The wild daily price swings continue as the bulls rush in to buy after the big morning gap lower, and this morning, it looks like we’re in for more overnight reversals and whipsaws. Home depot numbers point to a weakening consumer, making for dangerous conditions with the market trying to ignore the higher-than-expected inflation. But, of course, with emotions so high, perhaps the pending WMT report will patch up the overnight sentiment whipsawing us again. In addition, PMI, Existing Home Sales, and a slew of earnings reports will likely keep price action challenging.

Asian markets traded mixed overnight, reacting to factory activity as Putin ups his dangerous rhetoric as the war enters its 2nd year on the 24th of this month. As Credit Suisse continues to decline, with likely more Fed rate increases on the way, European markets began the day selling after recently notching record highs. With a big day of earnings reports with clues to consumer strength, PMI, and Housing data on tap, plan for more gaps and whipsaws.

Economic Calendar

Earnings Calendar

We kick off this holiday-shortened trading week with a hectic earnings calendar. Notable reports for Tuesday include ARNC, BCRX, CZR, CHK, COIN, CBRL, FANG, ELAN, ESPR, EXPD, FLR, TWNK, HD, HUN, IR, KAR, KEYS, KTOS, LZB, LPX, MDT, MELI, TAP, PANW, PSA, O, SBAC, SKT, TOL, WMT, RIG, & ZIP.

News & Technicals’

Home Depot reported its fiscal fourth-quarter earnings before the bell. The home improvement retailer was a clear pandemic winner and has remained resilient despite inflation and consumer habits shifting. Home Depot said it would spend an additional $1 billion to raise hourly employees’ wages. The home improvement retailer is the latest to signal that the labor market is still tight. Walmart, the nation’s largest private employer, recently announced raising its minimum wage to $14 an hour for store employees.

Walmart will report its earnings before the bell. The big-box retailer will likely share its outlook for the year ahead. Investors and economists are eager for clues about the health of the American consumer as inflation remains high.

Western nations and Ukraine have repeatedly rejected Putin’s narrative. However, the U.S. administration on Saturday formally concluded that Moscow had committed “crimes against humanity” during its year-long invasion of its neighbor. Feb. 24 will mark one year since Russia mounted a large-scale invasion of Ukraine, beginning a ground war in Europe that Putin still calls a “special military operation.”

The wild daily price swings continued on Friday with a substantial gap down open, but the bulls quickly rushed in to buy the lows on relatively low volume as VIX registered declining fear. Unfortunately, as I write this report, futures suggest yet another pre-market reversal as disappointing HD earnings hint at a weakening consumer amid higher-than-expected inflation reports. With the DOW consolidating rage expanding to 800 points, nearly daily overnight reversals, and huge point intraday whipsaws, there is little to no edge to be had for the average retail traders. This wild price action is a paradise for the quick in and out day trader but be warned because such times can end swiftly and painfully if the euphoric bullish assumptions suddenly shift. With a big week of earnings and potential market-moving economic reports, expect more of the same in the days ahead.

On Friday, markets gapped lower at the open (down 0.54% on the SPY, down 0.49% on the DIA, and down 0.75% in the QQQ), following through on Thursday afternoon’s selloff. From there, all three major indices bobbed sideways below the open until about 2:15 pm. At that point, a late-day rally saw the DIA cross the gap and turn green while the SPY and QQQ rallied back up above the open (into the gap) with all three going out near their highs. This action gave us a gap-down Doji in the QQQ, a gap-down, white-bodied Hammer in the SPY, and a gap-down, white-bodied candle with a small lower wick in the DIA. All three indices closed below their T-lines and the DIA retested and closed above its 50sma.

On the day, five of the 10 sectors were in the red as Energy (-2.97%) led the way lower and Communications Services (+1.12%) held up better than the other sectors. At the same time, the SPY was down 0.24%, the DIA was up 0.25%, and QQQ was down 0.71%. The VXX was flat at 11.67 and T2122 fell a bit more in the midrange to 44.71. 10-year bond yields fell significantly to 3.817% and Oil (WTI) is down 2.76% to $76.32 per barrel. So, on the day, we’ve seen a gap lower met with volatile indecision. This resolved into a bearish push to end the day. Again, this all happened on slightly less-than-average volume.

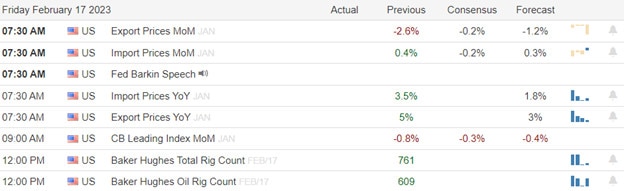

In economic news Friday, the January Export Price Index came in far higher than expected at +0.8% (compared to a forecast of -0.2% and the December reading of -3.2%). Meanwhile, the January Import Price Index came in just as expected at -0.2% (versus a forecast of -0.2% and a December value of -0.1%). Together, these indicate that the US was passing inflated prices on the rest of the world, while the price of our imported goods fell slightly. Elsewhere, two Fed speakers made headlines Friday. Fed Governor Bowman said “I think there’s a long way to go before we reach our 2% inflation objective and I think we’ll have to continue to raise the federal funds rate until we see a lot more progress on that,” while addressing bankers in Nashville. She also said, “We were seeing some progress in lowering inflation at the end of last year, but some of the data that we’re seeing early this year is not tracking with consistently lowering inflation in a way that I would like to see.” In a separate event, Richmond Fed President Barkin said the Fed still needs to raise interest rates higher but noted that he prefers to stick with slower, quarter-percent hikes. Barkin said, “I am not taking as much signal from the data that we’ve gotten recently on the demand side as you might if you start to see it for multiple months”.

In stock news, Reuters reported Friday that MSFT is already in talks with ad agencies on how it plans to incorporate paid links (ads) in the AI responses generated by the new ChatGPT-enabled Bing (which is already in beta release). Unnamed sources said that in addition, the AI-generated results will be more prominent (above) traditional search ads. Then after the close, the US Navy awarded LMT a $2 billion contract for hypersonic missile systems. Meanwhile, after hours a report circulated saying that TSLA is now considering buying metals (lithium) miner SGML. (SGML spiked in after-hours trade.) Over the weekend, META took a page out of the Twitter playbook and launched new subscription services for Instagram and FaceBook where a user buys a blue badge to mark them as “verified.” META is charging more than Twitter has (so far) for their badge at $12 on web and $15 on mobile (compared to Twitter’s $8 and $11 respectively). In addition to the supposed prestige of having the badge, META is promising greater “visibility and reach” for verified user’s posts, suggesting that their algorithm will treat verified users similar to ad buyers (promoting their posts over those from second-class users). Elsewhere, over the weekend Fortune reported that an online retailer named Temu (owned by US-listed Chinese online retailer PDD) has become the most downloaded shopping app in the US. During Q4, the Temu app was installed more than AMZN, WMT, TGT, or any other shopping app. Finally, UNP said on Monday that it has reached an agreement with two unions and will begin providing 2,100 of its workers with up to four paid sick days per year.

In stock legal and regulatory news, BDX convinced a US appeals court to reinstate three patents related to its medical injection device (Powerport). Elsewhere, the FDA granted accelerated approval to TVTX for their kidney disease drug IgAN. At the same time, the FDA also approved the APLS drug Syfovre (and macular degeneration drug). Meanwhile, a group of US Senators and Congressmen asked that the Surface Transportation Board delay a decision on a proposed merger of CP with KSU until after a Chicago-region impact assessment has been completed. On Saturday, Reuters reported that US Treasury Dept. sanctions authority has begun an investigation of US-listed, Austrian bank RAIFF over its business related to Russia and whether it is being used to skirt sanctions. Later on Saturday, the FDA announced that PEP is recalling 300,000 bottles of SBUX chilled Frappuccino drinks after glass chips were found in some bottles. On Sunday, the NHTSA added another deadly crash to its TSLA probe after a vehicle slammed into a fire truck on a California interstate Saturday, killing the driver, apparently while using the TSLA “Full Self-Driving” feature. Finally, the US Supreme Court will hear oral arguments today in a case that challenges social media and the Internet as we know it. The case will determine whether websites and social media companies are liable for everything posted (by the public) on their sites. META and GOOGL are the most obviously impacted. However, every website will be affected by the ruling on this difficult subject.

