The Dow set a new record high with a last-minute surge as the dark pool activity consolidated to the market. Both the DIA and SPY are in good technical condition, while the QQQ struggles in a downtrend. With a light day on the earnings and economic calendar, the market may be a bit more sensitive to the news cycle today. According to the VIX, fear is finally declining, but as traders can attest, the wild whipsaws in price action remain challenging. Plan your risk carefully as that condition is likely to continue.

Asian market closed higher in a volatile session with Nomura shares plunging 16% due to a U.S. hedge fund. Credit Suisse is also sliding sharply across the pond as European markets trade modestly higher with the U.K. relaxing pandemic restrictions. The U.S. futures point to a lower open this morning but are well off of overnight lows. Be careful chasing, and don’t be surprised if overnight lows receive a test as support.

Economic Calendar

Earnings Calendar

To kick off the last 3-days of the quarter, we have 69 companies listed on the earnings calendar, with a large number of them unconfirmed. The only verified potential notable report is from CALM.

News and Technicals’

With an end-of-day surge as the dark pool trading consolidated to the market, the DIA reached a new record high, and the SPY cleared some price resistance. President Biden is under pressure considerable pressure with more than 100,000 illegal immigrants crossed the border in February. Biden is also intending to push for the 4 trillion dollar infrastructure plan before moving on to his next phase of health and family care. Let’s hope we don’t run out of ink to keep printing money! A draft study jointly written by the WHO and China says animals are the likely source of the Covid outbreak. While France and Germany face a deteriorating public health situation, the U.K. is relaxing its restrictions allowing up to six people to meet outdoors. According to reports, the massive container ship stuck in the Suez Canal is not partially floated. Still, there is no indication of how long it will take to complete the operation and resume business.

On the technical front, the indexes got a big shot in the arm in the last few minutes of trading. The DIA managed a new record high by a few ticks, and the SPY lept above some concerning price resistance. At the same time, the QQQ lagged, remaining in a downtrend, as did the IWM. After another wild session, the VIX closed below a 19-handle, suggesting fear is diminishing, but clearly, the wild intraday whipsaw continues. In this all-or-nothing market, the T2122 indicator went from an oversold to indicating a possible overbought condition in just two trading days. As the morning pump begins, futures are well off of overnight lows but, as of now, suggest a lower open. I suspect another wild week of price is ready to begin.

The big question of the day, can the bulls follow-through with yesterday’s nice relief rally clearing some of the overhead price resistance? A weak 7-year bond auction has treasury yields ticking higher this morning to worry investors about coming inflation pressures. Additional pressures of the already strained supply chain may factor with the blockage of the Suez Canal that could take weeks to clear. Be careful not to chase or overtrade and remember as the futures pump up the open the pop and drops that occurred all week.

Asian markets caught some seeling relief overnight, seeing green across the board to end the week. European markets are also seeing some modest relief this morning following a better-than-expected global sentiment report. Ahead of possible market-moving economic reports and a light day on the earnings calendar, the bulls are working hard in the futures to continue yesterday’s bounce.

Economic Calendar

Earnings Calendar

On the Friday earnings calendar, we have a light day with 36 companies listed but only a handful of verified reports. There are no notable reports today.

News & Technicals’

Markets enjoyed a nice relief rally yesterday despite some concerning news. North Korea has kicked up its heels again, firing two ballistic missiles increasing the foreign policy challenges for President Biden. A blockage in the Suez Canal is delaying an estimated $400 million in goods every hour, adding worries to an already strained supply chain. Estimates suggest it could take weeks to clear the blockage. Social Media once again came under fire as pressure increases to change laws placing liability on the company for the content posted. I suspect substantial social media changes are on the way.

The challenge for the market today is follow-though with yesterday’s relief rally bounce. The DIA held nicely on its uptrend, and the SPY, through briefly falling below its 50-day average, proved to hold this critical psychological level by the close. As nice as it was to see the bulls fighting back, they still have some substantial overhead resistance hurdles in their path. The 10-year treasury is ticking up this morning to 1.65% after a weak 7-year bond auction. Big tech could continue to struggle with the rising yields and the growing political pressure they face in congress. Futures suggest a bullish open ahead of potentially market-moving economic reports, so be ready for volatility. As we know, the morning pump has created nasty whipsaws in price action this week. Stay focused and flexible.

