A sharp rally followed by a nasty reversal selloff leaving behind bearish candle patterns and more questions than answers heading into 3rd quarter earnings. The VIX closed above a 32 handle showing a level of uncertainty not generally associated with new record highs. I suspect the volatility will remain quite high, making the navigation through earnings season quite challenging even for very experienced traders. Stay sharp and plan for just about anything in the days ahead.

Asian markets saw modest losses across the board even as their June trade data beat expectations. European markets are trading lower this morning as concerns of the spiking pandemic infections weigh on investor sentiment. US Futures again find the energy to pump up in the premarket trying to ignore yesterdays selling damage as earnings season begins. Anything is possible, so stay focused and flexible.

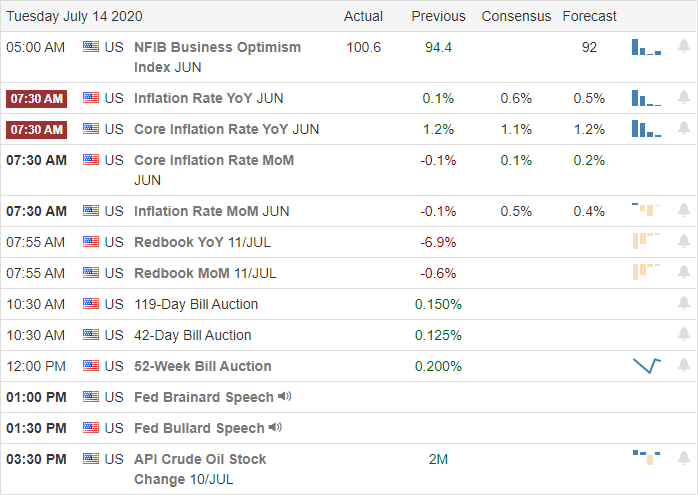

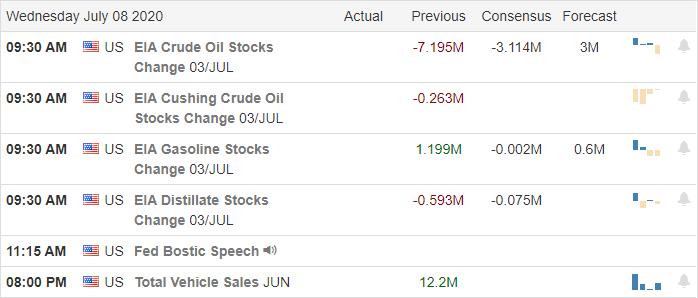

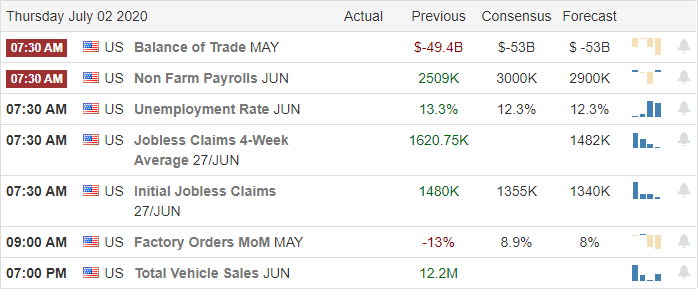

Economic Calendar

Earnings Calendar

Today we officially kick-off 3rd Quarter earnings with 14 companies fessing up to quarterly results. Notable reports include JPM, AMX, C, DAL, FAST, & WFC.

News and Technical’s

I’m guessing yesterday turned out to be a bit painful after the significant index gains quickly reversed after the Governor of California announced a sweeping roll-backs due to a 28% increase in infections. Two of the largest California school districts will not reopen favoring distance learning in an attempt to protect students and teachers from the virus. I had mentioned the possibility of a pop and drop pattern, but the way this reversal played out was strickly the sensitivity of the market to the news. Interestingly as the market rallied yesterday, the Absolute Breadth Index continued to decline. However, as soon as the selling began, the Breadth Index rallied with the selloff. I believe that a large portion of that problem is that just 5-companies now command a full 25% of the entire SP-500 weight. An imbalance that could become a significant problem should profit-taking take hold in the five heavyweights. Yesterday may have been a preview of what could happen if that should come to pass.