In energy news, Friday was another down day (and week) for Natural Gas. The March front-month Natty contract closed down 4.8% to $2.2750/mmBtu after hitting a 2.5-year low earlier in the session. With the sole exception of the prior week, the Natty has closed lower every week since the beginning of December. It has lost more than 65% in the process. Meanwhile, Oil (WTI) also ended Friday down 4.2% on the week. Oil analysts say that “rate hike jitters” have returned with vengeance. In addition, the oil traders are now also fearing the legally-mandated sale of 26 million more barrels of oil from the US Strategic Reserve hitting the market in the coming weeks/months. Finally, Bloomberg reported Friday that a record 311 mid-range tanker ships have recently been seen sailing without cargo or listed destination near Russia. (This is compared to an average of 14 such ships at any given time in the prior year.) The shift implies a new “shadow fleet” has been formed to help Russia avoid sanctions and keep shipping hundreds of thousands of barrels of diesel and gasoline per day. In addition, the removal of those ships from the global market has caused the cost of fuel tankers to skyrocket for regular routes such as those feeding Europe and the US East Coast.

Overnight, Asian markets were mixed on mostly modest moves. Hong Kong (-1.71%), Thailand (+0.66%), and Shanghai (+0.49%) were the exception to that rule with all other exchanges in the region moving only fractionally in either direction. In Europe, we see the bourses leaning to the red side at midday. The FTSE (-0.20%), DAX (-0.43%), and CAC (-0.35%) lead the region lower in early afternoon trade. However, Russia (+1.51%) is an outlier as they responded to President Biden’s surprise visit to Ukraine by dropping out of a nuclear arms treaty and vowing to keep pushing in their war of conquest against Ukraine. As of 7:30 am, US Futures are pointing to a gap lower to start the day. The DIA implies a -0.89% open, the SPY is implying a -0.84% open, and the QQQ implies a -1.08% open at this hour. At the same time, 10-year bond yields are spiking again to 3.882% and Oil (WTI) is up just under 1% to $77.06/barrel.

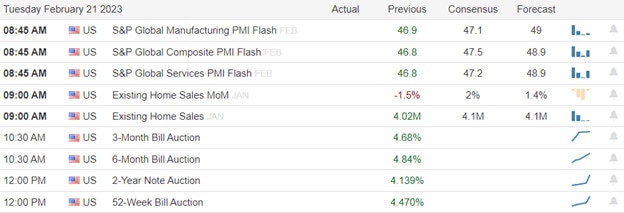

The major economic news events scheduled for Tuesday are limited to Mfg. PMI, S&P Global PMI, and Services PMI (all three at 9:45 am), and January Existing Home Sales (10 am). The major earnings reports scheduled for the day include ARNC, CEQP, DAN, ELAN, EXPD, FLR, HD, HUN, IR, JBT, JELD, LGIH, LECO, LPX, MDT, MIDD, TAP, NMM, PEG, TECK, TPH, TRN, WMT, WLK, and WLKP before the opening bell. Then after the close, ALIT, AGR, BXC, BCC, CZR, CWH, CHK, COIN, CSGP, CW, CVI, FANG, ESI, EQX, EXAS, FLS, GFL, IAA, IOSP, KEYS, LZB, MTDR, PANW, PSA, O, SBAC, TOL, RIG, UNVR, and WSC report.

In economic news later this week, on Wednesday the FOMC Minutes are released, the API Weekly Crude Oil Stock Report and Fed member Williams speaks. On Thursday, we get Q4 GSP, Q4 GDP Price Index, Weekly Initial Jobless Claims, and EIA Crude Oil Inventories. Finally, on Friday, the January PCE Price Index, January Personal Spending, Michigan Consumer Sentiment, and January New Home Sales are reported.

In terms of earnings later in the week, on Wednesday, we hear from ALLE, BIDU, BLCO, BCO, CRL, CSTM, CRVN, GRMN, GIL, IBP, IQ, NI, OSTK, PRG, SBGI, TRGP, TJX, TNL, UTHR, VRT, WWW, ATUS, ANSS, APA, BTG, CPE, CAKE, CHRD, CDE, FIX, CTRA, CCRN, DVA, EBAY, ETSY, EXR, GSM, FNF, ICLR, LBTYA, VAC, DOOR, MATV, MOS, MYRG, NTAP, NVDA, OPAD, OGS, OUT, PAGS, PARR, PK, PDCE, PXD, PR, RXT, RIO, RYI, SNBR, SM, STN, SUI, RUN, TDOC, VMI, and WES. Then Thursday, BABA, AMR, AEP, AMT, HOUS, AMBP, AAWW, BBWI, BHC, CBRE, CQP, LNG, COMM, DPZ, DTE, EME, AG, FCN, GPC, GFI, IRM, KDP, LKQ, MRNA, MODV, NTES, NEM, NICE, NOMD, OPCH, PZZA, PCG, PRMW, PWR, RCII, SPTN, SRCL, FTI, TFX, BLD, TAC, VIPS, W, YETI, ACCO, ATSG, ACA, ADSK, BALY, BECN, SQ, BKNG, BWXT, CVNA, CE, CGAU, CENX, CHE, CWK, EIX, ERIE, FTCH, FND, INTU, LYV, MTZ, MELI, OII, ZEUS, OPEN, PBA, PRI, RHP, SEM, SWN, VICI, WBD, and INT report. Finally, on Friday, we hear from CM, GTLS, CNK, EOG, EVRG, FMX, FYBR, GTN, DINO, IEP, LAMR, and CRC.

So far this morning, WMT, MDT, TAP, DDS, IR, JELD, TPH, ELAN, and MIDD have all reported beats on both the revenue and earnings lines. Meanwhile, HD, ARNC, CEQP, LPX, and JBT have all reported misses on the revenue line while beating on the earnings line. On the other side, HUN and DAN both beat on revenue while missing on the earnings line. Unfortunately, WLK, FLR, and LGIH missed on both the top and bottom lines. It is worth noting that MDT raised forward guidance, However, WMT, HD, TAP, DAN, TPH, ELAN, and TRN all lowered their own forward guidance.

With that background, it looks like the bears are following through to the downside again this morning. Perhaps this is a reaction to HD’s mixed report and both WMT and HD lowering guidance (HD also raised the wages of its hourly workers to the tune of $1 billion). I’m sure that a renewed lack of certainty about the Fed’s March rate action is not helping. (As of this morning, 79% of the Fed Futures bets are on a quarter-percent hike while 21% are looking for a half-percent hike in March.) The DIA is retesting its 50sma at the moment and it looks like the SPY may be headed toward the same retest soon. All three major indices are below their T-lines and the short-term trends are bearish. However, all three also have potential support levels not far below. Continue to be cautious about intraday reversals as we have seen recently.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Hawkish Fed tough talk engaged the bears on Thursday as disappointing inflation data brought the thing the market hates the most, uncertainty! The challenging big-point whipsaws and the short-term extension of the SPY, QQQ, and IWM exacerbates the situation as we move toward a 3-day weekend. Of course, one day does not make a trend, and I wouldn’t expect the bulls to give up easily. However, should price support levels break, fear could quickly spike as traders run for the door to protect capital heading into the long weekend. So expect another day of wild price swings as the drama unfolds.

