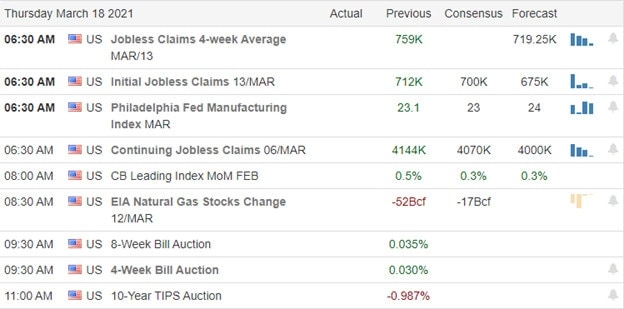

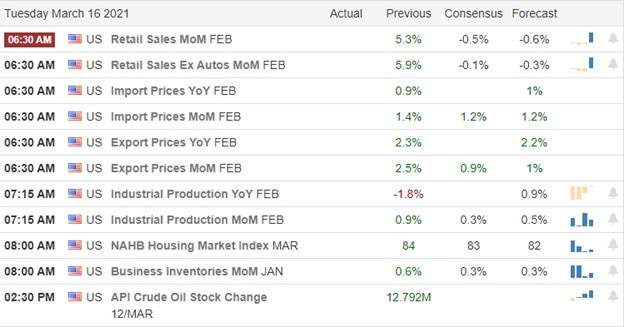

The possible inclusion of outdated data in its vaccine trial has AstraZenica back in the headlines this morning. After a nice relief rally that printed bullish morning star patterns in the SPY and QQQ, U.S. futures now suggest a follow-through to confirm the pattern could see a challenge by the bears. With a joint effort to sanction China by the U.S, EU, UK, and Canada, markets hold their breath, wondering what the Chinese retaliation could entail. Though Powell’s comments softened Treasury yields yesterday, they remain in bullish trends, so keep an eye on them.

Asian markets closed lower overnight after a choppy session, responding to a lackluster Baidu debut in Hong Kong. Across the pond, European markets trade with modest losses across the board as the new lockdown measures shake recovery sentiment. Ahead of earnings, New Home Sales, and another big day of Fed speak, futures markets point to some modest bearish pressure at the open. Stay focused.

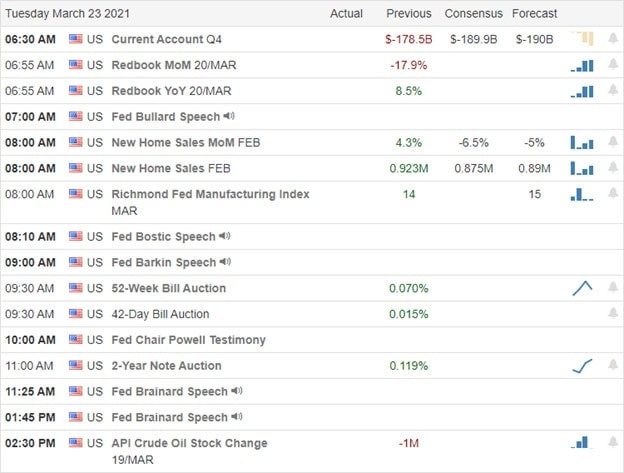

Economic Calendar

Earnings Calendar

The Tuesday earnings calendar has 49 companies listed, with 35 verified reports stepping up to quarterly results. Notable reports include GME, CHWY, ADBE, HOME, HUYA, INFO, & SCS.

News and Technicals’

AstraZenica is back in the news this morning but for the undesirable reason that they may have included outdated data in the vaccine trial. This morning, Tesla also has some undesirable news for firing an employee that is part of a whistleblower complaint to the federal safety investigation over solar fires. In a coordinated action, the U.S., EU, UK, and Canada imposed sanctions on Chinese officials on Monday. The countries cited human rights abuses which, of course, China has denied. We wait for the Chinese retaliation that will likely add tensions between the countries with trade ramifications possible.

Yesterday’s rally was a nice relief as the Powell comments softened bond yields. However, the treasuries remain in bullish trends that we will have to keep an eye on due to the market implications. The SPY and QQQ left behind morning star type patterns, but futures markets currently suggest the indexes may have some trouble following-through bullishly due to U.S./China tensions. Selling pressure in the financial sector and energy sector added minor technical damage to the IWM, putting in a possible lower high at price resistance yesterday. Further selling could intensify the concerns today. Keep in mind the SPY, QQQ and IWM now have overhead price resistance that must clear if it is to resume the rally. Stay focused and flexible.