Technically speaking, the flash selloff yesterday adds a bit of complication to the look of all the index charts as we begin 3rd quarter earnings. The DIA left behind a nasty shooting star pattern that once again failed the 200-day average. It would appear ahead of earnings they bulls are pushing to test the 200 once again as resistance at the open. The SPY left behind a bearish dark cloud cover pattern failing to hold the break of the early June island reversal pattern. The NASDAQ was the first index to have reversed yesterday from a very extended run leaving behind a bearish engulfing pattern on the QQQ. IWM finished the day with a dark cloud cover pattern, and the VIX ended the day printing a reversal that broke above its 50-day average closing above a 32 handle. With the VIX so elevated and facing an uncertain earnings season traders should expect challenging price volatility. Stay focused, and flexible as anything is possible in the days ahead.

As the bulls push for new record market highs this morning, it seems there is no price too high for some stocks with 3rd quarter earnings set to begin this week. With Covid-19 infections rising, some areas have reported hospitals are at capacity. Still, the market seems confident that no matter the impacts, the Fed and the Congress will cover the costs with more debt to keep the market going up. Expect the wild volatility to continue in the week ahead.

Asian markets rose sharply overnight, with the NIKKEI closing up nearly 2.25%. European markets are full-on bullish across the board this morning up more than 1.3%. US futures opened positive and continue to push higher this morning with a gap up open that will set new NASDAQ record highs at the open. Go bulls!

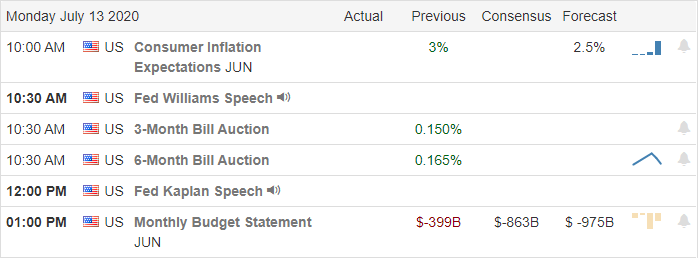

Economic Calendar

Earnings Calendar

This week we begin the 3rd quarter earnings season with the big bank beginning to report on Tuesday. We start the week with a light day with just 9-companies reporting with only one notable report coming from PEP this morning.

News and Technical s

I’m not sure it makes any difference to write about the impacts of coronavirus as the country continues to soar in new infections. As states require the wearing of masks such as Florida after reporting more than 15,000 new infections, protests broke out from groups saying that infringes on their rights. You can’t make this stuff up! If I were writing a novel, it would be so unbelievable it would not sell. Several areas in the country reporting that hospitals are at capacity treating Covid-19 patients, and the death toll in the US is back on the rise. Approaching earings, the market appears to have little to no concern about the pandemic with the expectation that the Fed and Congress will continue to escalate the deficit to keep the market going higher. With the national debt over 26.5 Trillion, the consequences of such spending are apparently irrelevant in today’s society.

Futures began trading last night seeing only bullishness, and that sentiment has only grown as we near the open of the day. The NASDAQ is poised to set another new all-time high at the open, and the SPY will gap above the island reversal that has recently served as resistance. The DIA, which has struggled with the resistance its 200-day average, will gap above it this morning at the open. Gaping to new record highs always carries with it the risk of a potential pop and drop, but with the bulls relentlessly willing to pay any price for stocks ahead of earnings, I would not rule out a big short squeeze sending indexes even higher. Expect wild price action to continue in the week ahead. Stay focused and flexible.

As we head into the weekend, the tech giants continue to lead the way setting new records while DIA, SPY, and IWM experience some selling pressure. At the same time, 18 million Americans remain unemployed as more than 1.3 million files for benefits. That nearly doubles the number we experienced in the depths of the 2008 and 2009 depression. The VIX continues to display the uncertainty the market faces as a select few stocks continue to rise to new price highs.

