The substantial point decline yesterday added insult to injury after the bell as Netflix disappointed investors with the substantial decline in subscriber growth. However, consumer staples, utilities, and packaged food-related stocks surged as investors moved to more defensive positions. Technically the QQQ suffered the most damage falling below the price support of the February high. With the sharp NFLX decline, the NASDAQ is vulnerable to more selling as the index seeks price support.

Asian markets had a rough night, with Japan declining another 2%, with Hong Kong not far behind, falling 1.76%. Despite that, the European indexes see green across the board this morning with modest gains. With a big day of earnings and a petroleum number later this morning, U.S. futures have recovered from overnight lows, currently pointing to a flat to a slightly positive open. Prepare for more price volatility as the market reacts to earnings data.

Economic Calendar

Earnings Calendar

On the hump day earnings calendar, we have 66 companies listed to report, but many are unconfirmed. Notable reports include CMG, ANTM, BKR, CP, CHDN, DFS, EFX, GL, HAL, KMI, LRCX, LVS, LAD, NDAQ, NEE, NEP, RHI, RCI, SNBR, VZ, & WHR.

News & Technicals’

After the bell yesterday, Netflix disappointed investors as subscriber growth declined sharply, and adding insult to injury, the company projects that next quarter the trend is likely to continue. A challenging beginning to the big tech reports. After a record of 109 SPAC (Special Purpose Acquisition Company) deals in March, the SEC shut off the pipeline with new accounting guidance. SPAC’s warrants will now receive the classification of liabilities instead of equity instruments. Amazon plans to connect your credit card to a palm print scan payment system in their Whole Foods stores. According to the company, they have already signed up thousands of users to the new technology. The debut of new Apple tech upgrades unimpressed investors yesterday, leaving behind a bearish engulfing pattern on the chart.

Although yesterday’s selling looks relatively benign on the index charts, I suspect it was painful for those not prepared for the substantial point decline. However, as we head into another big day of earnings data, the premarket futures try to put on a brave face recovering from overnight lows despite the big NFLX disappointment. Energy and financial sectors continued to show weakness yesterday as consumer staple and utilities sector stocks surged higher. Also, keep an eye on packaged food and farm-related commodities as California drought concerns and inflation worries push the stocks upward. With only petroleum numbers later this morning on the economic calendar, be prepared for the typically wild earnings price volatility as the market reacts.

Markets gapped down slightly on Tuesday and then followed-through most of the morning before grinding sideways in a tight range the rest of the day. This left us with a black Spinning Top indecisive candle in all 3 major indices on a so-far mild pullback of just over one percent. On the day, SPY lost 0.70%, DIA lost 0.77%, and QQQ lost 0.73%. VXX gained two percent on the day to 10.40 and T2122 fell a bit to 44.30, still in the midrange. 10-year bond yields fell significantly again to 1.562% and Oil (WTI) dropped 1.2% to $62.61/barrel.

After hours, NFLX reported a huge miss on subscriber numbers for Q1, despite a 24% gain in revenue and a strong beat on earnings. AAL also announced plans to begin hiring pilots again as travel continues to pick up. These both may be bellwethers of a market shift into reopening plays. Earlier in the afternoon, AAPL said they will begin enforcing the iPhone privacy changes FB has been fighting as of next week. This morning, GS has upgraded NCLH on the expectation of a resumption in cruises later this year.

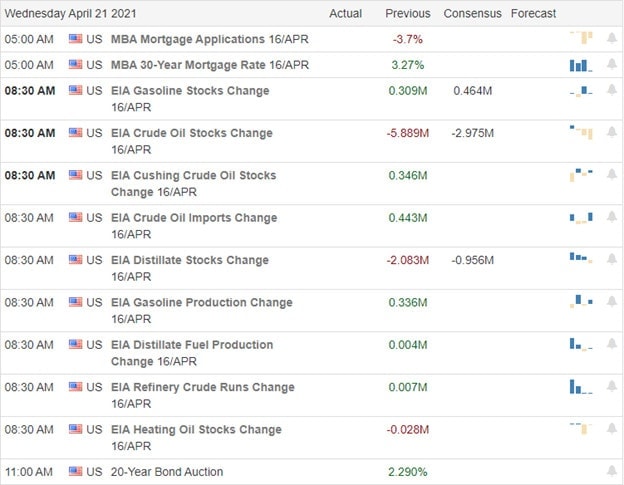

New mortgage demand jumped almost 9% as rates fell to almost a two-month low. This was the first increase in mortgage applications since February. Refinance applications jumped 10%, but remained 23% lower than one year ago.

