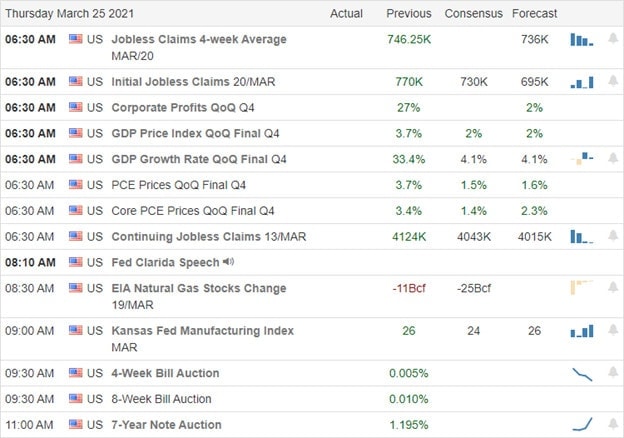

After Monday’s big jobs pop and waiting on the FOMC minutes, the bulls took a siesta yesterday, largely chopping sideways. Though we are likely not learn anything new in the minutes of the last Fed meeting, all eyes will be looking for clues for changes in their extremely dovish stance coming under fire due to inflation worries. With the 2nd quarter earnings season set to begin next week, don’t be surprised to see the choppy price action continue.

Asian markets closed mixed overnight, with the HIS slipping nearly 1%. European markets trade mixed with mostly modest price action across the board. After a decline of 20% in mortgage refinance demand, the U.S. has softened from early morning highs, currently suggesting a flat to modestly bullish open as we wait for the Fed minutes.

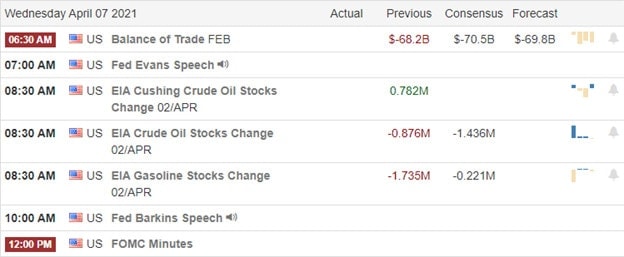

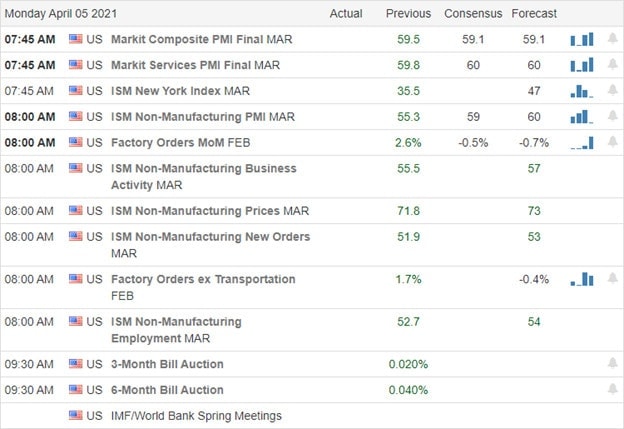

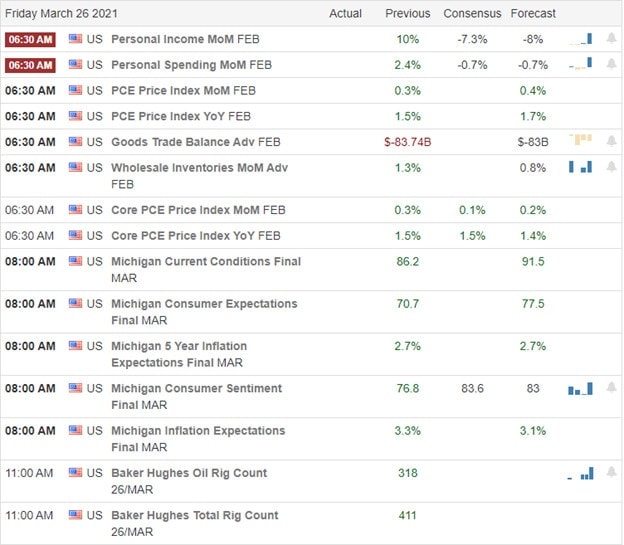

Economic Calendar

Earnings Calendar

On the Wednesday earnings calendar, we have just ten companies listed, though several are unconfirmed. Notable reports include LW, MSM, & SCHN.

