A spreading virus threat, a big week of earnings, economic data including an FOMC rate decision as well as an ongoing impeachment trial, could prove to be the perfect storm for price volatility. Markets around the world are reacting to the quickly spreading threat of the coronavirus that’s injecting a huge economic uncertainty to its potential impacts. Markets hate uncertainty and not much that creates more fear than a spreading contagion with no cure. Plan your risk very carefully as quick news-driven reversals and large morning gaps are possible during this uncertainty.

Japan traded lower in response to the virus, while most

Asian markets remain closed for the lunar holiday. European markets are falling sharply this

morning as virus fears grow, and US Futures are reacting sharply lower this morning

as well. At one point, Dow futures fell

500 points but have recovered slightly this morning now suggesting a gap down around

400 points at the open. Hold on for a

bumpy ride!

On the Calendar

On the Monday earnings calendar, we have over 70 companies reporting. Notable earnings include ARNC, CR, DHI, GGG, HMST, JNPR, & WHR.

Action Plan

We all knew there was an overextended condition in the

market, but who could have guessed it would be a microscopic virus that would

bring out the bears. With now five

confirmed cases here in the US, nearly 2900 cases worldwide and over 450 people

now listed as critical worries of severe economic impacts rose dramatically

over the weekend. Oil prices dropped

into the low 50’s as travelers are choosing to reduce their movements. In China, more than 25 million people are locked

down in cities where public travel has stopped operating and many businesses

have closed during their biggest holiday session. During the evening, the Dow futures dropped

500 points as markets around the world react to the quickly spreading virus.

We have a huge week of earnings with some of the biggest

companies reporting this week along with and FOMC rate decision and a big week

of economic reports. Combine all of that

with virus jitters and ongoing impeachment trial, we have the conditions for

the perfect storm of price volatility.

Plan your risk very carefully!

Inexperienced traders might want to consider sitting this out and protecting

your capital until this uncertainty passes.

Expect quick news generated price reversals and large morning gaps that

could be up or down, and the market reacts to the unknown.

The worry over the spreading coronavirus roused the sleeping

bears temporarily but calming words from the World Health Organization allowed

them to drift back into dreamland. By

the end close of the day, the bulls were solidly back in control and with the

big earnings beat out of INTC new records in the NASDAQ are likely at the open

today. During the night, the WHO held

off on declaring a global health emergency for now but it will be interesting to

see how the market deals with that pending possibility as we head into the weekend.

Asian market rallied from early lows to close the week mixed but mostly bullish after the WHO decision. European markets are decidedly bullish this morning in reaction to the WHO holding off on a global declaration. US Futures also saw a strong bullish reaction during the night, now pointing to a solid gap higher ahead of morning earnings reports and the latest reading of the PMI number at 9:45 AM Eastern.

On the Calendar

On the Friday earnings calendar, we get a little break with

just 36 companies stepping up to fess up to their results. Among the notable for the day are NEE, APD,

AXP, SYF, & SNV.

Action Plan

After a rather volatile day of price action, while the

market expressed its concern for the spreading coronavirus, those tenacious

bulls came charging back. During the

early evening, the futures traded positively but with rather modest gains until

the WHO decided to hold off on declaring a global health emergency at least for

now. After their decision, Asian markets

found their footing climbing out of the negative with following European indexes

following suit and US futures extending their bullishness. The big earnings beat from INTC after the bell

looks to not only recover yesterday’s modest selling but open at new record

highs this morning.

Now with 25 lives claimed by the virus and those infected

expanding to over 800, it will be interesting to see how the market responds heading

into the weekend. Next week some of the

biggest tech companies report such as MSFT, AAPL, FB, and AMZN. At current prices, there will be a lot of

pressure to perform, so let’s hope none of them stumble and that the health officials

begin to win the fight against corona and we can avoid the major economic

impacts of travel restrictions. As

normal, I will be looking to reduce my risk heading into the weekend, tucking in

gains for a restful and relaxing weekend.

The wild-eyed bullish charge slowed the last couple days as

early rally’s struggled to hold onto the highs.

However, the bears seem to be in hibernation with little to no willingness

to even test index price supports. Trends

remain bullish as we head into the biggest day earnings reports this week. The impeachment trial in the Senate seem to

be little more than a distraction during the spreading coronavirus is stealing the

media attention from the political drama.

As earnings roll out anything is possible so stay focused on price and

plan your risk carefully.

