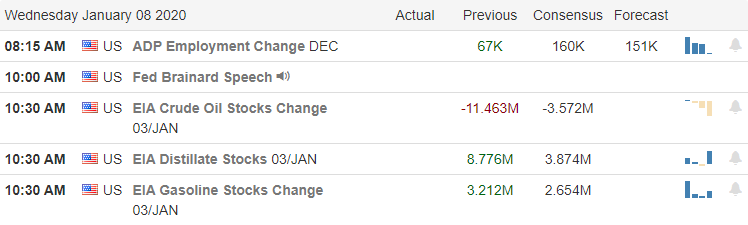

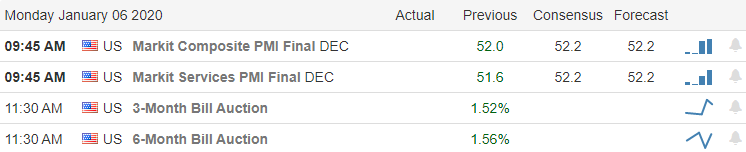

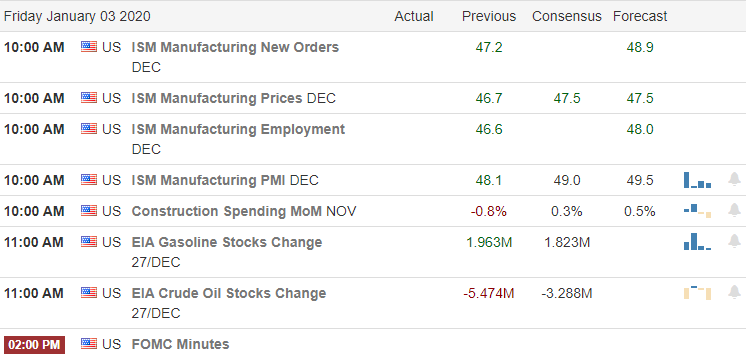

The bulls are running with wild abandon breaking records in

what seems an insatiable desire to buy up stocks. Closing at a new record high and only a few

points away for 29,000, the only stumbling block ahead is the Employment Situation

number that consensus estimates suggest a possible decline. Next week begins the 1st quarter

earnings season and the current rally seems to suggest tremendous confidence in

strong earnings outcome. Companies will

need to produce some impressive results to support current prices. Consider your rick carefully as we head into

the weekend.

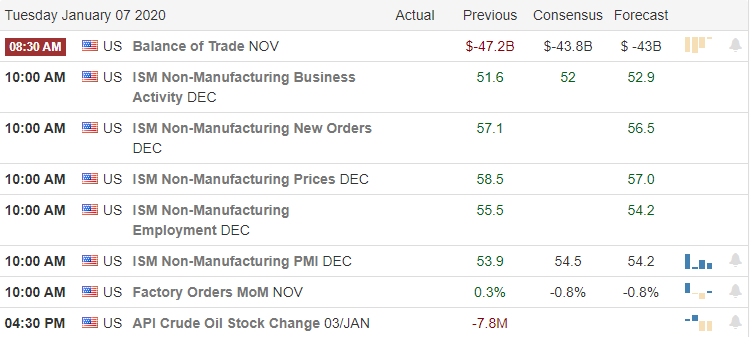

Overnight Asian markets closed the week mixed but mostly

higher. This morning European markets

are mostly bullish across the board as they continue to monitor US-Iran tensions. US Futures have been bullish throughout the

night and suggest a modest gap up open ahead of the Employment Situation

number. With the weekend quickly approaching

and the beginning of earnings season just around the corner, it may be a really

good time to take some profits and reduce some risk.

On the Calendar

On the Friday earnings calendar, we have just six companies fessing

up to quarterly results. However, the only

notable report today comes from INFY before the bell.

Action Plan

Another big day a rally yesterday as the bulls seems to have

an insatiable desire to buy up stocks. The

market gapped up to new record highs and continued to find more buyers throughout

the day. Futures this morning continue

to reach out for new highs ahead of the Employment Situation number at 8:30 AM

eastern. Such an exuberant rally ahead of earnings suggests the market believes

we will see substantial earnings growth this quarter. Analysts, however, are suggesting negative

growth is possible, which could create an interesting situation when earnings

season kicks off next week.