Asian markets closed the day lower across the board as virus infections weigh on recovery hopes. However, European markets are bullish this morning in reaction to hopeful Italian data. US Futures have recovered from overnight lows suggesting modest declines at the open ahead of a very light day of earnings reports and pending PPI data.

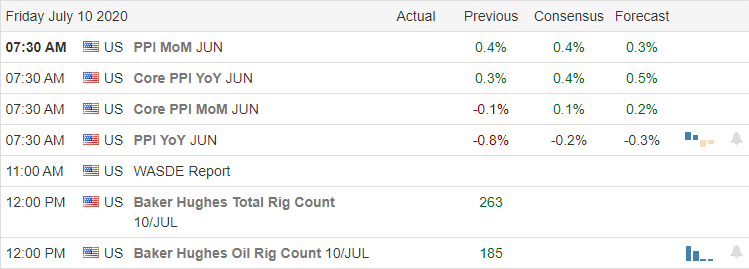

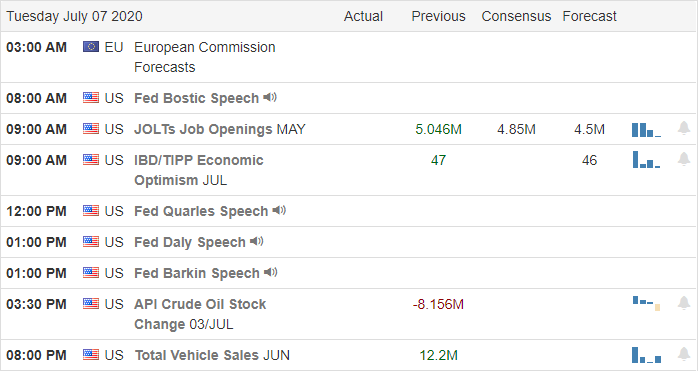

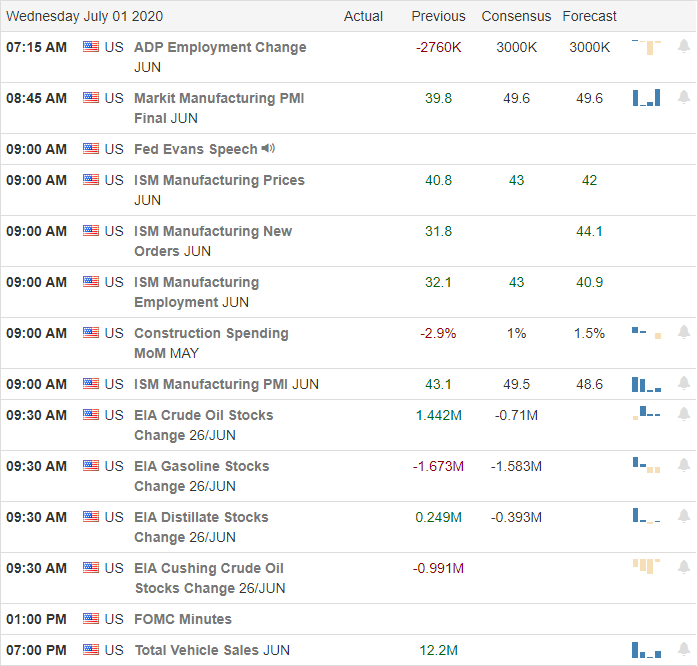

Economic Calendar

Earnings Calendar

On Friday’s earnings calendar, we have a light day with just 11 companies stepping up to quarterly results. The report from SJR is the only particularly notable report I see. Remember, the official kick-off to the 3rd quarter earnings season begins next week.

