Hawkish Comments

The bears came out to play yesterday after hearing the hawkish comments from the Fed that is willing to fight inflation aggressively with swift balance sheet reductions and higher interest rates. Even with yesterday’s selling, the indexes remain in bullish price patterns, but that could quickly change if the bulls can’t find the energy to defend price supports. So, after the usual morning push and pull, don’t be surprised if the price action becomes stale and choppy as we wait on the release of the Fed minutes and the volatility it often creates. As you plan forward into Thursday, keep in mind James Bullard speaks and has in the past pushed for a full point rate increase!

Asian markets closed mainly in the red overnight as treasury yields continue to rise, with tech leading the selling. However, the inflation-fighting Fed comments and added Russian sanctions have the European markets bearish this morning, with indexes red across the board. With oil numbers and the Fed minutes ahead, U.S. futures also point to a bearish open, with the tech sector feeling the most pressure.

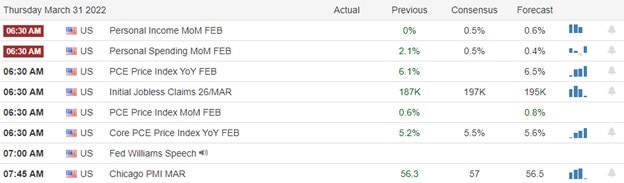

Economic Calendar

Earnings Calendar

We have just over 20 companies listed on the Wednesday earnings calendar, with the most unconfirmed. Notable reports include CLIR, LEVI, TLRY, RGP, RPM, SCHN & SMPL.

News & Technicals’

Fed Governor Lael Brainard and San Francisco Fed President Mary Daly spoke Tuesday, emphasizing the central bank’s commitment to fighting inflation through higher interest rates. “It is paramount to get inflation down,” Brainard said. Raising rates “is necessary to ensure that again, [you] go to bed at night, you’re not worrying about whether prices will be higher, considerably higher tomorrow,” Daly added. Twitter said in an SEC filing on Tuesday that Tesla CEO Elon Musk has been buying shares on almost a daily basis since the end of January. The filing indicates he’s spent $2.64 billion on Twitter stock. The disclosure came in a 13D filing, confirming that Musk now has an active stake in Twitter. JetBlue Airways made a $3.6 billion all-cash offer for Spirit Airlines, raising questions about Spirit’s deal to combine with rival discount carrier Frontier Airlines. The bid comes less than two months after Spirit and Frontier agreed to merge into a discount airline behemoth. Trading in Spirit shares was halted before the market closed Tuesday after the stock spiked more than 22% to $26.92. CDC Director Rochelle Walensky said high immunity levels from vaccination, boosters, and prior infection should provide some protection against the omicron BA.2 variant in the US. BA.2 makes up a growing proportion of variants in the U.S., but new infections are steady. Hospitalizations have been at their lowest level since 2020. BA.2 has caused significant outbreaks in Europe and China. Treasury yields rise on hawkish Fed comments, with the 5-year trading at 2.7635%, the 10-year at 2.6125%, and the 30-year rising to 2.6204% in early Wednesday trading.

The bears found some inspiration yesterday after hearing the hawkish comments from the Fed, which is willing slow the economy to fight inflation aggressively. However, even with yesterday’s selling, the index patterns held in bullish patterns. The question now is, will bears have the energy to follow through today breaking price supports, or will the bulls have the tenacity to defend? Today we have more Fed speakers, and later this afternoon, we could experience an extra dose of volatility at the release of the Fed minutes. If that’s not enough, one of the most hawkish Fed members, James Bullard, speaks Thursday morning! So, prepare for a bumpy road ahead as the market comes to terms with the fact the Fed must act to control inflation and will no longer serve as the guarantee of support.

Trade Wisely,

Doug