According to analysts, the price to earnings ratio is near a

20 year high. That could put a lot of

pressure on companies to perform nearly perfectly or suffer the result of disappointing

investors. It’s looking more and more likely

that Iran shot down the 737 with a Russian made missile. Iran has threatened additional retaliation. Amidst this uncertainty, the House passed a

resolution attempting to limit the Presidents’ power to take action with Iran. With the Dow, just a few points from reaching 29,000

for the first time ever, I’m guessing the institutions will do as much as

possible to get that headline. The only

possible stumbling block to that goal is the Employment number that consensus

suggests may decline today.

After an evening of missiles, turmoil, and rising tensions that

sent markets tumbling around the world, the message from the President that All

Is Well, restored frayed nerves and market prices. Shortly after the news of the attack, the Dow

Futures plunged more than 400 as a sobering reminder just how quickly geopolitical

events can affect the path forward for the market. Traders should carefully consider this and

plan their risk accordingly to protect themselves as tensions between the

countries remain very high.

Asian markets closed seeing only red overnight as oil and

gold prices spike after the Iranian missile attack. European markets have, however, recovered overnight

losses currently holding modest gains while closely monitoring developments. US Futures ahead of earnings and economic

reports now suggest a flat to slightly bullish open. Market jitters have subsided for now keep one

ear to the news as massive price volatility could be just one report away.

On the Calendar

On the hump day earnings calendar, we have 24 companies reporting

quarterly results. Notable reports

include STZ, BBBY, LEN, MSM & WBA.

Action Plan

After Iran fired more than a dozen missiles at Iraqi airbases

that house US troops. According to

reports, there were no lives lost in the attack but came with a warning from Iran

to withdraw forces from the area to avoid additional actions. Markets around the world quickly reacted with

the US Dow Futures sinking more than 400 points while gold and oil prices

spiked. However, after the President

issued a statement last night that all was okay, markets have recovered, but it

is a sobering reminder of how quickly geopolitical events can affect market

prices.

As tensions continue, traders should plan their risk

accordingly and always have a plan to protect your capital if this conflict

continues to escalate. As of yesterday,

the bullish trends remained intact, although the price action was choppy, reflecting

the uncertainty of the day. US Futures

now indicate a flat to slightly bullish open ahead of some notable earnings and

economic report. In times of turmoil, we

naturally first think of how the situation effect our money and ourselves. May I suggest we all take a minute to

remember our troops standing in harm’s way and their families undoubtedly

stressed and worried about their loved ones.

We risk only money, and they risk their lives to protect us!

Geopolitical fears proved to be no match for the relentless

march of the bulls yesterday. By the

close of the day, not only had they rejected the fear of the gap down but left

behind bullish engulfing candle patterns that held support and trend. However, the substantial rise in gold and oil

prices seems to be a huge contradiction to this exuberant bull run. As Iran promises retaliation and the US warns

waterway shippers of possible attacks, traders should plan their risk carefully

keeping a close on the developments in the middle east.

Overnight Asian markets also set aside retaliation fears

closing the day green across the board.

European markets are also rebounding this morning as fears seem to has

subsided. As I write this report US

Futures that boldly continued to rally overnight seem a bit more subdued ahead

of economic reports on International Trade, Factory Orders and the ISM.

On the Calendar

On the Tuesday earnings calendar, we have 10 companies

reporting with none that particularly notable.

Action Plan

The bulls shook off the fear of potential retaliation from

Iran yesterday rejecting the gap down lows of the last two trading days. To be honest, I’m not sure where the overall

confidence is coming from with Iranian generals publicly speaking about

retaliation and US warnings; they are concerned about waterway attacks. Nonetheless, the bulls remain relentlessly in

control of the trend that left behind bullish engulfing candle patterns on the

DIA, SPY, and QQQ.

Bullish is a good thing but over-exuberant blind bullishness

and become very dangerous so let’s hope it’s not the later. With the recent pullback, the T2122 indicator

has relaxed, allowing more room for the indexes to extend more to the

upside. However, there is a contradiction

in the VIX, which shows little to no fear while gold, (GLD) has gone nearly

parabolic in its rally over the last few days.