News & Technicals’

Markets took a siesta yesterday, waiting on the FOMC minutes. According to reports, second-quarter numbers will likely surge, and many believe the Fed will come under considerable pressure for maintaining its extremely dovish stance. Economists expect a 9% growth in the second quarter that could trigger strong inflation concerns. Though I doubt we learn much more than we already know, all eyes will be on the FOMC minutes looking for clues later this afternoon. Jamie Dimon chimed in to let us know that the expected economic boom is fueled by deficit spending. Thank you very much, captain obvious! Jeff Besos says he supports a hike to the corporate tax rate even though Amazon has come under fire for paying very little in taxes over the past years.

Technically speaking, the indexes are in good shape though perhaps a bit dangerous because of the overstretched condition. The QQQ has rallied sharply up more than 8% in just 9-trading days yet still has overhead resistance to overcome. With the softness experienced in the financial sector and energy sector yesterday, the IWM seemed to struggle and now shows us a possible head and shoulder pattern to keep an eye on. Ahead of the FOMC minutes, the 10-year treasuries continue to moderate, but this could be a temporary situation should the second-quarter numbers confirm inflation concerns. Keep in mind with the kick-off of earnings season just a week away, it could be possible to see choppy consolidation price action in the indexes as we wait for the inspiration.

Credit Suisse reported a $4.7 billion hit as the Archegos fallout continues. However, Treasuries show a little softness this morning, a day after the DIA and SPY leap to new record highs. Oddly, as the markets buzzed with bullish energy, the oil stocks suffered declines as rising pandemic infection rates raised futures demand worries. Another puzzling contradiction is seeing the VIX move up with the indexes. The moral of the story, stay with the bullish trends but don’t become complacent.

Asian markets displayed some wild contradictions last night as the NIKKEI declined 1.30%, and the HSI surged up 1.97%. European indexes are in rally modes on recovery hopes across the pond even as Credit Suisse cuts dividends to the hedge fund losses. U.S. futures seem to be taking a hiatus this morning point to modest declines ahead of the JOLTS report and light day of earnings. Let’s get ready to rumble!

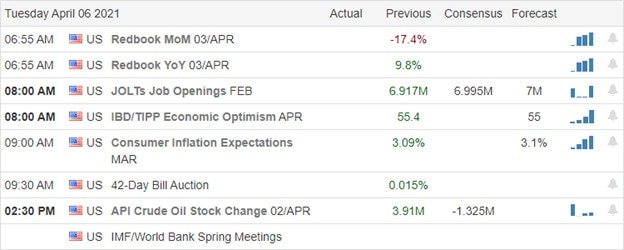

Economic Calendar

Earnings Calendar

In a light day on the earnings calendar with only eight verfied companies fessing up to quarterly results. I made a mistake looking at Tuesday’s notable reports thinking I was going over those on Monday. As a result, I will have to repeat yesterday’s stocks, LNN, MAXN,& PAYX.

News & Technicals’

The Archegos hedge fund scandal with Credit Suisse reporting a $4.7 billion loss as the fallout continues. To pass the Biden $2.3 trillion infrastructure plan Senate Leader Schumer will use budget reconciliation to pass the legislation without Republican votes, setting up another distracting political battle. Google announced it would stop using Oracle’s finance software in favor of the SAP. ORCL is indicated slightly lower this morning. Craig Irwin, a senior analyst at Roth Capital, placed a price target of $150 for Tesla. Tesla closed at $690.57 yesterday, suggesting a 78% haircut if Irwin is correct. In a bit of good news, Treasury yields are pulling back this morning, but I think it would still be wise to keep an eye on them as Congress works to print another $2.3 trillion in deficit spending.

