The North Korean summit abruptly ends with no deal and with the public Cohen political drama now behind closed doors the US Futures are suggesting only a modestly lower open. However, with more than 280 companies reporting and a busy economic calendar a lot could still change as we move toward this mornings bell.

Even though the bulls have given up a little ground the last couple days they still are in control of the uptrend and fought back yesterday cutting the initial losses in half by the close. The bears on the other hand continue to defend key resistance levels putting market between a rock and hard place and we will have to watch price closely for clues. Perhaps we slip into a healthy consolidation resting after such an extraordinary market run. If that’s the case, there will be some good trading for stock pickers as companies with price momentum can continue to elevate with relatively low volatility. That of course will change dramatically if the bears began to gain the upper hand. Stay focused and flexible.

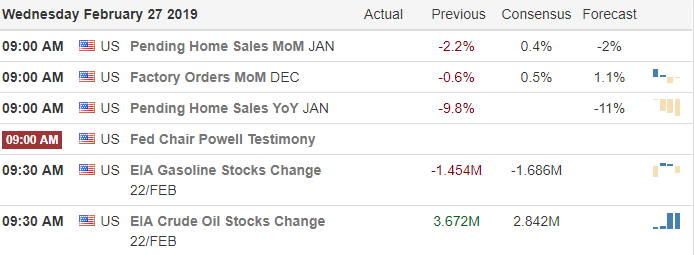

On the Calendar

We have a big day on the Earnings Calendar with more than

280 companies stepping up to report. Among

the notable earnings today are, DDD, ABB, ALRM, AMC, AMCX, BUD, ADSK, CARS,

CROX, ECA, GPS, EP, JCP, JD, KDP, LTC, MAIN, MAR, JWM, NRG, PRTY, SEAS, SPLK,

TC, VMW and WDAY.

Action Plan

After some initial selling the market became very choppy and

lethargic as the Cohen political drama which may be better described as a soap opera

played out at the US Capital. As near as

I could tell skimming through the highlights the only thing accomplished was

political grandstanding. The markets are

reacting lower this morning as due to the US/North Korean summit ends abruptly

with no deal. We also have India and Pakistan

exchanging air strikes as tensions between the two countries escalate.

Technically, the indexes continue to battle index resistance

levels and though the bulls gave up a little ground in the last couple trading

days they continue to fight hard to hold the current up trend. Asian markets closed lower and European are also

currently lower across the board this morning.

US Futures are pointing to a modestly lower open but with a big day of

earnings and economic reports anything is possible.

Futures are pointing to a modestly

lower open this morning as the market faces a day of historical events. First are

the decisions of nuclear disbarment of

North Korean a feat no sitting president has been able to accomplish.

Secondly a congressional hearing where the president’s former attorney is

expected to testify that is boss broke the law while

holding the highest office in the nation.

Add to that a big day of earnings reports and full economic calendar and

I think it’s safe to say the market has a lot a lot on its plate to digest.

The bulls have proven to be

very resilient and the trend is up so expect them to fight hard to defend against

any bear attack. However, we also have

to respect the price resistance in the index charts and plan for the

possibility that the political drama could impact the market with higher volatility. Saying that anything is possible would not be

an understatement and you never know exactly how the market could react with so

much to chew on today.

On the Calendar

On the Earnings Calendar we have a big day with more than

210 companies reporting quarterly results.

Some of the notable earnings are, AMT,

APA, BBY, BKNG, BOX, CPB, CHK, DF, FIT, TWNK,

HPQ, LB, LOW, ODP, PK, PBR, SQ, TDOC, TJX and WING.

Action Plan

As the US and North Korean

try to make nice while discussing nuclear disarmament abroad the president himself

will be under attack in a congressional hearing right here at home. Putting the president’s

challenges aside we should plan for the possibility of serious market impacts. As I write this morning note the futures are

pointing to only a modest decline at the open.

With a big day of earnings reports, important economic reports and a distracting

political drama anything is possible.

In our 11th week of rally and testing index price

resistance it would not be out of the question to see some profit-taking begin

or some price consolidation to reinforce a new level of support. However, the bulls have proven to be remarkably tenacious and with the market trend strongly

in their favor I would expect them to fight hard for higher prices. Avoid predicting, stay focused on price, remain

flexible, stay disciplined to your trading rules and prepare for a very interesting

day.

According to new reports the futures are down this morning because

investors are seeking clarity on the US / China trade deal. How can there be clarity when have been no

details and no deal has yet not yet finished?

Would it not be more likely that

the market is merely needing a rest after

the Dow has rallied nearly 4500 points in just over ten weeks? After an extraordinary run a rest or pullback is normal

and healthy price action to confirm or build price support.