The large-caps gapped down about four-tenths of a percent and the QQQ gapped down about six-tenths at the open. Then we saw another roller-coaster ride in the QQQ, while the large-caps made a jagged rally most of the day. This left us with a Bullish Engulfing candle in the DIA, and Piercing Candle in the SPY, and an indecisive Spinning Top in the QQQ. On the day, SPY gained 0.56%, DIA gained 0.65%, and QQQ lost 0.17%. The VXX fell 3% to 12.23 and T2122 climbed out of the oversold territory to 38.57. 10-year bond yields rose a bit to 1.631% and Oil (WTI) fell 4.5% to $58.44/barrel, this was odd because Brent fell sharply as the Suez Canal remains shut and 150 ships are already stacked up waiting to traverse (Europe gets most of its oil via tanker that passes through the canal, or takes at least a week longer to go around Africa).

Premarket, Fed Chair Powell told CNBC the obvious, that someday after substantial improvements, the Fed will start becoming less dovish. That plus a significant beat on the Jobless Claims and Q4 GDP fronts was enough to cause the gap-downs. Later, after-hours, the Fed also set the date (June 30) when big banks can begin buybacks and issue larger dividends. However, any bank that fails a stress test must wait until September 30 and would face higher capitalization requirements.

In other business news, the impacts of the global chip shortage continue to spread. Chinese electric car maker NIO is shutting its factory for a week due to the shortage. Congress also slammed the CEOs of FB, TWTR, and GOOG Thursday. This time the attacks were focused on failure to better stop “misinformation” related to election fraud, covid, and vaccines. The CEOs all rejected responsibility, putting the blame on former-President Trump and the general political divide of the country.

Related to the virus, US infections are plateauing at a level above the fall level after a month and a half of steep and steady decline in new cases. The totals have risen to 30,774,033 confirmed cases and deaths are now at 559,744. The number of new cases has ticked-up again to an average of 58,866 new cases per day. However, new deaths are mostly flat at 968 per day. CA, CT, and NC joined the growing list of states that are opening vaccine to all adults. President Biden has raised the goal to 200 million vaccinations within the first 100 days of his administration. This should be achievable as the country is averaging over 2.5 million vaccinations per day and the AZN vaccine is likely to be approved for emergency use soon.

Globally, the numbers rose to 126,193,313 confirmed cases and the confirmed deaths are now at 2,769,455 deaths. The trends have been good, but we saw a significant uptick today. The world’s average new cases are rising again (about 10,000 per day) and are not at 524,097 per day. Mortality, which lags, also ticked up, now at 9,073 new deaths per day. After-hours the EU announced that AZN must meet its vaccine commitments to Europe before being allowed to export any more elsewhere. Likewise, India has banned vaccine exports for the time being. This came as 3 additional regions of France went back into lockdown. In South American, Chile went back into lockdown, Peru recorded its highest number of cases so far, and Brazil reported another record number of Covid deaths Thursday.

Overnight, Asian markets were strongly green, with the lone exceptions of India. Shenzhen (+2.60%), Shanghai (+1.63%), and Japan (+1.56%) led the way. In Europe, markets are also green across the board at mid-day Friday. The FTSE (+0.72%), DAD (+0.75%), and CAC (+0.49%) are typical with a few smaller exchanges up over one percent. As of 7:30 am, US Futures are pointing to a mixed and more muted open. The DIA is implying a +0.32% open, the SPY implying a +0.19% open, and the QQQ implying a -0.19% open at this point of the morning.

