With the strong selling on Friday, the DIA tested and held its 50-day moving average by the close of the day with the SPY, IWM, and QQQ remaining safely above this crucial psychological support. As we head into a short week of trading, the VIX remains quite elevated, so expect the wild price volatility to continue, and the pandemic surge raises reopening uncertainty.

Asian markets closed down overnight with the NIKKEI dropping more than 2 % as the coronavirus death toll tops 500,000 worldwide. However, the European markets are cautiously bullish this morning seeing modest gains this morning. US futures opened trading lower but have recovered and pointed to a mixed but modestly optimistic open amid all the economic uncertainty.

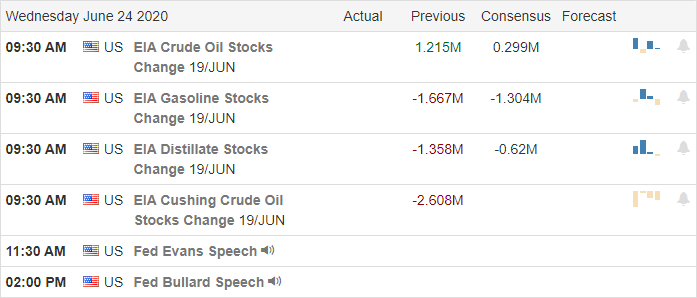

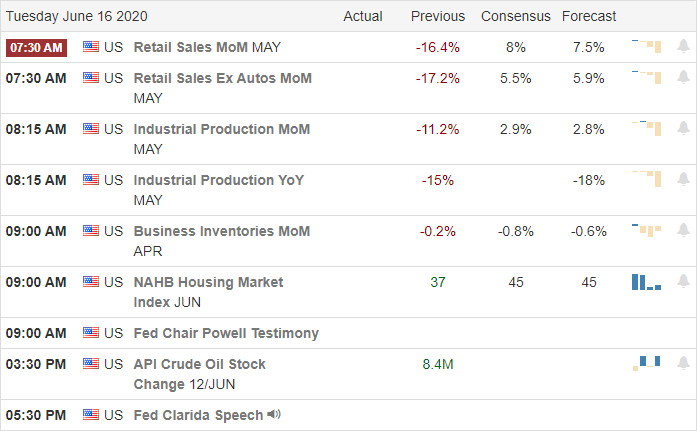

Economic Calendar

Earnings Calendar

With just 2-days to the end of the 2nd quarter according to the earnings calendar, we have about 50 companies reporting, but only the report from MU is particularly notable today.

Technically Speaking

As the summer temperatures rise, so does the spread of the coronavirus hitting new record highs. Several states are rolling back reopening plans and closing large gathering places such as many of the beaches in Florida. Although testing has only gone up by 7 to 10 percent, Arizona has seen an infection surge of 260% in June. Chesapeake Energy has filed for bankruptcy, and Boeing is laying off 12,000 people as the virus continues to impact the airline industry. Health and Human Services Secretary Alex Azar warned on Sunday that the time is running our for the US to curb the surge of the pandemic across the country. Speaker of the House, Nancy Pelosi, asked health officials to make it mandate the wearing of masks across the country.

The heavy selling on Friday tested the daily 50-moving average of the DIA as support, and by the close, the bull managed to hold onto this crucial psychological support. Financial stocks suffered as well on Friday after the Fed required the backs to freeze buyback programs and cap dividends. Futures opened Sunday evening gapping down but have recovered to pointing to a modest gap up open, Although putting on a brave face for today’s open remember the DIA, SPY, and IWM remain in a short-term downtrend and with the VIX elevated expect very volatile price action for the short trading week ahead.

Texas and Florida delay reopening plans, and the number of COVID cases surge to new records. Banks had a good day yesterday with a discussion of suspending provisions of Volker Rule, but after the close, the Fed put restrictions on banks after conducting stress tests. Disney announced an indefinite closure of its theme parks, and Apple said it will close more stores in response to the rising infection rates. As we slide into the weekend, the continued uncertainty is very visible in the elevated VIX.