The DIA and SPY printed fresh new record highs as recovery hopes energized the bulls. Interestingly oil stocks suffered yesterday as worries about the rising pandemic infections rates across the country could affect demand. Seemingly a direct contradiction to the overall market bullishness. Another puzzling contradiction is that the VIX moved higher yesterday at the same time the indexes were surging with bullish enthusiasm. Things that make you say, hmm? The QQQ continued its very steep rally yesterday but keep in mind there remains overhead price resistance to be dealt with before the all-clear can be sounded. Remember that it’s not unusual for the market to become a bit light and choppy as we wait for the FOMC minutes coming out tomorrow. However, the JOLTS report could keep the fires burning through the morning session.

While traders enjoyed a three-day weekend, the jobs report blew past consensus expectations adding 916,000 in March. That has the bulls working hard in the premarket point strong bullish open to follow the light volume but record-setting Thursday close. On the bullish side, the VIX is finally breaking down, but on the bearish side, treasuries ticked higher as inflation worries continue due to the vastly stronger than expected jobs number. Though we will set new records at the open, be careful not to chase already extended stocks.

Overnight Asian markets rallied to close green across the board, with the HIS leading the way, up 1.97%. European markets are also showing modest bullish across the board this morning, with tech shares gaining favor. Ahead of a light day of earnings & economic reports, the U.S futures point to a substantial gap up of more than 200 Dow points. Buckle up; it could be a somewhat volatile price action morning.

Economic Calendar

Earnings Calendar

We have 23 companies listed on the earnings calendar to kick off this week, but there are only 3-verified. Notable reports include LNN, MAXN, & PAYX.

New & Technicals’

During the Friday Easter shut down, the monthly government jobs report blew past the expectations, with payrolls jumping 916,000 in March. As a result, the U.S. Treasury yields edge higher in reaction to the strong jobs report’s performance due to inflation worries. Senator Roy Blunt on Sunday urged President Biden to cut his $2 trillion infrastructure plan to $615 billion with a focus on rebuilding physical infrastructure. Kevin O’Leary, chairman of O’Leary ETFs, calls for the U.S. to be “extremely aggressive” to level the playing field with China. He says that could include delisting Chinese stocks and shutting Chinese companies out of the U.S. court system. I suspect we will hear a lot more about this subject in the near future as tensions between the U.S. government & businesses grow against Chinese practices.

Although a light volume day, the SP-500 found a path to a new record high, topping 4000 for the first time in history. The Dow set another new record as well as the QQQ and IWM lagged behind. With the strong jobs report and the anticipation of a bullish 2nd quarter earnings season, the bulls should have the upper hand as long as inflation worries stay in check. With the DIA and SPY working together again, the lagging QQQ is less of a concern, but it would wise to respect the overhead resistance if bonds continue to rally. With the VIX finally falling below support levels, perhaps, we can get past some of these wild whipsaws and get a bit more confidence in the price action. Unfortunitually, the T2122 indicator is already in a short-term overbought condition, with the gap up this morning suggesting an extreme extension, so be careful not to chase already extended stocks in fear of missing out.

Yesterday registered a substantial surge into big tech, but the bullishness fell short of breaking through its 50-day average and remains challenged by significant overhead resistance. With bonds remaining stubbornly bullish after the unveiling of the infrastructure proposal, the question is, can we get a day of follow-though? Keep in mind with everyone thinking about the 3-day weekend ahead, the volume could become light and price action choppy after the morning economic news reaction.

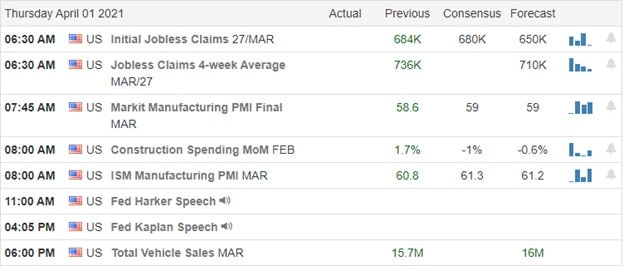

Overnight Asian markets closed green across the board, lead by Hong Kong surging nearly 2%. European indexes trade modestly bullish this morning as they await several data releases. On the first trading day of April U.S. points to modest gains ahead of Jobless Claims and ISM numbers as we slide toward the Good Friday shutdown. Plan your risk carefully.

