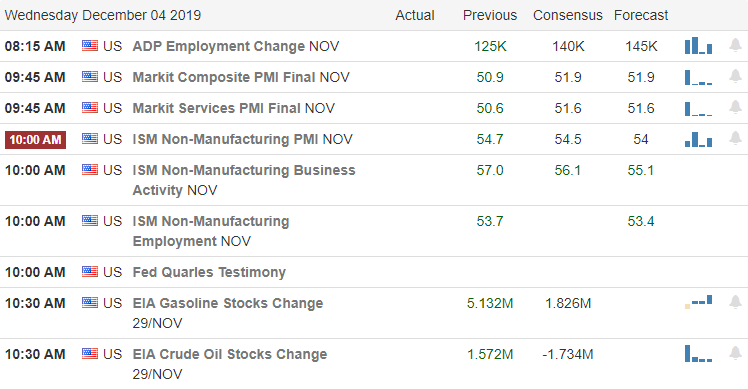

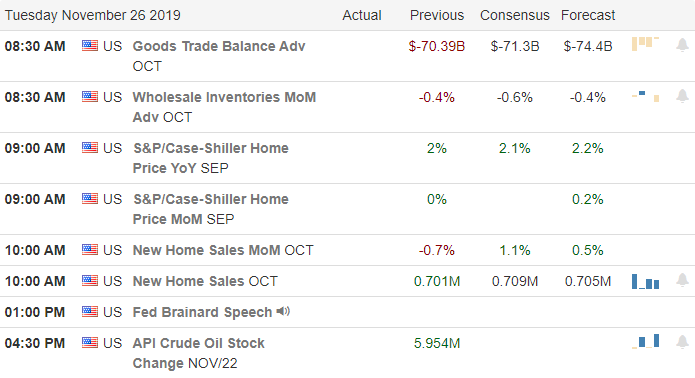

The so-called Phase 1 trade deal has become a ridiculous political

football creating a frustratingly news-driven market chopping up trader’s

accounts. The President says maybe we wait

until after the 2020 election, and the Dow drops more than 400 points. Bloomberg puts out a story citing “people

familiar with the talks,” and suggests a deal is edging closer, and the Dow gaps

up. All of the drams over a trade deal

that we no one really knows what it does or does not include. Silly!

The good news is that even though the short-term index trends broke

yesterday the bulls found the energy to defend important price supports and

longer-term trends. However, traders

will have to remain very nimble in this emotional football continues to be kicked

around.

Asian market closed seeing only red across the board overnight

with European markets in reaction to the Bloomberg story reversed early losses and

currently see green across the board. US

Futures ahead of earnings and economic reports are also reacting sharply higher

after the Bloomberg report with the Dow expected to gap up triple digits in

reaction.

On the Calendar

On the hump day Earnings Calendar, we have 31 companies

reporting their results. Notable reports

include RH, WORK, HOME, CPB, FIVE, HRB, RY, TLYS, and VRNT.

Action Plan

Yesterday the President said it might be better to wait

until after the 2020 election to make a deal with China. Commerce secretary came out echoing those

comments and said they have not ruled out imposing tariffs on imported European

Autos. Then at 5 AM this morning,

Bloomberg News reported that the US and China were edging closer to a trade

deal citing “people familiar with the talks.”

The Futures quickly rallied from overnight losses on the report. I don’t know about you, but all this market

manipulation around the so-called Phase 1 deal has become absolutely ridiculous.

Technically speaking, the short-term index trends broke

yesterday, but the longer-term bullish trends remain intact as bulls defended

key price action supports. Although

yesterday’s price action was quite bearish, the pullback may, in fact, open the

door to opportunity, so stay focused on price for clues. As a result of the Bloomberg report, the futures

point to a gap up open in the Dow of more than 100 points ahead of earnings and

economic reports. At 10 AM Eastern today,

impeachment hearings will resume providing a little distraction and drama to

the day.

