Last nights CNBC headline that reads, “US and China are reportedly drawing closer to a final agreement” lifted markets around the world with the hope a deal is forthcoming. Although the article goes on to say both countries still have to agree on a number of important issues the bulls grabbed a hold of that headline and ran. As a result, the US Futures point to a gap up open that indicate the SPY and the QQQ will open above key resistance levels assuming the bullish sentiment holds throughout the morning.

Once again assuming the bulls have the energy to hold this

new price level of support it opens the door for the market to test all-time market highs in the near future. Of course we still have to be watchful of a

pop and drop pattern if buyers fail to support the morning gap so be careful

not to chase. Remember we have the big employment

number coming Friday morning and it’s not unusual for the market to become

light and choppy as we wait.

On the Calendar

We have fewer than 30 companies reporting earing today as

the first quarter reports continue. Among the most notable are CALM, DGLY & KODK.

Action Plan

Shortly after the Asian markets open CNBC reported that the

US and China are drawing closer to a final trade agreement. Then went on to say, “Both countries have yet

to agree on a number of important issues.” None the less the Asian markets responded

bullishly to the headline closing higher across the board. Currently European

markets are mixed but mostly higher with the FTSE just slightly in the

red.

Consequently the US

futures are bullish across the board with the Dow indicating a gap up of 100

points or more as I write this report.

At the close yesterday the indexes all faced a challenging price

resistance level but as of right now both the SPY and QQQ indicate they will

gap through resistance at the open. That

certainly opens the door for a possible

new record market highs in the near future

assuming the bulls can hold above resistance.

Of course we must still watch for the possibility of a pop and drop pattern developing if buyers

fail to support the morning gap this morning.

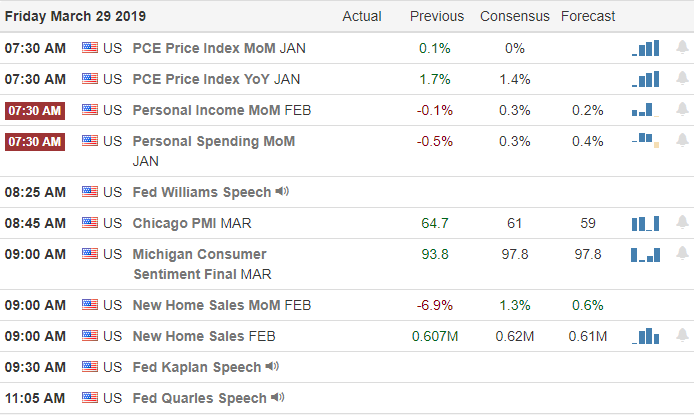

Remember we have the big Employment Situation number coming Friday

morning and it’s not uncommon for the price

action to become light and choppy as we wait.

The first trading day of the second quarter the bulls put on

a display of power charging through price resistance and breaking the last

weeks chop zone. Unfortunately, the bulls

stopped just short of the next price resistance hurdle in all four of the major

indexes. It would be completely rational to think the momentum of yesterday bullishness would be enough to carry the index’s over this price barrier. However, it’s also quite rational to think a little pause to take a breath or even some profit-taking

might be in order.

With the DIA and SPY finally

making a new high we technically in a much better position, assuming the bulls

can hold this newly attained elevation. The

QQQ stopped short of a new high yesterday closing at price resistance while the

IWM continues to languish in a downtrend.