Economic Calendar

Earnings Calendar

On the Thursday earnings calendar, we have 36 companies listed, but the majority are unconfirmed. Looking through the list, I can only come up with one notable report coming from KMX.

News & Technicals’

There was a surge into big tech yesterday, but overall it was a mixed bag of results, with profit-takers coming in at the close. President Biden’s $2trillion infrastructure is getting a mixed response as worries about the significant tax increases will slow economic and job recovery. Microsoft won a $21.9 billion contract for augmented reality headsets giving the stock a boost into yesterday’s close. Although the 10-year treasuries softened a bit yesterday, they stubbornly hold above 1.71% as inflation concerns continue.

While there was a general sense of bullishness in the market yesterday, in reality, the DIA, SPY, and IWM were in a resting mode while big tech enjoyed a substantial surge of energy. However, at the end of the day, the QQQ could not break above its 50-day average and still has considerable overhead resistance. The SPY missed setting a record high by just a few ticks and then ran into some profit-takers, which honestly surprised me during the end-of-quarter window dressing. The Absolute Breadth Index continues to raise the concern that overall momentum is lacking, and the nasty whipsaw of late keeps us guessing what comes next as the VIX chops with uncertainty. Plan your risk carefully as we head into the Good Friday shutdown and the 3-day Easter weekend.

This afternoon President Biden will unveil his more than $2 trillion infrastructure proposal as the first part of his recovery plan. If approved, it will raise the Corporate Income tax to 28%. Inflation concerns continue to weigh on investors’ minds, with the 10-year treasuries holding above 1.73% and the Case-Shiller, showing that housing prices grew faster over year over year over more than 15 years. Jobs data will be in focus the rest of the week, with Private Payrolls coming in before today’s open.

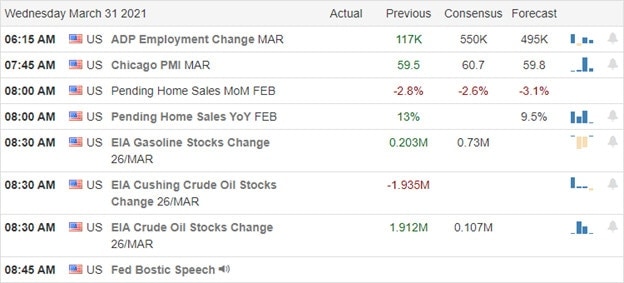

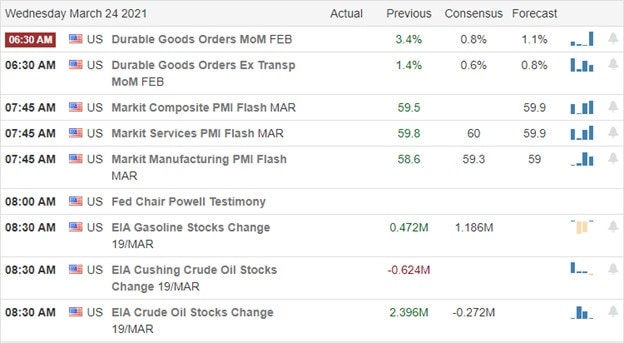

Overnight Asian markets saw declines across the board after coming under criticism for withholding pandemic data in its report to the WHO. European markets trade with modest losses this morning, worried about rising inflation. Ahead of a busy day of earnings, economic data, and the unveiling of the infrastructure plan, U.S. futures point to flat and mixed open.

Economic Calendar

Earnings Calendar

On the hump day earnings calendar, we have more than 100 companies listed, but a considerable number of them are not verified. Notable reports include WBA, MU, AYI, AESE, FUV, CONN, DGLY, GES, NG, & VRNT.