News and Technical’s

Another day of records with the NASDAQ reaching out to new highs while at the same time coronavirus infections in the US topped 63,000 for the first time. More than 1.3 million filed for unemployment last week, and the concern is that the numbers may now start to grow as states struggle in their efforts to recover with the recent surge in the pandemic infections. It’s interesting to note that even at 1.3 million, the number is double the worst numbers we experienced in the depression of 2008 and 2009. A day after the Supreme Court rules against the President, his competitor calls for an end of the era of shareholder capitalism, suggesting higher corporate taxes. Tensions continue to grow as following the impositions of sanctions of three local Chinese officials of China’s ruling Communist party over human rights abuses. China vows to retaliate.

As we head toward the weekend, the imbalance between the tech giants continues with the QQQ holding on to a strong uptrend while the DIA, SPY, and IWM experience selling pressure. I have to wonder what happens to the market if or when profit taking begins in the tech sector. The VIX continues to suggest a considerable uncertainty exists as it seesawed between a low of 26 and a high of 31 handles yesterday. Facing a light day on both the economic and earnings calendar, the market could be sensitive to the news cycle, and price action is likely to remain volatile. Next week begins the 3rd quarter earnings season, which is likely to keep the wild price action going into the near future. Stay focused and flexible, carefully considering the risk you carry into the weekend.

As the Nasdaq prints, another record high the US also sets a new national record of Covid-19 infections and health officials as calling for a federal policy to curb the spread. While on the surface, the market appears to have absolutely no concerns, yet the VIX remains quite elevated, and the Absolute Breadth Index continues to decline. An interesting dichotomy that could produce a bullish short squeeze or an attack by the bears as recovery concerns mount. Stay focused and flexible as the market grapples with what comes next.

Asian markets continue their bullish run with week lead by China, which rose 1.39%. European markets have seesawed between gains and loss this morning as they cautiously monitor pandemic numbers and the challenging recovery. Ahead of a light day of earnings and another round of jobless claims US futures point to a slightly lower open.

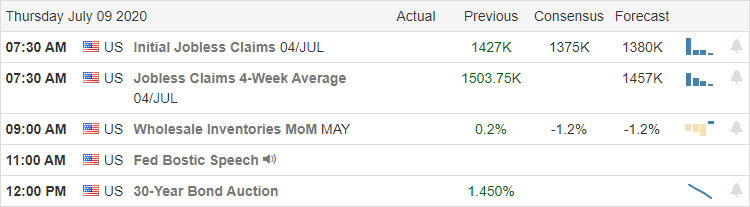

Economic Calendar

Earnings Calendar

On the Thursday earnings calendar, we have just 11 companies reporting quarterly results. Notable reports include WBA, BNED, FC, HELE, PSMT, & WDFC.

News and Technical’s

The bulls refuse to lose continuing to buy up the big tech giants with NASDAQ setting another record high lead by AAPL, which also closed the day at a record high. As the market continues to surge, so does the pandemic infections, hitting a new national record of 60,000 new cases reported in a single day. Health officials are calling for a federal policy action to curb the spread of the virus, suggesting another shutdown may be necessary. A new study warns of a potential wave of brain damage as an aftereffect of Covid-19 infections. The research shows patients suffering from temporary brain dysfunction, strokes, nerve damage, or other serious brain effects. A scary thought considering the US is now dealing with more than 3 million that have already been affected by the virus. According to reports, there is already a noticeable pullback in driving activity as people choose to stay home rather than risking infection. United Airlines warns that half of its workforce may be furloughed, suggesting up to 36,000 people could see their jobs cut as recovery hopes fade in the recent weeks. Bed Bath & Beyond announced they would close 200 stores after reporting a sharp sales decline of nearly 50%, and the Pier One said it would not reopen retail stores in their bankruptcy reorganization moving to online sales only.

Technically speaking, the DIA, SPY, and IWM indicate a possible higher low could be forming after yesterday’s rally, yet at the same time struggling with overhead resistance and potentially bearish candle patterns. Adding to the confusion is the fact that the VIX remains elevated, and the Absolute Breadth Index continues to decline. I see the potential for a bullish short squeeze and, at the same time, see the possibility that the bears could soon attack at any time due to growing recovery concerns. It’s also odd to see indexes setting new records while at the same time precious metals continue rally sharply. Ahead of weekly jobless numbers, the futures currently point to a slightly lower open. Stay focused on price action and remain flexible and prepared for just about anything.