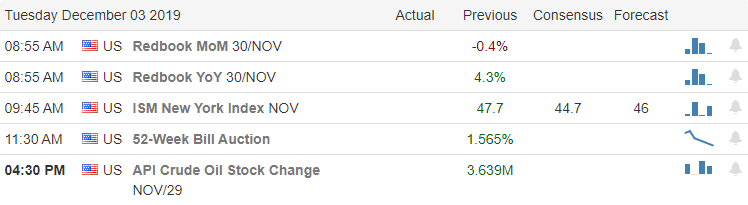

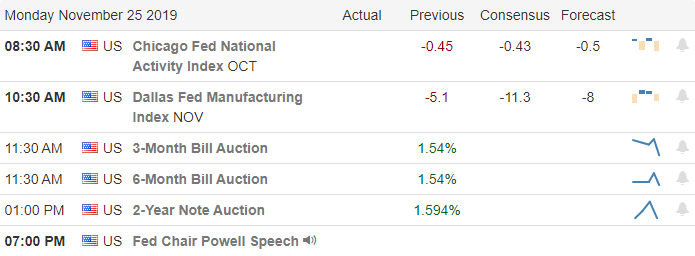

A miss on US Manufacturing and concerns of a US/China trade deal delay inspired the bears and triggered a wave of profit-taking yesterday. Threats of a possible 100% tariff against France in response to there new digital tax aimed at American companies as well as possible steel and aluminum tariffs for Argentina and Brazil added more pressure to the selloff. This morning the President raised concerns that the US/China trade agreement may not happen until after the 2020 election has futures pointing to more losses this morning.

Asian markets closed mixed but mostly lower overnight, with

Australia sinking more than 2%. Across

the pond Euro Zone indexes are mostly lower after the President’s comments on the

US/China trade delay. US Futures point

to a gap down open of about 100 Dow points following though after yesterday pop

and drop pattern leaving behind bearish engulfing candle patterns and lifting

the fear level in the VIX substantially.

Keep in mind that a pullback in a bullish trend may ultimately prove to

be a buying opportunity if the bulls prove strong enough to defend. So stay focused on the price for clues.

On the Calendar

On the Tuesday Economic Calendar, we have 20 companies reporting

quarterly results. Notable reports

include AZO, BMO, CONN, LE, MRVL, CRM, WDAY, and ZS.

Action Plan

The President’s trip abroad as proved to be quite eventful. After the passage of a digital tax in France targeting US companies, he has threatened new tariffs as much a 100% in retaliation. He also said steel and aluminum tariffs for Argentina and Brazil might be in play very soon. This morning the President suggested it might be better to wait until after the 2020 election to complete a trade deal with China sending the US Futures market sharply lower. All the while impeachment hearings resume on Wednesday here in the US while the President remains abroad scheduled to meet with the Queen.

Futures that had been modestly bullish most of the night now

appear to threaten a gap down this morning following through after Monday’s selloff. While the selling yesterday was worrisome, leaving

behind bearish engulfing candles, price supports, and overall trade largely

held up to the attack. However, follow-through

selling today may well create some technical damage to the index charts. The VIX closed the day just below a 15 handle

as fear quickly accelerated after the pop and drop day that energized the bears,

triggering a wave of profit-taking as trader scrambled to protect profits.

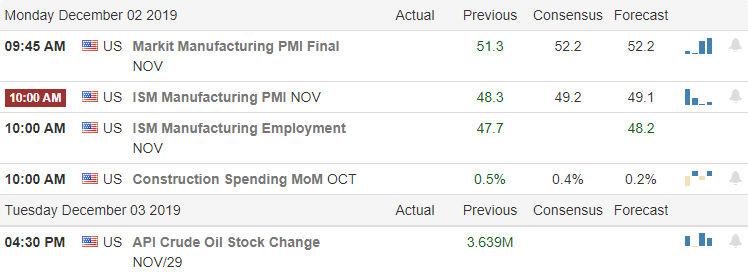

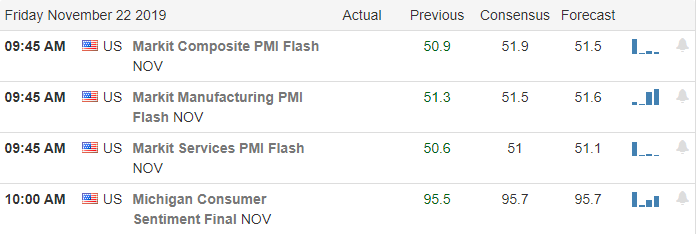

After a bearish short session on Friday, the bulls are trying to spark a rally this morning ahead of the PMI and ISM manufacturing reports. According to reports, the US consumer showed their confidence with an increase of 20% in Black Friday sales and an expectation that Cyber Monday could hit new record spending levels. That’s good for the economy but may prove to problematic for the market today with low volume as distracted traders search for online deals.