News and Technicals’

President Biden will unveil his infrastructure plan with more than $2 trillion in government spending over the next 8-years. Included in the proposal is a Corporate Tax increase to 28%. The second part of his plan will include Health Care and child care spending of another $2 trillion. The Amazon-backed food delivery company, Deliveroo, had a rough beginning in its London IPO, dropping over 30%. Those pesky 10-year Treasury bonds pulled back slightly yesterday but currently holding a 1.73% keeping the pressure on inflation worries. The Fed is also under pressure after the Case-Shiller Index posted housing prices were up 11.2% year over year, which is the most significant annual increase in more than 15-years. Critics point out the Fed is responsible for the sharp inflationary spike in housing due to its commitment to near-zero rates and its continued buying of mortgages- backed securities that total more than $2.2 trillion. The Fed now owns a full 1/3rd of the mortgage-backed securities market!

On the technical front, the DIA trend remains very bullish, and SPY is in good shape holding above price supports though it still struggles to join in on the record-breaking levels. IWM had a good day with the bulls defending critical price support as the financial sector gained ground. The QQQ continues to languish under its 50-day average, weighed down by rising bond rates. Jobs data will focus on the remainder of the beginning, with the private payroll number this morning. Keep in mind as you plan your risk forward of the Good Friday market shutdown.

Another day and another record close for the DIA, but it’s not all the sunshine and roses the bulls hoped for as the NASDAQ continues to languish below the 50-day average. With the 10-year Treasuries topping 14-month highs this morning, inflation worries could once again weigh heavily on the tech sector, adding an uncomfortable level of market uncertainty. Leaving behind a mixed bag of results in the indexes, it’s hard to be a committed bull and just as hard to be a committed bear. That said, traders should prepare for more volatile price action such as intraday whipsaws or complete reversals.

Asian markets closed with modest gains across the board overnight, with the HSI leading the way up 0.84%. European markets are also bullish across the board this morning, showing modest gains. With bond rising and a Consumer Confidence report at 10 AM, Eastern U.S. futures currently point to a mixed open. Stay focused and flexible as investors sort out their inflation concerns.

Economic Calendar

Earnings Calendar

On the Tuesday earnings calendar, we have 76 companies listed, but a significant number of them have not verified once again. Notable reports include CHWY, BEEM, BNTX, BB, FDS, LULU, MKC, PVH, QUWI, & XL.

News and Technicals’

Another record close of Dow after a choppy price action day with the VIX climbing back above 20 handles. The 10-year Treasuries is once again pushing higher, hitting a 14-month high touching 1.77%. In a joint letter published in newspapers worldwide, global leaders called for a pandemic treaty to improve cooperation and transparency. Signers to the letter included Prime Minister Boris Johnson, French President Emmanual Macron, and German Chancellor Angela Merkel. The U.S., China, and Russia have not signed on the Idea as of now.

We had a mixed bag of results in the indexes yesterday, with the DIA closing at record highs while IWM left behind a bearish evening star pattern. The bulls fought pretty hard in the QQQ lifting the index to its downtrend, printing an unconvincing hanging man pattern at resistance as it continues to struggle beneath the 50-day average. Recovering from early losses, the SPY tried to breakout but by the end of the day settled back to close below Friday’s close, unable to follow-through but perhaps just taking a rest above a price support level. Unfortunatunally, the VIX popped back above 20 handles, and the absolute breadth indicator indicated a lack of bullish momentum with more stocks declining or moving sideways than rising. Futures are mixed this morning, with rising bond rates likely rising inflation concerns once again. A few notable earnings reports and a reading on Consumer Confidence numbers are ready for yet another day of volatile price action.

The Dow set a new record high with a last-minute surge as the dark pool activity consolidated to the market. Both the DIA and SPY are in good technical condition, while the QQQ struggles in a downtrend. With a light day on the earnings and economic calendar, the market may be a bit more sensitive to the news cycle today. According to the VIX, fear is finally declining, but as traders can attest, the wild whipsaws in price action remain challenging. Plan your risk carefully as that condition is likely to continue.

Asian market closed higher in a volatile session with Nomura shares plunging 16% due to a U.S. hedge fund. Credit Suisse is also sliding sharply across the pond as European markets trade modestly higher with the U.K. relaxing pandemic restrictions. The U.S. futures point to a lower open this morning but are well off of overnight lows. Be careful chasing, and don’t be surprised if overnight lows receive a test as support.

