The U.K. reported a new, more contagious strain of the virus on Sunday, overshadowing the 900 billion stimulus bill agreement sending the futures sharply lower. If this morning’s gap-down reversal gains momentum, it could be a painful day with price and technical supports substantially lower. Though cooler heads may prevail, make sure you have a plan to protect your capital. Expect extreme sensitivity to the news as countries extend and strengthen restrictions in reaction to the new strain.

Asian markets closed mixed but mostly lower overnight. European markets trade decidedly bearish this morning as new travel restrictions go into place. U.S. futures have bounced off overnight lows but still point to a substantial gap down ahead of a light earnings and economic calendar day. Buckle up volatility and with an extreme sensitivity to news surrounding the new strain.

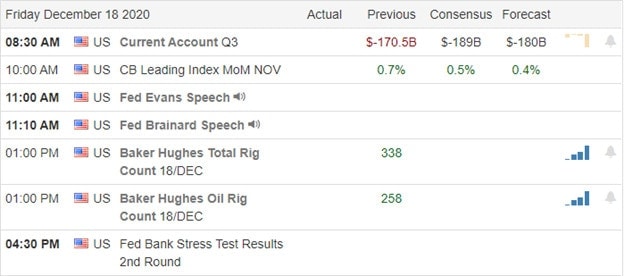

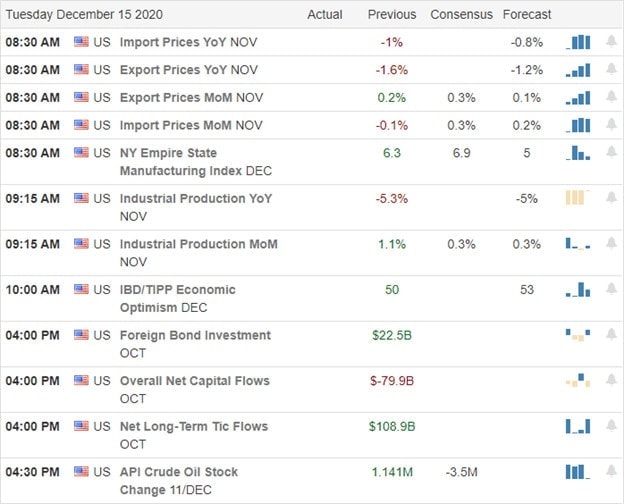

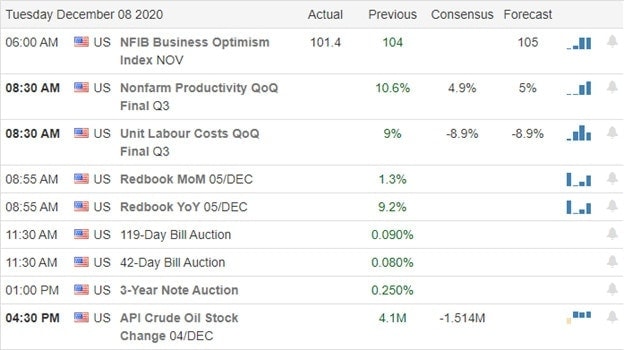

Economic Calendar

Earnings Calendar

As we kick off the Holiday week, we have a light earnings calendar. Notable reports include FDS & HEI.

News and Technicals’

The second vaccine from Moderna reaches hospitals today after emergency approval last week, with infection and death rates remaining very elevated. Late Sunday afternoon, Congress agreed on a 900 billion dollar stimulus bill, the 2nd largest in history. The House will vote on the bill later today, sending to on to the Senate for approval. Airlines are on track to receive another 15 billion in government support but must call back furloughed workers to receive the payments. Yesterday the U.K. scientists identified a new, more aggressively infectious strain of COVID. In reaction, several countries have already banned travel, and instead of the planned easing of restrictions ahead of Christmas, Parlement may add to lockdown restrictions in an emergency Parliament meeting. After hearing about the stimulus agreement, U.S. futures surged 200 points but have turned sharply bearish as new restrictions in reaction to the new strain worry investors.