Asian markets sold off across the board last night due to possible rate increases and the plunging Singapore exports. After notching record highs, European markets trade decidedly bearish this morning as traders grapple with the prospect of Fed uncertainty. U.S. futures also see the bears engaged this morning, pointing to a gap down open that could threaten support levels and the current bullish trends.

Economic Calendar

Earnings Calendar

We get a break in the pace of earnings today, but we still have some market-moving reports. Notable reports for Friday include AMCX, ABR, AN, B, CNP, & DE.

News & Technicals’

Dropbox recorded a real estate impairment of $162.5 million in the fourth quarter, bringing the markdown for the year to $175.2 million. The company signed a record office lease for its San Francisco headquarters in 2017 and then got hit with the Covid pandemic and a market downturn. “We were relatively quick to market with our subleasing plans, but the market has deteriorated, with many companies reducing their real estate footprint,” finance chief Tim Regan said Thursday.

The three unmanned aerial objects that were shot down over the weekend by the U.S. military were “most likely tied to private companies, recreation or research institutions,” President Joe Biden said. “Nothing suggests they were related to China’s spy balloon program,” he added. The remarks came after days of mounting pressure on the White House from Democrats and Republicans in Congress to share more of what was known with the public.

DoorDash reported better-than-expected sales for the fourth quarter and gave upbeat guidance for the current period. As a result, the stock climbed in extended trading on Thursday. The food delivery company said it authorized a buyback of up to $750 million of its shares.

Disappointing wholesale inflation numbers and hawkish Fed speeches encouraged the bears to engage yesterday with another huge point intraday whipsaw to keep traders guessing. However, the DIA remained within its wide-range chop zone by the end of the day, and the current bullish trends in the SPY, QQQ and IWM held above support levels by the close of trading Thursday. Although the price action left behind some concerning daily candle patterns, we must remember that one day does not make a trend. With Friday being a much lighter day of economic and earnings reports, the tough-talking Fed members and uncertainty that may create could be the driving force as we slide into a 3-day weekend. Expect the big point swings to continue on this expiration Friday with high emotions and indexes extended away from crucial moving averages.

Markets made a big gap lower at the open Thursday (down 1.27% in the SPY, down 0.91% in the DIA, and down 1.58% in the QQQ). However, within half of an hour, this began turning into a bear trap as a long, slow, steady rally started at 10 am. This rally had faded most of the gap by 12:50 pm and, from there, the indices ground sideways in a tight range until 2:45 pm. At that point, Fed member Bullard spoke and put a half percent hike in March back on the table. The bears immediately stepped in to start a strong selloff that has lasted right into the close, taking us out on the lows. This action gave us gap-down, black, Inverted Hammers with all three major indices crossing back below their T-line (8ema) after a retest.

On the day, all 10 sectors were in the red as Technology (-1.97%) led the way lower and Communications Services (-0.20%) held up better than the other sectors. At the same time, the SPY was down 1.38%, the DIA was down 1.25%, and QQQ was down 1.88%. The VXX has gained 5.06% to 11.63 and T2122 fell a bit more in the midrange to 57.63. 10-year bond yields spiked again, this time to 3.869% and Oil (WTI) is down 0.57% to $78.14 per barrel. So, on the day, we’ve seen a gap lower met with volatile indecision. This resolved into a bearish push to end the day. Again, this all happened on slightly less-than-average volume.

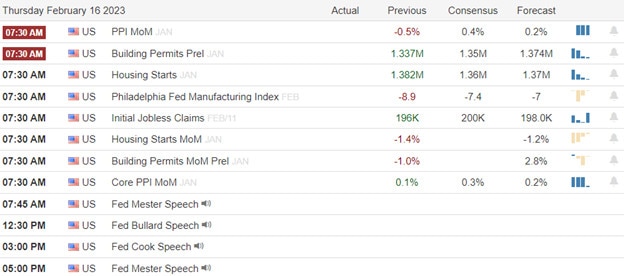

In economic news, the big story on Thursday was a much hotter than expected Jan. PPI number, which came in at +0.7% (compared to a forecast of +0.4% and far worse than the December reading of -0.2%). At the same time, January Building Permits came in slightly lower than expected at 1.339 million (versus the forecast of 1.350 million but better than the December number of 1.337 million). January Housing Starts also came in below what was predicted at 1.309 million (compared to the forecast of 1.360 million and the December value of 1.371 million). On the Weekly Initial Jobless Claims, they were better than expected at 194k (versus the forecast of 200k and also slightly better than last week’s 195k). Meanwhile, the Philly Fed Mfg. Index came in much worse than expected at -24.3 (compared to a forecast of -7.4 and also much worse than the January value of -8.9). In addition to those reports, we also heard from two Fed non-voting officials. Cleveland Fed President Mester said (at the February 1 meeting, before the two recent hot inflation numbers) “I saw a compelling economic case for a 50-basis-point increase, which would have brought the top of the target range to 5%.” (In other words, she did not think the voters were being aggressive enough.) Later on, St. Louis Fed President Bullard “Further Federal Reserve rate increases are needed to lock in disinflation.” He kept the idea of a 50-basis-point hike on the table. However, uncharacteristically for the uber-hawk Bullard, he also said “in broad macro terms it probably does not make too much difference (how fast the Fed moves from here).”

In stock news, an MS survey of the 80 main parts suppliers to the aerospace industry came out Thursday. The report showed that those suppliers likely cannot support the production hikes recently announced by both BA and EADSY (Airbus). Elsewhere, NSC took heavy public and media heat on Thursday for failing to show up at a town hall held related to the NSC train derailment and chemical spill in Eastern Ohio. (The NSC representatives said they did not attend because they feared for their safety in the face of nearly 5,000 local residents.) Meanwhile, in good economic news, GM CEO Barra told a conference Thursday that her company is seeing no sign of any slowing demand for cars. She also said, “we still have very good confidence in the market.” Then, after the close, BP announced it is acquiring TA for $1.3 billion at a price of $86/share.

In stock legal and regulatory news, the NHTSA announced TSLA is recalling 363,000 cars due to its “Full Self Driving” system. In response, TSLA CEO Musk took to Twitter to complain the term “recall” to describe the situation was “anachronistic and just flat wrong.” Meanwhile, a judge from the NLRB found that XOM had been advised by its negotiators that it would need to lock out refinery workers in Texas in order to achieve its goal of taking away seniority-based job protections. The judge had previously ruled the company needed to pay millions in back pay to the 650 workers it locked out for 10 months in 2021. Elsewhere, in a Delaware court, FOX argued Thursday that Dominion Voting Systems cannot prove its $1.6 billion in defamation damages. This filing came in response to Dominion’s request for a summary judgment in their favor based on communications and depositions by FOX executives and on-air talent. Later, after the close, it was announced that ALK lost a $160 trademark dispute with Virgin Airlines. ALK intends to appeal the judge’s ruling.

In energy news, the EIA Natural Gas Report showed that inventories are 17% higher than they were a year ago. This came after a smaller-than-expected draw for the week of 100 billion cubic feet (less than half of the prior week’s consumption). The March front-month Natty contract settled down 3.3% to $2.3890/mmBtu. In other Natural Gas news, after the close, Reuters reported at least three new US LNG export plants are expected to be approved by banks (financiers) this year. The most likely candidates are projects from SRE, ET, and NEXT. SRE said in January it has already sold all of the capacity of the new plant. NEXT has signed deals for 64% of its new project’s capacity (with pending deals that would take that number to 87%). ET hasn’t disclosed how much of its new plant capacity has been sold. However, it is worth noting that even if approved today, it can take up to 4 years to build and get regulatory approval to bring a new LNG production and export terminal online.