Economic Calendar

Earnings Calendar

To kick off the last 3-days of the quarter, we have 69 companies listed on the earnings calendar, with a large number of them unconfirmed. The only verified potential notable report is from CALM.

News and Technicals’

With an end-of-day surge as the dark pool trading consolidated to the market, the DIA reached a new record high, and the SPY cleared some price resistance. President Biden is under pressure considerable pressure with more than 100,000 illegal immigrants crossed the border in February. Biden is also intending to push for the 4 trillion dollar infrastructure plan before moving on to his next phase of health and family care. Let’s hope we don’t run out of ink to keep printing money! A draft study jointly written by the WHO and China says animals are the likely source of the Covid outbreak. While France and Germany face a deteriorating public health situation, the U.K. is relaxing its restrictions allowing up to six people to meet outdoors. According to reports, the massive container ship stuck in the Suez Canal is not partially floated. Still, there is no indication of how long it will take to complete the operation and resume business.

On the technical front, the indexes got a big shot in the arm in the last few minutes of trading. The DIA managed a new record high by a few ticks, and the SPY lept above some concerning price resistance. At the same time, the QQQ lagged, remaining in a downtrend, as did the IWM. After another wild session, the VIX closed below a 19-handle, suggesting fear is diminishing, but clearly, the wild intraday whipsaw continues. In this all-or-nothing market, the T2122 indicator went from an oversold to indicating a possible overbought condition in just two trading days. As the morning pump begins, futures are well off of overnight lows but, as of now, suggest a lower open. I suspect another wild week of price is ready to begin.

The big question of the day, can the bulls follow-through with yesterday’s nice relief rally clearing some of the overhead price resistance? A weak 7-year bond auction has treasury yields ticking higher this morning to worry investors about coming inflation pressures. Additional pressures of the already strained supply chain may factor with the blockage of the Suez Canal that could take weeks to clear. Be careful not to chase or overtrade and remember as the futures pump up the open the pop and drops that occurred all week.

Asian markets caught some seeling relief overnight, seeing green across the board to end the week. European markets are also seeing some modest relief this morning following a better-than-expected global sentiment report. Ahead of possible market-moving economic reports and a light day on the earnings calendar, the bulls are working hard in the futures to continue yesterday’s bounce.

Economic Calendar

Earnings Calendar

On the Friday earnings calendar, we have a light day with 36 companies listed but only a handful of verified reports. There are no notable reports today.

News & Technicals’

Markets enjoyed a nice relief rally yesterday despite some concerning news. North Korea has kicked up its heels again, firing two ballistic missiles increasing the foreign policy challenges for President Biden. A blockage in the Suez Canal is delaying an estimated $400 million in goods every hour, adding worries to an already strained supply chain. Estimates suggest it could take weeks to clear the blockage. Social Media once again came under fire as pressure increases to change laws placing liability on the company for the content posted. I suspect substantial social media changes are on the way.

The challenge for the market today is follow-though with yesterday’s relief rally bounce. The DIA held nicely on its uptrend, and the SPY, through briefly falling below its 50-day average, proved to hold this critical psychological level by the close. As nice as it was to see the bulls fighting back, they still have some substantial overhead resistance hurdles in their path. The 10-year treasury is ticking up this morning to 1.65% after a weak 7-year bond auction. Big tech could continue to struggle with the rising yields and the growing political pressure they face in congress. Futures suggest a bullish open ahead of potentially market-moving economic reports, so be ready for volatility. As we know, the morning pump has created nasty whipsaws in price action this week. Stay focused and flexible.

Treasury yields are rising this morning after another frustrating whipsaw spanning more than 600 Dow points closing all four indexes lower on the day. Lower highs and broken price support levels in the SPY, QQQ, and IWM should raise caution levels while the DIA continues to enjoy bullish leadership. With the Powell speaking tour behind us, keep a close eye on those treasury yields, and overhead price resistance as the indexes search for direction and momentum.

Asian markets closed mixed overnight, with tech suffering significant losses with the SEC adopting a new law that could delist Chinese companies from U.S. Exchanges. European markets trade modestly red as another pandemic lockdown weighs on investor sentiment. Ahead of the GDP and Jobless Claims futures at trying one again to pump up premarket.