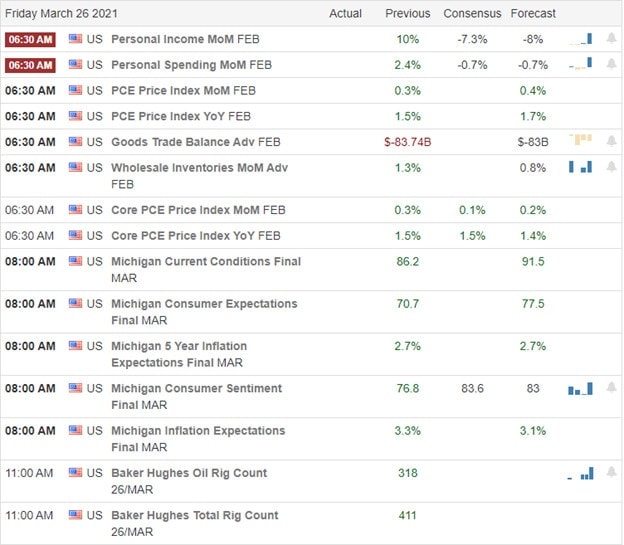

The major economic news scheduled for Friday includes Feb. Goods Trade Balance and Feb. Retail Inventories (both at 8:30 am), Feb. PCE Price Index and Feb. Personal Spending (both at 9:30 am), Michigan Consumer Sentiment (10 am), and US Federal Budget (2 pm). There are no major earnings reports on the day Friday.

Bond yields are up significantly again overnight, now approaching 1.68% on the 10-year. With inflation being the primary focus of the markets lately, that may mean we’ll see another reversal today. In either case, if you were watching the candle signals in the major indices on Thursday, remember that candle signals require follow-through. So, don’t chase reversals without that confirmation. Keep exercising some caution and prudence.

We’ve said it many times. You don’t have to trade every day. Keep your FOMO under control and consider whether you really want to be in that group of traders who’ve had their accounts smacked in the chop of the last couple weeks. Successful long-run trading means accepting that there are times when it’s best to sit on the sidelines. And for me, times when we have a choppy market are at the top of that list. So, follow your trading rules. If you are trading, follow the trend, respect both support and resistance, and don’t chase the moves you missed. As always, consistency is the key to long-term trading success. So, keep taking your trade goals (profits) off the table when you can, stick to your rules, and maintain that discipline. Also remember it’s Friday, so don’t forget to get your account ready for the weekend news cycle and to pay yourself.

Ed

Swing Trade Ideas for your consideration and watchlist: FDX, AN, IDT, OKE, HPE, GSM, SEEL, NUE. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

The reading of chart price action is one of the most important skills in the business of trading. So often we get lost in the indicators, scans and wild gyrations created by news volatility. However, slowing down, putting a little more effort into price action and anyone can Improve their chart reading skills.

Treasury yields are rising this morning after another frustrating whipsaw spanning more than 600 Dow points closing all four indexes lower on the day. Lower highs and broken price support levels in the SPY, QQQ, and IWM should raise caution levels while the DIA continues to enjoy bullish leadership. With the Powell speaking tour behind us, keep a close eye on those treasury yields, and overhead price resistance as the indexes search for direction and momentum.

Asian markets closed mixed overnight, with tech suffering significant losses with the SEC adopting a new law that could delist Chinese companies from U.S. Exchanges. European markets trade modestly red as another pandemic lockdown weighs on investor sentiment. Ahead of the GDP and Jobless Claims futures at trying one again to pump up premarket.

Economic Calendar

Earnings Calendar

The Thursday earnings calendar has 70 companies stepping up to report, but there are many unconfirmed numbers. Notable reports include BLNK, DRI, MOMO, MOV, & CLDX.

News & Technicals’

Treasury yields are pushing slightly higher again this morning, trying to hold onto bullish trends despite the very dovish Fed. AstraZeneca revised its vaccine data, indicating a lower efficacy rate after being called on the carpet for releasing outdated data. The SEC has opened an inquiry into a special purpose acquisition company (SPACs). The SEC is asking banks to provide information voluntarily, but according to the enforcement division, it could be a precursor to a formal investigation. There will be another hearing today in Congress as the CEOs of Facebook, Google, and Twitter face more questions about the spread of misinformation across social platforms. Chinese tech stocks have a rough night after the SEC adopted a law called the Holding Foreign Companies Accountable Act on Wednesday. Companies unwilling to meet the provisions of accounting could be de-listed from U.S. stock exchanges.