Related to the virus, US infections are rising again after plateauing at a level above the fall level. The totals have risen to 32,536,470 confirmed cases and deaths are now at 582,456. The number of new cases has ticked higher again and are back above the peak of last summer to an average of 67,151 new cases per day. However, deaths are just starting to plateau again, now at 747 per day. All Americans 16 and older are eligible for vaccination as of Monday. In bad news for JNJ on the PR front, as both the CDC and CNBC reported that the company lied to the public when it claimed that the competing vaccines from PFE and MRNA also have caused clotting issues. JNJ cited a study from Brown University, the lead author of which told CNBC there was no such finding or any problems whatsoever were found for any vaccines other than the one from JNJ.

Globally, the numbers rose to 143,663,051 confirmed cases and the confirmed deaths are now at 3,060,651 deaths. The trends have reversed and are now trending toward trouble again as we have seen significant upticks recently. The world’s average new cases continue to rise and is very near the all-time peak and are now at 789,158 per day. Mortality, which lags, is also rising sharply again at 12,196 new deaths per day. The WHO announced that the world has had more cases this week than any previous week since the beginning of the pandemic. Nonetheless, the Netherlands announced easing restrictions on April 28. JNJ vaccine shipments will resume in the EU, Norway, and Iceland after completion of the European clotting investigation. Meanwhile, in India the situation is getting desperate as the country reported another new high number of cases, hospitals are over capacity and the state containing Mumbai reported at least 22 deaths of people waiting for oxygen as supplies have been depleted.

Overnight, Asian markets were nearly red across the board. The only green in the region was Shenzhen (+0.35%). However, Japan (-2.03%), Hong Kong (-1.76%), and South Korea (-1.52%) were more representative. In Europe, markets are mixed, but lean to the green side so far in the day. Russia (-1.02%) leads the losses, but the FTSE (+0.46%), DAX (+0.24%), and CAC (+0.71%) are more typical of the continent at mid-day. As of 7:30 am, US Futures are pointing to a flat open. The DIA is implying a +0.04% open, the SPY implying a +0.02% open, and the QQQ implying a -0.14% open.

The only major economic news scheduled for Wednesday is Crude Oil Inventories at 10:30 am. Major earnings reports on the day include ANTM, ASML, BKR, ERIC, FHN, HAL, KNX, LAD, NDAQ, NEE, NVR, RCI, TEL, and VZ before the open. Then after the close, CACI, CP, CMG, CCI, EFX, KMI, LRCX, LSTR, LVS, PLXS, RHI, RUSHA, SNBR, STC, UFPI, VMI, and WHR report.

Despite the mild (controlled?) pullback of the last two days, the bears do not seem to have overpowering momentum. This feels like a normal relief pullback in a rally. Certainly the market has been extended on its strong run since the tail-end of March. However, there is a possibile support level just below and if the uptrend has been broken, it was a tightly-drawn trendline for sure. And we definitely have not bult a downtrend (which requires lower highs and lower lows). So, unless you are sure we are now in a bear trend, you might think twice before getting all-in on the short side.

Remember, cash is a valid position. We don’t have to trade every day or week for that matter. Make sure we have a trend and follow it. Do not predict reversals, but also avoid chasing trades you have missed. Respect support and resistance. Keep taking your profits off the table when you can and maintain your discipline. Stay on the right side of the market trend and follow those trading rules. As we know, consistency is the key to long-term trading success.

Ed

Swing Trade Ideas for your consideration and watchlist: GDX, BTG, SSRM, KGC, NUGT. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

It’s time to buckle up and get ready for the volatility that big tech news events can inspire. Apple will reveal its new products later today, and after the bell, Netflix will be the first tech giant to report quarterly results. With indexes so elevated, they will need to report near perfection to support current valuations. With lowered analyst expectations, it’s certainly possible, but traders should prepare for the possibility of substantial morning gaps as the market reacts. Market emotion is high, so plan your risk carefully.

Overnight Asian markets struggled as Japan dropped nearly 2% as China leaves lending rates unchanged. European markets display red across the board this morning, with global markets showing weakening sentiment. Ahead of earnings and the kick-off to big tech reports later today, U.S. futures currently point to a lower open as treasury yields rise.

