkcloud cover patterns and even a bearish engulfing pattern on the QQQ closing once again below its 50-day average. Look closely, and the QQQ has the hint of a head and shoulder pattern beginning to develop. That said, it now looks as if the institutions set a bear trap going to work immediately after yesterday’s close, pumping up the futures. Mortgage applications demand number in this morning indicate demand has stalled due to the rising rates, and I would suspect also playing a role is the rapidly rising housing costs. Don’t worry about that, though, because the Fed says there is no inflation. Okay, sorry for the sarcasm. With the ADP report, ISM Services, Petroleum Status, Beige Book, and those pesky bond rates stay on your toes as they try to fire off another morning short-squeeze.

Markets opened modestly higher Tuesday and then roller-coastered all day. However, a selloff the last 45 minutes of the day left all 3 major indices closing near their lows. All 3 printed big ugly black candles, but the QQQ was the sorts of the lot, printing a Bearish Engulfing candle. On the day, SPY lost 0.78%, DIA lost 0.44%, and QQQ lost 1.60%. The VXX only gained nine-tenths of a percent to 14.97 and T2122 fell all the way back down to 30.00. 10-year bond yields fell significantly to 1.405% and Oil (WTI) lost two-thirds of a percent to $59.35/barrel.

Manufacturing data Monday showed that the US economy is exploding (in a good way) even as the $1.9 trillion relief bill is being debated in the Senate and is expected to pass in the next two weeks. The Atlanta Fed real-time GDP estimates are showing that Q1 may exceed even the most optimistic estimates, now estimating Q1 to see at 10% GDP gain. However, not all sectors are in good shape. Mortgage demand fell again as rates rose again to the highest level since last July. In terms of counter-intuitive thinking, this may be bad for markets as traders fear the Fed will have to go back on its word and take a more hawkish stance by the end of the year.

President Biden invoked the Defense Production Act Tuesday and then negotiated an agreement between JNJ and MRK. As a result, MRK will use two of their manufacturing plants to make the JNJ vaccine and the delivery schedule for JNJ vaccine has been accelerated by two full months. In the early evening, President Biden said this will ensure that the US has enough vaccine to vaccinate every American adult by the end of May (versus the old schedule which would have reached that point by the end of July). Obviously this is great news for the economy and theoretically for businesses as well.

Related to the virus, US infections are starting to plateau at a level above the fall level after a month and a half of steep and steady decline in new cases. The totals have risen to 29,370,705 confirmed cases and deaths have now passed half a million at 529,214 deaths. As mentioned, the number of new cases fell slightly again to an average of 66,307 new cases per day. Deaths, which have always lagged, also fell slightly to 1,932 per day. TX dropped all mask and building capacity restrictions Tuesday. On the same day OH, MI, and several southern states also partially eased restrictions. Time will tell if going wide open now is another mistake or not.

Globally, the numbers rose to 115,076,964 confirmed cases and the confirmed deaths are now at 2,552,234 deaths. The trends have been good, but we saw a significant uptick today. The world’s average new cases has up-ticked again to 387,769 per day. Mortality also ticked up, now at 9,041 new deaths per day. In the UK, the latest data shows that even a single vaccination of a 2-dose regimen cuts the risk of hospitalization by 80% in people over 80 years old at least after 3-4 weeks of time for the vaccine to work. The study was only of PFE-BTNX and AZN vaccines. People aged 70-80 got only 61% protection from the PFE vaccine and 73% from the AZN. In Asia, China has now said more that 500 million of their population will have been vaccinated by the end of June.

Overnight, Asian markets were green across the board. Shanghai (+1.95%), Hong Kong (+2.70%), and India (+2.19%) paced the gains. In Europe, markets are mixed, but mostly green so far today. There are some major outliers such as Portugal (-1.74%) and Denmark (-1.41%). However, the FTSE (+0.82%), DAX (+0.90%), and CAC (+0.62%) are more typical of the continent so far today. As of 7:30am, US Futures are pointing to a green open. The DIA is implying a +0.65% gap up, the SPY implying a +0.56% gap up, and the QQQ also implying a +0.56% gap open.