Yesterday proved to be another disappointing whipsaw that covered more than 600 Dow points. Although the technical damage is not severe except in the tech sector, investor confidence is taking some damage as the wild swings continue to chop up trading accounts. That said, the futures are once again working to pump up today’s open even after a rough night for Asian markets and a very cautious start in European indexes. As long as traders are willing to chase the moring pump, there is no reason it can’t continue. Swing and position traders I likely finding this price action very frustrating, while experienced day traders are likely having a field day with the huge whipsaws. We are finally past the Powell speaking fest but face the potential market-moving economic reports of GDP and Jobless Claims before the open. Remember, one of the great thing about being a trader is that we can choose to stand aside protecting our capital when feel you have no edge. Just because the market’s open does not mean you have to put money at risk. Ask yourself, are you addicted to risk, or does your action constitute a good business decision?

Markets gapped up about four-tenths of a percent Wednesday. At that point, the large-caps roller-coastered sideways until early afternoon. However, the QQQ started a jagged selloff that lasted over the same period. Then all three major indices synced-up and sold off the entire afternoon, closing on the lows. This left the DIA in a black Inverted Hammer candle and the other two major indices just as big, ugly black candles. That said, all 3 remain in the recent range and still not far from all-time highs. So, we’re still just in the chop. On the day, the SPY lost 0.51%, the DIA was flat at +0.01%, and QQQ lost 1.69%. The VXX gained a bit under 1% to 12.61 and T2122 fell again, now well into oversold territory at 10.57. 10-year bond yields fell again to 1.608% and Oil (WTI) came back over 5.4% to $60.90/barrel.

During the day the big “reopening” plays (such as travel-related stocks) took a hit when the CDC said that cruise restrictions will remain in place until at least November 1. The new surges in Europe, Asia and South America may also have dampened outlooks. Still, it was the big tech names that led the fall with mega-cap FAANG names taking a big hit. As was expected, not much real news came from the second day of testimony by Treasury Sec. Yellen and Fed Chair Powell. However, Yellen did say she supports the Fed decision to allow big banks to do stock buybacks and that the bigger banks look healthier now than when the Fed had previously blocked buybacks. This led to a clash between her and Senator Warren over BlackRock, which Warren wants to be classified “too big to fail” and regulated more tightly.

The SBA says it will triple Covid recovery loans (maximum $150,000) starting April 6. On the opposite side of the coin, after hours, AAL terminated its government loan after raising $10 billion by selling bonds. In related news, JBLU is calling back more flight attendants as travel is picking up again.

Related to the virus, US infections are plateauing at a level above the fall level after a month and a half of steep and steady decline in new cases. The totals have risen to 30,704,292 confirmed cases and deaths have now passed half a million at 558,422 deaths. As mentioned, the number of new cases has ticked-up again to an average of 58,269 new cases per day. However, new deaths are mostly flat at 999 per day. A study of 1,100 discharged patients has found that 70% of people that were hospitalized for COVID-19 had not fully recovered even 5 months after release from the hospital. The CDC reported that it is encouraged by the pace of increase in vaccinations, but is worried about the pace of restriction-easing and poorly-behaving crowds such as large groups of Spring Breakers congregating to party as well as the up-tick in cases. AZN also revised its data reported to the CDC, lowering their efficacy claim to 76% from 79% after being challenged on the timeliness and accuracy of the data.

Globally, the numbers rose to 125,542,273 confirmed cases and the confirmed deaths are now at 2,758,757 deaths. The trends have been good, but we saw a significant uptick today. The world’s average new cases are rising again (about 10,000 per day) and are not at 513,085 per day. Mortality, which lags, also ticked up, now at 9,046 new deaths per day. Germany made the surprise announcement to reverse course and open up the country over the Easter holiday weekend. Elsewhere in Europe, the EU has changed its laws to allow it to block export of vaccines (particularly PFE-BTNX and AZN). This comes as AZN is behind in shipments to the EU and the UK has not exported any vaccine to the EU.