With the third wave of infections expanding across Europe, the country has gone back into lockdown. However, recovery hopes and the massive stimulus are on investors’ minds here in the U.S., with officials monitoring the rising cases in 21 states. With the 10-year treasury softening, perhaps the NASDAQ can gain enough relief to challenge its 50-day average as resistance. Though the DIA, SPY, and IWM left a reason for caution selling-off into Friday’s close, the bulls still control the trends. With Powell speaking three times this week and a busy economic calendar, price volatility is likely to remain high.

Asian markets closed the day mostly lower as the Turkish Lira weakens sharply. European markets are trying to shake off the 3rd lockdown as they chop around the flat-line this morning. U.S. futures are mixed up well off overnight lows as the morning pump begins ahead of Powell and the Existing Home Sale number. Plan carefully and avoid complacency.

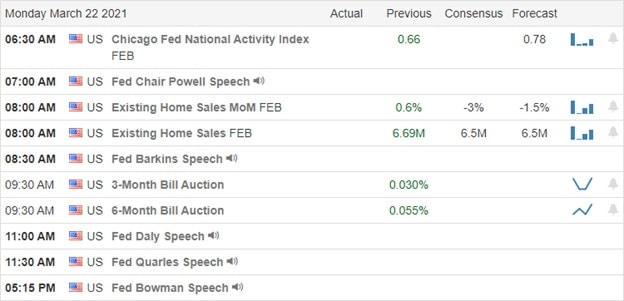

Economic Calendar

Earnings Calendar

Monday, we have 60 companies on the earnings calendar, but only 13 have verified their reports. Notable reports include NEWT, SNX, & TME.

News & Technicals’

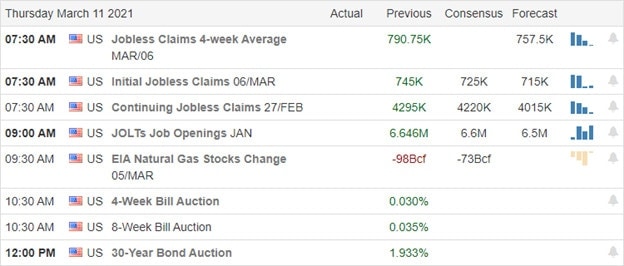

As we begin the week, Europe is back under lockdowns as the third wave of infections dash hopes for a spring recovery. Sadly, infections are reportedly rising in 21 states, with officials warnings against reopening too quickly and relaxing masking requirements. Canadian Pacific railway will buy Kansas City Southern for $25 billion if approved by regulatory agencies creating the first rail network connecting the U.S. and Canada. Treasury yields have softened slightly this morning, but according to Jim Bianco say it will not last, expecting they will heat up again in the second half of the year as the U.S. recovers economically.

Although Friday markets found sellers into the close, the DIA, SPY, and IWM are technically in pretty good shape, even though the candle patterns warrant a little caution. The QQQ remains the most technically vulnerable, having failed at a lower high below its 50-day average. Although we got past the FOMC announcement last week, we have a Fed speaker parade, including Jerome Powell Monday, Tuesday, & Wednesday. With Europe back in lockdown, futures are trying to rally off of overnight lows ahead of Powell’s speech and the latest reading on Existing Home Sales.

The calming words and dovish Fed policy meet with a feisty bond market worried about inflation, creating a failure of the 50-day average as techs suffered. Rising bonds engaged the bear in the market around the world during the night, even as a flurry of institutional reports try to calm fears. The good news is that bond rates have softened slightly this morning, allowing the future to breathe a sigh of relief. With concerning candle and price pattern in the charts to overcome the bulls will have to work overtime.

Overnight Asian markets closed the week with red across the board due to inflation worries. European markets also see red across the board this morning, spooked by the rising bond rates. However, here in the U.S., futures markets are green across the board, trying to put a brave face on concerning situation. Keep an eye on those bond prices and remain flexible.

Economic Calendar

Earnings Calendar

We have a light day on the Friday earnings calendar with less than 30 companies, but of those, there are only eight verified reports. With mostly small-cap companies reporting, the only notable I can come up with is ERJ.