Asian markets closed seeing only red as China locked down two cities attempting to slow the spread of the virus that has now infected nearly 600. European markets keeping an eye out for an ECB decision and new worries about trade with the US currently have their indexed mixed but mostly lower this morning. Even the US Futures are displaying caution this morning with mixed but slightly bearish results ahead of a big day of earnings reports.

On the Calendar

We have our biggest day of earnings reports this week and the

1st quarter reports with more than 100 companies in the hot seat

today. Some of the notables include AAL,

CMCSA, DFS, ETFC, FCX, INTC, ISRG, JBLU, KEY, KMB, MTB, ORI, SWKS, LUV, TRV,

UNP & VFC.

Action Plan

The little rally yesterday ended the day little changed with the Dow closing down less than 10 points. Although the indexes appear overbought and stretched away from key moving averages, the bears seem to be hibernating with little to no interest in attacking at the moment. During the night, China put 2 of its cities on lockdown as the coronavirus continues to spread with nearly 600 confirmed cases and 17 deaths so far. As a result, Asian markets were red across the board as the fear spread amongst investors. European markets are trading flat to slightly bearish this morning as they wait and ECB decision and the worry of trade issues rising after tough Presidential talk.

Overall index trends remain bullish and thus far, no daily

price support levels have breached. To

find anything remotely bearish in the indexes, you have to look at 15 min.

charts to see downtrends possibly developing.

With a big of earnings reports, anything is possible but futures are trading

mixed to slightly lower this morning choosing a little caution rather than the

wild-eyed bullishness we have experienced the last several weeks. I would not be at all surprised to see a

surge of volatility this morning as earnings roll out.

The bulls bang-out more new records pushing GOOGL into the 1

trillion market cap club and price to earnings growth hits the highest level since

Bank of America started recording the metric in the ‘80s. How much further can you go? That’s anyone guess, but as retail traders,

we must guard ourselves against getting caught up in the exuberance over-trading

or chasing trades already up several days in their bull run. With a 3-day weekend approaching, it may be

wise to take some profits and reducing risk in case sentiment happens to shift over

the weekend.

Asian markets closed the trading week, seeing green across

the board after China reported their economy grew as expected. European markets have also reached out to new

record highs this morning in reaction to the big gains in the US and China

news. This morning US Futures continue

to climb, suggesting a modest gap up open ahead of earnings and economic

reports.

On the Calendar

On the Friday earnings calendar, we have 21 companies

reporting results. Notable reports

include CFG, FAST, JBHUT, KSU, RF, SLB, & STT.

Action Plan

More new records attained as the bulls continue to surge

higher with wild abandon. Bank of America

reported that Price to Earnings Growth is now 1.8 hitting the highest level

since they began recording the number in the ’80s. For reference, a reading 1.0 PEG is considered

an overbought condition. That said,

nothing seems to stop the bulls from stretching this rally that pushed GOOGL to

a 1 Trillion market cap during yesterday’s bullish session. With a three-day weekend approaching, futures

currently suggest another gap up open and more record highs today with no sign

of slowing down just yet.

Trading such an overbought condition requires a strong adherence to your trading rules. It’s very easy with all the bullish exuberance to get caught up, tossing caution to the wind and over-trade. I have no idea when the tide will change, but believe me when it does; you don’t want to be over-invested because the reversal can be swift and extreme. Stick to your rules, size your trades properly, don’t chase stocks well into their run or when they are testing price resistance levels, have an exit plan if you’re wrong and remember to take some profits along the way! I wish you all a wonderful 3-day weekend.

Bad news at Boeing and a spreading coronavirus roused the

bears for a 150 point Dow pullback yesterday, but the futures point to gap up

open this morning as the relentless bulls keep buying with no regard to the extended

prices and historically high price to earnings ratios. As we begin our biggest day of earnings

reports this quarter, it looks like the lowered analyst’s estimates could continue

to fuel the markets even higher. However,

a word of caution. With stocks priced well

beyond perfection compared to earnings growth, keep in mind just one stumble

could trigger a quick reversal, so plan your risk carefully.

That is Question?

Asian markets shook off concerns of travel restrictions due

to the spread of the coronavirus to close green across the board

overnight. European markets are however,

muted at this hour showing mixed and cautious trading. US Futures tossed caution to the wind rising

sharply overnight and continue to point to a substantial gap up as ravenous

bulls can’t seem to buy up high priced stocks fast enough.