With coronavirus surging around in many US states, the business remains under tremendous pressure with additional closures and further delays of reopening of the economy. The huge back to the school shopping season is also in question as school districts and parents grapple with the difficult decisions of reopening and child safety. Yesterday’s mild selloff left more questions with bearish candle patterns appearing on the index charts at possible highs or near resistance levels. With the VIX rising in yesterday’s close expect price volatility to remain high and extreme sensitivity to news events.

Asian markets closed mixed but mostly higher, with Shanghai rising 1.74%. European markets are seeing modest declines across the board this morning as the surge in pandemic infections worries investors. US Futures chop around the flat-line this morning with a light day of earnings and economic news.

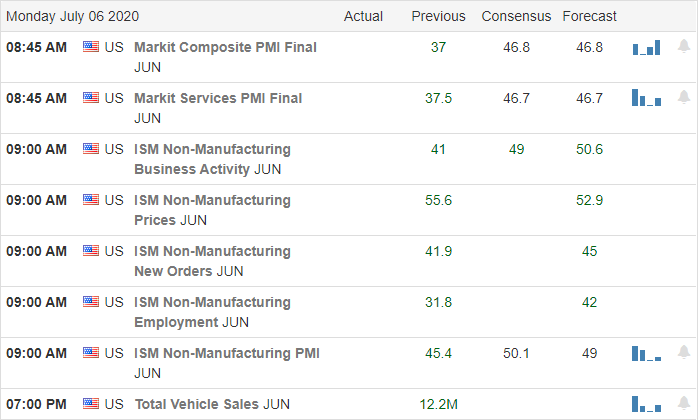

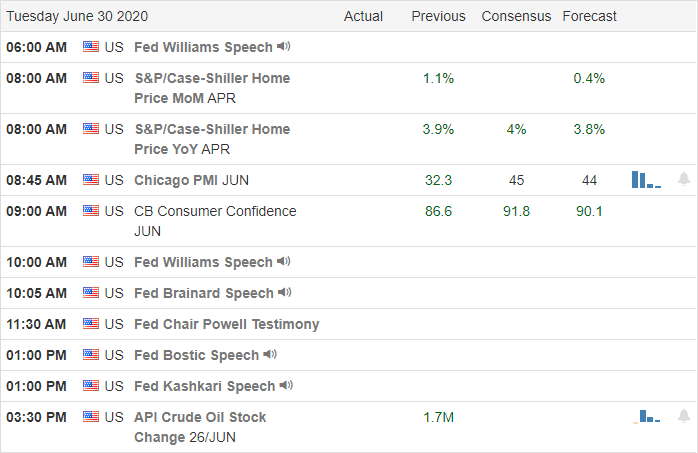

Economic Calendar

Earnings Calendar

On the Hump day earnings calendar, we have just 14 companies expected to report quarterly results. Notable reports include BBBY, MSM & SMPL.

News and Technical’s

US coronavirus infections have topped 3-million cases with states reporting more than 55,000 instances yesterday and 993 deaths. Arizona has seen a 26% increase in infections with the WHO suggesting just a 5% increase is troubling. In response to rapidly rising cases and hospitalizations, Texas canceled the state fair while San Francisco delays reopening indoor dining. It’s no wonder that parents have concerns about sending their children back to school this fall, and retailers worry about the back to the school shopping season. The President is suggesting he will do all he can to pressure schools to reopen. Tensions between the US and Chiana continue to grow after the FBI Director slammed their government for the use of espionage and cyberattacks against the United States. He said the stakes could not be higher, and the potential economic harm to American business as a whole almost defies calculation. These comments come on the heels of the Secretary of State threatening to ban Chinese social media apps.

