With last week’s strong bullish performance, the Dow finally pushed through its 50-day average, rising more than 1100 points in just 5-trading days. It will not be interesting how it deals with its downtrend resistance as the SPY and QQQ push for more records with big tech leading the way. As we slide toward the end of the quarter and the 4th of July holiday, can the bulls keep up the pace, or will they need a rest this week? Logic would say yes, but in this all-or-nothing high emotion market, I’m not sure logic applies. Stay with the trend all long as it continues but avoid complacency in this very stretched condition.

Asian markets saw red across the board overnight though the losses were modest. European markets are also showing modest declines across the board as the rise in pandemic infections weigh on sentiment. Ahead of a light day, earnings and economic data futures indicate a mixed but modest open as we slide toward the end of the 2nd quarter.

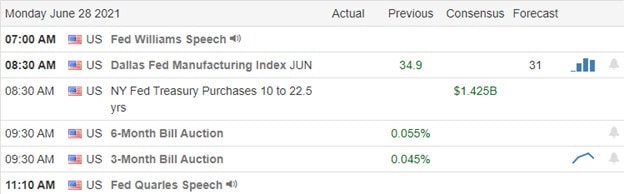

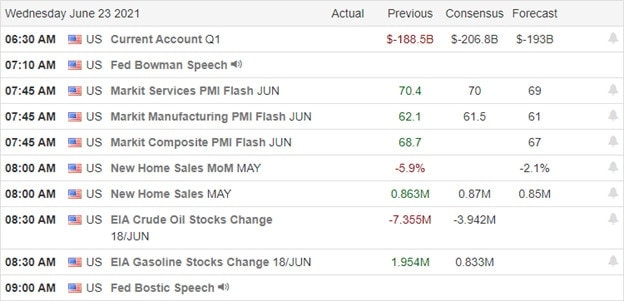

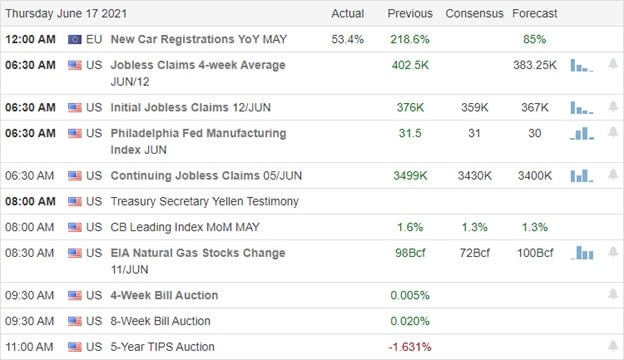

Economic Calendar

Earnings Calendar

We have a light day on the earnings calendar with just four verified reports to kick off the week. The only somewhat notable report is MLHR.

News & Technicals’

Britain’s Financial Conduct Authority said that Binance Markets Limited “is not permitted to undertake any regulated activity in the U.K.” It’s the latest sign of a growing crackdown on the crypto market from regulators around the world. After losing a confidence vote in parliament on June 21 after the left party withdrew its support, the Swedish prime minister resigned after losing a confidence vote in parliament. The 10-year treasury is easing slightly this morning, declining to 1.516% and the 30-year slipping to 2.143%. U.S. Senator Rob Portman, R-Ohio, said Sunday that the bipartisan infrastructure deal could move forward, following President Joe Biden’s clarification that he’ll sign the bill even if it comes without a reconciliation package. The president last week said that he would refuse to sign the deal unless the two bills came in tandem, a remark that angered and surprised Republican lawmakers.

After rising more than 1100 points in last week’s bullish surge, the Dow recovered its 50-day average and is now testing its downtrend as resistance. The rally led by strong bullishness big tech seems unconcerned about inflationary pressures, supply chain challenges, and antitrust efforts in Europe and those moving forward in the U.S. Though technically a bit stretched out, the trends in the SPY and QQQ showed no signs of slowing down by the close on Friday. After such a strong bull run, one has to wonder, can it continue this week, or will we need a little rest or even a profit pullback to check support levels. We have a light earings calendar as we slide toward the end of the 2nd quarter, with not much on the economic calendar to begin the week to inspire. Moreover, it is possible by mid-week that volumes may begin to decline as trader extend their 4th of July holiday.