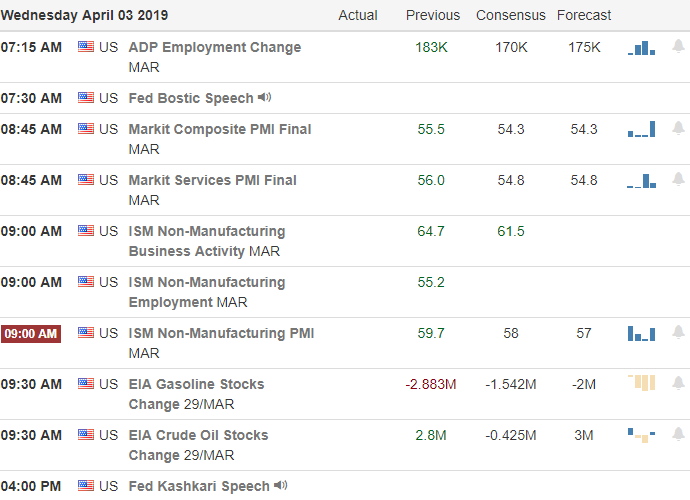

Futures are currently flat this morning but keep an eye on the Durable

Good Orders report at 8:30 AM Eastern as it could set the tone for the day.

On the Calendar

We have a significant

decline in earnings reports today with just

over 20 companies. Notable earnings include

GME, PLAY, NG & WBA.

Action Plan

After huge bullish one day rally where the Dow gained a

whopping 329 points the futures indicate a more subdued open this morning. As a matter of

fact, US Futures trading in the red

all night and have only begun to see positive prints in the pre-market

pump. Asian markets finish their trading

day mixed but mostly higher overnight. European

markets are bullish across the board this morning after reporting stronger than

expected factory activity overshadowing

another failed Brexit vote. Unless they

can come to an agreement in the coming

days the 5th largest economy will leave the bloc on April 12 with no

deal.

Although yesterday was a great day for the market finally

breaking a week-long chop zone the

indexes charts find themselves with yet another price resistance hurdle just above. Perhaps the sheer

momentum of yesterday’s bullishness is

enough to propel the indexes over the hurdle but

we shouldn’t expect the bear to give up easily.

After such a big one day move it would not be at all surprising to see a

little profit-taking to test overnight futures lows or pause the action to take

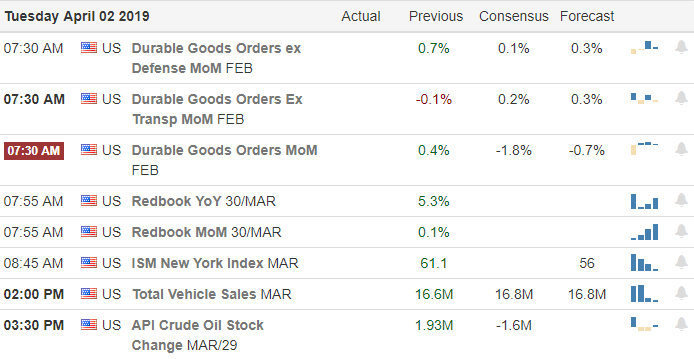

a breath. The Durable Goods Orders at

8:30 AM could set the tone for the day but the consensus estimate is expecting

a decline in this potential market-moving number.

Futures opened trading very bullish last night on optimism as the US/China trade negotiations resume in Washington DC today. The good vibes were significantly enhanced during the night when better than expected Chinese

manufacturing data came to light. Not surprisingly, Asian markets closed

sharply higher last night and European markets are strongly bullish this

morning ahead of yet another Brexit vote.

Perhaps this is the bullish shot in the arm we have been waiting for to provide the momentum required to break through the index price resistance that has proved so stubborn over the last few weeks. Keep in mind, we still have a full plate of economic and earnings data for the market to digest this morning that could either enhance or subdue how the market open. Be careful to avoid chasing the morning open with the fear of missing out. Watch and wait for price action to prove buyers will step in to support the gap. Remember gaping into price resistance can produce those nasty pop and drop patterns so it’s wise to exercise a little patience this morning.

On the Calendar

We have 164 companies reporting on the first day of the 2nd

quarter. Among the notable reports CALM,

DGLY & KODK.