After a gap down open, the bulls once again attempted a rally to test resistance levels but found resistance and ultimately selling off by the close. Potential bearish candle patterns such as an abandoned baby pattern or evening star patterns were left behind on the DIA, SPY. The QQQ left behind the uncertainty of a shooting star pattern, and the VIX rose above a 29 handle. Declining issues far outpaced advancing issues after the Schwab pointed out that 90% of the current market rally is attributed to just the top 10% of companies. This colossal imbalance raises the question, what happens to the market should these tech giants begin to selloff? An interesting question to ponder as we head for a relatively flat open with a light day of earnings and economic news.

The NASDAQ lept higher yesterday, setting new records while the Dow, SP-500, and Russell struggled to find follow-through to break price resistance levels. In a pattern that’s becoming all too familiar of late, the big morning gap struggled to find buyers or sellers as it chopped sideways the majority of the day. This morning with the EU forecasting an 8.3% economic slump and the US states beginning more business shutdowns, it looks as if the big gap this morning will be down trapping those that chased in yesterday.

Asian markets closed mixed but mostly lower overnight. European markets fall on concerning economic data with the DAX, FTSE, and CAC down 1% or more this morning. US Futures in reaction to virus-related business uncertainty suggest a substantial gap down at the open ahead of a light day of earnings and economic reports.

Economic Calendar

Earnings Calendar

On the Tuesday earnings calendar, we have 10-companies fessing up to quarterly earnings. Notable reports include LEVI and PAYX.

News and Technical’s

We have reached nearly 3 million coronavirus cases in the United States, with several states doubling infection rates in just two weeks. Florida is once again closing restaurants, health clubs, and group party venues, and some areas in Texas are reaching hospital capacity. Australia closed interstate borders in an attempt to slow the spread of the pandemic, and the Governor of California asks indoor business to close. With more and more states adding to shutdown orders and mulling future restrictions, it would seem the economic recovery continues to face considerable challenges. As tensions grow with China, the US is conducting war games in the South China Sea and, at the same time, looking at banning social media apps such as TikTok. During the night, the EU cut its economic forecasts for the region and is now projecting an 8.3% decline in the economy this year.

Yesterday’s big morning gap struggled to find follow-through buyers spending most of the day chopping sideways. The DIA, on a last-minute surge at the end of the day, breached the resistance of its 200-day average. Although the SPY tried hard to break the resistance of the early June island reversal pattern, it closed the day, failing to breakthrough. The QQQ lept higher with the tech giants leading the way while the IWM closed the day lower once again, unable to reach its 200- day average. With a light day of earnings and economic news, the market seems to have turned its attention to the impacts of the viral surge that is prompting business shutdowns in several states. As of now, the US futures are pointing to a gap down open that has the potential to create abandoned baby patterns at resistance in the DIA and SPY. With the VIX remaining elevated, expect the wild price volatility to continue today.

With markets around the world surging under bull pressure while at the same time coronavirus infection rates set new records, one has to wonder if the rally is real or if the world is suffering from a major case of denial? I guess we will find out if companies can support these prices with 3rd quarter earnings just around the corner. Set for a big gap up open, the indexes will be testing key moving averages resistance levels as well as the island reversal patterns created in early June. The question for today, will we see follow-through buying after the gap, or will it produce another pop and drop pattern like Friday?

Asian markets closed sharply higher overnight, with the Shanghai index leaping nearly 5.75%. European markets are very bullish this morning with the DAX, FTSE, & CAC all higher by more than 1.5%. US Futures point to a substantial gap up at the open as the bulls push once again push for new record highs in the tech sector.

Economic Calendar

Earnings Calendar

On Monday’s earnings calendar, we have 35 companies stepping up to report quarterly results. However, looking through the list, I’m not finding any of today’s reports as particularly notable.