A deal on infrastructure and another Trillion in deficit spending inspired the bulls to record highs in the SPY and QQQ, with the technicals in the DIA and IWM continuing to improve. After the bell, the big banks all passed their stress tests, and blowout earnings from NKE continued to inspire buyers in the overnight futures session. Assuming we get past the pesky inflation data coming out before the bell, it looks like we can bullishly party on right into the weekend.

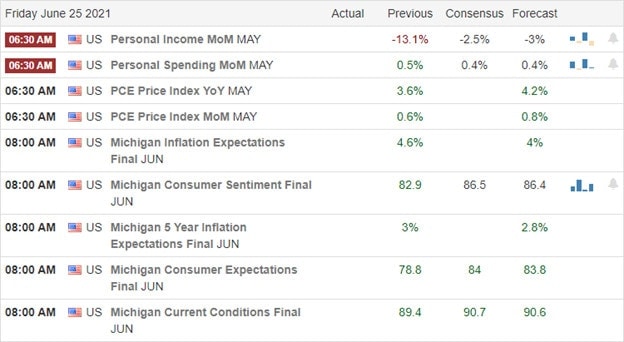

Asian markets closed green across the board, lead by the HSI, which surged 1.40% by the close. Across the pond, European markets trade mixed with inflation worries and fears of tapering raising caution. However, U.S. markets don’t seem to at concerned about inflation, pointing to a bullish open ahead of key inflation data. After such a strong recovery rally, don’t forget to take some profits as we slide into the weekend.

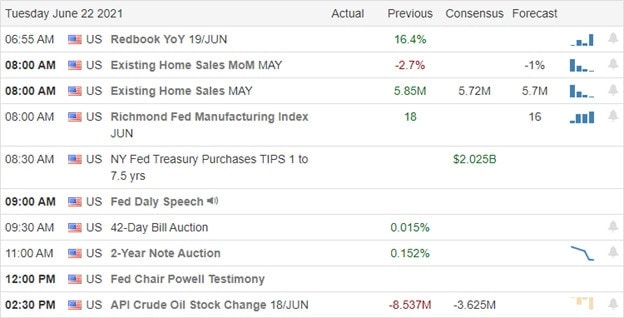

Economic Calendar

Earnings Calendar

On the Friday earnings calendar, we have a total of 16 companies listed, with just six verified reports. Notable reports include KMX, JKS, & PA.

News and Techinicals’

The big banks get clean bill health after all passing their stress tests as expected, with the FOMC continuing to push 120 billion a month. A bipartisan Senate group agreed on an infrastructure bill totaling nearly $1 Trillion without a plan to pay for it other than printing more money. The market surged high on this news because there is nothing this market likes more than deficit spending. It makes you wonder if they will be as inspired when it comes time to pay the piper? According to the National Association of Manufacturers, supply chain disruptions and inflated prices are not diminishing due to workforce shortages, and demand exceeds supply. Hackers are now attacking PC gamers with the malware “Crackonosh” hidden in free versions of games. Once installed, it hijacks the computer’s processing power to mine cryptocurrencies for the hackers. The 10-year Treasury yields edge higher this morning ahead of inflation data, trading this morning at 1.489%, with the 30-year dipping slightly to 2.093%.

Yesterday’s big gap up at the open quickly lost momentum until the announcement of another trillion of deficit spending was on the way for infrastructure. For now, deficit spending is like stock market crack, and we can’t seem to get enough these days. New records in the SPY and QQQ and the technicals continued to improve in the DIA and IWM. After the bell, the banks passed their stress tests, continuing to inspire the bulls in the overnight futures session with the DIA set to recover its 50-day on the opening gap. There is just one hurdle to cross this morning on inflation with the Personal Income and Outlays report before the bell. If there is no stumble there, a bullish push to close the week strong looks very likely. Party on!

The indexes chopped in a very tight range yesterday, but despite the uninspired price action, the NASDAQ was able to post its 16th record high this year. The tech sector continues to surge upward even as the antitrust bills aimed at the tech giants move forward with bipartisan support. The Dow remains the weakest of the indexes, still languishing below its 50-day average. However, the overnight surge in bullishness ahead of market-moving economic reports could test that resistance level in the Dow and may even break the SPY to another record high. Amazing!