Asian markets were green across the board overnight fueled on better than expected Chinese manufacturing numbers. Unfortunately, the European markets are flat with mixed results as their manufacturing once again shrink. US Futures have pulled back from overnight highs as we wait on US Mfg reports at 9:45 and 10:00 AM Eastern. With Dec. 15th tariffs quickly approaching and China threatening retaliation for the bill supporting a Democratic Hong Kong, the path forward may have some new obstacles to overcome. As always, stay focused on price action for clues.

On the Calendar

On the Monday Earnings Calendar, we have a light day with

just 15 companies reporting as trading resumes after the Holiday. There are no particularly notable reports

today.

Action Plan

The market reacted negatively in the low volume, short

session, Friday after the President signed the bill supporting the Hong Kong

protesters. The December 15th

tariffs now come into focus as trade negotiations stall, and China threatens retaliation. On a positive note, holiday deal shoppers

were out in force with Black Friday sales up 20% according to reports. Retail is expecting today, Cyber Monday, to

set new sales records as consumers show signs of ramping up their holiday

online shopping.

Positive Chinese manufacturing data helped to boost overnight

markets, but Euro Zone manufacturing activity once again declined tempering

this morning’s bullishness. This morning

at 9:45 and 10:00, we will hear find out how US Manufacturing measures up with

the PMI & ISM reports. Consensus

estimates look favorable. Don’t be

surprised if volume quickly declines after the morning rush with traders extending

holiday vacations and distractions from Cyber Monday shopping.

The President’s positive comments on the Phase 1 trade

agreement has once again inspired the bulls to continue to reach out for new

highs. The earnings miss by DE has

dampened the overnight bullishness, but with a big morning of market-moving

economic reports that are expected to be positive according to consensus, all

signs point higher. Typically, after the

morning rush of activity, the volume will quickly diminish as traders set-out

to begin their holiday celebrations. Plan

accordingly.

Asian markets closed mixed but mostly higher with high hopes

news of a completed trade deal will be forthcoming. European are green across the board this morning

in response to the favorable trade comments by President Trump. US Futures point to modest gains at the open after

setting new records for the 10th time this month.

On the Calendar

On the pre-holiday Earnings Calendar, we have 21 companies

reporting quarterly results. Notable

reports include DE & DAKT, both reporting before the bell today.

Action Plan

President Trump has once again inspired the market this morning

suggesting they are very close to completing the Phase 1 trade deal. However, he also said they want to see a

democratic outcome in Hong Kong, which many see as a major obstacle to Chinese support. Yesterday, we saw record highs for the 10th

time in the last 30 days. Clearly, the

bulls are in control, and the trend remains very strong.

Although we have a rather light day on the earnings calendar

we have a very busy morning on the economic calendar with several potential

market-moving reports. The consensus

estimates of these reports are all positive, so only a major surprise seems capable

of derailing this relentless bull. Keep

in mind that volume is likely to decline very quickly after the morning rush as

traders head out for their holiday plans.

Although the market is open for short a session on Friday, the HRC and

RWO trading rooms will remain closed until Monday Dec. 2nd. I wish you all a very Happy Thanksgiving!

With the bulls inspired by Hong Kong election results, renewed

trade hopes, and a huge day merger news made setting new record highs in the DIA,

SPY,and QQQ look easy as they quickly recovered last week’s pullback. Today, the attention will likely shift to earnings

and economic reports to find inspiration.

After such a big move yesterday and heading toward a major holiday. It

will be interesting to see if bulls can find the energy to continue their relentless

march higher.

