The tech sector continues to stretch higher, with talk of a new bull market ringing in the ears of traders fearful of missing out despite the short-term overbought condition. With a scorching hot labor market keeping the Fed active and signs of a weakening consumer raising, one has to wonder how long this can continue. The fear of missing out is a powerful emotion but guard yourself against chasing already extended stocks or indexes because a significant reversal to test support levels is not out of the question. Plan for another week of price volatility with another busy data week ahead.

Asian markets traded mixed and mostly lower overnight as traders reacted to the hot U.S. jobs data and the likelihood of more rate increases coming. European markets trade with a bit of bearishness to begin the week, and the U.S. futures point to gap down open with tech leading the way. I would not expect the bulls to give up easily but don’t rule out the possibility of a substantial pullback to test support levels at any time.

Economic Calendar

Earnings Calendar

Notable earnings to kick off the new trading week, ACTVI, CHGG, CMI, FN, IDXX, LEG, ON, PINS, RMBS, SPG, SWKS, SAVE, TTWO & TSN.

News & Technicals’

China urges calm after the violation of U.S. airspace. “What I want to emphasize regarding this unexpected accident is that both sides, especially the U.S., should remain calm,” said China’s Ministry of Foreign Affairs spokesperson Mao Ning in Mandarin, according to a CNBC translation. She was speaking at the first of the ministry’s daily press conferences after U.S. Secretary of State Antony Blinken indefinitely postponed his trip to Beijing in light of news that a suspected Chinese surveillance balloon was flying over the United States.

In 2022, Huawei announced it signed more than 20 new or extended patent licensing agreements. Huawei ranked fourth last year by the number of patent grants in the U.S., said IFI Claims Patent Services. In addition, according to the China Intellectual Property Administration website, Huawei filed for a lithography technology patent late last year.

The U.S. will transition the federal Covid vaccination program to the private market as soon as the fall. This means Pfizer and Moderna would sell the shots directly to healthcare providers at a higher price. However, Americans with health insurance would still get their Covid shots for free once the vaccine program goes commercial. But the uninsured may have to pay the total price of the shots after the current federal supply runs out. The federal vaccine program will not be affected by the end of the Covid public health emergency in May, the White House said.

As bullish confidence in tech surges with talk of a new bull market ringing in the investor’s ears, the weak manufacturing sector and the hot jobs sector fans the flames of uncertainty. However, the capacity of this market to ignore any bad data while rushing the buy during earnings reports has been truly remarkable. The question is, how long can it last? Friday’s selling relieved some short-term overbought conditions, but we should not be surprised if a quick and substantial pullback begins at any time. With another big week of reports, expect challenging price moves making for dangerous conditions for retail traders.

Markets gapped down on Friday (SPY gapped 1.24%, DIA gapped down 0.51%, and QQQ gapped down 2.29%) after January Payrolls crushed expectations. However, the bulls stepped in immediately to rally back to the Thursday close level in the first 60-75 minutes. All three major indices reached the highs of the day at 11:40 am. Then the bears over again to start a selloff that lasted into the close. This action gave us gap-down, Inverted-Hammer-type candles in the three major indices. The DIA also fell back below its T-line (8ema).

On the day, all 10 sectors are red as Utilities (-1.99%) lead the way lower and Energy (-0.27%) held up better than the other sectors. At the same time, the SPY is down 1.06%, the DIA is down 0.41%, and QQQ is down 1.78%. Meanwhile, the VXX is up 0.98% to 11.32 and T2122 is dropping but remains just inside the overbought territory at 82.24. 10-year bond yields have spiked higher to 3.526% and Oil (WTI) is down 3.56% to $73.19 per barrel. So, on the day, we saw a significant gap lower that the bulls tried to fade, only to be pushed back down by the bears. This all happened on heavier-than-average volume.

In economic news, the January Jobs Reports were the headline makers. January Nonfarm Payrolls increased a whopping +517k (compared to an estimate of +185k and the December value of +260k). January Private Nonfarm Payrolls also far exceeded the estimates at +443k (versus the forecast of +190k and a December reading of +269k). Both numbers crushed estimates as the leisure and hospitality sector showed a huge gain, followed by professional/business services, government, and healthcare. The increases happened despite the Jan. Participation Rate also increasing to 62.4% (from the December value of 62.3%). This surge in employment drove the January Unemployment Rate to a 53-year low (since 1969) of 3.4% (versus a forecast of 3.6% and a Dec. reading of 3.5%). So, despite over 100,000 job cuts announced in January by various firms, the economy is still producing jobs at a massive rate, far faster than expected. Markets were skeptical, but this could be a sign of the Fed threading the needle as inflation is falling while huge numbers of jobs are being created. In other economic news, the Jan. Services PMI beat expectations at 46.8 (versus the forecast of 46.6 and the Dec. value of 44.7). Finally, ISM Non-Mfg. PMI came in much hotter than expected at 55.2 (compared to the forecast of 50.4 and the Dec. value of 49.2). So, judging by payrolls and purchasing managers’ outlooks, the economy is much stronger than the news headlines had led us to believe.