After the close, AMAT, ED, AMN, DASH, ATR, RDFN, AL, DBX, DKNG, BFAM, and FBIN all reported beats to both the revenue and earnings lines. Meanwhile, TDS, USM, AEM, and COLD all missed on revenue while beating on earnings. On the other side, DLR, AEL, TXRH, MERC, and GLOB all beat on revenue while missing on the earnings line. Unfortunately, BIO and IAG reported misses on both the top and bottom lines. It is worth noting that AMN, COLD, RDFN, DBX, and HUBS all raised their forward guidance. However, DLR, BFAM, and FBIN lowered their forward guidance.

Overnight, Asian markets were nearly red across the board. Only Singapore (+0.52%) managed to stay green as Shenzhen (-1.61%), Hong Kong (-1.28%), and South Korea (-0.98%) led the region lower. Meanwhile, in Europe, we see a more mixed picture but the bourses are still leaning to the downside at midday. The FTSE (-0.26%), DAX (-0.94%), and CAC (-0.65%) are leading the region lower in early afternoon trade with only Russia (+0.56%) and Greece (+0.64%) appreciably in the green. As of 7:30 am, US Futures are pointing toward a gap lower to start the day. The DIA implies a -0.49% open, the SPY is implying a -0.70% open, and the QQQ implies a -0.90% open at this hour. At the same time, 10-year bond yields are up to 3.875% and Oil (WTI) is plunging, now down 3.5% to $75.71/barrel in early trading.

The major economic news events scheduled for Friday are limited to January Import Price Index and January Export Price Index (both at 8:30 am). The major earnings reports scheduled for the day include ASIX, AMCX, AXL, AN, CNP, CRBG, DE, MD, and PPL before the opening bell. There are no reports scheduled for after the close.

So far this morning, DE, AN, NWG, MD, and CRBG have all reported beats on both the revenue and earnings lines. Meanwhile, CNP and ACDVF missed on revenue while beating on earnings. However, ASIX reported misses on both the top and bottom lines. (PPL and AXL report later in the morning.) It is worth noting that DE raised its forward guidance.

In late-breaking news, American and Chinese officials (perhaps including Sec. of State Blinken) will be meeting on the sidelines of the Munich Security Conference that starts today. Analysts believe this will smooth over the relations and let the two sides set ground rules for surveillance overflights which have always occurred but then recently became a hyped story due to the Chinese Balloon a couple of weeks back. On the opposite side of the China topic, the country’s most influential financier (leading funder of tech companies) Bao Fan has disappeared and this is unnerving Chinese business leaders. It raises concerns on whether President Xi Jingping’s crackdown of private business has finished (as had been thought once he was elected to a third term). The end result is a bit of pessimism related to post-COVID recovery in China amidst fear of making headlines with new projects or of becoming too successful.

With that background, it looks like the bears are following through on what I’ll call the “Bullard Bear Turn” from yesterday afternoon. It is unlikely that Import/Export Prices change that direction. However, we did have some generally good earnings, including a “beat and raise” by DE this morning. So, there is a chance for a premarket reversal. All three major indices are now below their T-line (8ema), retesting their 17ema, and DIA is back down retesting its 50sma in the premarket action. Continue to be cautious about intraday reversals as we have seen the last few days. It would not take much for the bulls to realize Mester and Bullard are not voters this year and all the voters that have spoken continue to imply a quarter-point hike is the correct policy for the FOMC. Finally, remember its Friday…payday…ahead of a three-day weekend. So, take some profits and prepare for the long weekend news cycle.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

On Thursday, markets gapped lower at the open (down 0.55% in the SPY, down 0.46% in the DIA, and down 0.55% in the QQQ). After a volatile first half hour, which saw the QQQ recross the gap twice, all three major averages settled down into a slow, protracted rally until 2:20 pm. The next hour saw a modest pullback. However, a strong rally the last 30 minutes of the day took all three major indices out on their highs. This action gave us white-bodied, gap-down Marubozu-type candles in all three indices. They all held above their T-lines (8ema) and the QQQ is starting to look like a J-hook in the making.

On the day, seven of the 10 sectors were in the green as Technology (+1.29%) led the way higher and Energy (-1.21%) lagged behind the other sectors. At the same time, the SPY was up 0.34%, the DIA was up 0.14%, and QQQ was up 0.77%. The VXX lost 2% to 11.07 and T2122 fell just a bit and remains just outside of the overbought territory at 77.22. 10-year bond yields spiked again, this time to 3.795% and Oil (WTI) is down 0.59% to $78.59 per barrel. So, on the day, we’ve seen a bear trap open that turned into a slow, steady rally the rest of the day. Overall, the trend remains bullish and volume remains low.

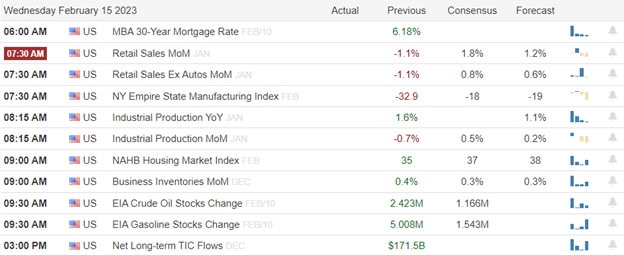

In economic news, the New York Fed Empire State Mfg. Index came in better than expected at -5.80 (compared to a forecast of -18.00 and a January reading of -32.90). Meanwhile, January Retail Sales also beat expectations, coming in at +3.0% (versus the forecast of +1.8% and the December value of -1.1%). At the same time, January Industrial Production came in worst than expected at dead flat (compared to the forecast of +0.5% but still better than the December reading of -1.0%). December Business Inventories reported as expected at +0.3% (right on the forecast and matching the reading from November). However, December Retail Inventories grew more than expected at +0.4% (versus a forecast of +0.3% and November reading of -0.3%) Later, the EIA Crude Oil Inventories report was even worse than had been signaled by the Tuesday API report. EIA showed an inventory build of 16.283 million barrels of crude (compared to a forecasted increase of just 1.166 million barrels and worse than the prior week’s 2.423-million-barrel build).

In stock news, the CFO of F told a conference that they identified ways to improve its cost by over $2.5 billion in 2023 through better management of production schedules as well as F expecting a drop in commodity prices. In other F news, the company said its F-150 Lightning production will remain halted through at least next week as they continue investigating “battery issues.” Meanwhile, Reuters reports that the CEO of TX is considering northern Mexico for the location of a new $2.2 billion steel plant. At the same time, TSLA CEO Elon Musk said he will unveil the third part of his “Master Plan” for the company on March 1. This will include bold goals for the growth of the electric car company. Elsewhere, the Wall Street Journal reported that BLCO is set to name a new CEO (Brent Saunders, who was also previously BLCO CEO) as of March 6. And finally, STLA announced a recall of 340,000 diesel Dodge Ram pickup trucks over electrical connector failures following six fires.

In stock legal and regulatory news, the US Dept. of Justice told a Delaware court that the US government should face a patent lawsuit over COVID-19 rather than MRNA. ABUS had filed the lawsuit against MRNA for patent infringement. Meanwhile, the Wall Street Journal reports that the Justice Department has sped up its investigation into AAPL antitrust complaints. Elsewhere, the EPA set a new soot pollution rule and Reuters reports the KMI and BRKA (for subsidiary PacifiCorp) both sent letters to the EPA warning of the costs they would incur complying. At the same time, the NTSB announced it is opening an investigation into a runway incursion in Honolulu Hawaii where a UAL 777 crossed a runway as a Cessna 208B was landing. Finally, after hours, FDA advisors unanimously voted in favor of allowing the EBS anti-overdose drug Narcan to be sold over the counter nationwide. The FDA is expected to release its final decision on March 29, but it almost always follows unanimous recommendations from the advisory panel.