Overnight Asian markets closed the day mixed in a choppy flat session. However, Europiean markets are decidedly bullish this morning after digesting Fed comments of longer-lasting inflation pressure. Though uninspired yesterday the bulls are pushing hard this morning in the premarket futures ahead of retail sales, GDP, and Jobless data. Fasten your seat belt; it could prove to be a wild price action morning.

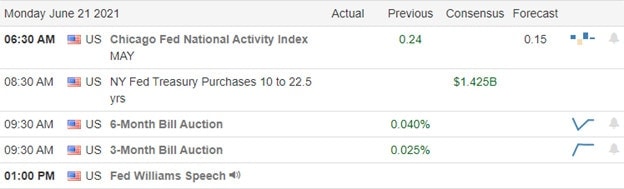

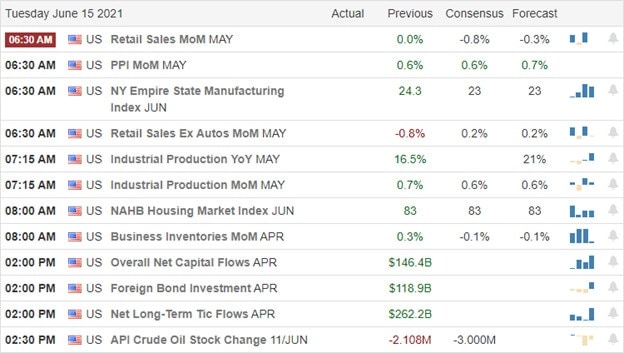

Economic Calendar

Earnings Calendar

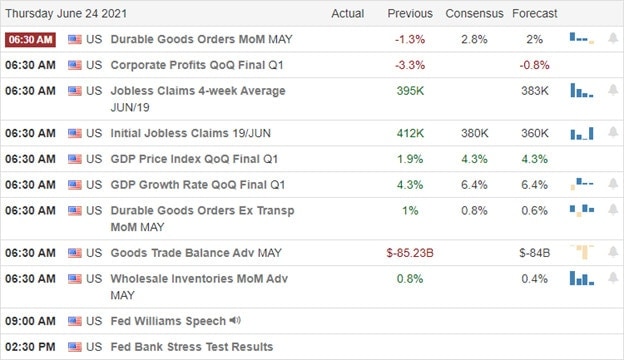

The Thursday earnings calendar is the busiest of the week, with 16 companies stepping up to report quarterly results. Notable reports include FDX, NKE, CAN, BB, DRI, RAD, & WOR.

News & Technicals’

After the bell today, we will hear the results of the banking stress testing. The big banks had a bumper year in with the Fed pumping money to them, and most expect all will pass the test. I would expect the banks will immediately announce stock buy-backs and increased dividend payments. The Amazon Prime day event looks to has set new records in the U.S., with sales totaling 9 to 12 billion, according to Adobe analytics. Despite massive lobbying efforts, the U.S. House Judiciary Committee voted to approve a bill to give antitrust enforcers more money as antitrust efforts aimed at tech giants in anti-competitive abuses. Treasury yields move higher this morning after Fed officials warn of longer-lasting inflationary pressure, with the 10-year rising to 1.502% and the 30-year climbing to 2.129% ahead of retail and GDP data.

Though the market marketed time chopping sideways, the NASDAQ managed to squeak out its 16th record high this year. Rather remarkable, in my humble opinion, the U.S. House voted to increase funding as the bipartisan aimed at the tech giants move forward. Moreover, with the Fed officials warning of a long-lasting inflationary environment, traders appear to no concern with futures pointing to new record highs at the open. The struggling financial sector could get a boost later today as the Fed releases the bank stress test results. Reports are already inferring they all passed with easy money continuing to flow to them from the Fed. With retail sales, GDP, Trade, and Jobless numbers before the bell, anything is possible by the open, and the premarket pump pushes for new records.

With the NASDAQ setting a new record, and the SP-500 within striking distance, the index technicals’ improved through overhead resistance in the DIA, IWM, and SPY are still a concern. The Dow remains the most significant concern after rallying 670 points off Friday’s low; it must yet deal with its 50-day average as resistance. Despite antitrust probes and bipartisan-supported proposed antitrust legislation, the tech giants did the vast majority of the market recovery, with Microsoft briefly hitting a two trillion market cap. We’ve come a long way in just two trading days. Remember to take some profits!