Overnight, Asian markets were mixed again. Japan (+1.14%) was by far the largest gainer with India (-1.54%) seeing by far the largest loss. Most of the region saw small to moderate moves in either direction. In Europe, markets are also mixed, but lean heavily red on modest trading so far today. The FTSE (-0.22%), DAX (-0.21%), and CAC (-0.19%) are typical, with some smaller exchanges remaining green. As of 7:30 am, US Futures are pointing to an open just on the green side of flat. The DIA is implying a +0.06% open, the SPY implying a +0.08% open, and the QQQ implying +0.07% open.

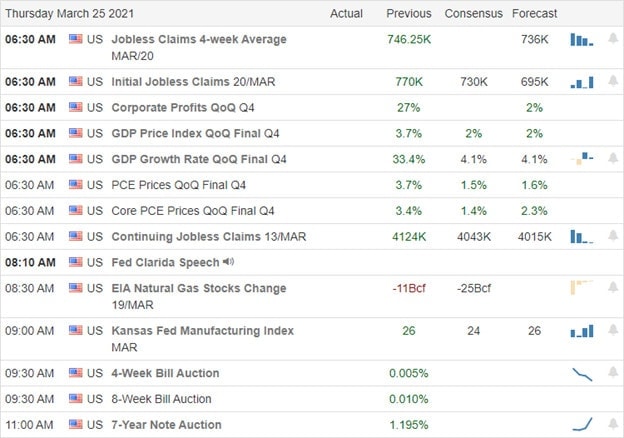

The major economic news scheduled for Thursday includes Q4 GDP and Weekly Initial Jobless Claims (both at 8:30 am), and a number of Fed speakers (Williams at 5:30 am, Clarida at 10:10 am, Bostic at noon, and Daly at 7 pm). Major earnings reports before the open include ARKO, DOOO, CL, DRI, MOMO, and BTU. Then after the close YY and SAIC report.

With Powell and Yellen testimonies done, for now, all eyes will be watching the Q4 GDP and Weekly Jobless Claims for some direction on how the economy is doing. However, these volatile chopping markets are not likely to take a new trend from that backward-looking data or from the flurry of Fed speakers today. So, continue to watch out for the intraday and intraweek swings we’ve been suffering from recently. Keep exercising some caution and prudence.

As I’ve said before, remember that you don’t have to trade every day. A successful trading for the long run needs to accept that there are times it is best to sit on the sidelines…and for me, times of high chop are at the top of that list. So, if you are trading, follow the trend according to your trading horizon, respect both support and resistance, and don’t chase the moves you missed. Another trade will be along any minute. As always, consistency is the key to long-term trading success. So, keep taking your trade goals (profits) off the table when you can, stick to your rules, and maintain that discipline.

Ed

Swing Trade Ideas for your consideration and watchlist: UBER, TMO, XLNX, KLAC, PYPL, NVDA, SMH, XLK, QQQ, SNPS, MPWR. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Elon Musk says you can now use bitcoin to your new Tesla, and at the same time, a Central Banker calls for more regulation on cryptocurrencies. Hmm. Yesterday’s selling came as worries over pandemic infection rates rise around the country, diminishing hopes of a summer recovery. Unfortunately, the selling added to the technical damage in the index charts. The bulls will have a lot of work ahead of them to recover overhead resistance levels in the SPY, QQQ, and now the IWM. Be careful as this choppy and whipsaw-riddled price action tends to chop up trader’s accounts.

Asian markets retreated overnight, closing red across the board with the NIKKEI and HIS down more than 2%. European markets trade with modest losses across the board as recovery concerns weighs on investors. However, here in the U.S., the premarket futures point to bullish open ahead of earnings, Durable Goods Orders, and another round of Powell testimony. Expect the choppy price volatility to continue.

