Monday was another big day for the Bulls. All three major index ETFs opened flat with DIA “gapping” the most by opening down 0.09%. However, that was the last we saw of the Bears. The SPY, DIA, and QQQ then gave us a long steady rally until the last 15 minutes of the day when we saw very modest profit-taking. This action gave us large, white-bodied candles with small upper wicks (and no lower wicks) in all three major index ETFs. All three remain well above their T-line (8ema). This happened on a bit lower-than-average volume in the QQQ as well as a well-below-average volume in the SPY and DIA.

On the day, nine of the 10 sectors were in the green with Communications Services (+1.42%) out front leading the way higher while Utilities (-0.06%) was the only sector in the red. At the same time, the SPY gained 0.77%, DIA gained 0.60%, and QQQ gained 1.22%. The VXX fell 0.75% to close at 18.42 and T2122 fell but remained in the middle of its overbought territory at 90.79. 10-year bond yields dropped again to 4.426% and Oil (WTI) spiked 2.12% to close at $75.50 per barrel. So, after a few days of consolidation, Monday was another move in the three-week-long strong rally. We are not extremely stretched but are overbought.

There was no major economic news reported Monday. However, the NY Fed released the results of its survey of US credit demand. The report said there was a “notable decline” in credit over the last year with applications down. (Down from 44.8% of those surveys in 2022 to 41.2% of those surveyed in 2023. The pre-pandemic level was a high of 45.8% in 2019.) However, the survey also found an increase in “interest in applying for more credit.” (This hit 29% in October versus the year-to-date average of 26%. The 2019 number for interest in applying was another high 27.2%.) Interestingly, this may fly in the face of the narrative that “things were great pre-pandemic” since more people were applying for credit and more people were interested in applying then versus now. However, I suppose it is also possible to argue that fewer people apply now because rates are higher and fewer are interested in applying because they may think they would be turned down.

In Fed speak news, Fed Presidents Goolsbee (Chicago) and Collins (Boston) sparked investor enthusiasm Monday. Both hinted at the possibility of rate cuts by May. In a speech, Goolsbee gave a sense of hope, suggesting the economy is on what he has called “the golden path” (lowering inflation without a crashing economy). Goolsbee did not provide specific forecasts or discuss a specific schedule for future interest rates. He did, however, acknowledge the market’s anticipation of rate cuts with a 28% chance priced into futures for March and a 58% probability by May. In the same vein, Boston Fed President Collins noted the encouraging pattern of inflation control from last Friday’s data. Collins also noted that while future hikes are still possible, they are not her primary expectation.

In stock news, MS announced a major reshuffle of their top executives in preparation for Ted Pick rising to the CEO role. At the same time, not to be outdone, C announced its own reshuffle as part of CEO Fraser eliminating an entire layer of management (300 senior management roles, which is just under 10% of the staff at that level of the company) as a part of “Project Bora Bora” restructuring. Later, Bloomberg reported NVDA is working with a spinoff from GOOGL (SandboxAQ) to use its high-end chips for drug and battery development by simulating chemical reactions. At the same time, MGM union workers rejected the tentative contract the union had negotiated (which included an immediate 18% pay increase). At the same time, Reuters reported that employees at two WFC branches have filed to have elections on whether or not to unionize. Elsewhere, AAPL announced it will delay the release of its $3,500 VR/MR Headset until March (the prior date was January) as the company is still having design issues. Meanwhile, NSANY (Nissan) announced it is following all other non-union automakers in hiking US worker wages. NSANY said it will increase US plant (9,000 employees) wages by 10% in January. After the close, FSR announced that its Chief Accounting Officer had quit, less than two weeks after joining the company. Also after the close, TSLA announced it will RAISE prices on its Model Y in China starting today, by an odd 0.6%. This may signal a slowing of the EV price war.