Asian markets traded mixed overnight, but the HSI was on fire, surging 1.79% by the close. With a stronger than expected PMI and inflation worries creeping in, European markets trade primarily in the red this morning though the FTSE is clinging to modest gains. Ahead of earnings and housing data, the U.S. futures currently suggest a flat to modestly bullish open. As you plan your day, keep a close eye on overhead resistance levels that may harbor entrenched bears.

Economic Calendar

Earnings Calendar

On the hump day earnings calendar, we have nine companies listed on the calendar though some are unconfirmed. Notable reports include FUL, INFO, PDCO & WGO.

News & Technicals’

Although pressed several times pressed with hyperinflation questions, Jerome Powell stuck to his guns, suggesting the recent spike is likely temporary. All we can do is hope he’s right as the Fed continues to pump 120 billion a month into the system. The China crypto crackdown continues to impact Bitcoin prices falling below 30,000 once again. The new Delta variant of Covid is likely to become the dominant strain in the next couple of weeks, according to Dr. Fauchi. He has declared this strain as the greatest threat to the attempt to eliminate the virus. In the U.K., consumer price inflation came in 2.1%, and chief economist Andy Haldane urges policymakers to cut their quantitative easing program or risk what he calls the “tiger of Inflation” incoming. The Eurozone business activity surged to its highest levels in 15-years. However, as inflation worries crop up worldwide, U.S. Treasury yields saw little movement this morning, with the 10-year holding at 1.472% and the 30-year drifting slightly lower to 2.102%.

The index technicals improved substantially, with the tech giants doing the vast majority of the heavy lifting. The NASDAQ closed at a new record high, and the SPY is within striking distance of new records though the index has more stocks moving sideways to down than those moving up. The DOW remains the weakest of the indexes, still below its 50-day average though it has surged 670 points off Friday’s low in just two trading days. The VIX has calmed substantially but has not made a new low as one would expect, with new index records being set. That said, traders should remain vigilant as huge price volatility is possible with the DIA, SPY, and IWM still facing overhead resistance. Remember, when the market moves big, it’s a good idea to take some profits along the way.

After Friday’s ugly selloff, the relief rally to fill the bearish gap was a nice reprieve. The SPY and IWM recovered nicely, closing above their 50-day averages, while the DIA remains the weakest index with substantial overhead resistance yet to overcome. Speculation and emotion are running high, as evidenced by the back-to-back 600 point swings. The wild price action favors day traders but makes it near to impossible to have an edge as a swing or position trader. Be very careful chasing buys as we test overhead price resistance levels that may have entrenched bears willing to defend.

Overnight Asian mostly rallied, with the NIKKEI leading the way, surging 3.12% through the HSI continued to drift south. European market trade mixed this morning with modest gains and losses as trade inflation and interest rate fluctuations. Ahead of a light earnings calendar and Housing numbers around the corner, U.S. futures have bounced off overnight lows but currently point to a flat open. After yesterday’s big relief rally, a little rest is not out of the question.

Economic Calendar

Earnings Calendar

On the Tuesday earnings calendar, we have just eight companies listed, with only half verified. Notable reports include KFY and PLUG.

News & Technical’s

The assault on the big tech’s continue with European Commission opened an antitrust investigation into Google. According to the report, the probe is looking into the advertising unit that has made it harder for rival online advertising services to compete. China’s illegalization of nongovernmental sanctioned cryptocurrencies has taken a toll on Bitcoin that has lost $300 billion in value since last Friday. Chinese authorities in the Sichuan province ordered crypto miners to shut down operations, and the Bank of China urged financial institutions not to provide crypto services. Fed Chairman Jerome Powell said in testimony prepared for delivery to Congress that the economy is growing, but faces continued threats from the Covid pandemic. He said inflation has risen “notably” but repeated his position that the price pressures are transitory. He has a story, and he’s sticking to it! The 10-year treasuries yields increased slightly this morning to 1.501%, and the 30-year advanced to 2.115%.