Overnight futures continued to push boldly higher as have oil prices

that at one point topped $70 a barrel yesterday. With little on the earnings calendar, the

market will look to the economic reports on International Trade, Factory Orders

and ISM numbers for inspiration. Also,

remember geopolitical news could create substantial reversals and price volatility,

so plan your risk accordingly.

Increased saber-rattling over the weekend as Iran and the US

exchange threats and tensions grow between the countries. Not surprisingly, markets around the world

are reacting negatively to the growing uncertainty. With little on earnings or economic calendar

to provide market inspiration, the news spin cycle will affect market sentiment

and price action volatility. Traders

will have to stay nimble and focused carefully on price action for clues. As of the close on Friday, index trends and

support held as the bulls stepped up to defend after the morning gap down. Unfortunately, we face a similar bearish gap

this morning.

Don’t forget me, I’m a tough guy too!

Asian markets closed in the red across the board as oil

prices jumped more than 2%. European indexes

are also trading negatively this morning as they monitor the growing tensions

between Iran and the US. Futures this morning

here in the US point to a substantial gap down open this morning to begin our

first full trading week this year.

Geopolitical events can create extreme shifts in sentiment as news comes

out. Plan your risk accordingly.

On the Calendar

On the Monday earnings calendar, we have just 4 companies

reporting, but none are notable and unlikely to any overall market effect.

Action Plan

With little on the economic and earnings calendar today, the

market will likely focus on the Iranian tensions and any news developments on

the subject. Over the weekend, Iran

voted to expel the US from the country and threats were made against the US

troops to be removed by force. The President

responded, saying the troops would remain right where they are unless Iran pays

back the American people for the expensive and newly created base. He also threatened sanctions like the country

had never seen before.

In response to the Iranian threat of retaliation, the

President said the US has picked out 52 targets if they do. Now the House, which is upset they were not

briefed on the Iranian airstrike, are trying to move forward a bill this week that

would attempt to limit Presidental powers.

As you might imagine, markets around the world continue to react negatively

to the saber-rattling and the uncertainty it creates. As of

the close on Friday, the bullish trend remained in tack and bulls had successfully

defended price support levels. Futures

this morning reflect the worry of the market pointing to a substantial gap down

at the open to begin our first full week of trading in 2020.

After a very exuberant Thursday rally, a US airstrike in

retaliation for the embassy attack is sending shock waves through the world

markets this morning. What a difference

a day makes as uncertainty once again raises its ugly head as we move toward

the weekend. As traders face an

uncertain weekend, it could easily trigger some profit-taking and increase the

overall price action volatility. Watch closely

if index price supports can stave off this initial knee-jerk reaction. If they begin to fail, profit-taking could

quickly increase.

Asian markets closed the day lower across the board but rather

subdued overall. European markets are

all in the red this morning in reaction to the Iranian tensions. US Futures point to a sharply lower open this

morning with the Dow indicating a gap down of more than 250. Buckle up; it could be a bumpy ride.

On the Calendar

On the Friday Earnings Calendar, we have 18 companies listed

as reporting, but just one confirmed report from LW and it happens to be the

only one that’s noteworthy on the day.

Action Plan

A day after an exuberant rally that set new records, the

market has a very different attitude this morning. During the evening in response to the invasion

of the US Embassy in Iran, a strategic killed one of Iran’s top generals

sending shock waves throughout the middle east and possibly escalating the

conflict. Qasem Soleimani is tied directly

to the deaths of over 600 Americans and was a very popular military leader in

Iran. What comes next is anyone’s guess,

and that uncertainty is evident with a quick look at the futures market.

Lettering design poster, banner.

The strong bullish trend over the last three months may

still hold after this morning’s knee jerk reaction, but overall, the market

hates uncertainty, and we can expect the VIX will respond to show some

fear. Keep a close eye on price supports

within the index trends. Failure of

supports heading into an uncertain weekend could set off a wave of

profit-taking. Remember, we have the

ISM, Petroleum Status and the FOMC minutes on the economic calendar along with

a parade of Fed speakers.