In OpenAI news, a few days after the company founder and CEO was ousted by the board (and immediately hired by MSFT), almost 700 of the 770 company employees threatened to resign, unless the company’s board resigns, in a formal letter. The list of signers of that letter includes every significant employee other than three C-suite executives. (The ousted CEO Altman was given authority to hire them all for MSFT by MSFT CEO Nadella.) If 90% of the staff did leave, OpenAI loses most (or all) of its value overnight. Not to be left behind, CRM CEO Benioff gave an open invitation to those OpenAI employees to join CRM instead of MSFT. Shortly afterward, significant VC investors in OpenAI told Reuters they are considering suing the board. For his part, MSFT CEO Nadella (MSFT is the largest shareholder of OpenAI) said that the governance (read board) of OpenAI needs to change immediately, regardless of whether or not Altman returns to that company.

In stock government, legal, and regulatory news, Reuters reported that employees at two WFC branches have filed with the NLRB to have elections on whether or not to unionize. The government of Canada announced Monday that it will put forward legislation to provide $20 billion in subsidies (over five years) for “carbon capture and net-zero energy” projects. At the same time, BAYRY (Bayer) was ordered to pay $1.56 billion to four plaintiffs by a MO jury over claims the company’s Roundup weedkiller had caused diseases including cancer. Later, Reuters reported that the SEC has been telling lobbyists and corporate executives that it may consider “scaling back” its long-anticipated environmental emissions and greenhouse gas reporting rules. (Back in March 2022, the SEC announced rules requiring public companies to report climate risks and material emissions. However, with only a one-vote majority over GOP SEC Commissioners, it seems corporate interests have won the fight and will take the sting out of the rules allowing corporations to mostly go on as usual. Elsewhere, a German court ruling (saying the government cannot reallocate unused Covid pandemic funds) has wiped $66 billion off the books and put many projects at risk. Those funds had been slated for subsidies for two chip plants (TSM, INTC, and IFNNY plants), a decarbonized steel capacity increase, and multiple EV battery supply chain projects (impacting TSLA). The next step is undoubtedly companies threatening to cancel projects, which had been pegged at creating 500k jobs. Later, a division of ASGN was named the primary contractor for a $61 billion (over 10 years) Dept. of Veteran Affairs IT overhaul project. At the same time, the NHTSA said it has opened an investigation into HYMTF and KIA over 16 separate recalls the companies have had to issue over 6.4 million vehicles relating to brake fluid leaks that could cause fires. Meanwhile, TM agreed to pay $60 million in a settlement with the CFPB (of which $12 million was fines) related to illegally bundling unwanted products into car loans that increased loan payments and hurt consumer credit ratings. At the same time, the US Senate has informed AAL, DAL, SAVE, and other airlines that it will hold a hearing investigating baggage, flight change, and seat selection fees. Later, the FDA warned healthcare providers not to use Monoject syringes from CAH (patient-controlled pain management devices) after the company initiated a recall.

After the close, A, BRBR, CENT, CENTA, KEYS, TCOM, and ZM…all…reported beats on both the revenue and earnings lines. It is worth noting that A, CENT, and KEYS have lowered their forward guidance. However, ZM raised its own guidance.

Overnight, Asian markets were mixed but leaned toward the green side on numbers and strength of move. Taiwan (+1.20%) and South Korea (+0.77%) paced the gainers while Singapore (-0.49%), Shenzhen (-0.26%), and Hong Kong (-0.25%) led the losses. In Europe, the bourses lean heavily toward the red at midday. The CAC (-0.23%) and FTSE (-0.47%) lead the way lower while the DAX (+0.23%) is one of only three exchanges in the green in early afternoon trade. In the US, as of 7:30 a.m., Futures are pointing toward a modestly red start to the day. The DIA implies a -0.15% open, the SPY is implying a -0.13% open, and the QQQ implies a -0.13% open at this hour. At the same time, 10-year bond yields are down to 4.41% and Oil (WTI) is off slightly to $77.70 per barrel in early trading.