In energy news, as reported above, oil prices closed down a little despite a massive oil inventory build. This EIA report was the fourth largest oil inventory build ever reported and almost 10 times the forecasted inventory increase. In addition, the US Dollar also climbed to a new 6-week high. So, the disconnect between WTI prices and the news is perplexing. In related news, US refineries are running at 86% of capacity when they would normally be over 90%. As a result, US gasoline inventories rose 2.317 million barrels which was not quite twice the 1.543 million barrels forecasted. However, distillate (diesel and heating oil) stockpiles fell for the first time in five weeks, dropping 1.285 million barrels compared to an expected build of 0.447 million barrels.

After the close, CSCO, SHOP, RSG, AR, EQIX, WCN, AEE, RUSHA, WELL, HST, AIG, AWK, ROKU, TWLO, ALSN, ROL, INVH, NEX, CPA, KGC, QDEL, RGLD, Z, SPWR, and SGEN all reported beats on both the revenue and earnings lines. At the same time, CYH, CF, MRO, ALB, AMED, NUS, SUM, TNET, and RNG all missed on revenue while beating on earnings. On the other side, EQT, SNPS, NTR, and AJRD all beat on revenue while missing on earnings. Unfortunately, ET, REZI, and TROX missed on both the top and bottom lines. It is worth noting that CSCO, RSG, EQIX, WCN, and ALSN all raised their forward guidance. However, NTR, WELL, HST, NUS, AMED, and SGEN all lowered forward guidance.

Overnight, Asian markets were mixed but mostly green. Shenzhen (-1.30%), Shanghai (-0.96%), and Malaysia (-0.26%) were the only red. Meanwhile, South Korea (+1.96%), Hong Kong (+0.84%), and Australia (+0.79%) led the larger group of exchanges to the upside. In Europe, with the exceptions of Greece (-0.18%) and Switzerland (-0.16%) the rest of the region is green at midday. The FTSE (+0.19%), DAX (+0.46%), and CAC (+0.97%) lead the region higher in early afternoon trade. As of 7:30 am, US Futures are pointing to a slightly red start to the day ahead of data. The DIA implies a -0.17% open, the SPY is implying a -0.27% open, and the QQQ implies a -0.33% open at this hour. At the same time, 10-year bond yields are flat at 3.795% and Oil (WTI) is also flat at $78.68/barrel in early trading.

The major economic news events scheduled for Thursday include January Building Permits, January PPI, January Housing Starts, Weekly Initial Jobless Claims, and the Philly Fed Mfg. Index (all at 8:30 am), and a couple Fed speakers (Mester at 8:45 am, Bullard at 1:30 pm, and Mester again at 6 pm). The major earnings reports scheduled for the day include ARCH, BLMN, CVE, CEG, CROX, CNB, ETR, EPAM, FOCS, GGR, GVA, HAS, HSIC, H KBR, KELYA, LH, NSRGY, NGD, NMRK, DNOW, NRG, OGN, PARA, PBF, POOL, POR, RCM, RS, STNG, SO, SCL, SYNH, TOST, USFD, VC, VNT, VMC, WSO, WST, WE, and ZBRA before the opening bell. Then after the close, AEM, AL, AEL, COLD, AMN, AMAT, ATR, BIO, BFAM, ED, CLR, DASH, DKNG, DBX, FBIN, GLOB, IAG, TDS, TXRH, USM, and VALE report.

In economic news later this week, on Friday, January Import Price Index and January Export Price Index are reported. In terms of earnings later in the week, on Friday, ASIX, AMCX, AXL, AN, CNP, CRBG, DE, MD, and PPL report.

So far this morning, SO, RS, HSIC, ETR, ZBRA, SYNH, EPAM, H, ARCH, VNT, GVA, POR, CROX, DNOW, and DDOG have all reported beats on both the revenue and earnings lines. Meanwhile, EADSY, REPYY, USFD, LH, KBR, HAS, BLMN, WST, and SCL have all reported missed on revenue while beating on earnings. On the other side, CVE, KELYA, VC, TOST, RCM, STNG, CEG, and PARA all beat on revenue while missing on the earnings line. Unfortunately, VMC, OGN, POOL, DNB, and WE all missed on both the top and bottom lines. It is worth noting that HSIC, RS, SYNH, BLMN, VC, GVA, and CROX all raised their forward guidance. However, HAS, ZBRA, EPAM, and WE all lowered forward guidance.

In late-breaking news, ASML (Dutch, chip fab lithography leader) reported that a China-based employee stole data from one of its internal software systems used to store technical information about chip-making machinery. This is the second breach of ASML linked to China in the last year and comes very shortly after ASML agreed to the announcement of President Biden’s ban on selling chip-making technologies to China. TSLA fired dozens of workers at its Buffalo NY plant one day after workers at the facility they plan to unionize. The Workers United union has filed a complaint with the NLRB over the obvious retaliation and effort to discourage organizing.

With that background, it looks like markets are flat to modestly lower in pre-open trading. However, all three major indices remain above their T-line (8ema) in an uptrend (although the DIA certainly be called more of a consolidation than a bullish trend). So, apparently, traders are waiting on more clues from the 8:30 am data dump before pushing hard in either direction. We do have generally good earnings as a tailwind, especially from CSCO last night. However, the PPI, Jobless Claims, and Philly Fed reports are likely to call the tune early. Beware of volatility early regardless of which way the post-data, premarket knee-jerk goes. The good news is that the volatility around PPI is likely to be less than that which surrounded CPI. Nonetheless, be cautious and remember that in the long run, your fortune will not be made in the first 30 minutes of the trading day.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

While economic data and Fed members suggest more work on inflation is required, the market has covered its eyes and ears, deciding no news is bad news, at least for now. As a result, the SPY, QQQ, and IWM continue to extend away from their 50-day averages as the DIA chops in a wide multiweek range. Before the bell today, we have another big round of market-moving economic and earnings reports to keep the price action challenging. Expect the big-point whipsaw to continue as fighting the Fed remains in vogue.

Asian markets traded mixed but primarily higher overnight, despite Japan posting its worst-ever trade deficit numbers. European markets continue to extend higher, with the CAC reaching an all-time high despite the Russian spring offensive picking up steam and possible recession. U.S. futures suggest an uncertain open, but with several pending market-moving reports, anything is possible. Expect considerable price volatility as investors digest the data.

Economic Calendar

Earnings Calendar

Notable reports for Thursday include AEM, AMAT, AAWW, BJRI, BLMN, CHUY, COHU, CEG, CROX, ED, DDOG, DLR, DOCN, DASH, DKNG, DBX, ETR, HAS, HSIC HUBS, H, LH, OGN, PARA, POOL, SHAK, SWAV, SO, TXRH, TSEM, USFD, VMC, WE, & ZBRA.

News & Technicals’

The European Union’s embargo on Russian oil products came into effect on Feb. 5, building on the $60 oil price cap implemented by the G-7 (Group of Seven) major economies on Dec. 5. China, India, and Turkey, in particular, have ramped up purchases to partially offset a fall in Russian crude exports to Europe of 400,000 barrels a day in January. According to the IEA’s oil market report, Russian net oil output was down by only 160,000 barrels a day from pre-war levels in January, with 8.2 million barrels of oil shipped to markets worldwide.

Bitcoin surged 11% to $24,655.94 at around 3:36 a.m. ET while ether was up more than 8% at $1,684.59, according to CoinDesk. The value of the entire cryptocurrency market rose more than $84.8 billion in the 24 hours before 3:39 a.m. ET. Crypto markets were on edge earlier this week after a step in regulatory scrutiny from U.S. authorities on stablecoins.

Ford expects production of its electric F-150 Lightning pickup to be down through at least the end of next week to address a potential battery issue that resulted in a vehicle fire. The updated timing comes a day after Ford confirmed production of the highly watched EV had been suspended at the beginning of last week due to a potential battery issue. However, Ford said it believes engineers have found the root cause of the issue.