After a very volatile overnight futures market fueled on the mixed emotions of stimulus and a more infectious strain of the virus, the market points a substantial gap down at the open. Dow futures more than 600 points but has thus far rallied off the overnight lows. That said, those that were buying up positions before the weekend will likely experience a painful reversal this morning. Perhaps cooler heads will prevail, but this is the kind of event that could easily trigger a swift and significant selloff. Try not to panic and stay focused on the price action but plan to protect your capital if the run for the door gains momentum.

The bulls and bears stood toe to toe yesterday, duking it out with either side unable to gain any momentum as we wait on Congress. Evidence continues to show that pandemic restrictions are slowing the economy, and with infection rates exploding to about 1 million every 4-days, I suspect that will only get worse. Has this rally already priced in the stimulus bill? Maybe, so be careful overtrading and consider your risk carefully heading into the weekend and the holiday week ahead.

Asian markets closed the week red across the board in reaction to the Bank of Japan rate decision. European markets this morning show modest gains even as a no-deal Brexit weighs on investor minds. U.S. Futures are trying to shake off overnight lows during the morning pump up that has become all too familiar of late. With a light earnings and economic calendar day, expect an extra dose of news sensitivity as we head into the weekend.

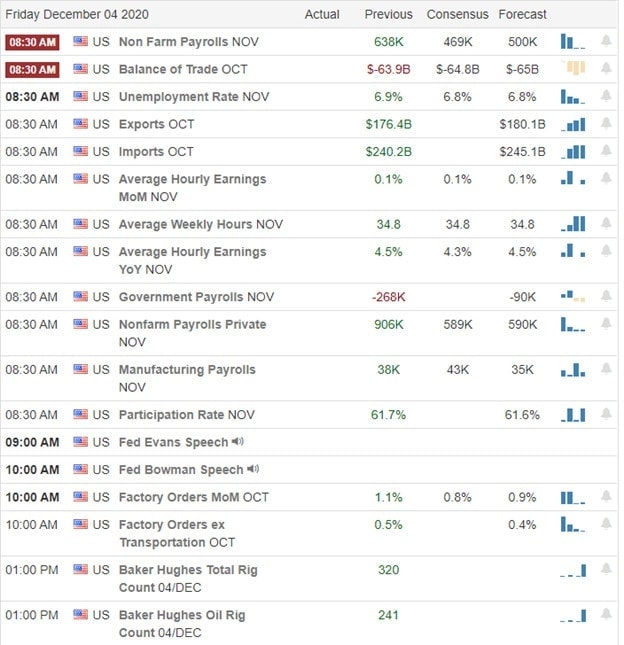

Economic Calendar

Earnings Calendar

We have a light day on the Friday earnings calendar, but we still have a few meaningful reports. Notable reports include APOG, DRI, NKE, & WGO.

News & Technicals’

With an afternoon vote, the FDA endorses the second vaccine choice, with Moderna gains approval for emergency use. A good thing as the infection rate explodes around the country, adding about 1 Million new positive tets in just 4-days. According to reports, the widespread hack included a breach at Microsoft. They are not suggesting millions of Americans may have been affected by the attack. The deadline for a Brexit trade deal is drawing near with several key disputes yet to resolve. A no-deal Brexit could create some stock market and currency market fluctuations. Keep an eye on this developing story.

After gapping higher on high hopes of a stimulus bill, the market seemed to lose momentum quickly and chopped in a narrow range the rest of the day. The Absolute Market Breadth Indicator continues to decline, and the T2122 indicator suggests a very extended condition in the indexes. That said, the bears don’t appear to have any teeth, and the trends remain bullish as we wait for a congressional decision. The indexes appear pensive and wound pretty tight, waiting on a news event that can create an explosive move in either direction. As you plan your risk into this weekend, keep in mind volume tends to decline quite sharply, heading into the Christmas holiday shutdown.

The market seems solely focused on stimulus, rallying the NASDAQ to new record highs. Little details such as declining retail sales, new record hospitalizations, and the highest daily death toll over 3600 Americans won’t stand in its way. Sorry for the sarcasm, but ignoring the economy’s actual state can make for a hazardous situation if the market sentiment suddenly decides to shift. Stay with the bullish trend but stay focused and have a plan to capture gains and protect your capital because a shift south could be swift and punishing.