In energy news, the front-month March contract for Natural Gas fell another 21% last week, closing at $2.41/mmBtu. This is the lowest wholesale natural gas price in the US for over two years. As a result, energy firms cut the number of active natural gas rigs to the lowest level since June 2020. Meanwhile, Oil (WTI) closed down 3.56% on the day, resulting in an 8% drop for the week. This may or may not be related to another cut in the number of oil rigs producing in the US. Regardless, the number of oil rigs fell by almost 2% over the week.

In stock news, the US Treasury Dept expanded eligibility for up to $7,500 tax credit to cover more expensive (SUVs). This includes newly eligible models from F, GM, TSLA, and VLKAF. In response to this news, TSLA raised the price of its Model Y by $1,000. Elsewhere, late Friday Bloomberg reported that DIS is in talks to sell more of its movies and TV series to rival networks. (No specific rivals were mentioned.) Meanwhile, HMC issued a “Do Not Drive” warning covering 8,200 of its vehicles over defective and unrepaired airbags. After the close, LUV confirmed that its CEO will be testifying in front of a US Senate hearing on Thursday related to the company’s holiday travel mess. Late Friday night, a train from NSC derailed near the border of Ohio and Pennsylvania. On Saturday, 32,000 DIS theme park workers voted to reject a DIS contract proposal by a margin of 96% rejecting to 4% in favor. The negotiations have been ongoing since August, but no date for the resumption of talks has been set yet.

In stock legal and regulatory news, on Friday, current and former US military members asked a federal judge to throw out the Chapter 11 bankruptcy filed by MMM subsidiary Aearo Technologies (as a means of protecting MMM against 230k lawsuits claiming the company’s defective earplugs had caused hearing loss for US military members). At the same time, FDX lost its bid to have a judge throw out a $366 million jury award over a racial discrimination lawsuit that FDX lost. Later, the Wall Street Journal reports that the US FTC is preparing to file an antitrust lawsuit against AMZN. Also after the close, a jury found that TSLA and its CEO Elon Musk were not liable in a securities fraud case stemming from Musk’s tweets saying he had secured financing and was going to take TSLA private at a price 23% above the then-current market price. In other court action, a US district judge denied the FTC request to stop META from buying virtual reality content maker Within Unlimited.

In miscellaneous news, the UN Food and Agriculture Organization (FAO) announced after the close Friday that world food prices fell again in January. This was the 10th consecutive drop in that food price index, with global food prices reaching the lowest level since September 2021. They specifically cited drops in vegetable oils, dairy, and sugar prices while noting that cereals and meat prices remained stable for the month. As an example, FAO said vegetable oil prices fell 2.9% in January while dairy prices fell 1.4%, and sugar declined 1.1%.

So far this morning, CAN, TKR, and IDXX reported beats on both the revenue and earnings lines. Meanwhile, AMG and IX missed on revenue while beating on earnings. On the other side, TSN beat on revenue while missing on earnings. Unfortunately, ENR missed on both the top and bottom lines. (CMI and ON report closer to the open.)

Overnight, Asian markets were mixed but mostly red. Hong Kong (-2.02%), Taiwan (-1.34%), and Shenzhen (-1.18%) led the region lower. Japan (+0.67%) was an outlier to the upside. In Europe, with the sold exception of Russia (+0.85%), bourses are red across the board at midday. The FTSE (-0.77%), DAX (-1.03%), and CAC (-1.40%) are leading the region lower in early afternoon trade. As of 7:30 am, US Futures are pointing toward a gap down to start the day. The DIA implies a -0.54% open, the SPY is implying a -0.71% open, and the QQQ implies a -0.91% open at this hour. At the same time, 10-year bond yields are spiking again to 3.604% and Oil (WTI) is up a quarter of a percent to $73.56/barrel in early trading.

There are no major economic news events scheduled for Monday. The major earnings reports scheduled for the day include AMG, CNA, CMI, ENR, IDXX, ON, IX, TKR, and TSN before the opening bell. Then, after the close, AMKR, ATVI, ACM, CINF, DIOD, FN, KMT, LEG, NOV, PINS, SPG, SSD, SKY, SWKS, SAVE, TTWO, and TFII, report.

In economic news later in the week, on Tuesday, December Imports/Exports, Dec. Trade Balance, and API Crude Oil Stocks are reported and Fed Chair Powell speaks. Then Wednesday EIA Crude Oil Inventories are reported and Fed member Williams speaks. On Thursday we get Weekly Jobless Claims. Finally, on Friday, Michigan Consumer Sentiment and Jan. Federal Budget Balance are reported and we hear from Fed members Waller and Harker.