Action Plan

Stronger than expected Chinese

manufacturing data and optimism as the US and China resume trade negotiations today

in Washington DC has futures signaling a substantial morning gap up open today. Asian markets closed bullish across the board

last night and European markets are also sharply higher this morning ahead of another

Brexit vote. We also have a busy

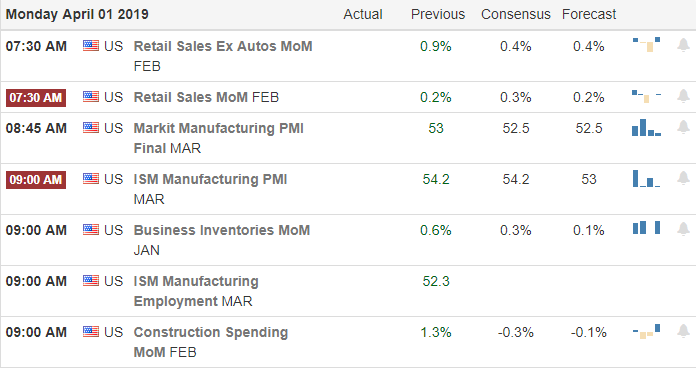

Economic Calendar this morning Retail Sales, PMI Manufacturing, Business

Inventories, ISM Mfg. Index and Construction Spending for the market to digest.

As I write this the Dow futures

indicate a gap of more than 175 points but at one point it was more than 200

points. If this bullishness holds, index

charts will be gapping above some price resistance levels or will be very near

then at the open. Keep an eye on the US points

this morning that has the possibility of enhancing or subduing the bullishness. Technically this could be the burst fo bullish

momentum to finally breakthrough the resistance above that has proved to be

such a stubborn obstacle for the last few weeks. With that said be careful not to chase the

gap up open. Let’s wait to see if the buyers

support the gap because the last thing we would want to see is a pop and drop

pattern.

US/China trade optimism inspired Asian markets to close

higher and currently European markets are

also feeling bullish ahead of another Brexit vote later this morning. As a result, the US Futures are very happy

this morning suggesting a 100 point gap up in the Dow at the open. As great as that sounds be careful chasing the morning gap because of the significant

resistance levels just above. Let’s wait

and is if buyers step in after the open supporting

this gap.

If you have yet to take some profits this week, remember

gaps are gifts and this morning may be a perfect

time to reduce risk by taking some

profits to the bank. Be careful not to over-trade as the market tests

resistance and keep in mind the bear are unlikely to give up easily. However, the hopefulness of a US/China trade deal may be just enough to

inspire the bulls to keep climbing. Stay

focused on price action and give consideration

to the risk you carry into the weekend.

On the Calendar

On the last trading day of the first quarter we still have

we still have companies more than 60 companies reporting. A good thing because 2nd quarter earnings season

will kick off in about three weeks.

Among those reporting BB and KMX are notable.

Action Plan

As US/China trade negotiators

gave the markets a lift overnight stating the talks were productive but stopped short of providing any

details. Asian markets closed higher across

the board on the trader optimism. European markets are also higher across the board

and later this morning the UK will once again vote on a Brexit plan that would

have them leaving the EU by mid-May.

That of course could create a market reaction and currencies may see some fluctuation in reaction.

Currently US Futures

are also suggesting a bullish open today

but except the QQQ the indexes still have

significant resistance levels above. The bulls and bears have been pretty equally matched

all week leaving behind indecisive candle patterns. Perhaps the positive comments on the trade negotiations

is enough to inspire the bulls but they will need some significant momentum to

break the bearish resistance levels above.

Remember not to chase a morning gap into price resistance. Wait and see if buyers step in supporting the

gap. Have a great weekend everyone.

Rumors of a US/China negotiations

breakthrough, declining 10-year Treasury yields and busy earnings and economic calendars the

market has a full plate this morning. The

question is will it be a satisfying meal or will it cause indigestion? On the Economic Calendar the GDP according to

consensus is expected to decline and Jobless Claims rise slightly at 8:30 AM

Eastern. One has to wonder if that could

fuel growth concerns or if the numbers will come in better than expected to

reduce those concerns.