The market seems to be in a phase where no news is bad news, as economic reports suggest the rate will continue to rise and remain elevated for extended periods. However, fighting the Fed or perhaps ignoring the potential consequences of doing so is now in vogue. Crypo’s also entered the game, surging 11% in the last 24 hours despite the SEC crackdown on the sector. Through all this pushing and shoving, the Dow remains locked in a multiweek consolidation with a price range of nearly 800 points. The tech sector continues to stretch higher even as bond yields and the U.S. dollar strengthens. How much longer this lasts is anyone’s guess but enjoy the ride and keep watch for signs of a reversal that could be substantially punishing once the reality of rate increases and recession returns.

Tuesday’s index prices went wild, generating multiple whipsaws as investors reacted to and tried to sort out the future ramifications of the CPI numbers. Unfrotunitally the big point swings may well continue into Wednesday as the market reacts to market-moving economic reports and a slew of earnings events to keep speculation volatility high. So plan carefully, as the significant point moves make it near impossible to hold onto a trading edge. Remember, cash is a position that protects your capital in these dangerous conditions.

While we slept, Asian markets reacted negatively to the hotter-than-expected CPI numbers seeing red across the board at the close. However, European markets trade mainly higher this morning seemly less concerned about possible inflationary economic impacts. Facing another big day of possible market-moving reports, the U.S. futures point to a lower open but rise from overnight lows waiting for retail sales figures.

A Goldman credit card would’ve been part of a suite of products to help enhance the profit margins and loyalty of its retail efforts, according to people with knowledge of the matter. However, when it scaled back plans to become the primary bank for the masses, the rationale for a Goldman card evaporated, said one of the people. Solomon acknowledged last month that the bank’s ambition in consumer finance outstripped its ability to execute on them.

A costly trading decision sees the annual net profit of Barclays dropping by 19%. The British lender took a substantial hit from an over-issuance of securities in the U.S., which resulted in litigation and conduct charges totaling £1.6 billion throughout 2022.

The Biden administration wants at least 500,000 publicly accessible electric vehicle chargers on US roads by 2030. Now, companies that build and operate charging networks — including Tesla, GM, Ford, ChargePoint, and others — stand to reap the rewards of federal funding if they meet new requirements. For example, white House officials announced that Tesla will open up 7,500 of its charging stations by the end of 2024 to non-Tesla EV drivers. Previously the company’s chargers in the U.S. were used mainly by and made to be compatible with Tesla Evs

In reaction to yesterday’s CPI, the indexes went wild, producing multiple whipsaws as investors grappled with what it means for future rate increases and the possibility of an overall economic slowdown. However, despite the hefty price swings, current support and resistance levels held, leaving more questions than answers as we face another day of likely market-moving reports. Along with impactful economic reports such as retail sales and industrial production, we have a hectic day of earnings to keep prices volatility high and traders making speculative bets on the direction. So, once again, plan for the possibility of big index point moves and continue to watch for those quick, sharp whipsaws.

Markets gapped down modestly after the CPI report. The SPY gapped 0.31% lower, DIA gapped down 0.29%, and QQQ gapped down 0.51%. However, that was just the start of the all-day whipsaw as the bulls immediately stepped in and rallied all three up to more than fade the gap, reaching the highs of the day at 10:15 am. Then the bears reversed the process driving prices back to new lows by noon. At that point, the bulls took us back up in a slower rally until 1:20 pm when we started a sideways grind. This action gave us indecisive candles (Doji or Spinning Top candles) in both of the large-cap indices and a larger body, but still very indecisive candle in the QQQ.

On the day, five of the 10 sectors were in the green as Technology (+0.84%) led the way higher and Consumer Defensive (-0.59%) lagged behind the other sectors. At the same time, the SPY was down 0.05%, the DIA was down 0.41%, and QQQ was up 0.74%. The VXX lost 3.34% to 11.30 and T2122 fell just a bit and remains just outside of the overbought territory at 77.05. 10-year bond yields spiked to 3.751% and Oil (WTI) is down 1.27% to $79.12 per barrel. So, on the day, we’ve seen a massive whipsaw that fizzled into indecision in the market. All 3 major indices held above their T-lines (8ema) and the overall trend is bullish on just under average volume.

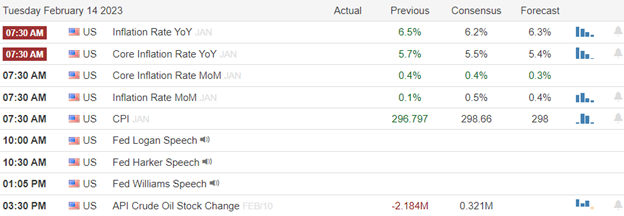

In economic news, the big news of the day was the January CPI which came in higher than expected (but also lower than December) at 5.6% (compared to the forecast of 5.5% and the December value of 5.7%). This resulted in a knee-jerk gap lower in the market that was immediately faded and devolved into a volatile and indecisive day. After the close, the API Weekly Crude Oil Stocks report showed a huge, unexpected build in oil inventories. The report showed a 10.507-million-barrel build (versus the forecast of a 0.321-million-barrel build and last week’s 2.184-million-barrel drawdown). In Fed news, Lael Brainard resigned as the Vice-Chair of the Fed after President Biden named her to head his Economic Advisors. Meanwhile, NY Fed President Williams told reporters that ending 2023 with the benchmark rate between 5.00% and 5.50% “seems to be the right kind of framing.” At the same time, Dallas Fed President Logan told a university audience, “We must be prepared to continue rate increases for a longer period than previously anticipated (if warranted).” However, Richmond Fed President Barkin told Bloomberg “It’s about as expected” (referring to the CPI data) and that “Inflation is normalizing but it’s coming down slowly”. Finally, Philly Fed President Harker said the CPI data did not change his view that the policy rate will have to rise over 5%, but that the Fed was “likely close” (to reaching a sufficiently high enough level to pause).

In stock news, KO said Tuesday that it will push ahead with price hikes in 2023 despite the price-increase halt called by poorer-performing arch-rival PEP. Elsewhere, QSR (owner of Burger King among other chains) named current COO Kuboza to take over as CEO on March 1. Later in the morning, F announced that it had halted production and shipping of its electric F-150 Lightning over what the company called “a potential battery issue.” Meanwhile, Air India announced a massive (record) order for 470 new jets (plus another 25 Airbus jets to be leased). The deal includes 220 planes from BA and 250 planes from EADSY (Airbus). The BA portion of the order includes 190 737 MAX, 20 787 Dreamliners, and 10 777X (mini-jumbos). Meanwhile, TSLA employees in upstate NY announced in a letter to management their intention to form a union. After the close, an SEC 13F filing disclosed that BRKA had increased its holdings of AAPL by over $3 billion in Q4 while it significantly cut its holdings of BK (by 60%) and sold off almost half of its ATVI holdings. BRKA also slashed its holdings of TSM in an odd “trader-like” move since Buffett had only held TSM for a few months.

In stock legal and regulatory news, XOM told a judge that a 10-month lockout of 650 union workers from one of their refineries was not intended to target union employees and was, instead, a move taken to reduce costs and improve profits. (The case is an appeal of an NRLB ruling calling for XOM to compensate the employees for the “illegal lockout” last year after finding the lockout happened after the union notified the company of a potential strike later in the year.) Elsewhere, a US Bankruptcy judge has indicated his intention to dismiss the JNJ talc unit bankruptcy that had been filed in an attempt to shield the parent company from nearly 40,000 lawsuits claiming JNJ talc caused cancer. After the close, the National Transportation Safety Board announced it was opening an investigation into the Dec. 18 incident when a BA 777 operated by UAL sharply dropped 2,200 feet to just 775 feet before recovering.