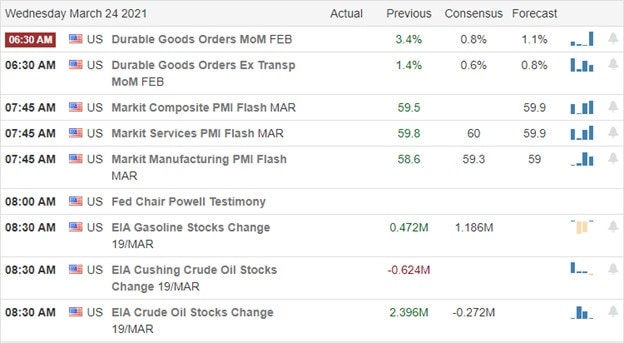

Economic Calendar

Earnings Calendar

On the hump day earnings calendar, we have 53 companies listed, but only half verified they would reveal quarterly results. Notable reports include KBH, GIS, FUL, RH, SCVL, TCEHY, WGO & WOR.

News & Technicals’

You can now buy your new Tesla using bitcoin, but Agustin Carstens from the Bank for International Settlements calls for regulation of what he called a ‘’speculative vehicle’. Interesting considering many central banks are actively exploring their digital currencies. Intel is working hard to get back on top with plans to make chips for other companies and spend 20 billion to build two new chip plants in Arizona. The wildly speculated GME shares fell 12% as the company said it might sell stock to fund a transformation. During the conference call that at one point reached maximum capacity, the company declined to answer any questions. No surprise that the company missed on both the top and bottom line.

Yesterday was a disappointing day in the indexes as the bear returned, adding more technical damage to the charts and essentially reversing the bullish hope of just one day ago. The culprit this time is the rising infections across the U.S. and lockdown in Europe as recovery hopes diminished. However, this morning the bulls are once again trying to pump up the sentiment in the premarket. We have Powell speaking again today, and so far, he seems to have calmed the bond market with his extremely dovish comments. In this choppy market environment, I’ve been hearing from many traders having their accounts chopped to pieces. The super bullish momentum has faded, making this a stock pickers market. Chasing and complacency are very dangerous.

The chop continued as markets opened mildly higher on Tuesday and then proceeded to roller-coaster until 3pm. However, a late day selloff took all three major indices out near the lows. This left us with large black-body candles with upper wicks across the three. On the day, SPY lost 0.79%, DIA lost 0.97%, and QQQ lost 0.44%. The VXX rose over 5.5% to 13.15 and T2122 fell dramatically to 12.50. 10-year bond yields fell to 1.622% and Oil (WTI) fell dramatically (6.5%) to $57.38/barrel.

Treasury Sec. Yellen and Fed Chair Powell had their first of two days of joint testimony on Capitol Hill. They told the House Financial Services Committee that stocks were “elevated,” but that they were not concerned about financial market stability. Powell also stressed that whenever the Fed decides it’s time to dial back asset purchases or other monetary easing measures, they will go slowly and communicate the coming change well in advance of taking action. However, that time is not now and they still want to see more substantial moves toward their goal of full employment.

After the close, INTC said it will spend $20 billion to build two new Fabs in AZ to build chips to compete (selling to other companies) with TSM, which had previously announced it would spend $35 billion to Fab plants in AZ. In the same industry, a week ago SSNNF (Samsung) had also said it would spend $14 billion to build a Fab plant somewhere in the US by 2023. All of these companies are chasing the global shortage of chips. However, there is also the risk that as the industry ramps production to meet pandemic/upgrade-cycle demand, that demand may fall after upgrades are complete and if the economy shifts back away from at-home work. (As always, the risk of a just-in-time supply chain is the inability to adapt to take advantage of surge demand, but excess capacity is dead weight on any company’s books.)

Related to the virus, US infections are plateauing at a level above the fall level after a month and a half of steep and steady decline in new cases. The totals have risen to 30,636,534 confirmed cases and deaths have now passed half a million at 556,883 deaths. As mentioned, the number of new cases has ticked-up again to an average of 57,661 new cases per day. However, new deaths continue to fall to 945 per day (first time below 1,000 since October). In some good news, the CDC reports the US is now administering 2.5 million shots per day of the vaccine. The White House also announced there will be 27 million doses shipped to the states this week (up from 22 million the week before). In other good news, GA, TX, OK, and other states joined the group that will allow all adults to receive the vaccine very soon. In other hopeful, but maybe not good news, more states are easing restrictions which expands the exposure risks.