News & Technicals’

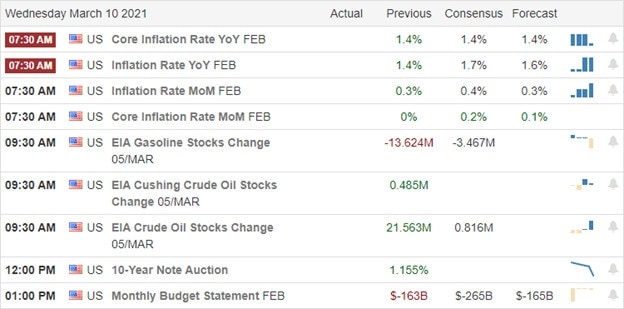

Feisty bond markets seemed to reject the calming words of Jerome Powell as worries of inflation pushed bond rates higher. Markets around the world have also reacted negatively, but the bulls are pushing back this morning after a flurry of institutional reports trying to calm nerves. The first U.S. – China meeting under the new administration began with long-winded speeches criticizing each other and flinging insults. It will be interesting to see how the meeting progresses today. The 10-year Treasury yields are moderating slightly this morning after touching a 14-month high bring a sigh of relief to the futures. Amazon has become the new home of the NFL after closing an 11-year media rights deal for Thursday night games. The U.S. House passed two immigration bills yesterday afternoon that creates a path to citizenship for millions setting up a fight in the Senate.

Yesterday’s selloff raises the level of caution, leaving behind potential bearish candle and price action patterns on the index charts. However, the bullish trends in the DIA, SPY, and IWM still exist, with the bearish failure of the QQQ at its 50-day average making up the bulk of the concern. Should those pesky bonds remain elevated, the tech sector could continue to struggle. Unfortunately, we have inserted the tech giants into the DIA and SPY indexes and given them a tremendous weight in the average. Should they continue to struggle, so could the overall averages. It would be wise to keep an eye on the bond market and avoid complacency.

Jerome Powell waved his exceedingly dovish magic wand, calming a worrisome market with intentions to hold near-zero interest rates until 2024. As a result, the DIA and SPY surged off of intraday lows to ink new record highs. Despite his efforts, the 10-year treasury trades higher this morning, touching 1.74% as inflation worries linger. That said, the QQQ remains the worrisome index with significant overhead price resistance though it squeaked out a close above its 50-day average. The best we can do as traders is to stay with the trend and avoid becoming complacent.

Asian markets surged overnight after the dovish Fed comments, with the HIS leading the way up 1.28%. European markets trade mixed with the DAX up over 1% while the FTSE and CAC hover near the flat-line. With earnings and Jobless claims and those pesky rising bond rates, the U.S. futures have bounced off of overnight lows in the premarket pump yet still point to a mixed open.

Economic Calendar

Earnings Calendar

We have 90 companies on the Wednesday earnings calendar, but a good number of them are unverified reports. Notable reports include CAN, CSIQ, DXLG, DG, DLTH, FDX, NKE, OLLI, WOOF, SCHL, SIG, UTZ, & WB.

News & Technicals’

After the Fed’s dovish comments that expect to hold interest rates near zero until 2024, the DIA and SPY inked new record highs. Unfortunately, the 10-year Treasury yield continues to rise, reaching 1.74% as investors worry about inflation. The European central bank chimed in to echo the Fed, saying they will not react to short-term inflation increases. The IRS announced yesterday they would move the regular April 15th tax deadline to May 17th to help with the taxation changes. Just in time to take advantage of the stimulus payments, Apple is reportedly preparing to roll out high-end iPads ahead of its usual release cycle. According to reports, GOOG plans to spend $7 billion to construct new data centers and office space in 2121.

On the technical front, the trends in the DIA, SPY, and IWM remain in good condition after the modest selling that occurred ahead of the Fed announcement. Though the QQQ squeaked out a close above its 50-day average, it remains the weakest of the indexes faced with considerable overhead resistance. If big tech continues to struggle with the rising bond rates, it could be an interesting challenge for the indexes due to the heavy tech weighting. We may have to consider the possibility of longer-term overall market consolidation as investors weigh inflation worries against the exceedingly dovish Fed. With Jobless Claims numbers in focus, the U.S. futures point to a mixed open.

Jerome Powell has a difficult task today as he attempts to walk a tightrope of rising inflation concerns and economic recovery. The 10-year Treasury yields hitting new highs ahead of the announcement raises the stakes, and the entire world economy is watching. Congress will have its own balancing act to perform today in a hearing to deal with illegal border crossings that have hit record highs. Stay focused and flexible because anything is possible as we wait on the data.

Asian markets closed mixed but mostly lower in a choppy cautious session as they monitor the FOMC. European indexes also trade cautiously this morning, bounding around the flatline as they wait on the Fed decision. Ahead of a big day of data, U.S. futures appear to be treading water near the flatline ahead of earnings and potentially market-moving reports. Buckle up!