Overnight Asian markets recovered from early losses to close with modest gains across the board. Across the pond, European markets advance with stimulus talks in focus. Ahead of Housing Starts, Jobless Claims, and the Philly Fed MFG Index, futures currently point to a bullish open fueled up on hopes of more federal deficit stimulus spending. Stay focused as we continue to extend.

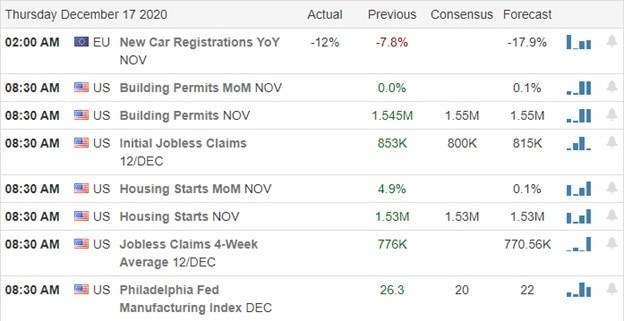

Economic Calendar

Earnings Calendar

As usual, the Thursday earnings calendar is one of your busiest days of reports. Notable reports include CAN, BB, FDX, GIS, JBL, NAV, RAD, & WOR.

News & Technicals’

Focused only on stimulus hopes and seemingly ignoring any other economic details, the futures are rising this morning. A miss on Retails Sales, a decline in PMI, with new records of more than 3600 deaths and hospitalizations while on the same day printing new a record on the NASDAQ. Jerome Powell left rates near zero and reintegrated the FOMC commitment to keep them low as long as necessary for the economy to recover. The FDA expects to vote on Moderna’s Covid vaccine later today, and Congress is making progress on the stimulus bill. Several states joined Texas in an antitrust lawsuit against Google, claiming collusion with Facebook fixing advertising prices. Antitrust against the tech giants seem to be shaping up as a theme for 2021.

At the risk of sounding like a broken record, stay with the bullish trend but have a plan to capture gains and protect capital if the market suddenly decides to care about the actual economy’s condition. Before the open, today will get readings on Housing Starts, Jobless Claims, and the Philly Fed MFG Index. The most likely to move the market would typically be the Jobless Claims, but with high hopes of newly printed stimulus debit, even a negative number could inspire new record index highs. I will reiterate that both T2122 and T2101 are both flashing clues to be cautious, so be careful not to overtrade or chase already extended stocks.

Just 2-weeks before Christmas, Senate leader McConnell congratulates Biden as the president-elect, and he and Schumer say a stimulus funding deal is on the way. That has the futures pointing to new record highs at the open, assuming the data deluge on the economic calendar doesn’t trip up the bulls. Keep in mind that shortly after the open price, action could become light and choppy as we wait for the FOMC decision and press conference beginning a 2 PM Eastern time. Stay on your toes and prepare for the possibility of some price volatility.

During the night, Asian markets closed the day mixed but mostly higher following the U.S. rebound on Tuesday. European indexes are advancing across the board following a positive global growth trend. Here in the U.S., the bulls are fueled up on stimulus hopes ahead of a big day of economic reports. Buckle up it could prove to be a wild ride.