Economic Calendar

Earnings Calendar

On the Tuesday earnings calendar, we have 35 companies listed, ready to report quarterly results. Notable reports include ABT, AN, CMA, CSX, DOW, EW, FITB, HOG, IBKR, ISRG, JNJ, KEY, LMT, MAN, NFLX, PM, PG, TRV, & XRX.

News & Technicals’

Later today, we have a couple of big tech news events that could have a market effect. First, Apple will roll out new versions of their high-end iPads and maybe even some new tech devices. After the bell, we will get our first tech giant earnings report when Netflix reveals its results. Keep in mind this sets the stage for possible market gaps on Wednesday’s open, which will likely continue as we progress through the tech titan reports. This morning the 10-year Treasury yields perked up to 1.619%, and the 30-year climbed to 2.315%, reacting to the latest earnings results that hint of rising inflation. India reports over 200,000 daily Covid cases for the 6th consecutive day topping over 15 million as hospitals struggle under the increasing pressure. According to the IEA, energy-related carbon emissions will surge by nearly 5% this year as the world Covid recovery begins. The organization is sounding a warning that this surge is unstainable for our climate.

Futures attempted a bounce in overnight trading, but we see a bit of bearishness as we begin another day of potential market-moving earnings reports so far this morning. The SPY and the QQQ look to be the most vulnerable, leaving behind evening star-type candle patterns in very extended market conditions. With price and moving average supports significantly lower, it could be a painful pullback should the bears find inspiration to attack. Thus far, earnings reports have come in glowing positive, but that could negatively affect inflation hawks watch rising treasury yields this morning. Expect the challenging price volatility to continue and even intensify as the risk of significant morning gaps increase as the tech giants begin to report. Stay focused and flexible as anything is possible during earnings season.

With last week’s bullish run, the SP-500 P-E ratio hit 37.5 as earnings top analysts lowered expectations by as much as 22%. Coca-Cola reported this morning topping analysts’ targets as the futures try to rise off of overnight lows. Keep in mind if the bears were to find inspiration, the price support levels in the SPY and QQQ are painfully lower due to their extended condition. Plan your risk carefully and avoid complacency remembering anything is possible as 2nd quarter earnings ramp up over the next couple of weeks. Significant morning gaps are possible.

Asian markets mostly rallied through the India markets plunged as pandemic infection rates continue to surge to severe levels. European markets trade mixed around the flatline as they monitor earnings and global sentiment. As the premarket earnings roll out, the U.S. futures rise off overnight lows but still point to a modestly lower open. Prepare for price volatility to remain challenging in this elevated market condition.

Economic Calendar

Earnings Calendar

We will have a busy week on the earnings calendar as the 2nd quarter earnings season ramps up. Notable reports include ACC, KO, HXL, Ibm, MTB, PLC, STLD, UAL, & ZION.

News and Technicals’

After another very bullish week in trading, the SP-500 P-E ratio hit 37.5, 89% above the historical 10-year average. However, there seems to very little concern about inflation, with the 10-year Treasury yields start the week modestly lower. Trip.com surged more than 4% from their issue price in its Hong Kong debut. According to reports, we reached a pandemic milestone with half of U.S. adults vaccinated with at least one shot. It occurred just one day after the U.S. reported the Covid death toll topping 3 million Americans. China’s CanSino Bilogicis will start clinical trials for a Covid vaccine administered through inhalation though the efficiency rates of China vaccines have much lower effective rates.

The DIA, SPY, and QQQ charts appear highly extended on the technical front, and though the futures indicate a lower open, they are well off of overnight lows as earings roll out. Logically one would expect a significant pullback to begin, but with the lowered analyst expectations, companies thus far have been able to top these targets by nearly 22%. Though many companies are not earning more than they were one year ago, the low expectations and the frenzy of buying something no matter the price could easily continue. However, should the market find a reason to stumble, the pullback could be very painful, so at the risk of sounding like a broken record, avoid overtrading but stay with the bullish trends as long as this party continues to rage.

Markets made a small gap higher at the open Friday and then ground sideways in a flat session to end the week. That left all 3 major indices in indecisive Doji candles, but also closing at new all-time high closes. On the day, QQQ gained 0.12%, SPY gained 0.33%, and DIA gained 0.41%. VXX fell a bit again to 9.81 and T2122 rose slightly further into the overbought territory at 88.82. 10-year bond yields fell again to 1.59% and Oil (WTI) fell half a percent to $63.07/barrel.