The trend is still up and but there are warnings signs that

this run is a bit overextended. However,

at this time there are no clues of failure and the bulls have proven to be remarkably resilient

fending off bear attacks quite easily of late.

I would not expect them to give up easily now but stay focused on price action

clues waiting to see if the sellers show up in support or the morning gap down

or if buyers step in rejecting the low.

On the Calendar

On the Earnings Calendar we have over 200 companies reporting today. Among the most notable are, HD, M, BGS, BMO,

BNS, LNG, CSGP, CBRL, DISCA, ELF, EV, FTR, GWPH, HTZ, SJM, TREE, MELI, MYL,

PANW, PZZA, PSA, SDRL, SSTK, TIVO, VSI, and WTW.

Action Plan

If we are to believe the news

CNBC is citing that the futures are lower because investors want clarity on the US / China deal! Hmm, all along there has little to know

details and the fact is there has been no official deal as of now. Seems more likely

is down because simply because it needs a rest after Dow rally of nearly 4500 points! Nonetheless, Asian and European markets are lower this morning and it doesn’t

help the situation with HD missed on earnings early this morning.

The President is on his way to Vietnam to meet with Kim Jong-un

to discuss nuclear disarmament. Don’t be surprised if news reports from the

meeting create a little market volatility.

Keep an

eye on the Housing numbers this morning at 8:30 AM Eastern. Let’s hope

they show a better result than the

existing home sales numbers last week or the open today could be a little

rough. The trend is still up but there

are several danger signs so stay focused on price. There may be nothing at all to worry about but

let’s have the bull prove that before taking

additional long risk.

My curiousness about how the markets would open as we enter

the 11th week of this market rally disappeared after the Presidential

tweet energized the bulls. About 10 minutes before the futures market opened

it was reported that the President would delay the Chinese tariff increase. As you might expect Asian markets rallied strongly

on that news last night and the bullish spread to European markets which are higher across the board this morning.

Following a trip point gap and run on Friday the US futures

point to yet another gap of nearly 150 points this morning. Although global economic stories continue to populate the news the bulls

appear to have no concern and there is even

some speculation that new market record highs are on the way. Though the trend is up please keep in mind there

are clues that the market is overbought as we test resistance levels. That certainly

does not mean that selling will soon begin but it does suggest we need to be

watchful and prepared in case the bull

stumbles.

On the Calendar

On the Earnings Calendar we have 130 companies reporting earnings

today. Notable reports, TWOU, AWR, APLE, CLDT, ETSY, LSI, MOS, OKE, PBPB, APTS, RCII,

SHAK, THC & VCYT.

Action Plan

About 20 minutes before the Futures

markets reopened yesterday I was checking the news and wondered how the markets would respond after ten weeks of rally and closing in the Friday tariff increase. That curiosity

went away when about 10 minutes before the futures

open the President tweeted he would delay hiking the China tariffs and

referenced the negotiations as

productive. As you might imagine when the

Asian markets began to open 2 hours later

they made significant gains on the

news. European

markets are currently higher and the US futures are suggesting about a 150

point gap higher this morning.

As we enter the 11th

week of this amazing rally there is now speculation that the market will reach

out for new record highs in the near future.

Although it seems a fruitless endeavor I will once again point out the significant

resistance levels just above and suggest caution as we rally to test them. We have another big week of earnings this

week and several very important economic reports for the market to digest as

well.

After a choppy Thursday with the market reacting to declining home sales futures markets were quickly lifted out the overnight doldrums with news of a pending trade deal. The story was very lacking in details but the

possible end of this trade war was enough to inspire the bulls to push for more

than a triple point gap up. A positive

close today will cap an extraordinary 9th straight week of market

gains.

Overhead resistance is certainly

still a factor and though I feel the fear of missing out just like everyone else

I will stick to my discipline and avoid chasing so late in the rally. I will also plan to use this mornings gap up

to take some profits where possible and reduce my weekend risk. My job is to advance my account and this late

in such an extraordinary run a Friday morning gap up is a gift I plan to take

to the bank.

On the Calendar

On the Earnings Calendar we get a little break today with less

than 50 companies reporting. Notable earnings

include, AN, COG, CHK, MGA, RY, RUTH, WPC

and W.

Action Plan

Another news report that the US and China are getting closer

on a trade deal quickly lifted the futures

out of negative overnight territory. Although

the report contained no information on the details or timing the bulls are

pushing a triple-digit gap up open this morning. As I mentioned yesterday a strong finish to

week would not be surprising to cap off a nine-week rally of more than 4200 Dow

points.