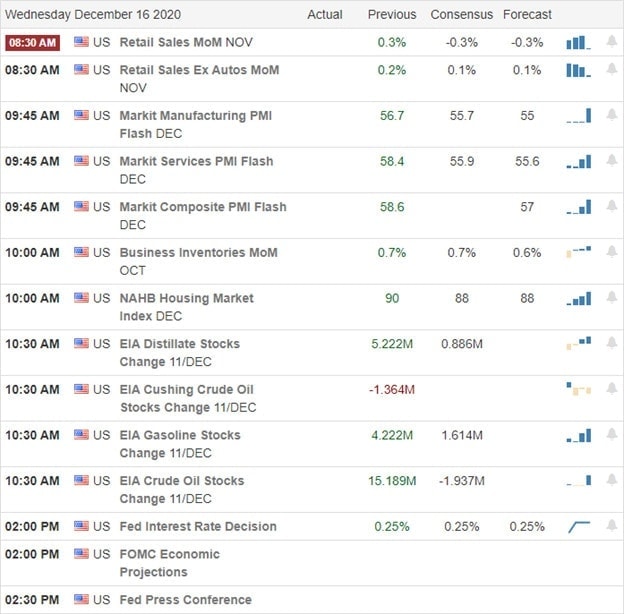

Economic Calendar

Earnings Calendar

The hump day earnings calendar is a light one, but we have a couple of reports worth a look. Notable reports include LEN & TTC.

News & Technicals’

After meeting yesterday on the stimulus bill, Senators McConnell and Schumer hope to soon progress on the funding deal. Hopefulness that the spending bill will soon be on the way is inspiring the bulls once again this morning, likely setting new record highs at the open today. However, attention will quickly turn to the busy economic calendar with Retail Sales, PMI Composite, Business Inventories, Housing Market Index, and EIA Petroleum Status. If that’s not enough to keep traders guessing, we have the FOMC Announcement and the Chairman’s press conference to keep the price volatility alive. In a move that seems to put the presidential election to rest, Senate Leader McConnell congratulates Biden on his win and urges Republicans not to reject the president-elect’s victory.

The bullish trends remain, and with hopes of more stimulus futures point to more record highs this morning. That said, clues are warning that a little caution is warranted. The Absolute Market Breadth indicator continues to downtrend even as the market rallies, suggesting fewer and fewer stocks keep the rally alive. Also, the T2122 indicator is once again suggesting a short-term over-extension. Stay with the trend but have a plan to protect your profits and capital if sentiment begins to shift quickly. Monday’s big rehearsal should serve as a reminder that bears still exist and how quickly the bullish tide can recede from this elevation.

Yesterday was a mixed bag of results in the indexes as vaccine news seems to have lost some of its power to inspire the bulls facing a long winter with more lockdown restrictions likely. However, with the healthcare system bursting at the seams with pandemic patients, Congress feels the pressure to pass a stimulus bill by the end of the week. Could this perhaps inspire a Santa Claus rally, or has is it already baked into the current index prices. Something ponders as you plan your risk facing a hectic week of economic data ahead.

Overnight Asian markets closed in the red across the board, responding to a resurgence of virus concerns. European markets trade cautiously mixed this morning with Brexit talks in focus. Here in the U.S., futures point to an overnight reversal as the bulls gain new energy with high hopes of stimulus money soon on the way.

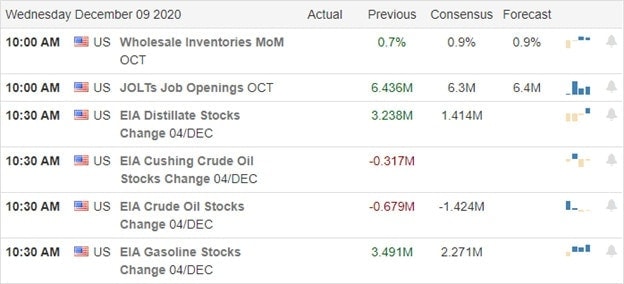

Economic Calendar

Earnings Calendar

On the Tuesday earnings calendar, we have a light day. Notable reports include AOUT and NDSN.

News & Technicals’

Yesterday the vaccine news that pushed the markets higher at the open ran out of energy, creating a mixed bag of results in the indexes. The QQQ and IWM managed to rally while the DIA and SPY sold-off as the VIX rallied, showing a little fear. It would seem the vaccine news has now baked in, and the market is beginning to focus on the genuine possibility of more restrictions and lockdowns impacting business. The Electoral College has confirmed Joe Biden as the next President of the United States and ended the Trump administration’s long legal battle. Futures are once again rising with Congress working to pass a stimulus bill by the end of the week. With the U.S. death toll topping 300K and the health care system strained nearing capacity in many parts of the country, Congress feels the growing pressure to respond. The big tech social media giants face hefty fines under new UK rules as the U.S. steps up with substantial antitrust pressure of their own.