Economic Calendar

Earnings Calendar

We have 65 companies listed on the Wednesday earnings calendar, but a significant number of them are unconfirmed. Notable reports include AOUT, CTAS, FIVE, MLHR, LE, RIDE, OTCM, PDD, WSM, & ZTO.

News & Technicals’

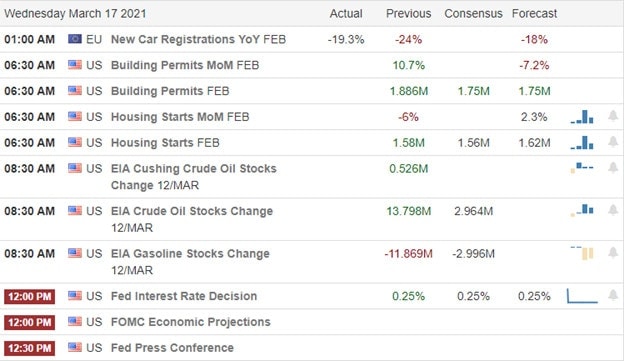

The pressure on Jerome Powell today as he attempts to walk a tightrope between Washington and Wall Street. The fireworks begin at 2 PM eastern with the FOMC statement followed by the press conference at 2:30. Treasury yields have hit a 13-month high this morning ahead of the Fed decision. Simultaneously, the pandemic is improving here in the U.S.; German cases are rising exponentially. A reminder that we may still have a long road ahead of us in the battle against Covid-19. Italy and France have decided to restart AstraZeneca vaccinations they recently stopped due to blood clotting concerns. There will be in hearing in Congress today as illegal border crossings hit record numbers. Democrats frame it as a minor problem while Republicans suggest it’s an all our crisis. It should be an exciting day of political pandering and soundbites.

Markets paused yesterday, somewhat holding their breath as we wait on the FOMC decision. Yesterday’s economic data was a bit disappointing, and today we get the latest reading on Housing Starts and the status of Petroleum reserves. Though potentially market-moving, all eyes will be on Jerome Powell’s tightrope walk later this afternoon. The DIA, SPY, and IWM indexes remain in good condition holding on to bullish trends. The QQQ is another matter leaving behind a concerning candle pattern at its 50-day moving average. What today’s follow-through price action on the tech sector could be of critical importance. With the 10-yields on the rise this morning, there is a lot at stake.

A choppy market session found sellers after the gap up open, but bulls ultimately won the day, climbing the wall of worry to set new records. However, futures trade missed this morning, facing the latest read on Retail Sales and the beginning of the 2-day FOMC meeting. As inflation concerns linger in the bond market, worries grow that the Fed could hint of interest higher rates in 2032. Should they do so, expect price volatility to follow as investors digest the future ramifications. Plan your risk carefully!

Overnight Asian markets rallied with modest gains across the board. European markets also trading in the green this morning, with VW surging 5.6%. U.S. futures have rallied off overnight lows but continue to suggest a flat, mixed open ahead of potentially market-moving economic reports. Fasten your seatbelts; the next couple of days could be an exciting ride.

Economic Calendar

Earnings Calendar

On the Tuesday earnings calendar, we now have more than 100 companies, but quite a few are not verified. Notable reports include COUP, CRWD, DBI, JILL, JBL, LEN, & VEL.

News & Technicals’

The market set new records in a choppy market session that seemed to struggle with momentum. Sweden and Latvia joined Germany, France, Italy, and Spain on Monday, stopping the administration of the AstraZeneca vaccine over blood clot fears. However, the company says there is no data that really justify these decisions and could have pandemic consequences. According to the U.S. solar industry, they posted record growth in 2020, adding 19.2 gigawatts of new capacity and an increase of 43% from last year. Solar installations are planned to quadruple by 2030.

As I write this report, the U.S. futures trade mixed with retail numbers and the beginning of the FOMC meeting in focus. Consensus estimates say retail numbers will decline rather sharply from the last reading, but they have set the expectation so low it may not be that hard to top the target. With bond rates moving up and worries about rising inflation, all eyes will be on the Fed announcement Wednesday afternoon. There is speculation that the committee could suggest rate increases by 2023. A long way off, but even a hint that higher rates are possible significant price volatility could be the result. Carefully consider your risk as you plan the path forward over the next couple of days. The NASDAQ is currently pricing in a gap up to test its 50-day average as resistance this morning. Will there be any bears ready to defend? Only time will tell.