On the Calendar

On the Hump day earnings calendar, we have the largest

number of reports so far this season, with over 80 companies fessing up to

their quarterly results. Notable reports

include ABT, ALLY, BKR, CTXS, FITB, JNJ, KMI, LVS, RJF, RCI, SLM, STLD, TER, &

TXN.

Action Plan

A bit of nervousness about the coronavirus temporarily woke

up the bears yesterday with concerns that this contagious and very deadly virus

could damage the economy restricting travel around the world. Of course, the news that Boeing expects further

delays before getting approvals to put the 737 Max back in the air aided in the

selling yesterday after the company broke down below a key price support level. After the bell, NFLX posted better than

expected earnings but disappointed on subscriber number particularly in the US

and Canada. The initial price reaction

was lower, but this morning NFLX is indicated modestly higher. IBM, after reporting five straight quarters

of decline, finally found the right stuff to top analysts estimates as their acquisition

of Red Hat helped them turn the corner.

Even with the 152 point decline in the Dow, yesterday index

trends remain intact with no break of price supports in the daily charts. Futures have been in bullish mode all night long

as we head into the biggest round of earnings so far this season. In an interview, the President proclaimed the

Dow would be 10,000 points higher if not for the Fed and indicated he was in pursuit

of another tax cut to help it along even more.

Stay bullish but remember that many stocks are priced well beyond

perfection. Any stumble could create a

quick and substantial pullback so carefully plan your risk carefully and resist

chasing stocks already running.

The bulls bang-out more new records pushing GOOGL into the 1

trillion market cap club and price to earnings growth hits the highest level since

Bank of America started recording the metric in the ‘80s. How much further can you go? That’s anyone guess, but as retail traders,

we must guard ourselves against getting caught up in the exuberance over-trading

or chasing trades already up several days in their bull run. With a 3-day weekend approaching, it may be

wise to take some profits and reducing risk in case sentiment happens to shift over

the weekend.

Asian markets closed the trading week, seeing green across

the board after China reported their economy grew as expected. European markets have also reached out to new

record highs this morning in reaction to the big gains in the US and China

news. This morning US Futures continue

to climb, suggesting a modest gap up open ahead of earnings and economic

reports.

On the Calendar

On the Friday earnings calendar, we have 21 companies

reporting results. Notable reports

include CFG, FAST, JBHUT, KSU, RF, SLB, & STT.

Action Plan

More new records attained as the bulls continue to surge

higher with wild abandon. Bank of America

reported that Price to Earnings Growth is now 1.8 hitting the highest level

since they began recording the number in the ’80s. For reference, a reading 1.0 PEG is considered

an overbought condition. That said,

nothing seems to stop the bulls from stretching this rally that pushed GOOGL to

a 1 Trillion market cap during yesterday’s bullish session. With a three-day weekend approaching, futures

currently suggest another gap up open and more record highs today with no sign

of slowing down just yet.

Trading such an overbought condition requires a strong adherence to your trading rules. It’s very easy with all the bullish exuberance to get caught up, tossing caution to the wind and over-trade. I have no idea when the tide will change, but believe me when it does; you don’t want to be over-invested because the reversal can be swift and extreme. Stick to your rules, size your trades properly, don’t chase stocks well into their run or when they are testing price resistance levels, have an exit plan if you’re wrong and remember to take some profits along the way! I wish you all a wonderful 3-day weekend.

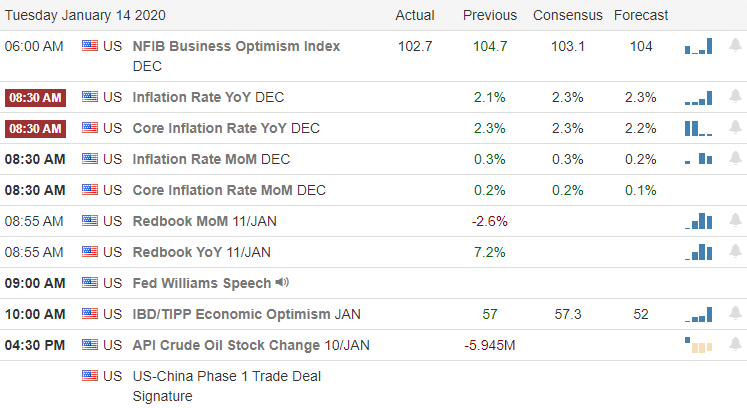

The Dow closes above 29,000 setting new records amidst a volatile afternoon of price action that required a last-minute rally regain that key psychological level. With the Phase 1 trade deal finally signed skeptics of the deal seem to have inspired the bears to begin probing for weaknesses creating a little price volatility, but so far, the bulls have proved to defend each attack. Although stocks are rising, so many appear very stretched out or testing resistance highs traders, have to be very careful not to over-trade and chase entries.