On Friday TSM released its annual report saying that trade tensions may well make the global chip shortage worse. Taiwan (particularly TSM) is already stuck between Chinese and American blacklists. However, the company warns that new protectionist measures in the works by both sides are making key chip-making equipment (such as from AMAT) harder to get and is hampering the company’s ability to increase capacity. This report came just days after two Republican members of Congress urged the US to mitigate the risk of using Taiwanese companies as suppliers of technology. TSM is the leading producer of chips in the world, supplying AAPL, AMD, NVDA, Samsung, and many other technology market leaders.

On Saturday the Consumer Product Safety Commission issued an “urgent warning” to consumers that they should stop using the PTON treadmill. PTON responded by saying there is no reason to stop using their machine if safety instructions have been followed. Then Sunday, a TSLA crashed in TX (killing two) apparently operating under the TSLA “Full Self-Driving” autopilot mode (with nobody in the driver’s seat. In better stock news, KO beat on both lines during pre-market and said demand has returned to pre-pandemic levels.

Related to the virus, US infections are rising again after plateauing at a level above the fall level. The totals have risen to 32,404,463 confirmed cases and deaths are now at 581,061. The number of new cases has ticked higher again and are back above the peak of last summer to an average of 68,151 new cases per day. However, deaths are just starting to plateau again, now at 738 per day. The CDC said Sunday that more than half of US adults have received at least one Covdi-19 vaccination dose and one-third of adults are now fully vaccinated. In addition, Dr. Fauci said Sunday he expects a decision on the JNJ vaccine to be made by Friday and he expects the vaccine to go back into use, with a warning label. However, the bad news is that US demand for vaccination is waning.

Globally, the numbers rose to 142,102,302 confirmed cases and the confirmed deaths are now at 3,035,109 deaths. The trends have reversed and are now trending toward trouble again as we have seen significant upticks recently. The world’s average new cases continue to rise and is very near the all-time peak and are now at 760,528 per day. Mortality, which lags, is also rising sharply again at 11,864 new deaths per day. Monday marked the 5th straight day of a record high for new cases in India. In Europe, PFE/BNTX have agreed to supply an extra 100 million does to the EU, including an extra 50 million during Q2 (bringing the Q2 total to 240 million and the grand total to 600 million).

Overnight, Asian markets were mostly green with India (-1.77%), Indonesia (-0.55%), and Malaysia (-0.50%) being the only red. Shenzhen (+2.89%), Thailand (+1.68%), and Shanghai (+1.49%) led the gainers. In Europe, markets are mixed on mostly modest moves so far today. Greece (-2.02%) is a dramatic outlier. However, the FTSE (+0.19%), DAX (-0.04%, and CAC (+0.41%) are typical of the continent. As of 7:40 am, US Futures are pointing to a red open. The DIA is implying a -0.24% open, the SPY implying a -0.26% open, and the QQQ implying a -0.33% open.

There is no major economic news scheduled for Monday. Major earnings reports on the day include KO, MTB, and PLD before the open. Then after the close, CCK, IBM, STLD, UAL, and ZION all report.

The bulls continue to refuse to be denied. Even with bad news for tech darling TSLA over the weekend, it does not seem like the bears have much traction as earnings continue to be blowout positive so far this quarter. On average 85% of the companies that have reported have beat estimates…and are beating by an average of 22%. So, think long and hard before you fight the trend. However, also be leery about this kind of bull run lasting too much longer without relief. Long runs without down days or pullbacks aren’t normal.

Follow the trend, don’t predict reversals, but also avoid chasing trades you have missed. Respect support and resistance. Keep taking your profits off the table when you can and maintain your discipline. Stay on the right side of the market trend and follow those trading rules. As we know, consistency is the key to long-term trading success. Also, remember this is Friday, so prepare for the weekend news cycle, and don’t forget to pay yourself.

Ed

Swing Trade Ideas for your consideration and watchlist: No trade ideas for Monday, but Rick will be back home Monday. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

The Dow topped 34,000 for the first time, and the SPY and QQQ followed with new record highs, and the indexes continue to stretch out. Though 10-year treasuries fell yesterday, they have rebounded slightly this morning, but with no bond auctions until next week, we will have to wait to see the direction of follow-through. Index trends are extraordinarily bullish, but as we extend, the danger of reversal grows, so don’t become complacent or overtrade because the pullback could be rather punishing.