New all-time highs as the indexes continue to extend with the smell of freshly printed money inspiring the bulls. In just 6-trading days, the Dow surged over 1900 points, and the party is not over yet, with the futures pointing to another gap up open. Stay with the trend, but I caution traders to avoid overtrading or becoming complacent. A pullback could begin at any time, and remember, a gap up to new highs brings with it the possibility of a pop and drop price pattern. Until then, enjoy the party!

Asian markets traded mixed but mostly higher overnight, and European markets advance with modest gains this morning. Ahead of an FOMC announcement Wednesday afternoon, expect price volatility to continues as the bulls push for more records at today’s open. Stay focused and flexible as we enter a busy week of earnings and economic data.

Economic Calendar

Earnings Calendar

On the Monday calendar, we have just short of 100 companies stepping up to report quarterly results. However, many of them are small-cap unverified reports. Notable reports include HQY, FENG,& VUZI.

News & Technicals

White House advisor Fauci is warning against lifting U.S. restrictions as Germany declares a 3rd wave of infections, and Italy prepares for an Easter lockdown with the infection rates rise. Ireland, Austria, and the Netherlands are the latest countries to suspend the AstraZeneca vaccine over blood clot concerns. According to the TSA, passenger screenings hit the highest levels in over a year as travel begins to recover. The 10-year treasury yield stubbornly holds above 1.6%, with an FOMC meeting just around the corner.

Indexes finished last week strong as new all-time high records continue on almost a daily basis. How long this bullish frenzy of buying can last is anyone’s guess, but chasing this rally could prove to be very dangerous as we extend. The current SP-500 P/E ratio is 80% above its 10-year average, and the 4-week new high/new low ratio continues to suggest an extremely overbought condition in the short-term. That said, the VIX continues to decline, closing above a 20 handle on Friday. The QQQ remains the problem child, still trading below its 50-day average with significant overhead resistance above. Ahead of the FOMC, treasuries continue to hold above 1.6% as inflation worries persist. Stay with the bullish trend but don’t become complacent because a rest or pullback could begin anytime.

In a prime-time address, President Biden says all adults should be able to receive at least one vaccination by the end of May and suggest things might get back to normal by the 4th of July. The market enjoyed a strong bullish run yesterday as investors celebrated the signing of the stimulus bill and the softening bond yields. Though we made the record books in the DIA, SPY, and IWM, the QQQ still has the overhead resistance of its 50-day average to overcome. Though we have a light day of earnings and economic reports, those pesky bond yields are creeping up with the 10-year back at 1.6%.

Overnight Asian markets closed mixed but mostly higher as the NIKKEI surged 1.73%. However, with bond yield climbing again, European indexes trade with modest losses across the board this morning. U.S. futures traded mixed coming off of overnight lows, trying to ignore bond yields and inspire more buying. This week experienced a fantastic bullish party extending the indexes, but one has to wonder if there is a nasty hangover just around the corner as bond yields creep higher. Plan carefully heading into the weekend.

Economic Calendar

Earnings Calendar

We have a lighter day on the Friday earnings calendar with just 31 companies stepping up to report. Notable reports include BKE, KIRK, & NOG.

News & Technicals’

In a prime-time address, President Biden will direct states to make all adults receive at least one vaccination by the end of May. Unfortunately, more countries have suspended the AstraZeneca vaccine due to rising issues of blood clots. The U.S. has not suspended its use so far. Although fear declined with successful 10 and 30-year bond auctions this week, the yeild is again topping 1.6% this morning. After signing the 1.9 Trillion bill, the White House says stimulus checks could start showing up in bank accounts as soon as this weekend assuming you use direct deposit. New York Governor Cuomo’s pressure continues to grow with calls for him to resign and an impeachment probe picking up steam.

Another day and more records highs for the indexes as the DIA, SPY & IWM bulls celebrate the next round of stimulus. The QQQ also enjoyed a nice rally with big tech finding buyers, but it still must deal with its 50-day average that may yet serve as overhead resistance. The VIX continues to weaken though tenaciously holding above a 20 handle. The four-week new high/new low ratio indicator signifies an extremely overbought short-term condition in the indexes, so be careful not to chase this late in the rally. With the bond rates popping back up this morning, it may be a good day to take some profits heading into the weekend.