Asian markets closed the week mixed but mostly higher with only Hong Kong closing in the red. This morning European markets are bullish with their indexes up more than 1.50%. After a choppy overnight session, US Futures point to a flat to open, heading into the uncertainty of the weekend.

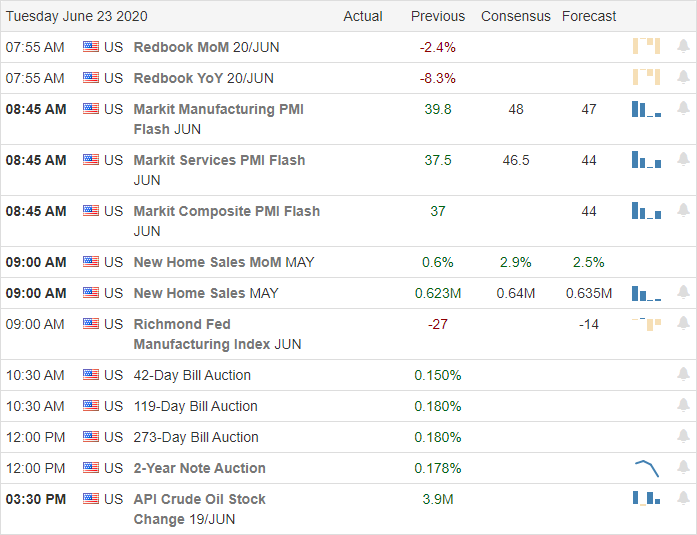

Economic Calendar

Earnings Calendar

As we wind down 2nd quarter earnings, we have just 14 companies reporting on this Friday. Notable reports include JRJC and FIZZ.

Technically Speaking

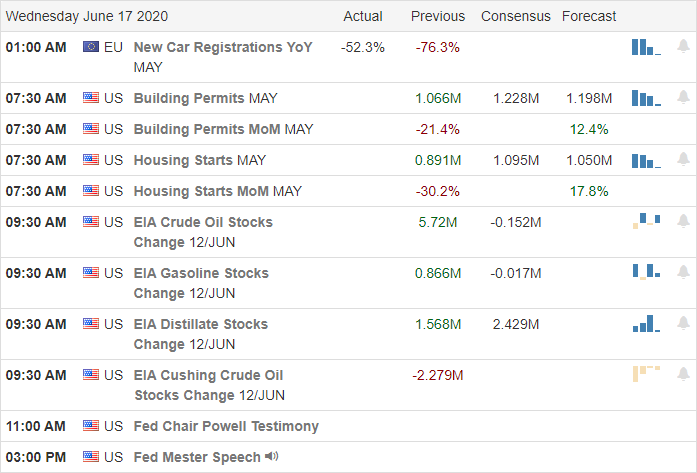

Another choppy day as the market dealt with virus concerns and unemployment coming in stronger than expected. During the day, both Texas and Florida suspended their reopening plans after hitting new record-high infection rates. Across the nation, new cases topped 40,000 yesterday with the death toll reaching 125,000. Disney announced they would suspend the reopening of their amusement parks indefinitely, and Apple will close more stores in response to the rising infection rates. Banks rose sharply yesterday on the news that the government may ease or remove some of the provisions of the Volker Rule. After stress testing, the banks are now required to cap dividend payments as well as end all stock repurchase programs until September. Nike reported that sales declined 38% last quarter, and the stock is indicated to open only slightly lower this morning.

We had a volatile overnight future as the market responded to the bank stress test results, but in the standard fashion of late, they have rebounded this morning pointing to flat to slightly bullish open. It seems that any and all negative economic news only inspires the bulls to buy. Perhaps, we are experiencing the end of quarter window dressing, but with the QQQ having rallied 50% from the March lows, I wonder how much longer this ravenous bull run can continue. The DIA, SPY, and IWM continue to cling to their longer-term up-trends, but the current short-term downtrend and the elevated VIX indicates and underlying stress that could bring the bears out of hiding next quarter. Of course, all of this could change if the Fed puts their printing pressed into overdrive, and Congress offers up more stimulus. Consider your risk carefully as we head into the weekend.