Globally, the numbers rose to 124,919,952 confirmed cases and the confirmed deaths are now at 2,748,590 deaths. The trends have been good, but we saw a significant uptick today. The world’s average new cases are rising again (about 10,000 per day) and are not at 500,528 per day. Mortality, which lags, also ticked up, now at 8,932 new deaths per day. Germany expanded its lockdown until mid-April as a surge in cases is underway. The WHO reports that cases are rising in many regions as a wave based mostly on variants is underway. Elsewhere, on Tuesday, Brazil reported its highest number of Covid deaths again (breaking above 3,000/day for the first time) and India also reported the most deaths it has seen in 2021. In other bad news, Hong Kong has suspended use of the PFE-BNTX vaccine due to an unspecified packaging defect.

Overnight, Asian markets were mixed again, but leaned strongly red. Japan (-2.04%), Hong Kong (-2.03%), and Shenzhen (-1.47%) led the losses. However smaller exchanges such as Malaysia (+0.45%) and Thailand (+0.42%) managed to stay green. In Europe, markets are following Asia with the larger exchanges in the red and smaller exchanges staying in the green so far today. The FTSE (-0.15%) and CAC (-0.10%) are just on the down side of flat, but the DAX (-0.41%) is picking up steam to the downside at mid-day. As of 7:30am, US Futures are still pointing to a green open. The DIA is implying a +0.42% open while the SPY implies a +0.44% open and the QQ is leading the way implying a +0.82% open.

The major economic news scheduled for Wednesday includes Feb. Durable Goods Orders (8:30 am), Mfg. PMI and Services PMI (9:45 am), Fed Chair Powell and Treasury Sec. Yellen testify (10 am), Crude Oil Inventories (10:30 am), and a couple of other Fed speakers (Williams at 1:45 pm and Daly at 3 pm). Major earnings reports before the open are limited to ESLT, GIS, TCEHY, WGO, and WOR. Then after the close CNCX, FUL, KBH, and RH report.

Powell and Yellen are unlikely to say anything in their statements that were not said to the House yesterday, However, the questions asked and answers given always poses the possibility of news. With inflation being the intense focus of markets recently, there may be more waiting on them to finish (usually early afternoon) in the market today. Either way, watch out for the intraday swings and volatility we’ve been seeing in recent weeks. Exercise some caution and prudence.

Remember that you don’t have to trade every day. Warren Buffett’s first rule of making a lot of money is to not lose a lot of money. In other words, know when it’s best to sit on the sidelines…and for me, times of high chop are at the top of that list. So, follow the trend according to your trading horizon, respect both support and resistance, and don’t chase the moves you missed. Another trade will be along any minute. As always, consistency is the key to long-term trading success. So, keep taking your trade goals (profits) off the table when you can, stick to your rules, and maintain that discipline.

Ed

Swing Trade Ideas for your consideration and watchlist: No Trade Ideas for Wednesday. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

The possible inclusion of outdated data in its vaccine trial has AstraZenica back in the headlines this morning. After a nice relief rally that printed bullish morning star patterns in the SPY and QQQ, U.S. futures now suggest a follow-through to confirm the pattern could see a challenge by the bears. With a joint effort to sanction China by the U.S, EU, UK, and Canada, markets hold their breath, wondering what the Chinese retaliation could entail. Though Powell’s comments softened Treasury yields yesterday, they remain in bullish trends, so keep an eye on them.

Asian markets closed lower overnight after a choppy session, responding to a lackluster Baidu debut in Hong Kong. Across the pond, European markets trade with modest losses across the board as the new lockdown measures shake recovery sentiment. Ahead of earnings, New Home Sales, and another big day of Fed speak, futures markets point to some modest bearish pressure at the open. Stay focused.