The bulls lifted the Dow above 32,000 for the first time in history as the market celebrates the passage of one of the biggest spending bills of all time. Treasury yields also softened after a successful 10-bond auction sending industrial and consumer defensive stocks soaring as big tech continued to suffer. With more than 150 earings reports, Jobless Claims, JOLTS, and a 30-year bond auction ahead, the bulls push for another gap up open to keep the party going. Be careful not to chase such an extended rally because a significant pullback could begin at any time but until then, enjoy the ride!

Asian markets advanced overnight, led by the Hong Kong surging 1.65% at the close of the session. European markets traded mixed this morning as they chop cautiously around the flatline waiting for the next move of the ECB. U.S. Futures want the bullish party to continue pointing to a gap up open ahead of earnings and jobs data.

Economic Calendar

Earnings Calendar

As usual, Thursday is the busiest day of the week on the earnings calendar, with more than 150 companies reporting quarterly results. Notable reports include DOCU, LOCO, XONE, GCO, GOGO, GRDX, J.D., PRTY, PBPB, STNE, TTSH, TLYS, ULTA, MTN, WPM, & ZUMZ.

News & Technicals’

The passage of the stimulus bill lit a fire under the bulls pushing Dow above 32,000 for the first time in history. It is one of the biggest spending packages in history and the first legislative win for President Biden. Simultaneously, the President is under heavy pressure with more than 150,000 illegal border crossings in February, setting new records. The 10-year treasury yield softened slightly after a quick and successful auction yesterday afternoon. Today there will be a 30-year auction that to keep an eye on at 1 PM eastern. Denmark suspends using the AstraZeneca Covid vaccine after severe cases of blood clots reported in those vaccinated. President Biden will speak to the nation in a prime-time address on Thursday where he plans to announce the “next phase” of his pandemic response.

When it comes to the chart technicals, there is no question that bulls are large and in charge in the Dow, cementing new records prices. Although the NASDAQ has also enjoyed a nice relief rally, big tech continues to struggle with price resistance levels closing the day well below its 50-day average. Industrial and consumer defensive sectors continue to see substantial rallies as the massive rotation of the pandemic high flyers hits a fevered pitch. Be very cautious not to chase overextended stocks. With such a massive point rally in just a few days as a substantial pullback would not be out of the question and could begin at any time. Until then, enjoy the ride as the market celebrates the creation of deficit spending.

The bulls went back to work in the NASDAQ yesterday, lifting the index 3.69%, with the Dow briefly touching a new record high. However, the bulls still have a lot of ground to recover, with the QQQ, SPY, and IWM still challenged by overhead resistance. I think the big question the market has to grapple with is the bullishness of another 1.9 Trillion in stimulus and the possible bearishness that could create in interest rates and inflation. The success of the 10-year bond auction at 1 PM eastern today could be telling.

Asian markets closed mixed after a choppy session that saw selling into the close of the day. European markets seesaw this morning with modest gains and losses as the rally momentum seems to have faded. Ahead of earnings and a reading on the CPI, U.S. futures trade mixed in the premarket as inflation worries linger.

Economic Calendar

Earnings Calendar

On the Wednesday earnings calendar, we have just short of 100 companies fessing up to quarterly results. Notable reports include AMC, ASAN, BLDP, BBW, CPB, CLDR, EXPR, FOSL, FNV, LC, NGMS, SUMO, tup, UNFI, & VRA.

News & Technicals’

The bulls went back to work on Tuesday, pushing the Dow to a new high, but afternoon selling closed short of a record high close. The SPY and QQQ rallied sharply, testing resistance levels of price and downtrend, with big tech leading the gains. The U.S. House plans to pass the Senate revised stimulus bill today, and the President says he will sign it as soon as it hits his desk, adding 1.9 trillion in deficit spending. At 1:00 PM Eastern today, there will be a bond auction of the 10-year Treasuries. The last 10-year auction triggered a sharp rise in rates raising significant concerns of inflation. I may be wise to keep an eye on today’s auction if it energizes the bears for another attack. Representative Suzan DelBene is reintroducing a bill aimed at creating a national standard for digital privacy rights allowing states to build on the protections of the federal standard.

A look at the index charts, and it’s pretty easy to see the DIA is leading the way in printing a new record high before the profit-taking heading into the close. IWM is also in good condition though still challenged by some overhead resistance. Both the SPY and QQQ rallied sharply but still must address the downtrend as well as price resistance levels above. Keep in mind that that the QQQ remains the weakest of the indexes needing to recover more than 10 points to challenge its 50-day average as resistance. Before the bell, we will get the latest reading on CPI, and later today, it may be wise to keep an eye on the 10-year bond auction.