After the close, ANDE, GXO, ABNB, HLF, SCI, AKAM, WIRE, and CRK all reported beats on both the revenue and earnings lines. Meanwhile, MCY, ENLC, and CLW beat on revenue while missing on earnings. On the other side, CNDT and GDDY missed on revenue while beating on earnings. Unfortunately, DVN and WFG missed on both the top and bottom lines. It is worth noting that ABNB raised its forward guidance while CNDT and GDDY both lowered their guidance.

Overnight, Asian markets leaned heavily to the downside with only India (+0.48%) and Malaysia (+0.28%) in the green. Meanwhile, South Korea (-1.53%), Hong Kong (-1.43%), and Taiwan (-1.42%) led the region lower. In Europe, we see the opposite picture taking shape at midday. Russia (-1.35%), Greece (-1.18%), and Finland (-0.53%) are the only appreciable red while the FTSE (+0.15%), DAX (+0.58%), and especially the CAC (+1.42%) lead the rest of the region higher in early afternoon trade. As of 7:30 am, US Futures are pointing to a start to the day just on the red side of flat. The DIA implies a -0.10% open, the SPY is implying a -0.16% open, and the QQQ implies a -0.17% open at this hour. At the same time, 10-year bond yields are down slightly to 3.751% and Oil (WTI) is down two-thirds of a percent to $78.55/barrel in early trading.

The major economic news events scheduled for Wednesday include NY Fed Empire State Mfg. Index and January Retail Sales (both at 8:30 am), January Industrial Production (9:15 am), December Business Inventories and, December Retail Inventories (both at 10 am), and EIA Weekly Crude Oil Inventories (at 10:30 am). The major earnings reports scheduled for the day include ADI, AVNT, GOLD, BIIB, CHEF, FIS, GNRC, ICL, KHC, LAD, MLM, OC, PSN, RPRX, RBLX, R, SABR, SITE, SAH, SUN, TMHC, TTD, WAB, and WAT before the opening bell. Then after the close, ALB, ALSN, AMED, AEE, AIG, AWK, AR, CF, CSCO, SYH, CPA, ET, EQT, EQIX, HST, INVH, KGC, MRO, NEX, NUS, NTR, QDEL, RSG, REZI, RNG, ROKU, ROL, RGLD, RUSHA, SGEN, SHOP, SUM, SPWR, SNPS, TNET, TROX, TWLO, WCN, WELL, and Z report.

In economic news later this week, on Thursday, we get January Building Permits, January PPI, January Housing Starts, Weekly Initial Jobless Claims, Philly Fed Mfg. Index, and a couple of Fed speakers (Mester, Bullard, and Mester again). Finally, on Friday, January Import Price Index and January Export Price Index are reported.

In terms of earnings later in the week, on Thursday, we hear from ARCH, BLMN, CVE, CEG, CROX, CNB, ETR, EPAM, FOCS, GGR, GVA, HAS, HSIC, H KBR, KELYA, LH, NSRGY, NGD, NMRK, DNOW, NRG, OGN, PARA, PBF, POOL, POR, RCM, RS, STNG, SO, SCL, SYNH, TOST, USFD, VC, VNT, VMC, WSO, WST, WE, ZBRA, AEM, AL, AEL, COLD, AMN, AMAT, ATR, BIO, BFAM, ED, CLR, DASH, DKNG, DBX, FBIN, GLOB, IAG, TDS, TXRH, USM, and VALE. Finally, on Friday, ASIX, AMCX, AXL, AN, CNP, CRBG, DE, MD, and PPL report.

So far this morning, KHC, BIIB, ADI, TMHC, OC, WAB, ICL, AVNT, WAT, and CHEF have all reported beats to both the revenue and earnings lines. Meanwhile, ADRNY, GOLD, SAH, MLM, GNRC, RPRX, and TTD all missed on revenue while beating on earnings. On the other side, SUN and PSN both beat on revenue while missing on the earnings line. Unfortunately, LAD and SITE reported misses to both the top and bottom lines. (R and RBLX report later this morning.) It’s worth noting that ADI, TMHC, AVNT, and CHEF all raised forward guidance. However, MLM lowered its forward guidance.

In late-breaking news, TSLA has agreed to open 7,500 of its charging stations in the US to electric vehicles from other car makers. This move was necessary for TSLA to continue qualifying for certain government incentives. Elsewhere, GS announced it is dropping plans for a branded credit card as it takes another step further away from consumer banking as part of its strategic reorganization. Finally, US mortgage rates rose to 6.39% (from 6.18%) for a 30-year, fixed-rate, conforming loan. This spike had the expected effect on mortgage applications as overall volume fell 7.7%. (Including a 13% fall in refinance applications and a 6% fall in new home purchase applications.)

With that background, it looks like markets are looking to open very modestly lower (at least before the data dump this morning), while holding above the T-line (8ema) in all three major indices. However, the trend in all three remains bullish with resistance not too far above in the SPY and DIA as well as to a lesser extent in the QQQ. The volatility should not be as bad as yesterday’s CPI-induced whipsaw. However, be cautious regardless.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

The bulls produced a Monday reversal on surprisingly low volume as they rushed to buy up risk ahead of the pending CPI report that could produce a substantial price move. Will the bulls get rewarded, or will the report produce a Valentine’s day massacre? We will soon find out and then turn our attention to Wednesday’s market-moving Retail Sales and Industrial production numbers. A slew of earnings will only add to the challenge, so buckle up and prepare for a wild ride over the next few days,

Asian markets mostly gained relatively modest results as Japan nominated their next central bank chief. European look to extend yesterday’s reversal rally, projecting confidence in the pending inflation number. Despite reports that the CPI report could deliver some disappointing sticky inflation reading, the U.S. trade higher in the premarket, hoping to extend yesterday’s big upward push.

Economic Calendar

Earnings Calendar

Notable reports include ABNB, AKAM, ANDE, BTU, CLF, CRK, CNDT, DVN, GDDY, GFS, GXO, HLF, HWM, KO, MAR, QSR, SCI, SU, TRU, TRIP, UPST, WEBR, & ZTS.

News & Technicals’

All market eyes Tuesday will be on the release of the Labor Department’s consumer price index, a widely followed inflation gauge. Economists are expecting that the CPI will show a 0.4% increase in January, which would translate into 6.2% annual growth. However, there’s some indication the number could be even higher. The Federal Reserve is determined to keep fighting inflation so that the report could harden their position.

Inflation in the U.S. is likely to be “far stickier” and could last a decade, according to Bill Smead, chief investment officer at Smead Capital Management. Wall Street is gearing up for news on key inflation data later Tuesday as the Labor Department will release its January consumer price index.

President Joe Biden is expected to name Federal Reserve Vice Chair Lael Brainard to the White House’s top economic policy position as early as Tuesday. Brainard would replace White House National Economic Council (NEC) Director Brian Deese, who has announced his resignation.

We began the week with another reversal as the bulls rushed to buy, pressing resistance levels, seemingly unconcerned about the potential big-point reaction from the pending CPI report. While the VIX registered a reversal of fear, volume was surprising considering the big move in the indexes. Expect a substantial price reaction as the number comes out, and don’t rule out the possibility of a wild whipsaw before the open. Anything is possible, and the market will turn its eyes toward the Retail Sales and Industrial Production numbers on Wednesday morning.

On Monday, stocks gapped very modestly higher (up 0.16% in the SPY, up 0.05% in the DIA, and up 0.45% in the QQQ) at the open. Then a slow, but steady rally took over until 12:45 pm. From that point, all three major indices ground sideways with the QQQ even having a slightly bearish trend to that grind for the rest of the day. This action gave us white-bodied candles with small upper wicks. (QQQ also had a lower wick.) All three major indices have crossed back above their T-line (8ema) and both large-cap indices are also at least retesting a resistance level. Meanwhile, the QQQ is retesting the uptrend level it failed last Thursday. This all happened on a very much lower-than-average volume.