The major economic news for Wednesday includes Feb. ADP Nonfarm Employment (8:15 am), Feb Services PMI (9:45 am), Feb. ISM Non-Mfg. PMI (10 am), Crude Oil Inventories (10:30 am), Fed Beige Book (2 pm), and 2 Fed speakers (Bostic at noon and Kaplan at 6:05 pm). Major earnings reports on the day include DLTR, DY, and PDCO before the open. Then after the close, AEO, CNR, MRVL, SPLK, and TCOM report.

It seems inflation fears (or the lack thereof on some days) have been the major market drivers recently. While pre-market futures look good to the bulls, the stories of a potential blowout GDP for the quarter are likely to strike fear in traders watching the Fed. Without a crystal ball, the best we traders can do is to have a plan with protection in place to handle the volatility of the market jerks one way and then the other. All we know for sure is that we are near all-time highs in a manic market. So, preparedness is the key here.

Follow the trend, respect support and resistance, and don’t chase those moves that you miss. Another trade will come along any minute. So, forget about predicting reversals or breakouts. Just book your trade goals when you can and stick with your discipline. Achieve your ambitions in the long-run by taking short-term trade gains off the board consistantly as they are met, over and over again.

Ed

Swing Trade Ideas for your consideration and watchlist: SPWR, TER, RAD, ROKU. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Although yesterday’s short squeeze was a welcome relief, the bullishness left behind overhead price resistance questions to be addressed. Unfortunately, the long-term treasuries are once again raising some caution that the bears could once again attack. Reports suggest that the rising long-term bonds could soon bring a Fed policy change in an attempt to address the turmoil. Expect challenging price action to continue as the market grapples with bond uncertainty and a big round of retail earnings reports.

Overnight Asian markets saw modest declines across the board after the RBA leaves the cash rate unchanged. However, European markets trade modestly higher with the hope U.S. Bond yields are stabilizing. With a wave of retail earnings reports, a light economic calendar, and an eye on rising bonds, futures currently point to a flat to a modestly lower open.

Economic Calendar

Earnings Calendar

On the Tuesday earnings calendar, we have a big round of retail reporting quarterly results. Notable reports include TGT, AZO, KSS, JWN, ROST, ANF, AER, BGS, BGFV, CHS, DIN, FUBO, HPE, KTB, LL, SE, URBN, & VEEV.

News & Technicals’

Yesterday’s rally was very encouraging, but we still have some resistance above in the indexes charts, and questions yet to answer. According to reports, Fed policy changes could be on the way in an attempt to calm the nerves in the recent bond market rate surge. Apparently, one operation under consideration will dust off the so-called ‘operation twist,’ which would involve the Fed selling short-term bonds and buying up long-term treasuries. That said, 20 and 30-year treasuries are trading higher this morning. President Biden’s first foreign policy challenge may be slipping through his fingers with a former U.S. ambassador saying an Iran nuclear deal is unlikely to happen this year. Tensions continue to escalate amid the recent Syrian airstrikes against Iranian-funded facilities. Elizabeth Warren and Bernie Sanders are now proposing a 3% wealth tax on billionaires that have dubbed the Ultra-Millionaire Tax Act.

After yesterday’s short squeeze rally, the index charts still have the inconvenience of overhead resistance levels blocking the path to new highs. After such a huge short-squeeze rally, a pullback directly after is not a big surprise, but rising long-term treasuries could add a significant complication for the bulls. Though recovering from overnight lows in the morning, pump-up futures indicate a little weakness this morning. So the big question to be answered in the light of stimulus checks just around the corner will the pressure on interest rates bring the bears for another attack? We have a light day on the economic calendar with a significant focus on retail earnings today. Be prepared for the challenging price action to continue.