News and Technical’s

After a holiday, 3-day weekend markets around the world surge higher. With 3rd quarter earnings only a couple weeks away, there seems to be no price too high as market leaders set new records. I can’t decide if this rally is justified or if the entire world is suffering from a major case of denial. Over the weekend, health departments reported increased infection rates in 40-State with some Texas regions reaching their hospital capacity. Florida reported more than 10,000 new infections each day of the long weekend. Lawlessness is also on the rise with more 40 shootings in New York alone that resulted in an 8-year old innocent bystander killed by a stray bullet. Although 1.4 million people filed for unemployment last week, the Employment situation number better than expected rehiring occurred over the previous month. With unemployment, at 11%, the market appears to ultra-confident that the coming earnings season will support current stock prices.

With the market set to open with a huge gap up open, the DIA and IWM will once again attempt to break above their 200-day averages. The QQQ will challenge new record highs, and the SPY will test the resistance fo the island reversal pattern printed in early June. I expect T2122 to reach into the bearish reversal zone at the open, so be careful chasing the open with a fear of missing out. Please make sure there are follow-through buyers rather than the pop and drop pattern like we saw on Friday’s morning gap.

The NASDAQ soars to new record highs, as does the number of coronavirus infections across the country. As business once again close and state rollback reopening plans, the market appears to have no concerns whatsoever, pointing to a substantial gap ahead of the holiday shutdown. Bad news has become good news, and the good news is now seen as excellent news, and no price is apparently too high for the bulls. Today is all about the jobs, then expect volume to drop off quickly as we head into an early market close for the holiday.

Asian markets closed higher across the board even as hundreds of protesters were arrested in Hong Kong under the new security laws. European markets trade sharply higher this morning boosted by vaccine hopes with banks up as much as 4%. Ahead of employment data and jobless claims, the US Future point a gap open even as virus numbers surge to a new daily record high.

Economic Calendar

Earnings Calendar

On the Thursday earnings calendar, we have just seven companies reporting results. The only somewhat notable report is that from KFY.

News and Technical’s

As we hit a new daily record high of coronavirus infections and states rollback reopening plans, the US Futures point to new record highs. California has once again closed all indoor operations for about 70% of the States population due to rising numbers. New York has also announced to rollbacks, and Apple said it would close 30 more stores across the country in response. Congress extended the paycheck protection program, and it looks as if Congress is moving forward with another round of direct payments to taxpayers that could be as much as $6000 per household. With MSFT and AMZN leading the way, the QQQ set new record highs yesterday with the DIA and IWM closing the day slightly lower.

Today we get both the Employment Situation number and the weekly Jobless Claims. If the consensus estimates are correct, the rehiring last month is likely a new record since the numbers have been tracked all the way back to 1939. Looking at the market, the millions that remain unemployed and the current round of further state shutdowns don’t seem to matter. Bad news is good news, and good news is excellent news as there appears to be no price too high as stocks continue this historic rally. One has to wonder if the upcoming earnings can support current market prices. Only time will tell. Keep in mind that we have an early market close today, and volume is likely to fall off quickly after the morning reports as traders head out for the 3-day weekend. Have a safe and fantastic 4th of July, everyone!

After a late-day surge, the market closed inking the most robust quarterly rally since 1987 fuled by trillion upon trillion of stimulus and historic central bank operations. However, immediately after the cash close, the futures began selling off and now point to a substantial gap down at the open, taking back most of yesterday’s rally. With a long weekend beckoning traders to extend vacations, look for volumes to decline over the next couple days after the morning reaction to earnings and economic news.

Asian markets closed mixed but mostly higher after June manufacturing activity beat expectations. European markets are decidedly bearish this morning with indexes declining by as much a 1.50%. US Futures point to a gap down open ahead of a big morning of economic data and worries of rising virus infections weigh on the market.

Economic Calendar

Earnings Calendar

On the 1st day of the 3rd quarter, we have 13 companies stepping up to report quarterly results. Notable reports include M, STZ, CPRI, & GIS.