The major economic news scheduled for Tuesday is limited to October Existing Home Sales (10 a.m.), FOMC Meeting Minutes (2 p.m.), and the API Weekly Crude Oil Stock Report (4:30 p.m.). The major earnings reports scheduled before the open include ANF, AEO, ADI, BIDU, BBY, BURL, CAL, DKS, DY, IQ, J, KSS, LOW, MDT, NJR, and YSG. Then, after the close, ADSK, GES, HPQ, JWN, NVDA, and URBN report.

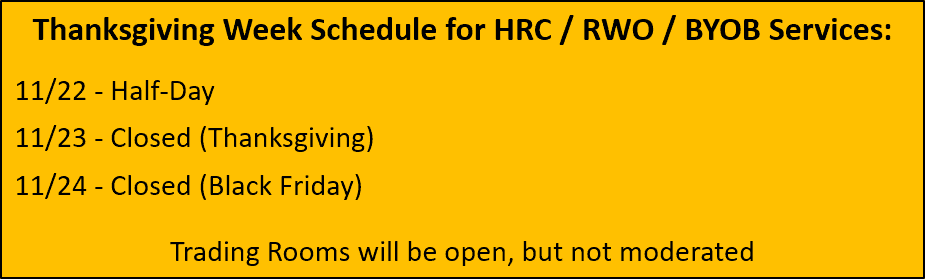

In economic news later this week, on Wednesday, Oct. Core Durable Goods Orders, Oct. Durable Goods Orders, Weekly Initial Jobless Claims, Michigan Consumer Sentiment, Michigan Consumer Expectations, Michigan 1-year Inflation Expectations, Michigan 5-year Inflation Expectations, and EIA Weekly Crude Oil Inventories are reported. There is no major economic news scheduled for Thursday with markets and Federal agencies closed for Thanksgiving. Finally, on Friday, we get S&P US Mfg. PMI, S&P US Services PMI, and S&P Global Composite PMI.

In terms of earnings reports later this week, on Wednesday, DE reports. There are no reports on Thursday. Finally, on Friday we hear from HTHT.

In miscellaneous news, MCO said Monday that “structural demand” for US bonds remains very strong, despite the increased volatility of recent months. Specifically, Moody’s said not to worry about bond demand because, “As the Fed reduces its Treasury holdings, foreign central banks, pension funds, insurance companies and households will be stabilizing factors in the market.” (This seems to be a bit at odds with the rating agency’s recent change of US debt outlook to negative. However, it may be informed by the just-passed CR which eliminates the immediate prospect of a US government closure.) Elsewhere, the US Dollar dropped to its lowest level in two months Monday as expectations of interest rate increases are now past. Meanwhile, in Germany, producer prices fell a whopping 11.0% year-on-year in October. Finally, CNBC reported that gas prices have fallen to their lowest Thanksgiving week price since 2020 after nine consecutive weeks of drops in the national average gasoline price.

So far this morning, ANF, ADI, DKS, DY, IQ, KSS, and MDT all reported beats on both the revenue and earnings lines. Meanwhile, BIDU, BBY, CAL, and LOW all missed on revenue while beating on earnings. On the other side, J beat on revenue while missing on earnings. Unfortunately, BURL missed on both the top and bottom lines. It is worth noting that ADI, J, and LOW lowered their forward guidance. However, ANF, DKS, HIBB, and MDT raised their guidance.

With that background, all three major index ETFs opened the premarket just inside the large white candle from Monday. So far in the early session, they have printed small, indecisive, black-bodied candles. The SPY, DIA, and QQQ all remain well above their T-line (8ema) and 50smas. So, the Bulls are in control of both the short-term and 4-5-month trend. In terms of extension, the T-lines (8emas) are not too far extended but Monday’s candle did put all three major index ETFs at the edge of being stretched again. Meanwhile, the T2122 indicator has fallen back but remains in the middle of its overbought range. So, we have some slack to work with but we are still leaning toward the need of pause or pullback. With that said, keep in mind that the market can remain overbought longer than you can last predicting a reversal too soon.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Comments are closed.