Asian markets closed mixed but modestly higher with Alibaba

making a huge splash in Hong Kong markets.

European markets are treading cautiously with mixed results as they

continue to monitor US/China trade news.

US Futures are rather subdued this morning ahead of earnings reports and

several potential market-moving economic reports. With markets at new record highs consider

your risk carefully as the holiday shutdown approaches.

On the Calendar

On the Tuesday Earnings Calendar nearly 50 companies

reporting results. Notable reports

include BBY, ADSK, BNS, BOX, CHS, CBRL, DELL, DKS, DLTR, EV, GES, HRL, HPQ,

MOV, VEEV, and VMW.

Action Plan

Monday became on the biggest merger days in history, providing

additional energy to an already bullish sentiment setting new records in the

DIA, SPY, and QQQ in the process. T2122

suggests this bull run still has some upside potential but could soon reach a

short-term overbought condition if the bulls continue to find inspiration to

rally. Earnings reports could provide

that inspiration, or perhaps it will be the New Home Sales and Consumer

Confidence reports at 10:00 AM Eastern.

One thing for sure is that the bulls remain firmly in control of a trend

that shows no price action clues of ending at this point.

Futures markets seem much more subdued this morning, perhaps

needed a little rest after such a big effort yesterday. It is also possible with the Holiday looming

and the nasty weather conditions moving across the country that traders will

try and escape early. Don’t be too

surprised if volumes begin to decline quickly with price action becoming very

light and choppy after the morning rush Wednesday. As we push new market highs, plan your risk carefully

heading into the holiday.

The pendulum of the Phase 1 deal that has swing somewhat

bearish heading into the weekend has this morning swing back to the bullish

side, helping to inspire a Monday morning gap.

The bulls got an early start after news that pro-democracy candidates

won big in Hong Kong. The pullback last

week that held trading sets up a great opportunity if the bulls can remain inspired

to attack all-time market highs as we head into the Thanksgiving Holiday.

Asian markets rallied substantially overnight in reaction to

Hong Kong election results. European

markets are also green across the board this morning on renewed US-China trade

hopes. US Futures opened bullishly and

remained strong throughout the night, currently pointing to gap up opens across

all indexes. Perhaps Santa can begin his

run early this year fueled by strong consumer sentiment.

On the Calendar

On the Monday earnings calendar we have 31 companies

stepping up to report. Notable reports

include PANW, A, AMBA, HPE, NTNX, & PVH.

Action Plan

Trade uncertainty dimmed Friday bullishness, but they have

spun the story once again, and this morning, the bulls are pushing for a higher

open. Pro-democracy candidates won big

in the elections on Sunday in Hong Kong with a record voter turnout. A major step for the people of Hong Kong but

they still have an uphill fight with the Beijing control of top

leadership.

With the short holiday week, we still have several notable

earnings reports Monday & Tuesday and a busy economic calendar through Wednesday. However, expect volumes to decline quickly by

mid-week and remain relatively low until Dec. 3rd as traders extend

their Thanksgiving vacations. That being

said the market indexes appear setup to attack new record highs as long as sentiment

on the Phase 1 agreement remains positive.

Last week’s strong consumer reading suggests Santa could have a nice run

this year.

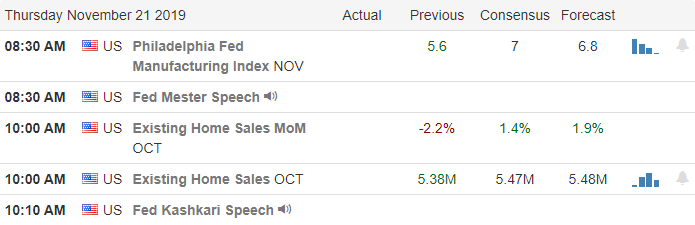

Although we have had 3-days of pullback in the indexes, the VIX shows little to no fear, and so far the indexes has suffered no discernible technical damage. According to reports, the likelihood of a completed Phase 1 trade deal before the scheduled December 15th tariff increase has diminished. As we head into the uncertainty of the weekend and the coming holiday, it may be difficult for the bulls to find much inspiration. However, a consolidation at this level would be productive and bullish as we wait for some political clarity.