Although the DIA and SPY selling was significant, the daily charts remain in bullish trends but signal a bit more caution is warranted. It is still possible that the indexes experience a Santa Claus rally is a stimulus bill does get passed. Still, we should also consider the possibility that stimulus hopes have already been priced into the market. With pandemic lockdown restrictions on the rise and a long winter ahead, the stimulus bill’s passage may well become a sell the news event. Yesterday’s price action points to growing volatility and points to the danger of chasing stocks that are already quite extended. We have a lot of data coming our way in the next few days, so plan your risk carefully and remember to take some profits along the way.

Jobless claims disappointed markets yesterday but having Congress adjourn for the weekend without reaching a stimulus deal appears to be the more significant disappointment this morning. The Whitehouse’s legal battle could also create considerable volatility in the days ahead, depending on how or if the Supreme Court gets involved. The market hates uncertainty, and as we slide into this weekend, considering this historic rally, traders have some tough decisions to make. Capture gains or wait, holding on to hopes for the week ahead. What’s your choice?

Asian markets finished the week with mixed results, but European markets see red across the board as Brexit, and the U.S. stimulus battle continues. The U.S. futures market point to a bearish open that could test index trend supports as traders grapple with the weekend’s uncertainty. It’s been a while since the bears showed much of a willingness to fight but never forget they can attack anytime, so have a plan to protect your capital should they decide to show some teeth.

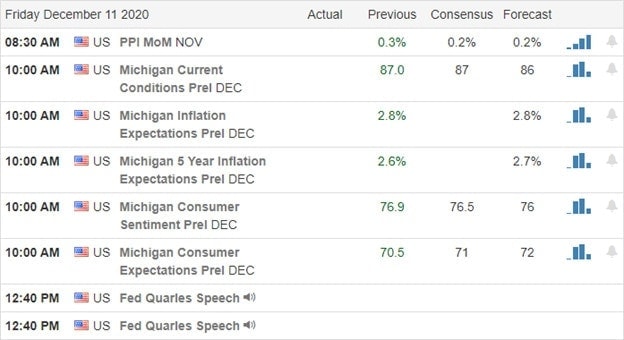

Economic Calendar

Earnings Calendar

Although we have some very small-cap companies, Friday is a light day of quarterly reports. Looking through the list, I could only come up with one somewhat notable, JOUT.

News & Technicals’

An increase in unemployment has the bears stirring about yesterday, but overall the market was still hoping that Congress would reach a stimulus deal. Instead, Congress passed a single week stopgap spending bill avoiding a government shutdown and then adjourned for the weekend. As a result, the market is showing its disappointment, suggesting a bearish open. Prizer’s Covid vaccine took a big step forward with the FDA’s advisory committee recommendation for emergency use. Now it moves up the ladder looking for a full FDA agency approval. In a move that bucks the overall market love affair with Tesla, Jefferies downgraded the company, suggesting they don’t believe the carmaker can dominate the auto industry. Battleground states urge the Supreme Court to reject Texas efforts to overturn the election results. Seventeen states have joined with Texas setting up an interesting legal battle that could create substantial market shockwaves depending on how the battle progresses.

Although the pullback may be disappointing to many, the T2122 indicator has signaled this possibility for some time. Should the early morning bearishness hold through the open, the short-term trends will receive a test of support. If the bulls have the energy to defend, then there is no harm in taking a little break in the current rally. However, if the bears become emboldened, price support suggests that the pullback could be quite painful. Remember, the market has the propensity to throw a bit of a temper tantrum when they don’t get their stimulus fix. Stay focused and have a plan should the bears decide to show their teeth.

The markets once again took their cues from vaccine news and hopefulness for federal stimulus as the SP-500 topped 3700 for the first time in history and the Nasdaq set its 50th record high for the year. Valuations continue to soar as the overall market P/E Ratio stretches 72% above the 10-year average. The U.S. added 1 million new infections in just 4-days, but that is not slowing down the bull run with a parade of big investment banks predicting a bullish 2021 market. Trade with the trend but have a plan should the sentiment suddenly shift because current market prices are long from technical supports.