Though gapping up the indexes

will still be challenged by the price resistance just above so be careful not

chase this morning. As normal I plan to use

a Friday morning gap as an opportunity to take some profits and reduce weekend risk

if at all possible. This week we have

seen the bull ignore falling retail sales numbers and yesterdays decline in

home sales but I don’t believe that can continue forever. Stay disciplined on the job of protecting

your capital and advancing your account.

Have a great weekend everyone.

The FOMC stands aside, the US and China are said to be

outlining a trade deal, index trends are up, and

the bulls point to the 9th straight day of gains. A truly extraordinary bull run that is also in

the 9th straight week up without looking back. Oddly enough bonds continue to trend higher

and even gold and silver have printed significant gains at the same time.

In a run such as this, profits have been easy to come by but its also very easy to become complacent. Such a strong bull run can lull traders to sleep and forgetting about the hungry bears lying in wait for their opportunity to attack. The trends are clearly bullish so stay with the trend but make sure you’re not chasing stocks late in their rally and over-trading. Respect resistance levels and exercise caution as price challenges them and remember to take some profits to the bank.

On the Calendar

On the Earnings Calendar we have a big day with more than

225 companies reporting results. Among the

notable report are: BIDU, BCS, BYD, CZR, ED, CUBE, DLPH, DPZ, DBX, FSLR, FLR,

HL, HPE, HRL, KHC, MORN, NEM, RMAX, STMP, STOR, VER, WEN, WIN & ZG.

Action Plan

Eight straight days of rally and in the 9th

straight week of an extraordinary index rally and the bulls appear energized

to continue that winning streak this morning.

New overnight that US and China may now be outlining the details of a trade

deal have the futures once again pointing to a modest gap up at the open. Asian markets closed mixed but modestly

higher overall and European are currently mixed this morning as well.

Today we have very busy earnings

and economic calendars to keep us on our toes as we progress toward the

open. Yesterday the FOMC minutes

yesterday reinforced that the committee expects to take a wait and see approach

giving them more time to evaluate the economic impacts of past rate increases. As expected there was some price volatility

after the minutes released but ultimately the bulls remained solidly in control

as we push upward to test significant market resistance levels. At this time there is nothing in price action

in the index charts to suggest bearishness but we must respect the resistance

above and avoid chasing so late in the rally.

The overall market trend is up and the bulls continue to maintain a remarkable amount of energy and tenacity to drive forward. However, with the index now in the ninth week up and drawing near major resistance levels it may be time to raise caution levels. Although the market seems convinced that there will be a positive outcome of the trade negotiations it’s possible we have already priced in that possibility. Which means any negative news coming out the negotiations or delay in the completion would receive a harsh reaction by the market.

On the Calendar

Recently we have seen bonds

going up with the market and yesterday gold and

silver joined in with a big burst of buying.

That’s an odd occurrence and makes me wonder what will decouple

first. With the Dow up over 4200 points

in nine weeks on its own should give everyone a little pause on it own. Remember to take some profits as stock and

indexes near resistance levels and be careful chasing new entries this late in

the rally.

On the Earnings Calendar we have nearly 190 companies reporting

earnings today. Some of the notable earnings

today are: WBA, FDX, A, ALB, CAR, SAM, CAKE, CDE, CYH, CVS, GRMN, GDDY, HFC,

IAG, JACK, NE, OC, PAAS, O, SO & RGR.

Action Plan

As the indexes move closer and closer to major resistance

levels I feel the need to become more and more cautious about adding new long

long positions. Though I’m cautious let me be very clear that

the trend

is still up and the bulls are still currently very much in control. I am also beginning to become concerned that

the market has already priced in a trade

deal with China. Which means if there is

any negative news or a delay in its completion the market could react harshly.

Today we have the release of the FOMC Minutes of the last

meeting. Don’t be surprised to see light and choppy price action leading up to its

release and some price volatility directly after. There is a news report out this morning suggesting

the market could be a bit more sensitive to the minutes given length and elevation fo the current rally. Futures are pointing to a modestly lower open this morning but with all

the earnings reports this morning that could easily change. As always stay focused on price and protect trading

gains and your capital as we move closer

and closer to resistance levels.

The US Futures are taking a little rest this morning as US/China

trade negotiations resume amid new

tensions here in America. Asian markets were

flat and mixed overnight while European markets slide south with banks leading the way. As a result US markets futures are currently pointing lower but there is still a

lot of morning earnings yet to come to influence today’s open.