A spike in COVID-19 numbers and the prospect of a Biden presidency brought out the bears yesterday as we wind down what has proved to be a remarkable 2nd quarter. Some huge uncertainties lye ahead as several southern states reports new record infection levels. AAPL announced it is closing several more stores in response as Texas nears COVID related ICU capacity. Facing a big day of economic data, the futures point to a modestly lower open as the VIX looks to another day of significant volatility.

Asian markets closed mixed but mostly lower overnight as the IMF slashes economic forecasts. European markets trade mixed but lean slightly bullish this morning as Wirecard files for bankruptcy. Here in the US, with a big data dump, futures point to declines, but I would not expect the bulls to give up easily. Prepare for the considerable price volatility to continue.

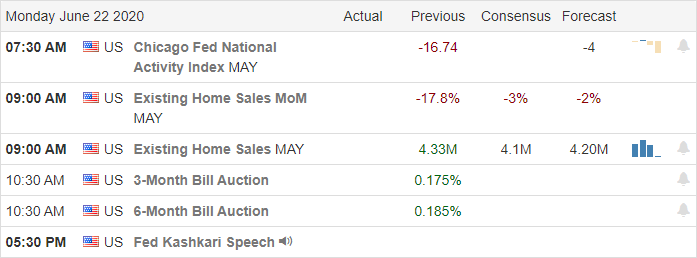

Economic Calendar

Earnings Calendar

On the Thursday earnings calendar, we have the largest day this week, with 26 companies stepping up to report. Notable reports include DRI, FDS, MKC, RAD & NKE.

Technically Speaking

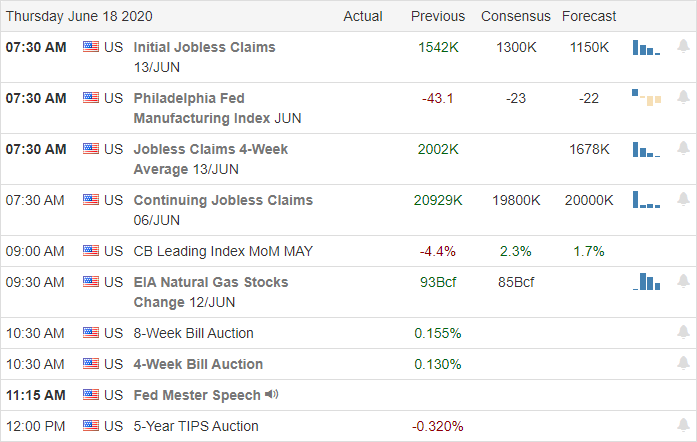

The bears made a big appearance yesterday with the Dow selling-off 710 points in reaction to rising coronavirus cases. Yesterday they reported more than 35,000, but this morning CNBC is reporting the daily spike above 45,000, which would be a new single-day record. According to reports, infection rates have increased by 30%, while testing has only increased by 7%. New York and several other states are requiring travelers from hot spot states to quarantine for 14 days, and Europe is considering restricting travel from the US. AAPL announce it is closing more stores in Texas as the state nears ICU capacity. New polls indicate that Joe Biden has taken a big lead in the Presidential race, and some are suggesting that the market could see more weakness ahead as a result. A resurgence of the pandemic, widespread public unrest, and a presidential election is likely to keep the market on edge and volatility high for the next several months making 2020 one for the record books.

The DIA, SPY, and IWM created a lower high on Tuesday and lower low yesterday, leaving behind bearish evening star patterns. The QQQ also printed and evening star pattern but closed the day above recent support and continues to remain above its trend. I don’t expect the bulls to give up easily, and unless we see enough selling in the QQQ to break the uptrend, the big five tech giants can continue to hold up the indexes. If significant profit-taking begins in AAPL, MSFT, GOOG, FB & AMZN as the 2nd quarter winds down, we could face a very different market in the weeks and months ahead. Facing a big day of economic data and rising pandemic uncertainty, anything is possible, and we should plan for substantial volatility as we head toward the weekend.