Asian markets traded mixed but mostly higher overnight, with the Shanghai down more than 1%. European markets are currently bullish across the board this morning, with Brexit talks in focus. U.S. Futures point to another morning of bullishness ahead of the JOLTS report and several earnings reports.

Economic Calendar

Earnings Calendar

On the Hump day earnings calendar, we have another light day but still have several quarterly reports of potential market moving. Notable reports include ADBE, CPB, DBI, HOV, VRA & VRNT.

News and Technicals’

It’s becoming all too common, with the market setting new record highs based on vaccine news and federal stimulus hopes. The SP-500 tops 3700 for the first time in history as the Nasdaq prints its 50th record high for the year. As the markets surge higher, so goes the pandemic infections adding 1 million new cases in just 4-days. Phizer is now warning that people with significant allergic reactions shouldn’t take the vaccine after two of Britain’s National Health Service experienced severe reactions. However, both are not recovering, according to the national medical director. Citi Private Bank added its voice to the chorus of big investment banks predicting market gains in 2021 and went on to say it loves these ‘unstoppable’ trend. Mortgage rates continue to fall, setting the 14th record low of the year today, driving more refinance demand.

Without question, the bulls have shown remarkable resiliency and a willingness to buy almost anything, no matter the price. Trends remain strong as we continue to extend steeply away from technicals supports. Stay with the trend, but once again, I caution you to be very careful not to overtrade or chase already extended stocks. Remember, what goes up in a euphoric market rally tends to have severe correction consequences at some point in time. Be prepared in case the sentiment suddenly shifts.

The NASDAQ sets if 49th record high of the year even as the bears make half-hearted attempts in the SPY and DIA. While there are clues that the economy is slowing due to pandemic shutdowns, the bulls remain resolute, showing a willingness to keep extending. Even with vaccines coming to market, we still have a long winter ahead of us, and in the short-term, markets look very extended. Euphoric markets tend to last longer than most would expect, so stay with the trend, avoid chasing extended stocks, and be careful not to overtrade. Runs like this tend to end in an ugly way.

Asian markets closed modestly lower across the board overnight, and European markets see red with a Brexit deal hanging in the balance. Ahead of earnings, another light economic calendar, and Congress still unable to get their act together, U.S. Futures point to lower open.

Economic Calendar

Earnings Calendar

Although the earnings have been winding down, we still have several stepping up with quarterly reports. Notable reports include CHWY, GME, AZO, CONN, GWRE, HRB, THO., BF.B.

News & Technicals’

Although we had a little selling yesterday, it was very controlled, and by the end of the day, the bulls maintained control of the trends. The NASDAQ fought the selling, rising to its 49th high record for the year. The Pfizer vaccine has begun rolling out, with a 90-year-old woman in the UK receiving the very first dose. The UK is dubbing the event at V-day after suffering considerable losses across the country due to the pandemic. With the federal government facing a funding shutdown on the 11th, the best it seems that Congress can do is attempt to pass a spending bill that will cover a single week of operation as they continue to haggle over the stimulus bill. With management like that, it’s no wonder that the federal debt is quickly approaching 30 trillion.

Bulls remain in control of the trends, and the T2122 indicator continues to flash a short-term overbought condition. There are so many stocks looking parabolic; it’s very reminiscent of the euphoria present in the 1999, 2000 tech bubble. Although the market conditions are very different, the fear of missing chase of very extended stock prices is much the same. A euphoric market can last much longer than one might think, but it is usually swift and very punishing for those coming to the party late when they end. Although I sound like a broken record, I want caution traders to stay with the trend but guard yourself against overtrading and avoid chasing already extended stocks.