Friday’s close saw a little selling coming into the market with

the VIX bouncing up 6% by the close, but overall, the index trends remain bullish. Heading into another mid-week holiday with a

nasty winter storm spreading across the east coast low volume algo-driven chop

could be the bulk of price action after the opening rush. Trade and Housing numbers could provide some short-lived

inspiration, but our time may be better spent reviewing this year’s results and

preparing goals & plans for 2020.

Happy New Year

Asian markets closed the day mixed but mostly higher waiting

on November Hong Kong data. European markets

this morning are trading lower across the board but on light holiday volumes. US Futures suggest a flat to ever so slightly

bullish open ahead of the International Trade in Goods and Pending Home Sales November

results.

On the Calendar

On the 2nd to last trading day of 2019, the Earnings

Calendar indicates there are just eight companies reporting today but seven of

the report are unconfirmed and I don’t see a single notable report among them.

Action Plan

A New Beginning with Right Way Options in 2020

With a nasty winter storm spreading across the east coast

and another mid-week holiday facing the market trading volume is likely to diminish

quickly after the morning rush. We have little

to nothing on the earnings calendar for the market to react to, so it will likely

look to the economic calendar for some inspiration. Consensus expects a widening of the gap in November’s

reading on International Trade in Goods number at 8:30 AM Eastern and an

increase in the 10:00 AM Pending Home Sales report. Of course, news events could temporarily fire

up some price action, but most likely, the next couple of days will see a lot

of algo-driven chop.

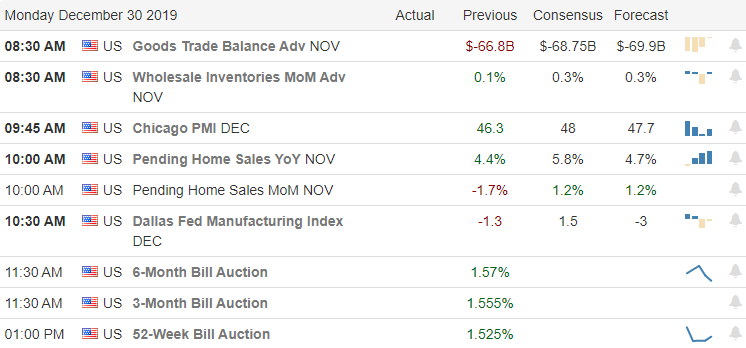

There is always the possibility of a little end of month

window dressing but there is also the chance we could see some end of year

profit-taking. Last Friday saw a slight

increase in the VIX, but so far this morning the US Futures are suggesting a

flat to ever so slightly bullish open.

Rather than trading, the next few days may be better spent reviewing

this year’s results looking for improvements to trading rules and plans. Perhaps, start by setting goals for 2020 and building

watchlists so that you can jump-start the New Year as a better, more prepared

trader.

Although Santa has returned to the North Pole and his jolly

Ho, Ho, Ho, has faded into memory, the big guys’ influence continues as the strong

retail numbers continue to inspire the bulls.

Lead by AMZN’s record-breaking sales results, there were new record

highs achieved in the DIA, SPY and QQQ on relatively low holiday volume. As we head into the weekend and the New Year,

the bulls seem to have plenty of momentum on their side, but be careful not to become

too complacent.

The count down has begun.

Asian markets finished the week mixed but mostly lower. European markets this morning see only green following

the optimistic lead of Wall Street. US

Futures point to a gap up open on this last Friday of 2019, fulled by momentum

with very little on the earnings or economic calendar to provide inspiration.

On the Calendar

On the Earnings Calendar, we have 18 companies reporting but

none are particularly notable.

Action Plan

Strong holiday retail sales continued to inspire markets

higher yesterday as it seems Santa’s influence remains strong this year. Once again, the DIA, SPY and QQQ reached out

for new record highs yesterday on low holiday volume. There is no doubt this has been an amazing

quarter to top off a truly remarkable decade for the market. As we slide into the weekend with just three

trading days left in 2019, the momentum is certainly with the bulls and there are

no indications in the price action they are ready to stop just yet.

Finish Strong!