Economic Calendar

Earnings Calendar

The Thursday earnings calendar has 70 companies stepping up to report, but there are many unconfirmed numbers. Notable reports include BLNK, DRI, MOMO, MOV, & CLDX.

News & Technicals’

Treasury yields are pushing slightly higher again this morning, trying to hold onto bullish trends despite the very dovish Fed. AstraZeneca revised its vaccine data, indicating a lower efficacy rate after being called on the carpet for releasing outdated data. The SEC has opened an inquiry into a special purpose acquisition company (SPACs). The SEC is asking banks to provide information voluntarily, but according to the enforcement division, it could be a precursor to a formal investigation. There will be another hearing today in Congress as the CEOs of Facebook, Google, and Twitter face more questions about the spread of misinformation across social platforms. Chinese tech stocks have a rough night after the SEC adopted a law called the Holding Foreign Companies Accountable Act on Wednesday. Companies unwilling to meet the provisions of accounting could be de-listed from U.S. stock exchanges.

Yesterday proved to be another disappointing whipsaw that covered more than 600 Dow points. Although the technical damage is not severe except in the tech sector, investor confidence is taking some damage as the wild swings continue to chop up trading accounts. That said, the futures are once again working to pump up today’s open even after a rough night for Asian markets and a very cautious start in European indexes. As long as traders are willing to chase the moring pump, there is no reason it can’t continue. Swing and position traders I likely finding this price action very frustrating, while experienced day traders are likely having a field day with the huge whipsaws. We are finally past the Powell speaking fest but face the potential market-moving economic reports of GDP and Jobless Claims before the open. Remember, one of the great thing about being a trader is that we can choose to stand aside protecting our capital when feel you have no edge. Just because the market’s open does not mean you have to put money at risk. Ask yourself, are you addicted to risk, or does your action constitute a good business decision?

Elon Musk says you can now use bitcoin to your new Tesla, and at the same time, a Central Banker calls for more regulation on cryptocurrencies. Hmm. Yesterday’s selling came as worries over pandemic infection rates rise around the country, diminishing hopes of a summer recovery. Unfortunately, the selling added to the technical damage in the index charts. The bulls will have a lot of work ahead of them to recover overhead resistance levels in the SPY, QQQ, and now the IWM. Be careful as this choppy and whipsaw-riddled price action tends to chop up trader’s accounts.

Asian markets retreated overnight, closing red across the board with the NIKKEI and HIS down more than 2%. European markets trade with modest losses across the board as recovery concerns weighs on investors. However, here in the U.S., the premarket futures point to bullish open ahead of earnings, Durable Goods Orders, and another round of Powell testimony. Expect the choppy price volatility to continue.

Economic Calendar

Earnings Calendar

On the hump day earnings calendar, we have 53 companies listed, but only half verified they would reveal quarterly results. Notable reports include KBH, GIS, FUL, RH, SCVL, TCEHY, WGO & WOR.

News & Technicals’

You can now buy your new Tesla using bitcoin, but Agustin Carstens from the Bank for International Settlements calls for regulation of what he called a ‘’speculative vehicle’. Interesting considering many central banks are actively exploring their digital currencies. Intel is working hard to get back on top with plans to make chips for other companies and spend 20 billion to build two new chip plants in Arizona. The wildly speculated GME shares fell 12% as the company said it might sell stock to fund a transformation. During the conference call that at one point reached maximum capacity, the company declined to answer any questions. No surprise that the company missed on both the top and bottom line.

Yesterday was a disappointing day in the indexes as the bear returned, adding more technical damage to the charts and essentially reversing the bullish hope of just one day ago. The culprit this time is the rising infections across the U.S. and lockdown in Europe as recovery hopes diminished. However, this morning the bulls are once again trying to pump up the sentiment in the premarket. We have Powell speaking again today, and so far, he seems to have calmed the bond market with his extremely dovish comments. In this choppy market environment, I’ve been hearing from many traders having their accounts chopped to pieces. The super bullish momentum has faded, making this a stock pickers market. Chasing and complacency are very dangerous.