A new record in the QQQ on the morning gap, but all the indexes struggled to find follow-through buyers with declining breadth as prices failed to break above the bearish engulfing candles left behind last Friday. As the tech sector led rally prints, all-time highs coronavirus infections have spiked 30% over the previous seven days, according to reports. The Whitehouse health advisor warned yesterday day afternoon if this trend continues, a full shutdown of infected states to combat the spread may be required. A disturbing thought considering the fragile condition of businesses and historic unemployment.

Asian market closed mixed but mostly modestly lower overnight. European markets spooked by the rapidly rising virus infections around the world are decidedly bearish this morning seeing red across the board. Ahead of alight day on the earnings and economic calendar, US Futures point to a bearish open and more price volatility ahead.

Economic Calendar

Earnings Calendar

On the Hump Day earnings calendar, we have just 11 companies reporting quarterly results. Somewhat notable reports include BB and WGO.

Technically Speaking

A day after the Nasdaq gapped up to notch a new record high, the market struggled to find willing buyers to follow through. By the close, the DIA and IWM failed to rise above the Friday selloff candle while remaining under their 200-day average. While well above its 200-day average, the SPY tried hard to break above Friday’s bearish engulfing candle, but by the end of trading Tuesday, the bulls failed to breakthrough. The QQQ left behind a possible reversal pattern with a shooting star that could become an abandoned baby reversal if the index gaps lower at the open. The Absolute Breadth Index continued to show that yesterday’s rally lacked buyer’s momentum with the big internet techs garnering the vast majority of the attention. While the market has chosen to ignore pandemic numbers according to reports, the number of infections has risen 30% in the last 7-days. The Whitehouse public health adviser suggested yesterday if this trend continues, a total shutdown of an effected state may be required to combat the spread. Let’s hope that does not occur!

Ahead of a light day of earnings and economic reports, the market may be more sensitive to the news cycle that this morning seems to be heavily laden with COVID related stories. Weekly homebuyer mortgage demand slipped slightly in today’s reading but remained 18% higher than last year. As the 2nd quarter winds down after achieving a history-making rally, we can expect considerable volatility in the days ahead. A rotation into income securities and safety plays may be underway with a noticeable increase in precious metals. Although it sold off on yesterday’s gap up, the price action in the VIX-X continues to suggest considerable uncertainty closing above 31 as the Tech Sector hit new records. A small but noticeable clue that price action could remain very challenging in the day ahead.

Fueled by just a few tech giants, the market rallied on Monday in a somewhat choppy session even as the Absolute Breadth Index declined. MSFT and AAPl hit new record highs, and the QQQ had a new all-time closing high on Monday as is set to make another new high as the index gaps up this morning. Falling Existing Home Sales and rising COVID infections did nothing to dissuade the bulls from buying.

Asian markets closed in the green across the board in a will evening of trading due to peter Navarro’s comments on the US/China trade deal. European markets are decidedly bullish this morning, with the DAX up more than 2.5%. Ahead of PMI and New Home Sales US Futures point to a substantial gap up open that will likely ink a new record high in the Nasdaq.

Economic Calendar

Earnings Calendar

On the Tuesday earnings calendar, we have just six companies reporting. The only somewhat notable reports today is LZB.

Technically Speaking

Markets rallied yesterday with MSFT and AAPL reaching out to new record highs. According to the WHO we also set a new world record with more than 180,000 new coronavirus infections. In the US, we saw more than 31,000 new infections reported with Multiple US states experiencing rapidly rising hospitalizations. Protests in the park across the street from the White House attempted to pull down the statue of Andrew Jackson, and in Seattle, a protester held district of the Capitol Hill area now has the attention of Govoner due to the growing violence. We also had a very wild night in the futures market. Futures fell sharply after Peter Navarro was reported to have said the China Trade deal was dead. Later Navarro denies saying that stating the agreement isn’t over and the futures quickly recovered. Yesterday, AAPL announced IOS 14 is coming in September and reported their new iPhones and iPads would no longer include INTC chips. INTC is indicated higher this morning, go figure. Existing-Home Sales slumped substantially last month; however, it seems, any and all bad news only inspires the bulls to buy.