Without question the index trends are still up and the bulls

at least to this point appear to have almost

limitless energy to drive higher. There

are clues that this run is overextended and profit taking could soon begin but

it would be unwise to fight a relentless bull run. Trying to predict a top is just as wrong as

trying to predict a market bottom. Eventually the bulls will rest and the price will pullback but wait for the clues and

follow them rather than predict. Having

said that I would be cautious about adding too many long positions this late in the rally.

On the Calendar

On the Earnings Calendar we have 159 companies reporting results

today. Among the most notable today,

WMT, AAP, NBL, LC, AWK, CTB, CXW, DVN, ECL, FE, GPC, HLF, HST, HSBC, KAR, LZB

& TSRH.

Action Plan

After a nice 3-day weekend the current futures look as if

they want to extend the vacation by taking a little rest this morning with a

modest pullback at the open. Don’t be too surprised

if the overall market is a little sluggish this morning as well with many

traders likely extending their vacation

as well. US/China trade negotiations resume today here in the US amid

new tensions. Expect some fast price

action if there are any news leaks from the negotiation

table.

Earnings continue to roll in by in large positive and although

we are seeing a little softness this morning the bulls are clearly in charge

and the trends are still up. According

to T2122 we are very overextended but

with indexes so close major resistance levels I would not be at all surprised

to see the markets continue to extend to test them. I see these resistance levels at the DIA 260 area,

SPY 281, QQQ 171 and IWM around 158.

After more than a month and a half bull run the bulls

continue to show resiliency fighting hard yesterday after a very disappointing retail sales report. Overnight future traded into the red as the Asian markets reacted to the possibility of a

slowing US Economy but this morning the futures have recovered pointing to

modest bullish open.

Take a look at the weekly index charts with our a single down candle since 12/28/18 with the Dow nearly 3700 points off the low and the SP-500 nearly 400 points higher. Truly an amazing rally that has provided traders with fantastic gains. Considering that as we head into the weekend be careful not chase entries this late into the rally and remember to take some profits.

On the Calendar

On the Earnings Calendar we get a little break today with

only about 50 companies fessing up to earnings results. Notable reports DE, MCD, NWL, PEP, RBS, YNDX.

Action Plan

After a disappointing Retail

Sales report and discovering that the

President is planning to declare a national emergency the market dipped

slightly to end the day. However, the

bulls fought back hard all day long choosing to ignore the data with amazing resiliency. Ironically

Asian markets traded lower across the board in response to a slowing US Economy

and overnight US Futures traded into the red.

Once again the bulls refuse to lose and this morning the as I write the morning note, futures markets are pointing to modest

gains at the open.

There is no doubt that the index trends are still up and although

they appear stretched and losing price momentum more upside is certainly possible driven by earnings results. As we head toward the weekend remember to take

some profits and evaluate the level of risk you will hold through the weekend. We have had an

incredible month and a half bull run providing great profits, don’t give it back

by chasing entries so late in the rally.

Have a great weekend everyone!

I find the hyper-confidence currently displayed by the US markets a bit puzzling this morning especially with president reportedly considering a 60-day extension of the tariff deadline. Nonetheless the bulls are in full on beast mode this morning ahead a huge day of earnings reports and government shutdown delayed retail sales numbers.

Asian markets were subdued overnight as trade negations are

scheduled to continue into Friday. However, European markets are higher amid earnings

result and the US Futures currently indicate another gap up open. There is not a clue in the price action suggest

bearishness but this late in the rally I must admit concern about adding new long

risk with the indexes so extended. Enjoy

the ride and hold on tight and let’s hope the negotiations progress as positively

as the market is pricing everything.

On the Calendar

On the Earnings Calendar we have more than 220 companies

reporting earnings today. Watch for

notable reports from NVDA, CM, CGC, AMAT, ARCH, ANET, AZN, AVP, BLMN, CBS, CC,

CME, KO, CS, DUK, GEO, IRM, SIX, WM &

ZTS.

Action Plan

We have another interesting day ahead of us and I have to be

honest the hyper-confidence of the US

Market has me nervous and a bit

puzzled. First, reports are now questioning

whether or not the President will sign

the compromise bill which would avoid the Friday night government shutdown. I find that difficult to believe but if true I’m

confident the market will react negatively if that were to occur. Secondly, the market seems to believe a Chain

trade deal is imminent but the president reportedly is considering a 60 extension of the

deadline.

Would that not suggest negotiations

are not going that well and how is dragging this threat out another 60 days reason

to gap the market higher this morning? Things that make me say Hmmm? Asian markets were very subdued overnight but

European markets and US Future are still

determined to run higher. Remember we

have a big day of earnings and Retail Sales numbers that may move the market

around before the open.