Yesterday’s relief rally filled the bearish gap left behind in Friday’s price action in the DIA, SPY, and IWM. The DIA remains the worst technical condition remaining below its 50-average with substantial overhead price resistance yet to overcome. However, the SPY and IWM recovered their 50-day averages but still have to price resistance levels above to yet to overcome. The SPY remains in a bullish trend even as semiconductor stocks suffered a pullback due to the China crypto mining crackdown. I wouldn’t call the 600 point swings in the last two days trading days healthy price action. In fact, it’s difficult to impossible for swing and position traders to have an edge in this kind of trading environment. Big price swings and high volatility favor the day trader. As the index charts approach price resistance levels, be prepared for the possibility of bearish pushback. Expect price volatility to remain high, with large intraday whipsaws and overnight reversals possible.

As the bears rode roughshod over the market to end the trading week, some significant technical damage was created in the index charts. With more economists warning of a possible 10 to 20 percent correction, price volatility can become quite extreme as emotions run high between those wanting to rush in and buy the dip and those welcoming the correction in prices. If this is the beginning of a correction, big daily price swings are possible with overnight reversals and intraday whipsaws to challenge trader skills. Observe price resistance levels as possible areas of bear attacks.

Asian markets had a rather rough night of trading with the Nikkei, leading the selling down 3.29%. However, European markets are trying to bounce off last week’s lows this morning, showing green across the board but modest gains thus far. Here in the U.S., we don’t do modest much anymore. We either rush in or run for the door, and this morning is no exception, with futures surging higher off of overnight lows. Watch for violent price action and big price swings as the bull and bears duke it out in early trading.

Economic Calendar

Earnings Calendar

We have another light day on the earnings calendar to begin a new week of trading with just five companies listed with the report from NPSNY as only one verified.

News & Technicals’

Bitcoin fell 7% Monday morning as the China crackdown on cryptocurrency mining extended to the southwestern provinces of Sichuan. Another economist Mark Zandi has joined the chorus of economists warning that inflation headwinds could create a 10 to 20 percent correction. Adding it may take a year to recover to just the break-even level. Staffing issues that are in turn creating maintenance issues have caused American Airlines to cancel hundreds of flights. According to the report, about half the cancellations were because of unavailable flight crews. Supply chain issues are likely to affect the Amazon Prime Day sales that began at midnight Monday. Businesses reported they are being hit hard by global shortages of shipping and semiconductors, while some worry they may run out of stock during the massive sales event. Treasury yields have fallen to a two-month low, with the 10-year trading at 1.438% this morning as the 30-year rose slightly to 2.043%.

A rough week of selling left some significant technical damage in the index charts. The SPY, DIA, and IWM closed below their 50-day averages. The QQQ fends off the bears as the tech giants resisted the selling pressure holding onto price support levels as well as the current bullish trend. Fear spiked, closing the VIX above a 20 handle and well above its 50-day average while the Absolute Breadth Index registered a rise in momentum on the selling wave. If this is the beginning of a correction, we can expect the price action to become very volatile, with overnight reversals and intraday whipsaws becoming commonplace. This morning a short squeeze may be possible but be careful with rushing in to buy the dip if prices remain under resistance levels where the bears might be digging in defenses. Big daily price swings are possible, so plan your risk carefully and avoid complacency.

The tech giants almost single handily lifted the QQQ to new record highs while China’s plan to release reserves toppled trends in inflationary stocks and commodities. At the same time, the DIA suffered technical damage in a wild price action day with a substantial whipsaw intraday. With price volatility so high, day traders likely have the upper hand, while swing and position traders may find the whips in price action challenging to downright unsavory.

While we slept, Asian markets closed mixed through the HIS rallied 0.85%. European markets are decidedly bearish this morning as the tumble in commodities continues. The U.S. futures currently point to a lower open with a very light day of earnings and economic data to provide inspiration as we slide into the weekend. Should the tech titans happen to turn south, it could be a painful day.

Economic Calendar

Earnings Calendar

We have a very light day on the Friday earnings calendar with just 3-companies listed and only one verified report coming from GLBS, which is not particularly notable.