On a technical basis, the DIA and IWM remain below there 200-day averages, but it would appear this morning’s gap up will test them as resistance. The SPY will test the high of Friday’s selloff, and the QQQ will set a new record high at the open today. The Absolute Breadth Index declined on Monday as the majority of the index’s rally came in the big tech giants AAPL, AMZN, MSFT, GOOG, FB, and NFLX. Although the VIX-X pulled back yesterday, it remains quite elevated even as the bulls push to new record highs, so stay on your toes as quick reversals and whipsaws are possible. Today will get readings on PMI and New Home sales with a very light day on the earnings front.

Although health officials are very concerned about the rapid resurgence of coronavirus, the bulls appear ready to continue buying despite the possible impacts. They will have to overcome some bearish engulfing candles printed on Friday and an elevated VIX suggesting that price action will remain quite volatile. Though putting on a brave face this morning, I suspect the market will be quite sensitive to virus news so focused and ready for possible whipsaws and reversals.

Asian markets closed modestly lower overnight, and European markets are whipsawing this morning and currently red across the board as they monitor the coronavirus surge in the US. Here in the US Future point to a bullish open but have pulled back from morning highs as the bulls trying to say; virus, we don’t care about no stinking virus! I guess if can beat it will just try to ignore it, as we hope for more government stimulus.

Economic Calendar

Earnings Calendar

On Monday’s earnings calendar, we have just 11 companies fessing up to quarterly results. Notable reports include JKS and TTM.

Technically Speaking

During the weekend, the US saw surging coronavirus infections topping more than 30,000 on Saturday and Sunday. Health officials are concerned that some states could see a sharp rise this week, but as of now, the market appears completely unconcerned as US Futures rise. China announced it would suspend imports of poultry as a result of the Tyson plant coronavirus concerns. Airlines that have been bleeding money due to the pandemic have plans to expand flights in June and July and say they believe they will back to normal by the end of the year. There is concern spreading that it may be challenging to have a college football season this year as more and more players are becoming infected. On Friday, AAPL touched new record highs but triggered an afternoon selloff when they announced the closure of several stores in states where the virus is rapidly spreading.

The DIA left behind a bearish engulfing candle by Friday’s close, failing once again at the 200-day average. IWM also seems to be struggling near its 200-average but managed to hold above Thursday’s low. The SPY printed a bearish engulfing pattern while maintaining a stronger technical pattern, and the QQQ continues to lead the markets holding near record highs. I must admit to a bit of surprise that bulls seem oblivious to the spreading virus as they once again point to a gap up at the open. The VIX remains quite elevated, closing above a 35 handle on Friday, so expect the volatile price action to continue and sensitivity to virus-related news.

Yesterday saw very choppy price action as the market grappled with concerns of rising coronavirus infections and hospitalizations. However, with central banks continuing to inject trillions of dollars into the markets, the bears struggle to find traction. While some are beginning to call the current rally, a bubble others continue with the mantra, don’t fight the fed! With the VIX holding above a 30 handle, we should continue to expect the challenging price volatility to continue as we wait for the next round of jobless numbers.

Asian markets closed mixed but mostly lower overnight as outbreak concerns weigh on investors. European markets are trading modestly lower across the board this morning. Ahead of the light day of earnings reports and jobless claims, US Futures point to modest declines at the open.

Economic Calendar

Earnings Calendar

On the Thursday earnings calendar, we have just 11 companies reporting quarterly results as the 2nd quarter season winds down. Looking through the list, I can only find one marginally notable report today coming from SWBI.

Technically Speaking

Buyers and sellers seemed to be somewhat in agreement yesterday as market largely chopped sideways. The internet giants rose while the vast majority of companies struggled with the Absolute Breadth Index declining. Futures saw some modest selling during the evening but have since rallied after a report our of China saying they have new the coronavirus outbreak under control. The shutting down of about half the flights in and out of Beijing would seem to be in contradiction. US virus infections continued to rise yesterday, with more than 26,000 new cases reported. Hot spots include Texas, Arizona, Florida & California. The Bank of England voted to add another 100 billion to its bond-buying program as central banks continue unprecedented operations to combat the impacts of the coronavirus.