Asian markets closed the day green across the board as China reported economic growth of 18.3% last quarter. European markets are also bullish across the board this morning as earnings inspire the bulls. U.S. futures have recovered from overnight lows, pointing to a modestly bullish open ahead of earnings and housing data. Expect price volatility to remain high, and keep an eye out for possible intraday whipsaws or even reversals if profit-taking picks up heading into the weekend.

Economic Calendar

Earnings Calendar

We have 20 companies listed on the Friday Earnings calendar, but several are unconfirmed. Notable reports include ALLY, BK, CFG, KSU, MS, PNC, & STT.

News & Technicals’

According to the WHO, the Covid infection rate is approaching the highest level so far worldwide. The agency says they will continue to assess the crisis and adjust advice accordingly. Pfizer’s CEO said yesterday that a third Covid vaccine dose within 12 months is likely needed and went on to say it’s possible people will need to get vaccinated annually. Daily U.S. Covid cases remain above 70,000 new infections daily. China says its economy grew 18.3% but was below an expectation of 19%, and their GDP numbers suggest the recovery has already begun to slow down. The 10-year treasury help yesterday’s sharp rally as it pulled back but is slightly rebounding this morning. With on bond auctions today, we will have to wait until next week to see if the slide and follow through.

It has become an almost monotonous phrase in the last year of the U.S. Stock market, but we made new record highs in the DIA, SPY & QQQ yesterday while the IWM lagged. The Dow topped 34,000 for the first time as the indexes continue to stretch in nearly parabolic chart patterns. The bulls found energy as companies blew past expectations and economic data came in much more robust than expected. Analysts have lowered expectations so much that so far this season, reports have topped them by more than 20%. Some might call that manipulation! That said, the trends remain extraordinarily bullish, and there is no reason to believe it can’t continue, so don’t fight the tape. However, traders should avoid overtrading and remain vigilant because as this market continues to extend, the danger of a punishing reversal grows.

Markets gapped higher on blowout March Retail Sales and lower than expected new Jobless Claims. Then we saw a rally the first 90 minutes of the day before grinding sideways in a tight range the rest of the day in all 3 major indices, all closing very near the highs. All 3 indices also closed at new all-time highs. On the day, SPY gained 1.08%, DIA gained 0.86%, and QQQ gained 1.51%. VXX fell another 3.30% to 9.97 and T2122 fell a little, but remains just inside the overbought territory at 82.53. 10-year bond yields fell sharply on the day to 1.569% and Oil (WTI) gained a third of a percent to $63.35/barrel.

On a very small sample size, so far this earnings season companies are far above consensus estimates. Of the 34 that have reported as of day-end Thursday, 88% have beat estimates…and beat them by an average of 22%. Overseas Friday, China has announced that its GDP grew 18.3% in Q1. This may help put the recent Chinese clamp-down on bank lending into context. (Which may correlate to US market fears over Fed action as our own economy is also growing very fast.)

In miscellaneous news, In Thursday’s retail sales report, every segment of retail is now above pre-pandemic sales levels with the lone exception of restaurants. The NFL also picked CZR, DKNG, and Fanduel as their sports-betting partners in a 5-year deal worth about $1 billion. Airlines companies have said they are expecting massive domestic travel rebounds, but DAL, UAL, and AAL are still bearish on international traffic (especially to Europe) returning to pre-pandemic levels this year.

Related to the virus, US infections are rising again after plateauing at a level above the fall level. The totals have risen to 32,224,139 confirmed cases and deaths are now at 578,993. The number of new cases has ticked higher again and are back above the peak of last summer to an average of 71,919 new cases per day. However, deaths are just starting to plateau again, now at 727 per day. There was a lot of bad news on the vaccine front Thursday. During the day, it was made public that the CEO of PFE had told CNBC on April 1 that it is likely people will need a booster shot within 12 months of being fully vaccinated. At the same event the CEO of JNJ had told CNBC that people may well need to be vaccinated against covid annually. CNBC did not say why this news was kept quiet for two weeks afterwards. The CDC also disclosed that 5,800 who had been vaccinated contracted the virus anyway with about 7% of those infected requiring hospitalization and 74 dying. Paired with fear over blood clots and general ignorance/skepticism about vaccines, this does not bode well for a virus that is quick to evolve (mutate). In skepticism front, over 14 million doses have piled up unused, mainly in Southern states such as MS, TN, AR, AL, GA, LA, and MO.