The technical s of the index charts don’t provide much in the way of clarity either. The QQQ remains the market leader holding on to a nice uptrend while the DIA and IWM struggle with resistance in a modest downtrend. The SPY appears to want to break the tie but continues to hover just above support and below resistance with indecisive price action. I think it’s safe to say anything is possible so plan accordingly.

On the Calendar

We have nearly 120 companies reporting earnings on the

calendar today. Notable reports include,

ACN & QIWI.

Action Plan

Futures were looking lower last night as Asian markets reacted negatively to the declining

10-year treasury yield. However, with

the rumor of a US/China breakthrough in the

trade negotiations European markets are up across the board and the US Futures have

responded bullishly bouncing off their overnight lows. As I write this Futures point to a flat open

but with nearly 120 companies reporting earnings and a full economic calendar

it’s anyone’s guess how we open trading today.

The consensus is suggesting a decline in the GDP number and a

slight increase in Jobless Claims 8:30 AM Eastern. It will be interesting to see if these two

reports will add to or take away from the economic slowdown concerns. The DIA

and the IWM are still in technical down-trends

under significant resistance levels even after the nice recovery off of

yesterdays lows. The SPY continues to

hover between support and resistance and the

QQQ remains the strongest of the indexes holding on to its uptrend. With so many

factors pushing and pulling the market

today anything is possible.

While the market keeps

a close eye on possible interest rate inversion and possible economic slowdown

the US Futures point to a bullish open and a welcome relief to last Friday’s

selloff. Currently the Dow futures point

to more than a 100 point gap up as I write this but still has to clear the

Housing Starts hurdle at 8:30 AM Eastern. A miss of consensus estimates could fuel the fire of economic slowdown while a beat

could clear the way for a bullish morning gap.

As nice a relief rally may be please remember it will take a

huge effort by the bulls to clear the technical damage created in last Friday’s

selloff. The DIA and IWM still the lower

high and are technically in a downtrend.

The SPY while technically stronger

still has significant resistance to deal

with while the QQQ continues to enjoy the

benefits of market leadership. Be careful

not to get caught up in fear of missing

out and chasing into positions as the market tests

price resistance.

On the Calendar

We have just under 60 companies reporting quarterly earnings today.

Notable reports today include CRON, OLLI, CCL FDS, INFO, KBH, MKC &

VALE.

Action Plan

After a very indecisive price action day the DIA finished up

a whopping $0.11, SPY down $0.21, QQQ down $0.31 and IWM up $0.66 we have a

substantial change of attitude this morning.

First Asian markets closed mixed but the NIKKEI and HIS posted solid gains lifting the US Futures. The good vibes continue this morning with European markets bullish across the board with

modest gains. As I write this Dow futures

suggest a gap up of more than 100 points but we still have some economic hurdles to cross before the open.

Besides some notable earnings the 8:30 AM Housing Starts

number will be important this morning amidst

the worries of an economic slowdown. Consensus estimates of 1.213 million units which is just slightly less than the

previous reading. Although a gap up will

be a nice relief remember we still have substantial

technical issues to overcome particularly

in the DIA and IWM so we must still keep a close eye on price resistance levels

above. However, the QQQ is still technically

sound holding higher lows and continues as the market leader at the moment.

If the US futures are any indication

of the day we have ahead we should expect price action to become a bit more

volatile and challenging and the 21% one day

rally in VIX seems to confirm that possibility.

During the night the Dow futures were up more than 100 points shortly

after the open but reversed sharply and traded more than 120 points lower as

Asian markets fell sharply due to global growth concerns.

Technically both the DIA and

the IWM have confirmed lower high failures at price resistance. Although Friday’s price action raises major

concerns for the SPY the pullback in QQQ is only a test of support and the

overall uptrend at this point. Currently

the US futures are only pointing to a modestly lower open but we should expect an

extra dose of price volatility so plan your risk carefully.

On the Calendar

On the Earnings Calendar we have over 70 companies reporting

earnings today. Among the notable reports RHT 7 WGO.