News and Technicals

The last day of the 2nd quarter spent most of the morning session chopping in a narrow range, but in the afternoon, the bulls seized control, pushing the index up into the close. Thanks to the trillion upon trillion in central bank operations and governmental stimulus, we had the most robust quarterly rally since 1987. Interestingly enough, as the market surged higher into the close, the Absolute Breadth Index declined, and the VIX held above a 30 handle. Gold and silver also sharply rallied often considered a safe-haven trade. During testimony to congress, Dr. Fauci, the White-House health advisor, said the coronavirus outbreak is going to be very deturbing and may top 100,000 new cases per day. Yesterday the US reported just over 46,000 new infections and more than 750 further deaths. As the death toll approaches 130,000, Goldman Sachs called for a national mask-wearing requirement in public to save the economy. During the night, the Senate voted to extend the small business coronavirus relief program called the Paycheck Protection Program through August 8th. Also during the night, Hong Kong makes its first arrests just one day after China’s new so-called national security law. The law says that any person that acts to undermine national unification faces punishment up to a lifetime in prison.

Yesterday’s rally pushed the DIA up to test its 500-day moving average, but by the close was unable to muster the energy to break above. The SPY comfortably held above its 200-day while the IWM remained substantially below. The DIA, SPY, and IWM are still within a short-term downtrend while the QQQ continues to dominate the market with MSFT and AAPL doing the majority of the lifting yesterday. Immediately after the cash close yesterday, the futures began to selloff and now point to a significant gap down this morning. With a busy economic calendar, the next 2-days and rising concerns on the impacts of the rising pandemic, anything is possible as we approach the 4th of July market shutdown. Expect volume to begin to decline as traders take off early to extend their vacation time.

The market continued its roller-coaster ride of wild volatility, rising sharply in hopes of more government stimulus on the way as the coronavirus spread to more than 44,000 people yesterday. Several states have once again closed bars and fitness facilities as the WHO warns that the worst is yet to come in the world war against the pandemic. Overnight China defiantly passes the so-called national security law for Hong Kong and threatened retaliation for any actions brought against them. What that means in the weeks and months ahead is anyone’s guess.

Asian markets rallied overnight as their June PMI beat expectations. European markets trade mixed in a whipsaw session as they react to Chinese data and the WHO pandemic warning. US Futures appear to be struggling for the inspiration to follow-through yesterday’s bullishness pointing to a flat open ahead of a big day of Fed speak that includes Jerome Powell.

Economic Calendar

Earnings Calendar

On the Tuesday Earnings Calendar, we have just 15 companies stepping up to report on this last day of the 2nd quarter. Notable reports include FDX, AYI, CAG & SCS.

Technically Speaking

The market overlooked rising coronavirus and rallied sharply, mainly on the hope there will be more governmental stimulus on the way. Yesterday, we saw an increase of 44,734 new cases of the virus reported in the US. According to the reports, China has discovered a new strain of the coronavirus, and the WHO warns the worst is yet to come. Shell has announced that it will take a massive write-down up to 22 billion as a result of COVID impacts on the industry. Wells Fargo said it would cut dividends after the Fed stress tests, but JPMorgan, Citi, and Goldman stated they would matain dividends in the coming quarter. During the night, China passed what they called a Hong Kong national security law for Hong Kong that has drawn criticism from around the world. When asked about possible repercussions, Chinese officials defiantly stated they would retaliate against any actions or sanctions brought against them. Boeing had its first successful test flight of the 737 Max yesterday as they pursue recertification of the aircraft after the deadly crashes that grounded them more than a year ago.

Although the Dow rose 580 points by the close yesterday holding on to its 50-day average, the index continues to remain in a short-term downtrend. The SPY printed and Piercing Candle Pattern holding its 200-day average while the IWM did much better breaking the high of Friday’s big selloff. As wonderful as that may seem on the surface, the SPY and IWM technically remain in short-term downtrends with the Absolute Breadth Index pulling back yesterday. A big part of yesterday’s rally likely was nothing more than short-covering. On the last trading day of the quarter, anything is possible, but as of now, the futures seem to be struggling for the inspiration to follow-through on the bullishness for a second day, suggesting a flat open.