Reddit Squeezing and Russian Phishing

Markets started with a little gap (up a quarter percent on SPY, half percent on DIA, and down a tenth of a percent on QQQ). However, that was it for the day as markets traded sideways in a tight rant the rest of the day. This left all 3 major indices as small-body, black-body candles. It should be noted that all week stocks have been trading on very low volumes, as markets look ahead to a long weekend. On the day, SPY (+0.03%) was flat, DIA (+0.36%) gained a tad, and QQQ (-0.38%) lost just a bit. The VXX fell almost 5% again to 34.16, and T2122 sneaked into the overbought territory at 82.93. 10-year bond yields rose to 1.601% and Oil (WTI) was up nine-tenths of a percent to $66.79/barrel.

MSFT said in a blog post that the same Russian hacking group (MSFT has named the group Nobelium) that carried out the SWI attack early last year have launched a new attack. The impacts of last year’s catastrophic attack are still not fully known or at least have not been made public. However, it appears that the new attack has targeted at least 150 organizations globally. MSFT said that at least 25% of the targeted groups in the latest attack are humanitarian or human-rights-related organizations. However, governments, consulting companies, and non-governmental think tanks are also among the targets, which span 24 countries so far.

The Reddit crowd continues to pump the “meme stocks” as AMC shares shot up over 36% on the day and GME gained over 11%. AMC is up 121% on the week and GME up almost 44% over the same time. The so-called “short-squeeze” plays certainly work when the squeezers can collaborate on social media. These moves seem to be continuing in pre-market trading Friday.

Related to the virus, new US infections continue to fall. The totals rose to 33,999,680 confirmed cases and deaths are now at 607,726. However, the number of new cases is falling again and are back down to an average of 23,060 new cases per day (the lowest number since June). Deaths are also still falling and are now down to 526 per day (the lowest number since March 2020).

Globally, the numbers rose to 169,710,788 confirmed cases and the confirmed deaths are now at 3,527,082 deaths. The trends are better again as we have seen a slowing in the rate of increase now that India has passed its peaked. The world’s average new cases are falling quickly now, but remain at 538,292 new cases per day. Mortality, which lags, is also falling, but remains at 11,280 new deaths per day. SNY and GSK have begun Phase 3 trials of their own joint-venture vaccine.

Overnight, Asian markets were mixed, but leaned to the green side on very uneven trading. Japan (+2.10%), Taiwan (+1.62%), and Australia (+1.19%) stood out among the gainers. Meanwhile, losses were mild, with New Zealand (-0.50%) and Shenzhen (-0.30%) being the most significant. In Europe, markets are nearly all green so far today. The FTSE (+0.31%), DAX (+0.60%), and CAC (+0.69%) are typical of the continent at mid-day. As of 7:30 am, US Futures are pointing to another gap higher. The DIA is implying a +0.50% open, the SPY implying a +0.39% open, and the QQQ implying a +0.36% open…but some significant economic data lies ahead before the open.

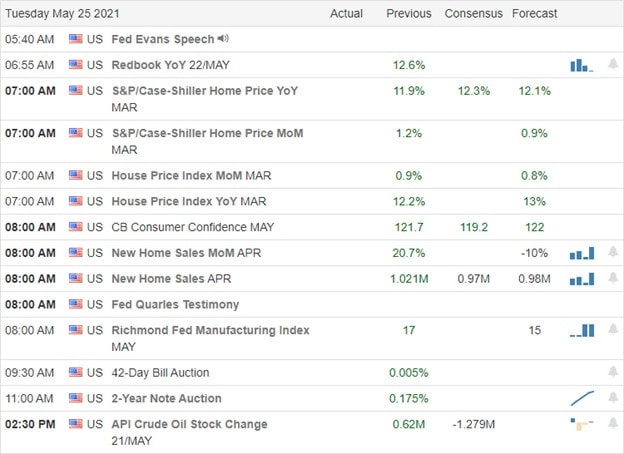

The major economic news scheduled for Friday include April PCE Price Index, April Trade Balance, April Personal Spending, and April Retail Inventories (all at 8:30 am), Chicago PMI (9:45 am), and Michigan Consumer Sentiment (10 am). Major earnings reports before the open include BIG and CAL. There are no major earnings reports after the close.

Markets are seeking to end the pre-holiday week on a positive note as the bulls look to make the first push of the day. Expect volume to dry up quickly today, but then again the entire week has happened on low volume. The PCE Price Index might have an effect if it touches the inflation nerve of Mr. Market. Beyond that, look for traders to square up their books, place their hedges, and hit the road early today.

As always, keep locking in profits as soon as you achieve your trade goals and maintain discipline by following your trading rules. Stick to the trend (appropriate for your trade horizon) and respect support and resistance levels (but don’t just assume they will hold). Consistency is the key to long-term trading success. So, keep hitting singles and doubles rather than swinging for the fence. Don’t forget to pay yourself on Pay Day, or that this is a long weekend. And enjoy the holiday!

Ed

Swing Trade Ideas for your consideration and watchlist: No trade ideas today. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service