However, we all know that what goes up must eventually come

down, so we must not get complacent and be ready to act if and when the bears

decide to reassert themselves. Futures

this morning point currently point to a mixed open with the Dow suggesting a

substantial gap up at the open. Gap up

opens at new market highs make me watchful of the dreaded pop and drop possibility

so be careful not to chase the open, wait to see if there are buyers that

follow-through. With such a strong trend

and momentum, follow-through may not be much of a wait even though there will

be very little inspiration in the earnings and economic calendar today.

Santa always seems to have some influence over the market during

this time of year but this year we have experienced an exceptional Santa Claus rally. A better than expected quarter of earnings, a

dovish FOMC, strong employment, and the Phase One tariff relief has made it pretty

easy for the jolly old man and reindeer to pull out record highs day after

day. With China now in the news

following through on tariffs cuts, the bullish trend shows no clues of stopping

just yet.

An RWO Membership is a great last minute Gift!

Asian markets closed mixed but with very modest gains and losses overall. European markets are trading mixed and mostly flat as traders seem to be taking profits and cutting risks heading into the holiday. US Futures point to modest gains this morning ahead of Durable Goods and New Home Sales numbers. After the morning rush, it would not be a surprise to light and choppy price action as traders head out for holiday plans. I would not rule out the possibility of some profit-taking at some point in the day.

On the Calendar

On the Earnings Calendar, we have just 13 companies

reporting on Monday. Ten scheduled on Tuesday

and with the market closed for Christmas on Wednesday, there will be no earnings

reports. Of the companies reporting, their none that are particularly notable the

entire week!

Action Plan

Santa’s Coming to Town!

With Santa’s reindeer pulling hard, the markets continue to rally

setting new records nearly every day. News

that China is cutting tariffs as part of the Phase One trade deal may allow

this Santa rally to continue on this eve of Christmas Eve. Today may be the best day of volume this week,

but traders should carefully consider the risks of the typical very low volume

that could easily continue right into the New Year. I would not be too surprised to see volumes

drop quickly after the morning rush of activity as traders head for their

holiday plans.

With nothing much to react to the earnings calendar, the market

will likely turn to the economic reports to find some inspiration. Keep an and eye on the Durable Goods report

at 8:30 AM Eastern and the New Home Sales numbers at 10:00 AM. As a reminder, Right Way Options trading room

will be open Tuesday and Thursday for chat only; there will not be a moderator. Of course, on Christmas day, the room is

closed. As a result, there will be no morning blog

post or Morning Market Prep Video until Friday.

I wish you and your family a very Merry Christmas!

Markets ignore impeachment of the President and power higher

once again, setting new record highs. Santa

Claus has done well this year! Now the

question on trader’s minds is, can this rally continue right into the weekend

or will there be some profit-taking as trade reduce risk ahead of the

holiday. With a light earnings calendar,

the market will likely look to the big reports on the economic calendar for inspiration. As of now, the bulls are solidly in control

of the bullish trends, and the bears seem to no willingness to fight back as

the VIX continues to decline.

Membership is a great Gift!

Overnight Asian markets closed the week mostly lower as

Japan’s automakers fall after the US House passed the North American trade

agreement. European markets see only

green this morning as the rally continues after the Phase 1 trade deal lifted

spirits. Here in the US, the Futures

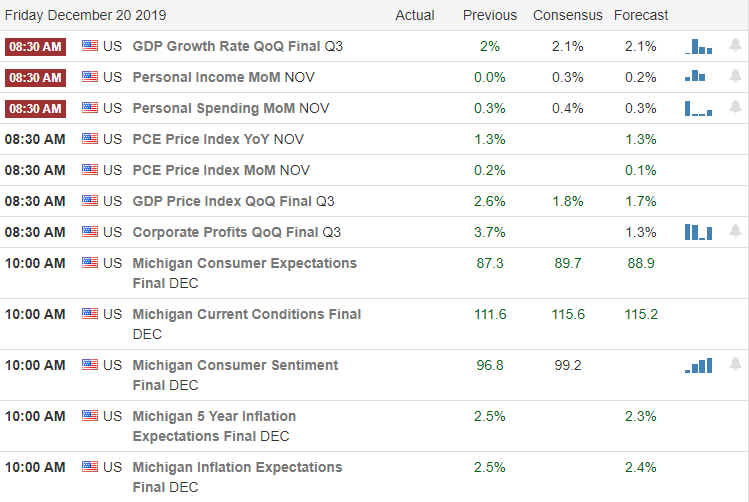

currently point to a flat slightly bullishly leaning open ahead of GDP, Personal

Income and Outlays, & Consumer Sentiment reports.