Economic Calendar

Earnings Calendar

The Tuesday earnings calendar has 49 companies listed, with 35 verified reports stepping up to quarterly results. Notable reports include GME, CHWY, ADBE, HOME, HUYA, INFO, & SCS.

News and Technicals’

AstraZenica is back in the news this morning but for the undesirable reason that they may have included outdated data in the vaccine trial. This morning, Tesla also has some undesirable news for firing an employee that is part of a whistleblower complaint to the federal safety investigation over solar fires. In a coordinated action, the U.S., EU, UK, and Canada imposed sanctions on Chinese officials on Monday. The countries cited human rights abuses which, of course, China has denied. We wait for the Chinese retaliation that will likely add tensions between the countries with trade ramifications possible.

Yesterday’s rally was a nice relief as the Powell comments softened bond yields. However, the treasuries remain in bullish trends that we will have to keep an eye on due to the market implications. The SPY and QQQ left behind morning star type patterns, but futures markets currently suggest the indexes may have some trouble following-through bullishly due to U.S./China tensions. Selling pressure in the financial sector and energy sector added minor technical damage to the IWM, putting in a possible lower high at price resistance yesterday. Further selling could intensify the concerns today. Keep in mind the SPY, QQQ and IWM now have overhead price resistance that must clear if it is to resume the rally. Stay focused and flexible.

With the third wave of infections expanding across Europe, the country has gone back into lockdown. However, recovery hopes and the massive stimulus are on investors’ minds here in the U.S., with officials monitoring the rising cases in 21 states. With the 10-year treasury softening, perhaps the NASDAQ can gain enough relief to challenge its 50-day average as resistance. Though the DIA, SPY, and IWM left a reason for caution selling-off into Friday’s close, the bulls still control the trends. With Powell speaking three times this week and a busy economic calendar, price volatility is likely to remain high.

Asian markets closed the day mostly lower as the Turkish Lira weakens sharply. European markets are trying to shake off the 3rd lockdown as they chop around the flat-line this morning. U.S. futures are mixed up well off overnight lows as the morning pump begins ahead of Powell and the Existing Home Sale number. Plan carefully and avoid complacency.

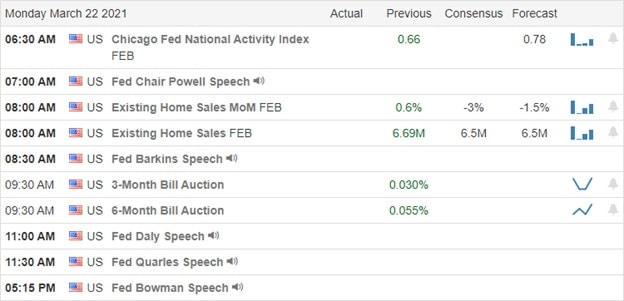

Economic Calendar

Earnings Calendar

Monday, we have 60 companies on the earnings calendar, but only 13 have verified their reports. Notable reports include NEWT, SNX, & TME.

News & Technicals’

As we begin the week, Europe is back under lockdowns as the third wave of infections dash hopes for a spring recovery. Sadly, infections are reportedly rising in 21 states, with officials warnings against reopening too quickly and relaxing masking requirements. Canadian Pacific railway will buy Kansas City Southern for $25 billion if approved by regulatory agencies creating the first rail network connecting the U.S. and Canada. Treasury yields have softened slightly this morning, but according to Jim Bianco say it will not last, expecting they will heat up again in the second half of the year as the U.S. recovers economically.

Although Friday markets found sellers into the close, the DIA, SPY, and IWM are technically in pretty good shape, even though the candle patterns warrant a little caution. The QQQ remains the most technically vulnerable, having failed at a lower high below its 50-day average. Although we got past the FOMC announcement last week, we have a Fed speaker parade, including Jerome Powell Monday, Tuesday, & Wednesday. With Europe back in lockdown, futures are trying to rally off of overnight lows ahead of Powell’s speech and the latest reading on Existing Home Sales.