Although the DIA and IWM remain above there 50-day averages and longer-term trends, yesterday’s price action left behind the potential of a lower high price pattern. The IWM pattern failed at the daily-200 average, leaving behind the possibility of a short-term head and shoulders pattern. With the SPY closing the day well above its 200-day averages and the QQQ eking out another bullish day, both hold much stronger technical patterns. That said, shorting amid all the central bank operations around the world is a bit like trying to swim up a fast-flowing river! Today we will get another reading on jobless claims, but the market seems to have clearly demonstrated that unemployment will not get in the way of this bullish optimism. Expect another day of price volatility at the VIX remains quite elevated closing yesterday just above a 33 handle.

As stats reopen their economies, consumers were out in force shopping according to the retail sales number. Although they remain sharply lower year over year, the bulls produced a massive gap at the open that proved to be very volatile are the coronavirus brings new China restrictions. Here in the US, governor’s remove restrictions on restaurants and health clubs, several states reported a record number of infections yesterday. The VIX remains elevated as the market continues to rally, creating extreme price volatility intraday to challenge even the most adept day trader skills.

Asian markets closed mixed but mostly higher as the IMF warns of an unprecedented crisis. European markets have fluctuated this morning but currently point to modest gains across the board as US Futures once again suggest a substantial gap up open. Stay focused on price action and remain very flexible with such high price action volatility.

Economic Calendar

Earnings Calendar

On the Hump Day earnings calendar, we have a light day with 12 companies stepping up to report quarterly reports. Looking through the list, I only see one marginally notable report from ABM.

Technically Speaking

Fueled by much better than expected retail sales, the already bullish futures lept higher at the open. Though consumers returned to shopping with a vengeance raising hope of the recovery, the year over year numbers still needs a lot of improvement. News that China is implementing another round of restrictions with a resurgence of coronavirus cane close to reversing the bullish intraday, but the bulls charged back in before the close of day. Although the reopening of the economy has the bulls out in force, it is coming at a high cost, with several states reporting a record number of COVID-19 infections and hospitalizations yesterday. Should this trend continue, it will make a recovery very challenging for all struggling retail business. However, there was positive news of a treatment that, in a preliminary test, shows signs of improving the survivability of those hospitalized.

At the close yesterday, the DIA recovered and held just above its 200-day average while IWM remains challenged by this key resistance. The SPY closed well above its 200-day, attempting to test the island reversal pattern created on the June 11th gap down. The QQQ remains by far the most resilient of indexes lead by the internet giants, AAPL, AMZN, MSFT, GOOG & FB. The T2122 indicator is once again signaling a short-term extended condition with the Dow recovering more than 1400 points in just 2-days of trading. Although the VIX has pulled back the last couple of days, it remains very elevated closing above a 33 handle as the extreme price volatility continues to keep the danger level high. The enormous overnight reversal gaps and the rapid intraday price swings have made the market particularly dangerous for retail traders. They are either forced to hold and pray, suffering whatever the market hands out, stand on the sidelines, or attempt day trading the extreme volatility. Its no surprise there is another gap expected this morning, but what comes next in Coronaland is anyone’s guess.

Fear of the rising virus hospitalizations, debit, bankruptcies, and growing tensions with China & North Korea are apparently no match for an FOMC with an unlimited checkbook. From Monday open to Tuesday, a swing of 1000 points just in the morning gap after the Fed adds another 750 billion in direct company bond purchases. This morning the indexes will challenge the huge June 11th gap as the massive price volatility continues.

Asian markets roared back overnight with Japan rising nearly 5%, and European markets reverse to bullishness with the DAX up over 3% on in reaction to the Fed spending. Ahead of the Retail Sales numbers and the Chairman’s congressional testimony US Futures are decidedly bullish, suggesting a considerable gap in the indexes.