On the Calendar

On the Friday Earnings Calendar, we have just 14 companies fessing

up to their results. Notable reports,

BB, CCL, & KMX.

Action Plan

Markets defied the Presidential impeachment by the House

rallying to new record highs confident that the Senate will respond with an

acquittal. With the mid-week holidays

just around the corner, Santa has delivered the market a very nice rally without

the wild volatility. Perhaps this

bullishness can continue right on through the new year, but being a little more

conservative, I’m likely to go to the bank today, lowering my risk into the

weekend. Don’t get me wrong; there is

nothing in the charts at this point that suggests bearishness but anything can

happen over the weekend and I’m happy with a bird in the hand.

Five Golden Rings!

With a relatively light day on the earnings calendar, I

would expect the market to look to the economic reports of GDP, Personal Income

and Outlays, & Consumer Sentiment to find inspiration today. Consensus estimates suggest the reports will remain

strong so a surprise reading could upset the apple cart, so as always, stay focused

on price action for clues. If you’re

traveling this weekend to join family and friends to celebrate Christmas, I

wish you all safe travels and a Very Merry Christmas!

You can’t make this stuff up! While the market consolidates at record highs,

the House votes to impeach the president while he takes the stage at a packed

out campaign rally. Thus far, the market

seems to have taken the vote in stride as the bullish trend remains intact. With several earnings and economic reports this

morning, perhaps the market can find some inspiration to break out of the

consolidation that began after the Monday morning rally. However, with the Holiday’s just around the

corner volume is likely to remain light after the morning burst of energy.

Asian markets closed mixed but mostly lower overnight, with

the central bank holding rates steady. European

indexes trade mixed but slightly lower this morning after the Bank of England announces

no rate changes. US Futures have bounced

around the flat-line this morning with an ever so slight bullish lean ahead of

an economic calendar data dump.

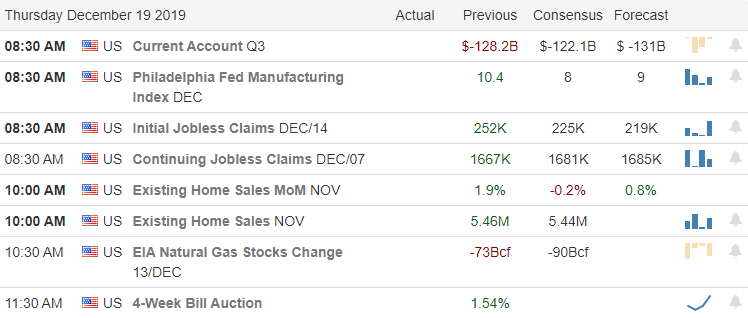

On the Calendar

On the Thursday Earnings Calendar, we have our biggest day this

week, with 26 companies reporting. Among

the notable reports are RAD, ACN, CAG, DRI, SAFM, FDS & NKE.

Action Plan

As expected, the market wandered sideways in consolidation, waiting

for some inspiration. During the evening,

the full House voted to impeach President Trump. The tally showed that not one of the President’s

party voted in favor of the impeachment with just a few from the opposing party

not voting to impeach. So far, the

overall market has seen no reaction to the vote. Overall the bullish trends remain intact and

the bulls have the upper hand although there was a tiny hint fear with the VIX

rising ever so slightly at the close yesterday.

After the bell yesterday MU reported better than expected

earnings lifting the stock and this morning, we have a few reports that may

help the market find some inspiration.

However, it’s more likey it will be the economic reports, Jobless

Claims, Philly Fed Survey, & Existing Home Sales that will fuel the bulls

or bears this morning. With the Holiday’s

rapidly approaching, don’t be too surprised if a morning burst of energy quickly

fades into light and choppy price action.