Asian markets closed mixed overnight as trade uncertainty

weighed on investor’s minds. Across the

pond, European markets are bullish following positive Euro data. US Futures point toward a modestly bullish

open ahead of Consumer Sentiment that consensus expects to increase slightly at

10 AM Eastern. Plan your risk carefully

as we head into the weekend.

On the Calendar

On the last day of trading this week, we have just 15 companies

reporting earnings. Notable reports

include BKE, FL, HIBB, and SJM.

Action Plan

During the impeachment hearings, the congress could not be

bothered to pass a federal budget but did set aside enough time to kick the can

down the road with another stopgap spending bill to avoid a government shutdown. It now looks as if there will not be a Phase

1 trade agreement before the scheduled December 15th tariffs

increases. China said in a report that they

want a trade deal but are not afraid to fight.

Impeachment hearings have not progressed into Russian election meddling as

the political drama extends.

With a light day of earnings and economic reports the US Futures

are trying to put on a brave face and break the 3-day pullback as we head into

the weekend. With not many places to

find inspiration and trade up in the air it may be difficult for the bulls to

gain much traction. However, if they can

prevent additional selling and slip the indexes into a consolidation I believe

that would be a win keeping the market trends bullish. Although we pulled back there has been on

technical damage, and this rest appears to very constructive thus far. According to the VIX, fear of a selloff remains

very low as we head into the weekend.

The possible delay of the Phase 1 trade deal and the

questions about that means for the December 15th tariff increases

brought out the bear yesterday. However,

by the end of the day the technicals of the index charts took little to no

damage. Even the VIX by the end of the

day showed little to no fear growing in the overall market. That being said, the market is obviously

quite sensitive to the notion of increased tariffs by the end of year, and it

will likely continue to be a driver of market sentiment requiring traders to remain

nimble.

Asian markets closed in the red across the board in reaction

the possible trade deal delay. This

morning European markets are lower across the board as the concern of Hong Kong

bill passed by Congress could affect trade relations going forward as it heads

to the President’s desk for signature.

US Futures are flat to slightly bearish ahead earnings and economic

calendar reports.

On the Calendar

On Thursday’s Economic Calendar, we have 46 companies reporting

earnings. Notable reports include JACK,

LB, LXB, NTES, and QIWI.

Action Plan

A story suggesting there would not be a Phase 1 deal this

year brought out the bears yesterday.

The major concern was not the Phase 1 deal; it’s the question as to what

happens with the tariffs scheduled to increase December 15? Clearly and increase before the end of the

year could have serious impacts on a market that has rallied on the optimism of

a partial deal. Though we have a few

earnings reports today, it’s unlikely the market will see much impact from their

results; instead, the market may focus on the economic calendar news with

Jobless Claims, Philly Fed Survey, and Existing Home Sales.

Although yesterday selling was a concern, the technicals of

the index charts took very little damage yesterday. Personally, I think the pullback to at this

point was good to relieve the relentless bullish pressure. In fact, this pause in the rally could setup new

buy opportunities assuming we can get some clarification on the Phase 1 negotiations

and December 15th tariffs.

Stay on your toes as this political football continues gets kicked about

along with market sentiment.

Some nasty retail earnings and tough talk raise concerns about the so-called Phase 1 trade deal bring a needed pause in the bull run. Even bulls need a little rest from time to time, and this little pullback may prove to be very productive as long as the overall index trends hold. Better earnings results out from TGT and LOW have already recovered some the overnight losses in the futures market now suggesting a modest gap lower at the open.

Overnight Asian markets closed the day bearish across the

board on growing trade tensions. European markets are also reacting lower this morning,

seeing red across the board. US Futures

have lifted overnight lows but continue to point to modest declines ahead of

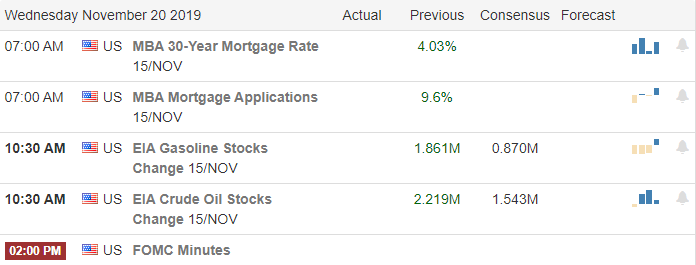

more impeachment hearings and the FOMC minutes due out at 2 PM Eastern today.