Good Morning! Do I smell Friday on the way?

Asian markets closed mixed but mostly higher seesawing around the flat-line most of the session. European markets are lower across the board being less than impressed with the partial trade deal with China. However, here in the US, there appears to be no tepidness whatsoever with the Futures pointing to yet another significant gap up that will set new records. Over exuberance like this can sometimes end badly, so plan your risk carefully and have an exit plan ready to go if sentiment reverses.

On the Calendar

On the Thursday earnings calendar, we have 29 companies fessing

up to quarterly results. Notable reports

include BK, SCHW, CSX, MS, PBCT, PPG, & TSM.

Action Plan

For the first time, the Dow closed above 29,000 amidst a volatile afternoon session after the signing of the Phase 1 trade deal. In the deal, China has agreed to buy 200 billion of Ag products based on market conditions over the next two years. As you might imagine, skeptics abound that China intends follow-through on the deal. Next week the Senate begins the impeachment trial of President Trump. Although the Senate is expected to acquit the president of all charges, it’s likely to serve as a major distraction next week with a wall-to-wall media circus.

Index trends continue to remain bullish though the price action

indicates that the bears are probing for weaknesses creating a little volatility. That being said, the bulls seem to have relentless

energy recovering from a late afternoon selloff in the last couple minutes of

the day. Today we have a few potential

market-moving earnings events and a big morning of economic data to inspire the

bulls or bears. I suspect the Retail

Sales figures will be the biggest focus today after TGT reported holiday toy

sales were lower than expected. Ahead of

all this data, the futures once again point to a substantial gap up open. As always, guard yourself against the fear of

missing out emotion by waiting to see if actual buyer follow-through after the gap

before committing to additional risk.

Is the bull weakening or just taking a break hoping to find

inspiration in big bank earnings and the signing of the Phase 1 trade

deal. With a push in very select stocks,

the Dow once again pushed through the 29,000 barrier but was unable to hold it through

the close after being reminded that tariffs will remain in place for the immediate

future. As always, during earnings

season, anything is possible, so set aside bias and focus on the price action

for clues.

Asian markets closed in the red overnight ahead of the

signing of the Phase 1 deal. European

markets are mixed this morning trading very near the flatline, cautiously as

they monitor earnings results. US

Futures traded in the red overnight but have paired most of the losses ahead of

earnings, economic, and the Phase 1 signing ceremony that seems to have lost

its luster among the bulls.

On the Calendar

On the Hump day earnings calendar, we have just 22 companies

reporting today but there are several potential market-moving reports. Among the notable are UNH, AA, BAC, BLK, GS,

KMI, PNC, USB, & PNC.

Action Plan

After a little struggle, the Dow finally found the

inspiration to rally breaking temporarily above 29,000 but was unable to hold

it by the close. While we have the

signing of the Phase 1 deal, later today, tariffs will stay where they are until

there is confirmation of China’s compliance with the agreement, and Phase 2

negotiations begin. Most agree that it will

likely be after the Presidental election.

Although there was a bit of a bull/bear struggle in the price action

yesterday, the bullish trends remain intact.

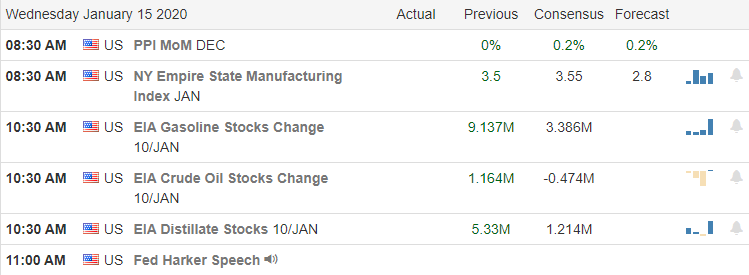

Today we have several potential market-moving earnings

reports and an economic calendar that includes PPI, Empire State MFG., Petroleum

Status numbers and the Beige Book.

Futures traded lower all night, but the morning pump has already begun now

pointing to a flat open before we get the reports from BAC & GS. As of yesterday, it looked as if the bulls started

running low on energy but perhaps they can be reenergized this morning by strong

bank earnings. Stay focused on price and

guard yourself against over-trading while price deals with resistance while

working to hold trend.

