Wild Ride on Wall Street

The wild ride on wall street continues as traders capitulate, dropping the Dow more than 1000 points only to race back in to close all four indexes in the green. However, with a big day of earnings that includes the tech giant, MSFT traders fear the potential outcome with the VIX closing near a 30 handle. Add to that a worrisome Consumer Confidence due to inflation impacts and, of course, a pending FOMC decision Wednesday afternoon, and we have all the ingredients for additional volatility today.

Asian markets retreated sharply overnight, closing in the red across the board. However, European markets see only green this morning, trying to relieve the pressure of the recent selloff. That said, the price volatility continues this morning, with the Dow futures suggesting a substantial gap down and keeping traders guessing as to what comes next! So, prepare for another day of wild price action.

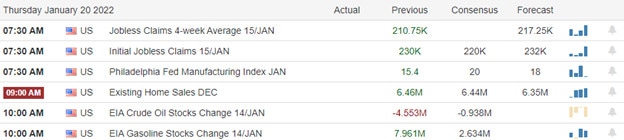

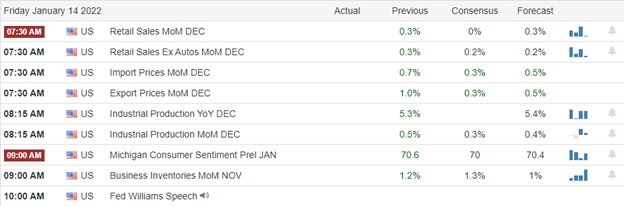

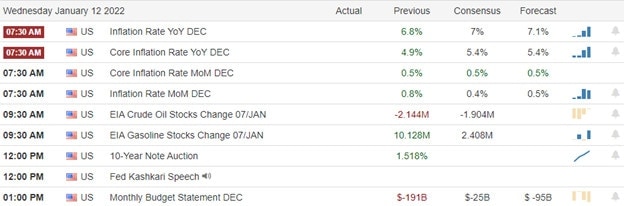

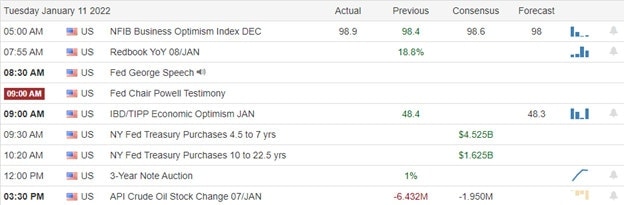

Economic Calendar

Earnings Calendar

We have a busier day on the Tuesday earnings calendar with another big tech report to punctuate the day. Notable reports include MSFT, MMM, AGYS, AXP, ADM, BXP, CNI, COF, GGIV, GE, HA, HYMPY, INVZ, JNJ, LMT, LOGI, NAVI, NEE, NEP, PCAR, PII, RTX, TXN, TRMK, UMC, VZ, WSBC, & XRX.

News & Technicals’

Crisis talks aimed at averting a military confrontation between Russia and Ukraine appear to be faltering, as Western allies prepare for a possible conflict between the neighbors that could be “painful, violent and bloody.” The U.S. Department of Defense has said that about 8,500 American troops are awaiting orders to deploy to the region if Russia does invade Ukraine. Europe has been conspicuously absent from last-ditch negotiations to prevent tensions between Russia and Ukraine from spilling into conflict. Bitcoin, the world’s largest virtual currency, briefly plunged below $33,000 Monday to its lowest level since July. It’s since recovered above $36,000 but is still down almost 50% from a record high of nearly $69,000 in November. That’s got some crypto investors talking about the possibility of a “crypto winter.” IBM shares jump after the company reported a 6% growth in revenue over the fourth quarter. IBM executives have been telling investors to look for mid-single-digit revenue growth. The company spun out its managed infrastructure services unit during the quarter into a publicly held company named Kyndryl. President Joe Biden called Fox News reporter Peter Doocy “a stupid son of a bitch” on a live microphone Monday after Doocy asked Biden if inflation was a political liability to him. Doocy regularly baits Biden during press events, shouting over other reporters and trying to get the president off guard. Biden has a long record of swearing on hot microphones. Treasury yields climbed in the early Tuesday trading, with the 10-year rising to 1.7760% and the 30-year edging up to 2.1133%.

No doubt about it yesterday was a wild ride as traders capitulated with the Dow falling more than 1000 points then surged back up to close the day green across all four indexes. But, unfortunately, the wild volatility continued in the overnight futures markets, dropping more than 250 Dow points. Today we have a busy day of earnings, with the MSFT report coming after the bell. After the NFLX disappointment and the considerable Nasdaq selloff, there is a palpable uncertainty as we wait for the tech giant to report. During the morning session, we will face Case-Shiller home price numbers and worrisome Consumer Confidence numbers amid rising inflation. Of course, anything is possible with an FOMC decision just around the corner, so buckle up for the wild ride to continue.

Trade Wisely,

Doug