News & Technicals’

Commodities plunged yesterday as China announced a plan to release reserves of metals that included Copper, Aluminum, palladium, and platinum. The move caused a spike in the U.S. dollar, also affecting Gold and Silver, as well as oil and grain futures. That said, we can expect most of the prices to recover due to the rising inflation. Morgan Stanley has upgraded Occidental due to higher prices suggesting a 40% increase in the stock. Exon Mobil received a similar upgrade earlier this week. Remarkably with inflation on the rise, the 10-year Treasury note fell this morning to 1.477%, and the 30-year dipped to 2.067%, likely giving the Fed a sigh of relief. The Covid-19 delta variant initially discovered in India is now spreading around the world, becoming the dominant strain in some countries, such as the U.K., and likely to become so in others, like the U.S. The variant now makes up 10% of all new cases in the United States, up from 6% last week. Studies have shown the variant is even more transmissible than other variants.

Yesterday’s price action saw traders rushing into the tech giants lifting the QQQ to new record highs. At the same time, the DIA suffered some technical damage following through to the downside after failing its 50-day average on Wednesday. With 40% of the SPY weighted by the tech giants held its ground but fell just short of breaking back above price resistance, and though the IWM recovered substantially, it has the uncertainty of a lower high followed by a lower low. China’s action tossed a monkey wrench into inflation-related stocks breaking established trends adding another layer of uncertainty as to what happens next. One thing for sure is that price volatility and huge intraday whipsaw will keep us all guessing. Stay focused and flexible as we slide into the weekend. Happy Father’s day!

The Fed decided to stay the course, continuing to buy $120 Billion in debt per month as the FOMC acknowledged rising inflation is more substantial than expected. Though the initial reaction to the statement brought out the bears, the bulls charged back in a late afternoon rally. The only index suffering some technical damage was the DIA which closed below its 50-day average. Long story short, stay with the trend because the market no longer cares about debt or inflation.

Asian markets traded mixed overnight, with the Nikkei slipping nearly 1% while the HIS rallied. European markets are pulling back modestly this morning across the board. Ahead of earnings, Jobless claims, and manufacturing data, U.S. futures point to a modestly bearish open after rallying well off the overnight lows. Stay focused and watch for whipsaw moves as the bulls and bears sort out dominance issues with overhead resistance levels as the battleground.

Economic Calendar

Earnings Calendar

We have a slightly busier day on the Thursday earnings calendar, with eight companies reporting. Notable reports include ADBE, JBL, KR, & SWBI.

News & Technicals’

Eleven Republican senators now support a bipartisan infrastructure framework, which would give a bill enough votes to pass the Senate if all Democrats get on board. However, several liberal senators have signaled they could oppose the bipartisan plan, saying it does not go far enough to fight climate change or income inequality. China launched the first astronauts into space on Thursday as China challenges the U.S. in several technology areas. The bill to make Juneteenth the 12th federal holiday sailed through Congress, passing the Senate by unanimous consent with the House passing the bill just one day later sending it on to the President to sign into law. After spiking yesterday, U.S. Treasury yields drifted lower Thursday morning, with the 10-year coming in a 1.56% and the 30-year dipping to 2.179%.

The FOMC acknowledged rising inflation suggesting a rate increase is possible sometime in 2023 while at the same time continuing to buy debt at $120 billion per month. The initial negative reaction whipsawed yesterday afternoon as buyers rushed back in after the press conference. Though the SPY, QQQ, and IWM recovered substantially, the DIA suffered some technical damage closing below its 50-day average. If the highest PPI on record is of no consequence to the market and the Fed continues to grow their more than 7 Trillion balance sheet, I guess the new normal is no financial metric matters anymore! Stay focused on price action and stay with the trend as long as it lasts.

Ahead of the FOMC meeting, the tech giants lifted the SPY and QQQ to new record levels almost entirely on their own as the vast majority of the stocks slid sideways or south yesterday. At the same time, new records were made, the VIX rallied slightly, and the absolute breadth index continued to decline with the lack of momentum. Hedge fund manager Tudor Jones says go all-in on inflation trades if the Fed stays the course or expect a “taper tantrum,” should they make a course correction. We will find out Wednesday afternoon what their decision will be, so plan your risk accordingly.