On the Calendar

On the hump day Earnings Calendar, we have more than 50

companies reporting today. Notable

reports include LOW, TGT, JACK, LB, LZB, NTES, and QIWI.

Action Plan

Yesterday’s gap up opens eventually turned into a pop and

drop pattern with the Dow closing the day with a bearish engulfing candle. However, the SPY and QQQ found enough buyers

by the end of the day, and the price action finished the day with just a little

rest from breaking daily records. It

would seem tensions between the US and China have once again flared with new tariffs

threatened as part of the rhetoric. Today

the impeachment show continues on the capital hill while the market waits for

the FOMC minutes at 2 PM Eastern.

Even with the slight bearishness of yesterday index trends

remain intact while the VIX continues to register little to no fear of in the market. Although the futures are under slight

pressure this morning, I see this pullback as nothing more than a rest so

far. Of course, that could quickly

change if the Phase 1 proposal falls apart, but my guess is that’s not likely at

least for now. We needed a little rest,

and as long as the overall trends hold, this pullback may well prove to be nothing

more than a pause in an otherwise very bullish trend. Futures point to modest gap down at the open,

but be very careful chasing the open down as many will see this as an opportunity

to buy. As always, wait for proof of

follow-through!

While the bulls seemed to struggle to find inspiration in

the morning session, there was a constant and persistent push in the Dow futures,

which led the indexes throughout the entire day, ultimately setting new record

highs. Oddly, even so-called safe-haven sectors

are being swept up in this relentless bull run.

A rare thing to see, so enjoy it.

How long this can last is anyone’s guess, so don’t get caught up in the

emotion of will bullishness stay focused on price action, plan carefully, and

remember to take profits along the way!

While trouble in Hong Kong continues to get more violent

Asian markets managed to close mostly higher though China said yesterday they

were pessimistic about a trade deal. European

stocks joined the US markets in bullishness setting 4-year highs and are green

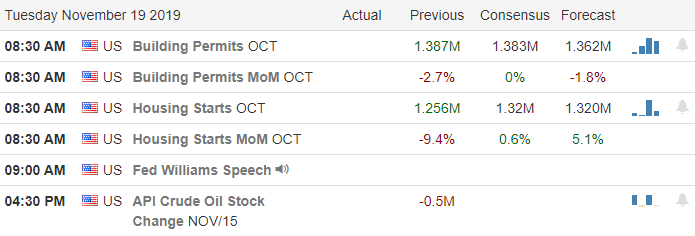

across the board this morning. US

futures pared gains slightly after HD missed on sales expectations but still

point to new record highs ahead of the Housing Starts number at 8:30 AM

Eastern.

On the Calendar

On today’s Earnings Calendar we have just over 60 companies

reporting. Notable reports include HD,

JKS, KSS, MDT, TJX, and URBN.

Action Plan

Pimco predicts the US and China will sign a Phase 1 trade

deal before Christmas causes the futures to leap higher. However, after HD missed on sales expectations,

futures have softened but continue to point to another record high open. Impeachment hearings resume this morning, and

according to reports, the President is considering the idea of testifying in

his own defense. Expect the political

drama to attract a good deal of attention, but it’s unclear if the bulls will waver

in their march higher even if the news is bad.

Although the markets seemed to lack momentum yesterday, the

constant push in the futures market finally broke the log jam setting new

record highs for the day. It’s

interesting to note value stocks and consumer defensive stocks are moving up in

concert with growth and high beta stocks, which is quite odd. Relentless bullishness seems to be the best

description of the current market, and it doesn’t seem to matter what their

buying just buy something. How long this

can last is anyone’s guess, but enjoy it because it’s not often such an event

occurs. As always keep your emotions in check,

stay focused on price remembering how quickly sentiment can shift.