Other late-breaking (and less market-related) news includes the “over-hyped” story of the Chinese spy balloon that the US shot down this weekend. Navy divers continue their work to recover the wreckage from the 7-mile-wide debris field. This story was over-hyped because it is the fourth recent such Chinese balloon overflight of the US (dating back to three during the Trump Administration) and is certainly not the only Chinese surveillance of the US that goes on constantly (satellites, perimeter flights, hacking, human assets, etc.). Nonetheless, the news cycle and political opportunity conspired to make this one a story. The only thing that matters here is if and how a US response might impact US-Chinese trade relations. The other story was a pair (7.7 and a 7.5 on the Rictor scale) of earthquakes in Southern Turkey. These should have minimal international market and business impacts but do have the potential to roil oil markets because they technically were located in the Middle-East and not extremely far from Syrian oil fields.

With that background, it looks like the SPY is going down to retest its T-line as support during pre-market trade. At the same time, DIA is failing its T-line as support and retesting its 50sma as support, all while QQQ pulls back but has not reached its T-line yet. DIA remains in its wedge, while the trend remains strongly bullish in the SPY and QQQ (trends have not even been retested by the pullback this morning). So, be careful and nimble on any short positions you might take and remember the bias is still bullish.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Markets diverged at the open Thursday (the SPY gapping up 1%, the QQQ gapping up 2.21%, and DIA gapping up just 0.17%). At that point, the DIA sold off hard for 15 min. while the SPY and QQQ just chopped for the first 45 minutes. Then SPY and QQQ both rallied hard for 40 minutes before joining DIA in a sideways grind with a slightly bullish trend that lasted until 2 pm. However, at that point, markets sold off hard for a little over an hour. Finally, the last 60 minutes saw a bounce. This action gave us an indecisive gap-up, Spinning Top candle in the SPY, a black-bodied hammer in the DIA, and a gap-up white-bodied candle with upper and lower wicks in the QQQ. SPY also completed a Golden Cross (50sma crossed above 200sma).

On the day, six of the 10 sectors were in the green as Technology (+3.58%) leads the way higher, and Energy (-1.99%) lagged behind the other sectors. Meanwhile, the SPY was up 1.44%, the DIA was down 0.16%, and QQQ was up 3.59%. At the same time, the VXX was up 2.19% to 11.22 and T2122 fell but remains deep in the overbought territory to 96.39. 10-year bond yields plunged down to 3.395% and Oil (WTI) was down 0.85% to $75.76 per barrel. So, on the day, we saw very divergent markets as the massive technology big dogs pulled the QQQ and SPY higher while the DIA languished. However, at the end of the day, we saw indecision across the board. This all happened on heavier-than-average volume.

In economic news, Weekly Jobless Claims came in better than expected at 183k (compared to the forecast of 200k and the prior week’s reported 186k). Q4 Nonfarm Productivity also came in much better than expected at +3.0% (versus the forecast of +2.4% and the Q3 reading of +1.4%). In addition, Q4 Unit Labor Costs were also far better than expected at +1.1% (compared to a forecast of +1.5% and the Q3 reading of +2.0%). However, December Factory Orders came in lower than expected at +1.8% (versus the forecast of +2.3%, but far better than the November number of -1.9%). On the whole, I think the Fed liked those numbers as productivity was stronger than expected while labor costs rose less than expected and while factory activity remained positive (growing) it was not as hot as the average economist had predicted.

In stock news, Medicare Advantage released its proposal to DECREASE rates by 2.27% in 2024. This was both unexpected and far below the 5% increase in 2023 (when it had proposed increasing 4.48%). As a result, UNH, HUM, CNC, ELV, CVS, and CI all took a hammering Thursday. Elsewhere, KKR made a bid to buy the controlling interest in Italy’s largest phone company for somewhere north of $22 billion. (VIVHY owns the largest block of shares now at 24%.) Meanwhile, the FTC has rejected a petition from META to have FTC Chair Lina Khan recused from participating in any review or decision on META’s proposed acquisition of (virtual reality app maker) Within Unlimited. Finally, EU lawmakers agreed to tougher rules related to political ads that are targeted at limiting the power of GOOGL and META in the name of countering misinformation.

In energy news, the front month March Natural Gas contract closed lower to $2.456 per mmBtu. This closing price came after trading at a 22-month low earlier in the session. The continued fall in natty prices happened despite a larger-than-expected drawdown for US storage in the weekly inventory report. (The EIA reported a draw of 151 billion cubic feet, compared to the expected drawdown of 142 billion cubic feet.) Meanwhile, Oil dipped mainly on the back of a rebound by the dollar from its lows on Wednesday. A Reuters report also said that Chinese oil imports were lower in January than in either December or November at 10.98 million barrel per day versus 11.37mbpd and 11.42mbpd respectively. Elsewhere, US Gasoline inventories have gone up almost 13 million barrels since January 1 and even distillates (Diesel and Heating Oil) stocks rose last week, for the first time in five weeks.