On the day, nine of the 10 sectors were in the green as Consumer Cyclical (+1.51%) led the way higher and Energy (-0.020%) lagged behind the other sectors. At the same time, the SPY was up 1.18%, the DIA was up 1.12%, and QQQ was up 1.60%. The VXX lost almost 4% to 11.69 and T2122 rose but remains just outside of the overbought territory at 77.27. 10-year bond yields fell to 3.705% and Oil (WTI) is a half of a percent to $79.25 per barrel. So, on the day, we saw the bulls in charge all morning and then a dead market most of the afternoon. This just seems like trader’s waiting on the CPI data Tuesday to give a clue about what the Fed may do in March.

In Fed news, Federal Reserve Governor Bowman spoke Monday. She said “I expect we’ll continue to increase the federal funds rate because we have to bring inflation back down to our 2% goal…” Bowman went on to say that a very strong labor market alongside moderating inflation means a “soft landing” remains possible. In other Fed news, the NY Fed announced that a January survey of consumers shows the biggest monthly drop in “wage growth” (income growth) expectations in 10 years. The expected wage growth fell 1.3% to +3.3% for the year as of January.

In stock news, early Monday TWLO announced another round of layoffs, eliminating about 17% of its workforce and closing some offices. In other layoff news, UPS said Monday that it will join rival FDX is looking to reduce headcount in the areas of the US where demand is down. This comes ahead of UPS negotiations with the Teamster union (contract expiring July 31). Meanwhile, Reuters reports that the recent spate of big tech layoffs is a boon for farm equipment makers who are snapping up hundreds of tech workers. Specifically, the article mentioned DE, CAT, and CNHI as hiring hundreds of engineers each from the pool of former employees from the likes of AMZN, MSFT, and META. Elsewhere, ALC agreed to pay JNJ $199 million to settle an intellectual property suit related to laser eye-surgery devices. F announced that they will recognize the UAW at the new $3.5 billion battery plant in Marshall MI (reported here last week). This means that if a majority of workers at that facility just sign a card supporting a union, then the UAW will represent all workers without the need for formal votes. Finally, AMZN announced that it has successfully tested its “Zoox” robotaxis using employees as passengers on public roads between two AMZN facilities in Foster City, CA. The milestone moves the project closer to publicly available self-driving cars as well as competing with GOOGL’s “Waymo” robotaxi project.

In energy news, after hours Monday, the Biden Administration said that the government is planning to sell another 26 million barrels of oil from the Strategic Reserve. The White House says they do not want to do so now that oil prices have stabilized. However, a budget mandate enacted in 2015 (pertaining to the current fiscal year) mandates the sale of 26 million barrels this year. The Energy Dept. has sought to stop these sales in an effort to begin refilling the reserve. However, without new Congressional action, the sale is required by law. After this sale, the US reserve would drop to about 345 million barrels.

After the close, CAR, ACGL, IAC, ANET, CDNS, SEDG, and PLTR all reported beats on both the revenue and earnings lines. Meanwhile, ES, FE, and AMKR beat on revenue while missing on the earnings line. On the other side, MRC missed on the revenue line while beating on earnings. Unfortunately, ASTL missed on both the top and bottom lines. It is worth noting that ANET, CDNS, and SEDG all raised their forward guidance. However, AMKR, JHX, and PLTR lowered their forward guidance.

Overnight, Asian markets were mixed on mostly modest moves. Thailand (-0.73%) paced the losses while India (+0.89%), Japan (+0.64%), and South Korea (+0.50%) led the gainers. Meanwhile, in Europe, the bourses are leaning toward the green side at midday with the notable exception of Russia (-1.27%). The FTSE (+0.40%), DAX (+0.42%), and CAC (+0.50%) are leading the region higher in early afternoon trade. AS of 7:30 am, US Futures are pointing to a modest green start to the day (ahead of CPI data). The DIA implies a +0.13% open, the SPY is implying a +0.28% open, and the QQQ implies a +0.43% open at this hour. At the same time, 10-year bond yields are down to 3.69% and Oil (WTI) is off 1.55% to $78.90/barrel.

The major economic news events scheduled for Tuesday include January CPI (8:30 am) and the API Weekly Crude Oil Stock Report (4:30 pm). We also get a couple of Fed speakers (Harker at 11:30 am and Williams at 2:05 pm). Major earnings reports scheduled for the day include CAE, CLF, KO, ECL, ENTG, EXC, FELE, GTX, GEO, GFS, HRI, HWM, LCII, LDOS, MAR, BTU, PKI, QSR, TRU, WCC, and ZTS before the opening bell. Then after the close, ABNB, AKAM, ANDE, CLW, CRK, CNDT, DVN, WIRE, ENLC, GDDY, GXO, HLF, MCY, NU, SCI, SU, TX, and WFG report.

In economic news later this week, on Wednesday, NY Fed Empire State Mfg. Index, January Retail Sales, January Industrial Production, December Business Inventories, December Retail Inventories, and EIA Weekly Crude Oil Inventories are reported. On Thursday, we get January Building Permits, January PPI, January Housing Starts, Weekly Initial Jobless Claims, Philly Fed Mfg. Index, and a couple of Fed speakers (Mester, Bullard, and Mester). Finally, on Friday, January Import Price Index and January Export Price Index are reported.

In terms of earnings later in the week, on Wednesday, ADI, AVNT, GOLD, BIIB, CHEF, FIS, GNRC, ICL, KHC, LAD, MLM, OC, PSN, RPRX, RBLX, R, SABR, SITE, SAH, SUN, TMHC, TTD, WAB, WAT, ALB, ALSN, AMED, AEE, AIG, AWK, AR, CF, CSCO, SYH, CPA, ET, EQT, EQIX, HST, INVH, KGC, MRO, NEX, NUS, NTR, QDEL, RSG, REZI, RNG, ROKU, ROL, RGLD, RUSHA, SGEN, SHOP, SUM, SPWR, SNPS, TNET, TROX, TWLO, WCN, WELL, and Z report. On Thursday, we hear from ARCH, BLMN, CVE, CEG, CROX, CNB, ETR, EPAM, FOCS, GGR, GVA, HAS, HSIC, H KBR, KELYA, LH, NSRGY, NGD, NMRK, DNOW, NRG, OGN, PARA, PBF, POOL, POR, RCM, RS, STNG, SO, SCL, SYNH, TOST, USFD, VC, VNT, VMC, WSO, WST, WE, ZBRA, AEM, AL, AEL, COLD, AMN, AMAT, ATR, BIO, BFAM, ED, CLR, DASH, DKNG, DBX, FBIN, GLOB, IAG, TDS, TXRH, USM, and VALE. Finally, on Friday, ASIX, AMCX, AXL, AN, CNP, CRBG, DE, MD, and PPL report.

So far this morning, EXC, KO, WCC, MAR, LDOS, ZTS, QSR, HWM, GFS, HE, ENTG, and GEO all reported beats to both the revenue and earnings lines. Meanwhile, CLF, TRP, LCII, and HRI all beat on revenue while missing on earnings. On the other side, PKI missed on revenue while beating on earnings. Unfortunately, GTX and TRU both missed on both the top and bottom lines. It is worth noting that ZTS and GFS raised forward guidance. However, PKI, HWM, GTX, and ENTG all lowered their own forward guidance.

With that background, it looks like the bulls are looking to a positive open at this point. However, that is sure to change to either a nasty gap down or to a bigger gap up once the CPI numbers are out. Regardless of how that turns out, be careful wading into the volatility at the open. There is likely to be jerks in both directions before the bell stops ringing. However, the trend remains bullish, at this point, in all three major indices. SPY and DIA are still not quite broken free of their resistance test (they are passing so far) and QQQ is back up against the uptrend line dating back to the first of the year.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service