Globally, the numbers rose to 139,809,244 confirmed cases and the confirmed deaths are now at 3,002,313 deaths. The trends have reversed and are now trending toward trouble again as we have seen significant upticks recently. The world’s average new cases continue to rise and is very near the all-time peak and are now at 736,804 per day. Mortality, which lags, is also rising sharply again at 11,592 new deaths per day. The WHO said today that the global infection rate is nearing the all-time high again. In South America, Brazil continues to have a new record number of deaths daily and Columbia has locked-down its 5 largest cities again. In Asia, India again had a record number of new cases amidst a religious pilgrimage festival. Other countries in the region reporting surges are Indonesia, the Philippines, Malaysia, and Cambodia (all of which have instituted some kind of restrictions).

Overnight, Asian markets were green across the board on incredibly strong growth numbers out of China. However, interestingly, the increases in exchanges were moderate with Hong Kong (+0.81%) being by far the largest gainer. In Europe, markets are mostly green on more diverse trading. The CAC (+0.35%), FTSE (+0.50%), and DAX (+0.94%) are typical of the spread across the exchanges of the continent. As of 7:30 am, US Futures are pointing to an open on the green side of flat. The DIA is implying a gain of 0.16%, the SPY implying a gain of 0.10%, and the QQQ implying a gain of 0.03%..

The major economic news scheduled for Friday is limited to Mar. Building Permits, Mar. Housing Starts (both at 8:30 am) and Michigan Consumer Sentiment (10 am). The major earnings reports on the day include ALLY, BK, CFG, KSU, MS, PNC, and STT before the open. There are no earnings reports scheduled for after the close.

The bulls just refuse to be denied it seems. For example, the DIA has not seen a significant black candle this month. So, don’t fight the trend. With the strong news out of China and a lack of much data or reports in the US today, the bears are not likely to have much energy. However, also be leery about this kind of bull run lasting too much longer without relief. Long runs without down days or pullbacks isn’t normal.

Follow the trend, don’t predict reversals, but also avoid chasing trades you have missed. Respect support and resistance. Keep taking your profits off the table when you can and maintain your discipline. Stay on the right side of the market trend and follow those trading rules. As we know, consistency is the key to long-term trading success. Also, remember this is Friday, so prepare for the weekend news cycle, and don’t forget to pay yourself.

Ed

Swing Trade Ideas for your consideration and watchlist: No trade ideas for Friday, but Rick will be back home Monday. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Big bank earnings lifted indexes to new record highs, but the intraday whipsaw left behind some concerning candle patterns as the news-driven price volatility challenges traders. Emotions are very high, and with the flood of inexperienced money that entered the market over the last several months, that is likely to continue. Institutions say this the economic growth in this quarter could rival that of 1984 as we ride the tidal wave deficit fueled stimulus spending. Stay with the trend and enjoy the party as long as it lasts but be warned, the risk is high as the indexes continue to stretch beyond logical limits.

Asian markets traded mixed but mostly lower, struggling for direction. European markets surge to new records as they monitor earnings this morning. U.S. futures point to a substantial gap higher after yesterday’s volatile whipsaw, likely setting new records at the open. I suspect wild price volatility will be with us for several weeks, so plan your risk wisely.

Economic Calendar

Earnings Calendar

We ramp up slightly today on the earnings calendar, with more than 50 companies stepping up to report quarterly results. Notable reports include TSM, AA, BAC, BLK, SCHW, C, DAL, JBHT, PEP, PPG, RAD, USB, UNH, & WIT.

News & Technicals’

The beginning of earings fueled new record highs as the big banks topped expectations, and that trend continues today, with BAC already beating estimates. Besides a busy earnings day, we have an economic calendar chalked full of potential market-moving reports to keep traders and investors busy. Instructions say this could be the strongest quarter of economic growth since 1984, and it would seem that no price is too high as in this stimulus-fueled buying frenzy. President Biden announced that U.S. troops will leave Afghanistan by September 11th though some suggest this action will only worsen the situation.

After a nasty whipsaw yesterday that left behind some concerning daily candle patterns, the bulls are back on the job this morning. Traders will have many data points to track this morning with earnings and a jam-packed economic calendar. I think it would be wise to plan for significant price volatility in the weeks ahead as the index charts continue to extend. Logic would suggest a market pullback could begin at any time, but there is little logic in this buying frenzy pushed by a tidal wave of deficit spending. Although market conditions like this typically end in a punishing selloff trying to fight it is unwise. Remember, a market can remain irrational much longer than we can remain liquid. Don’t chase; avoid overtrading, resist complacency but stay with the trend riding this wave as long as it lasts.