While we slept, Asian markets traded mixed with the Nikkei surging up 0.96% while the Shanghai fell 0.91%. However, European markets this morning work for modest gains and new records cautiously waiting on the FOMC. With a significant economic data dump, futures in the U.S. trade mixed, and flat as the Fed beings its 2-day meeting. Will they or will they not react to inflation? Market direction may well be determined by the answer at 2 PM Eastern tomorrow.

Economic Calendar

Earnings Calendar

On the Tuesday earnings calendar, we have 18 companies listed, but a large number of them are unconfirmed. Notable reports include HRB, ORCL, & LZB.

News and Technicals’

New closing records in the QQQ and SPY supported almost entirely by the tech giants, with the rest of the market largely sliping sideways or south. According to Jamie Dimon, JPMorgan is hoarding cash rather than buying Treasuries or other investments due to the possibility of higher inflation that’s here to say. He is one of the first investment banks to break ranks with the idea that the spike in inflation is transitory. Hedge fun manage Paul Tudor Jones suggested to “go all-in on inflation trades” if the Fed stays the course and ignores the spike in inflation. Tudor says the market will experience a “Taper Tantrum if they do make a course correction.” Interestingly trade doesn’t seem to share the same inflation concerns, with the 10-year treasury notes falling to 1.484 this morning and the 30-year dipping to 2.176%. Could it be complacency has raised its ugly head?

Today begins the 2-day FOMC meeting and a substantial economic calendar data dump that could inspire and bring in some early price volatility. As the QQQ and SPY set new records, the T2122 indicator slid south, and the absolute breadth index declined, with just a select few tech stocks doing the heavy lifting. That said, the SPY and QQQ index charts hold fast to bullish trends. IWM remains below overhead resistance while the DIA looks tired and the most at risk if the bears find some inspiration. As we wait on the FOMC decision, choppy price action would not be a surprise. However, with PPI, Retail Sales, Industrial Production, Housing, and Manufacturing numbers just around the corner, prepare for some early session volatility. Who knows, with so much data, the bulls or bears could find some inspiration to end this chop ahead of the Fed.

Though inflation came in very hot, the bulls and bears stayed evenly matched, producing choppy uncertain price action while clinging to trends yet challenged by overhead resistance. So now we likely hurry up and wait for the FOMC decision on Wednesday afternoon to see if they will be the tiebreaker of this momentum-less consolidation. Will they or won’t they begin to taper the easy money policies in response to inflation? That is the question to be answered!

During the night, Asian markets saw bullishness though some were closed due to holidays. European markets continue to push higher, setting new records this morning. With a light day of earnings and economic data, the U.S. point to a flat yet slightly bullish open, with the Nasdaq leading the way to test resistance highs. Watch for the pop the possibility of more pop and drops as we wait on the Fed.

Economic Calendar

Earnings Calendar

We have 12 companies listed on the earnings calendar with many unconfirmed earnings to kick off the week. The only somewhat notable report I can come up with today is HEXO.

News & Technicals’

Bitcoin is surging again this morning after Musk suggests Tesla may again accept cryptocurrency as payment. However, Sygnia CEO Magda Wierzycka lambasted him saying, “What we have seen with Bitcoin is price manipulation by one very powerful and influential individual.” Regulators may block Nvidia’s attempt to buy the chip designer Arm, whose energy-efficient chip architectures are used in 95% of the world’s smartphones. According to reports, Qualcomm is now interested in investing if NVDA is blocked. The biotech firm Novavas plans to file for authorization with the FDA in the third quarter after testing their Covid vaccine is safe and 90.4% effective overall. With the FOMC just ahead, the U.S. treasury notes rose slightly this morning, with the 10-year coming in at 1.464% and the 30-year climbing to 21.52%.

Though the bullish trends continue, the choppy uncertain price action and both the bulls and bears wondering what comes next. Floating on a river of newly printed money, the bulls want to keep the party going. However, the high inflation reading in last week’s CPI has the bears concerned, keeping them in play as well. So perhaps the FOMC will be the tiebreaker when they reveal their decision Wednesday afternoon. Will they begin to taper easy money policies or keep the pedal to the metal, pumping money into the system? We will know more Wednesday after the statement and the chairman’s press conference. Until then, the choppy uncertain price action is likely to continue, with various meme stocks surging here and there as they gamify stock trading. So maybe the best description of the first part of this week is, hurry up and wait!