With a choppy overnight futures session and very high price-to-earnings multiples, the first earnings season of a new decade officially begins today! Yesterday the bull run continued with new record highs in the SPY and QQQ even as analysts expect sub-par year-over-year earnings performance. The question on everyone’s mind is, will it matter or will the tenacious bulls continue to lower their head and push even higher. Only time will tell. In such a strong bull market, it’s very easy to become complacent and over-trade. Plan your risk carefully, and even though the trend remains strong, make sure you have an exit plan and understand the risks you are taking in case the bears come out of hiding and begin to impose their will.

Asian markets overnight closed mixed but mostly lower as the

Yuan rose ahead of the Phase 1 deal signing.

As I write this report, European markets are trading modestly lower

across the board. US Futures markets have

been choppy ahead of the big bank earnings that will likely set the stage for

today’s market.

On the Calendar

Today is the official beginning of the 1st

quarter earnings season, which seems to extend almost all the way into the 2nd

quarter. Make sure your checking when a

company reports before making a trading decision as part of your trade planning

to avoid possible unfortunate surprises.

We have 20 companies reporting today, with the most notable being DAL,

C, JPM, SPHA, INFO, WFC, & WIT.

Action Plan

We have seen rather choppy futures overnight heading into the

official beginning of 2020 earnings.

Trends have been incredibly bullish ahead of a week outlook for earnings

results, but the big question is, will it matter? Year over year, comparisons show that companies

are making less; consequently analysts lower the expectations bar making it

easier for the company to leap over the target.

With price-to-earnings multiples going higher and higher as stocks

continue to race higher, we have to question how long this condition can

continue.

Analysts seem to suggest a market pullback is likely, but

the very strong bullish trend would seem to suggest the bulls don’t care what

the analysts think. Another imbalance we

currently see in the market is that only 5-companies, AAPL, GOOGL, AMZN, MSFT, and

FB make up 18% of the total market cap of the entire S&P-500. According to Morgan Stanley, this is

unprecedented dominance, while Bank of America is warning the “rising correlation

and concentration risks’ for the market.

So what is the retail trade to do?

Set aside your bias, focusing on the price action on the indexes and the

stocks you choose to trade. Plan your

trades, understand the risks before entering and trade your plan with the

knowledge that Price is King!

After briefly breaching 29,000 with a very narrow large-cap

leadership, Friday’s price action ultimately left behind bearish engulfing candle

patterns while still solidly holding onto bullish trends. With earnings season kicking off on Tuesday

with big bank reports, the expected signing of the Phase 1 trade deal on

Wednesday, and a busy economic calendar, traders will have to be ready for

almost anything. In such a strong

bullish run, it’s easy to become complacent, but with stocks trading at such

high multiples, that would be unwise. Plan careful, and never forget the market can

quickly shift direction.

Asian markets closed green across the board last night as

they await the signing of the Phase 1 trade deal. European markets, however, are trading

cautiously this morning with indexes flat to mostly lower focused on developing

geopolitical tensions with Iran. US

Future this morning seems to be tossing caution to the wind pointing to a gap

open. With Friday’s bearish engulfing

pattern, be very careful chasing into this morning gap.

On the Calendar

On the Earnings Calendar, we have just 12 companies reporting

results but there is only company SJR that’s particularly notable today. However, keep in mind 1st quarter

earnings season kicks off on Tuesday with several big bank reports.

Action Plan

There was a very interesting weekend of news with talking

heads issuing very contradictory predictions of the future direction of the

market. Protestors hit the streets in Iran

after the government admitted to downing the Ukrainian 737 passenger plane. The President has come out in support of the

Iranian protestors noting their courage is inspiring. At the same time, the Iranian leadership continues

to threaten additional retaliation. Scheduled

for Wednesday this week is the expected signing of the Phase 1 trade deal with

China, that’s to provide some protection for US intellectual property as well

as large Ag purchase commitments from China.

With markets already at very high multiples and expectations

of slower earnings growth, reports indicate that GS, BAC and other large

investment banks are advising their clients to move assets to a more passive

dividend collection strategy as they expect only a 2% market growth in the coming

year. At the same time, others are

suggesting 2020 could be a solid earnings growth year and projecting substantial

market growth. I think all the contradiction

would suggest that no one can predict the future and the best we can do as

retail traders is to setaide our bias, focus on the charts, and price action

within. Up, down or sideways price action

will lead the way to a profit.