Markets opened flat on Wednesday despite a blowout quarter announced during pre-market by JPM. The DIA had a small rally the first hour, traded sideways until mid-afternoon and then sold off the rest of the day. The SPY did the same minus the morning rally and the QQQ sold off all day long. This left us with a Bearish Engulfing candle in the QQQ, a Shooting Star type candle in the DIA and just a black candle in the SPY. No record high closes, but none of the 3 are more than 1.25% from their all-time high close. VXX gained 2% to 10.29 and T2122 climbed back into the overbought territory at 87.50. 10-year bond yields rose slightly to 1.632% and Oil (WTI) spiked more than 4.5% to $62.93/barrel.

Banks continue to top estimates on blow-out trading gains even amidst loan losses. Today BAC and C followed the lead of JPM, WFC, and GS yesterday in beating on both the top and bottom lines. In other sectors, UNH and PEP also posted beats on both lines.

“Expert” analysts are also expecting a pop from Retail Sales numbers this morning. The driver expected for this move is the $1400 stimulus checks the public has gotten during the last month. In fact those analysts are expecting more than a 6% increase, with some going as far as to say they expect a 10% increase over February. So, the potential exists for disappointment of a miss versus expectations and also for a beat that drives infation fear. Be careful.

Related to the virus, US infections are rising again after plateauing at a level above the fall level. The totals have risen to 32,149,223 confirmed cases and deaths are now at 578,092. The number of new cases has ticked higher again and are back above the peak of last summer to an average of 72,688 new cases per day. However, deaths are just starting to plateau again, now at 746 per day. After hours, the CDC decided to postpone a decision on resuming use of the JNJ vaccine while more research can be done on the potential blood clotting issue. In better news, the country will go over 200 million vaccination doses delivered on Friday as the country went over 195 million on Wednesday according to the CDC. Finally, a Duke University report says the US will have 300 million excess vaccine doses by July due to anti-vaxxers, science-skeptics, and evangelicals.

Globally, the numbers rose to 138,976,244 confirmed cases and the confirmed deaths are now at 2,988,801 deaths. The trends have reversed and are now trending toward trouble again as we have seen significant upticks recently. The world’s average new cases continue to rise and is very near the all-time peak and are now at 722,922 per day. Mortality, which lags, is also rising sharply again at 11,543 new deaths per day. In Asia, India has imposed more restrictions, including a curfew in the capitol amidst another record high number of new cases that has caused banquet halls and hotels to be converted into make-shift hospitals. In Japan, a high-ranking official did not rule out cancelling the Olympics again during an interview with the Tokyo Broadcast System. Closer to home, Brazil is seeing its outbreak continue to see record deaths.

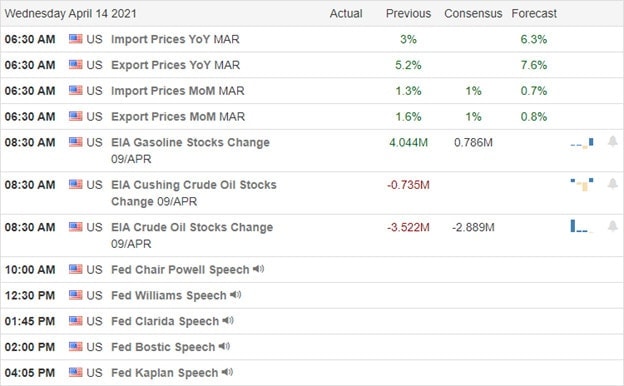

Overnight, Asian markets were mixed again. Taiwan (+1.25%) was an outlier to the upside with Thailand (-1.61%) an outlier to the downside. Most regionals exchanges showed moderate moves in either direction. In Europe, markets are mostly green on modest moves at this point in the day. The FTSE (+0.33%), DAX (+0.19%), and CAC (+0.22%) are typical with Russia (-0.81%) and Portugal (-0.79%) leading the losses. As of 7:30 am, US Futures are pointing to a green open. The DIA is implying a +0.40$ open, the SPY implying a +0.44% open, and the QQQ implying a +0.67% open. Bond yields slipped again overnight as well with the 10-year yield now at 1.618%.