Action Plan

After 2-years of investigation it would seem the Mueller findings have cleared the President of the collusion with Russia. The Attorney General also says the report did

not find enough evidence to charge the president with obstruction of

justice. Now one would think that mess is finally behind us but I would bet money

that’s it’s far from over and will become

a never-ending story in the political

spin cycle. Rockets fired into Israel

will cut the Netanyahu visit to the US short and raises concerns of a violent escalation

in the area.

Futures have been a roller-coaster

ride overnight. First the Dow futures rallied more than 100 points after the AG cleared the

president. Then Asian markets opened and

fell sharply with the Dow futures reversing and dropping more than 120

points. European

markets are modestly lower across the board but the early morning pump has the

US futures suggesting only a modestly lower

open as I write this. I will not be at all surprised if both the overnight

high and low get tested at some point during the day.

Remember Friday’s sharp escalation in VIX suggests a bit more volatility

price action is not out of the question so plan your risk accordingly.

Global Growth concerns once again raise its ugly head after European data disappoints just one day after a broad-based market

rally. I must admit I was hoping for a

little follow through to the upside this morning but the futures are currently pointing to a gap down open across all

indexes. Overall it has been a great

week of gains in the QQQ & SPY and some profit-taking as we head into the weekend

should not be that surprising.

Although yesterdays strong

rally may have felt as if the all-clear sounded, however, a quick look at the index

charts shows us that price resistance above is still at work. The DIA

and IWM are particularly problematic with the lower high still in force even

after such a bullish move Thursday. Keep

that in mind as you plan your risk heading into the weekend.

On the Calendar

We have a light day on the Earnings Calendar with less than 40 companies reporting. Notable earnings DXLG, HIBB, JKS & TIF.

Action Plan

After such a big rally on Thursday that was very broad-based I was hoping for a little more

upside this morning. However, the market

has different plans after some disappointing European

data once again raises concerns of a global

economic slowdown. Asian markets managed

an ever so slightly bullish close across the board but this morning European markets are all seeing red.

US Futures that have been out of sync of late have linked

back up and currently indicate a lower open today. The recently

problematic Existing Home Sales out at 10 AM Eastern could belay some slow down

concerns if the number comes in showing an increase as the consensus is

expecting. Of course if it misses the exact

opposite may be true adding to the slow

down concerns this morning. All and all

it has been a fantastic week of gains and there is nothing wrong with a little

profit-taking as we head into the weekend.

The FOMC signals no rate increases for the rest of the year

but the market seems very unimpressed by the action. While the market has been trying to ignore the

clues of an economic slowdown the Fed appear to have taken a no-confidence vote in its strength. Financials quickly reacted negatively to the news and are looking slightly

lower this morning.

Asian and European

market responded mostly higher on the

news but the US Futures currently show mixed

reviews. The Dow indicates a slightly

lower open while the NASDAQ is suggesting slightly higher. Technically speaking the SPY and the QQQ are

in very good shape but the Dow and the IWM having printed lower highs at

resistance there is reason for a little caution. Also keep an eye on the VIX that once again

quietly crept up yesterday. If that

continues it could trigger a little profit-taking as we head toward the

weekend.

On the Calendar

We have nearly 100 companies reporting earnings today with

the most notable being, NKE, CSIQ, CTAS, CEO, CAG, DRI, LE, PTR & TCEHY.

Action Plan

The market seems quite

unimpressed by the FOMC decision to avoid raising interest rates for the rest

of the year. Normally low rates would

inspire the market but in this case the FOMC appears not so confident in the overall economy. During the night the Dow Futures were down

about 100 points even though Asian and European

markets responded marginally higher. As I write

this futures have rallied in the pre-market pump but it would not surprise me to the

overnight lows tested sometime today.

The QQQ remains very strong, the SPY is holding firm in consolidation but the DIA and IWM continue

to signal a little caution due to their lower high prints. All indexes continue to have resistance challenges

above making the path forward difficult to determine. The VIX edged higher again yesterday

suggesting a little fear might be creeping

in which could lead to some profit-taking if that were to continue as we head toward the weekend.