Economic Calendar

Earnings Calendar

On the Tuesday earnings calendar, we have just over 20 companies reporting their quarterly results. Notable reports include LEN, ORCL, GRPN, HRB, & MFA.

Technically Speaking

With slow and steady pressure, the bulls recovered from the substantial morning gap down as the incredible price volatility continues. Yesterday we heard the Planet Fitness declared bankruptcy, but the stock rallied during the day. Today 24 Hour Fitness joined them in declaring bankruptcy. United Airlines burrowed 5 billion against its frequent flyer program, and Hertz announced a new stock sale with the suggestion that investors will lose their money. However, none of that seems to matter these days, including rising coronavirus, unemployment, and the soaring national debt. That said, the market celebrated the news that the FOMC will add another 750 billion to buy bonds directly from companies. The President announced a plan to spend Trillion on infrastructure and will sign an executive order on police reform later today.

This morning ahead of the Jerome Powell’s testimony on the hill and several economic reports, we are once again expecting a 500 point gap at the open. Yesterday, bearish, today bullish. Count it up; that’s a 1000 point swing in just the morning gap! Amazingly that seems to have become the new normal. Today’s gap will test the 200-day average on the DIA and IWM as resistance and move us to back up into the vast gap down created on June 11th. The SPY quickly recovered its 200-day average yesterday, and the QQQ rally regained the breakout high of last February with the big internet tech companies leading the way. With the market tossing around 500 point gaps, what happens next is anyone’s guess, so prepare for another wildly volatile day.

News that Beijing is once again instituting coronavirus isolation measures and the resurgence of hospitalizations here in the US have the bears on the prowl this morning. As of Friday, longer-term trends and major price support areas, as well as 50-day averages, remain bullish. However, the substantial spike in the VIX could make the days ahead very challenging for traders, and those bullish technical s could quickly turn bearish. With the Fed step up their operations, will the Congress approve more stimulus, will it be enough to keep the economy afloat if the feared second wave of infections begins to inflate? Tough questions to answer, making the path forward very uncertain.

Asian markets closed lower across the board, with the NIKKEI falling nearly 3.5% overnight. European indexes are decidedly bearish this morning as the threat of virus rebounds. US futures point to a rather grim gap down with the Dow expected to fall more than 500 at the open. It would appear the wild ride of 2020 is far from over, and the complexity of the recovery will be far more challenging than the recent rally would suggest.

Economic Calendar

Earnings Calendar

On the Monday earnings calendar, we have a relatively light day. Notable reports included JKS & TTM.

Technically Speaking

The Friday’s bounce after the Thursday rout was a nice break in the selling, but the news over the weekend has the bears charging again this morning. We learned during the night that Beijing as reinstated isolation measures in some areas, established checkpoints and closed some schools due to a resurgence of the Coronavirus. Here in the US, even as the States try to reopen their economy’s infection rates and hospitalizations are accelerating. Planet Fitness has filed for bankruptcy and said they would close about 1000 locations as it attempts to reorganize. I suspect we will begin to hear of many more bankruptcies in the coming months as the full measure of business impacts is realized. According to reports, protesters have taken over a small area of Capitol Hill in Seattle, forcing a police station to close for the safety of the officers. The President has theathend to mobilize the national guard to restore order, but the idea does not have support by the governor.

As bad as the Thursday sell was, the longer-term bullish trends and major price supports have so far held in the DIA, SPY, and QQQ. They all remain above their respective 50-averages, and the QQQ thus now is merely testing the breakout as support. Unfortunately, the spike volatility could quickly shift those bullish technicals as the uncertainty about the path ahead with the resurgence of the virus. There are those once again predicting a market calamity, and those that believe the virus news has blown everything out of proportion, and the recovery will resume. The fact is no one knows the futures and the best we can do as traders; avoid the prediction and stay focused on price action for our trade queues or stand aside if you fell the risk of uncertainty is too high. Remember, there is no shame in protecting your trading capital; in fact, that is one of the primary jobs in this wild business of trading.