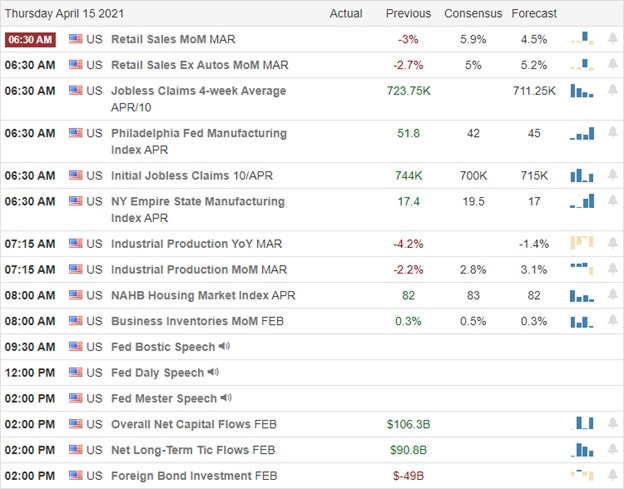

The major economic news scheduled for Thursday includes Weekly Initial Jobless Claims, Mar. Retail Sales, NY Empire State Mfg. Index, and Philly Fed Mfg. Index (all at 8:30 am), Mar. Industrial Production (9:15 am), Feb Retail Inventories (10 am) and 2 Fed speakers (Bostic at 11:30 am and Daly at 2 pm). Major earnings reports on the day include BAC, BLK, C, DAL, PEP, RAD, TSM, TFC, USB, and UNH before the open. Then after the close, AA, JBHT, PPG, and WIT report.

Despite yesterday’s less than stellar day, the bulls remain in control of the trend and spirits seem buoyed by earnings reported so far. This is shaping up to be a tremendous quarter for growth, meaning the next cycle should be even better than this one for earnings. However, the fear of inflation remains the ghost in the room for markets. With a number of reports coming this morning that could be seen as good or bad despite what they report.

Follow the trend, don’t predict reversals, and don’t chase trades you have missed. Respect support and resistance. Keep taking your profits off the table when you can and maintain your discipline. Stay on the right side of the market trend and follow those trading rules. As we know, consistency is the key to long-term trading success.

Ed

Swing Trade Ideas for your consideration and watchlist: No trade ideas for Thursday. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

The choppy dull days of the last couple of weeks could be over as the market reacts to big bank reports and Coinbase IPO. I worry that we have pushed prices so high that companies will have to report near perfection to support their current valuations. I wonder if the massively hyped Coinbase IPO will disrupt the market as traders pull funds from other stocks as they rush to fund their IPO purchase, fearing they will miss out. Fasten those seatbelts it may prove to be a very wild ride in the days and weeks ahead.

Asian markets traded mixed but mostly higher overnight, with Hong Kong surging 1.44%. European markets seem to be taking a wait-and-see approach this morning, trading hovering near the flatline. As earnings roll out, U.S. futures are trying to hold on to a positive open, but gains at this point look to be very modest. However, anything is possible, so stay on your toes as we react to the news.

Economic Calendar

Earnings Calendar

We officially kick off the 2nd quarter earnings today with 17 companies listed on the calendar ready to fess up to quarterly results. Notable reports include BBBY, JPM, GS, HOFT, INFY, LOVE, SJR, & WFC.

News & Technicals’

Today we have the potential for wild price volatility with big bank reports and the IPO of Coinbase. On the earnings front the due to the substantial rally we have experienced in anticipation, companies will need to report very near perfection to support current prices. With so much hype surrounding the Coinbase IPO, it could prove a significant market distraction disrupting stock prices as traders pull money out of other stocks to fund their purchase of this record-setting new issue. I obviously don’t know what happens next, but we may soon long for the dull choppy days of the last week as price volatility ramps up in news-driven reports.

With the SPY and QQQ setting new record highs, their charts appear significantly extended and almost parabolic over the last three weeks of trading. Clearly, the rising infection rate and the pulling of the JNJ vaccine are of no concern to this market. The hotter than expected CPI also proved to be of no consequence as traders chase into stocks with no price too high apparently. I have to admit this makes me very nervous that the market could be running at full speed toward a very steep cliff. However, I have seen many times in my trading career that an overly exuberant market can last much longer than anyone would expect. That said, as retail traders, the best we can do is stay with the trend being careful not to chase already extended stocks and guard against overtrading and complacency.