A slowing job growth proved to be no concern for the market on Friday, pushing all four indexes into new record territory. The rapidly rising pandemic infection rate, the death toll is, however, forcing states to increase restrictions as hospitalizations strain the capacity limits of the health care system. That said, no price seems too high as investors rush into stocks focused on stimulus hopes, vaccine news that points to 2021 recovery. However, at this elevation, if the market stumbles, the resulting pullback could be very painful if the market does suddenly decides we have pushed too high too quickly in anticipation.

Asian markets closed in red across the board overnight. European markets trade mixed as they push forward with last-ditch Brexit efforts. U.S. futures trade lower this morning but are will off the overnight lows as the morning lows as institutions try to keep investors buying, predicting a 2021 spring economic restart.

Economic Calendar

Earnings Calendar

We have several notable companies fessing up to quarterly results on the Monday earnings calendar. Notable reports include CASY, HQY, JKS, SFIX, SUMO & TOL.

News & Technicals’

Even with a sizable miss on the jobs front, the market continued to surge higher, setting new record highs on all four indexes. Futures markets are currently looking a bit lower this morning but have already bounced off the morning lows with the morning pump-up underway. As investors work the price, the market for a hopeful spring recovery of the pandemic rising oil prices becomes noticed at the gas pumps, with the national average price rising $0.04 a gallon. Simultaneously, the White House health advisor says this winter will be the worst event that this country has faced. California has issued a statewide stay at home order, and states around the country continue to ramp up restrictions measure to combat the spread.

Trends remain very bullish, and there seems to be a non-stop barrage from institution headlines predicting a massive restart to the economy in 2021. I certainly hope they are correct, but that has created a potentially dangerous short-term overbought condition. The T2122 indicator continues to warn that a pullback could begin at any time; however, stimulus hopes, vaccine news, record holiday salse, and 2021 predictions have investors willing to ignore the current pandemic economic impacts. How long this can continue is anyone’s guess but be careful not to overtrade because one day, the market may suddenly decide to care about the impacts, and the technical supports are a long way from current prices.

Ahead of the Employment Situation report, U.S. futures see nothing but bullishness, pushing for more record highs at the open. Let’s keep our fingers crossed that the pandemic, which is shutting down business all over the country, has not yet trickled into employment. The NASDAQ set its 47th new high record for the year in yesterday’s bull run even as hospitalizations reach critical capacity issues and the death toll surges. Have a plan just in case the market suddenly decides to care because it’s a long way to the daily 50-moving average.

Asian markets closed Friday trading mixed as SMIC shares plunge in Hong Kong after the Pentagon blacklisting. European market trade cautiously higher focused on U.S. stimulus efforts and Brexit issues. With a light day on the earnings calendar, the U.S. futures point to more recording highs ahead of the government’s reading on employment.

Economic Calendar

Economic Calendar

We have a light day on the Friday earnings calendar. Notable reports include BIG & GCO.

News and Technicals’

Bulls remain large and in charge, with the Nasdaq making it 47th new record high this year. News that suggested distribution issues with the new Phizer vaccine created a wild whipsaw near the end of the day. That said, the current market shakes off any concerning news, and the bulls rush back, bidding up already stretched and high priced stocks. Biden is endorsing the latest Covid stimulus deal saying it’s a good start, which would suggest even more deficit spending is on the way in his administration. A lot is riding on the 900 billion stimulus package success as Congress rushes to avoid a government shutdown on December 11th. In a surprising move, Warner Media announced that all scheduled 2021 new movies would simultaneously release to movie theaters and the HboMax.com streaming service. A massive blow to the theater business and a reminder of how the pandemic is reshaping the business landscape. Not that market cares, but there were more than 210,000 new infections reported yesterday and nearly 3000 deaths as hospitalizations soar, straining healthcare capacity. Also, in the news, the Pentagon blacklists China chipmaker SMIC and oil producer CNOOC in a reaction to a long history of Chinese espionage complaints.

Trends are most certainly bullish, and although all my trades are long positions, I’m becoming more and more concerned about the overextension I see so many stocks. Trade with the trend but guard yourself against overtrading and chasing already extend stocks. As yesterday’s vaccine news triggered the end of the day, whipsaw reminds us just how sensitive this market is and how quickly significant profits can disappear.