In miscellaneous news, corporate stock buyback programs tripled in January (versus a year ago) to $132 billion. It is worth noting that this is significant because 2022 saw a record $1.26 trillion in stock buybacks and analysts (such as GS and MS senior market analysts) had been expecting buybacks to fall 40% due to recession fear. This tends to indicate that so far, corporations are not nearly as concerned about recession impacts as analysts expected (or are just in better financial shape than analysts knew). On another hopeful note, in their report, CLX not only beat expectations but also raised guidance and said there would be no further layoffs in 2023.

After the close, AMZN, GILD, HIG, X, CTSH, LPLA, MCHP, CLX, SKX, POST, MEOH, DECK, COLM, BYD, OTEX, SIGI, ENSG, TEAM, GEN, and CRUS all beat on the revenue and earnings lines. Meanwhile, F and RGA beat on revenue while missing on earnings. On the other side, QCOM, KMPR, HUBG, BZH, and CVCO all missed on revenue while beating on earnings. Unfortunately, AAPL, GOOGL, GOOG, SBUX, SKYW, and MTX missed on both the top and bottom lines. It is worth noting that MCHP, POST, and TEAM all raised their forward guidance. However, CTSH, SKX, and COLM lowered their forward guidance.

Overnight, Asian markets leaned to the green side with the exception of China. Hong Kong (-1.36%), Shanghai (-0.68%), and Shenzhen (-0.63%) were the only red in the region. Meanwhile, India (+1.38%), Australia (+0.62%), and Singapore (+0.61%) led the region higher. In Europe, the picture is much redder in color at midday. The FTSE (+0.25%) is among the minority of bourses in the green while the DAX (-0.55%) and CAC (-0.15%) are more typical in early afternoon trade. As of 7:30 am, US Futures are pointing toward a down start to the day. The DIA implies a -0.26% open, the SPY is implying a -0.72% open, and the QQQ implies a -1.29% open at this hour. At the same time, 10-year bond yields are flat at 3.396% and Oil (WTI) is off just pennies to $75.69/barrel in early trading.

The major economic news events scheduled for Friday include Jan Avg. Hourly Earnings, Jan. Nonfarm Payrolls, Jan. Participation Rate, and Jan. Unemployment Rate (all at 8:30 am), Services PMI (9:45 am), and ISM Non-Mfg. PMI (10 am). Major earnings reports scheduled for the day include AON, ARCB, AVTR, SAN, BSAC, BBU, BEPC, BEP, CBOE, CHD, CI, LYB, MOG.A, NFG, REGN, SAIA, SNY, and ZBH before the opening bell. Then, after the close, there are no scheduled reports.

So far this morning, SAN, BBU, REGN, AON, ZBH, CHD, NFG, and UI have all reported beats to both the revenue and earnings lines. Meanwhile, CI, LYB, ASAZY, CBOE, and AVTR missed on revenue while beating on earnings. On the other side, BEP beat on revenue while missing on earnings. Unfortunately, SNY, ARCB, and SAIA missed on both the top and bottom lines. No major changes to guidance have been announced yet this morning.

So, the big news overnight was the disappointing misses by the big dog tech names, AAPL and GOOGL and GOOG (which both complained of low interest from advertisers). F also missed on earnings, and probably more importantly, had a dismal report compared to arch-rival GM’s information from earlier in the week. Combined with this morning’s bad reports from trucking companies (ARCB and SAIA), the mix is likely to have Mr. Market in a worried mood (in terms of the economy) ahead of the January Payrolls report. Regardless of mood, we have to realize that it is going to be hard for the SPY or QQQ to go up when AAPL, GOOG, and GOOGL go down. Even with the beats by AMZN to help, that will be a tough lift given how much volume those three tickers trade each day. With that said, it is worth noting that all three have made significant recoveries from their pre-market lows. As a result, the major indices (SPY and QQQ) are hanging in too ahead of the data.

With that background, it looks like the recent leaders (QQQ and SPY) are going to gap down. However, neither is even close to retesting its up-trending T-line (8ema). DIA is retesting its T-line from above again. However, it has been chopping sideways in its wedge for some time now. So, this is nothing to be too worried about. SPY did complete its Golden Cross yesterday (50sma crossing up the 200sma). However, QQQ also ran into a resistance level. So, technically, markets still have a bullish bias. However, remember that it’s Friday… payday. So, pay yourself, lock in profits, and prepare your account for the weekend.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Markets gapped down modestly on Wednesday (down 0.31% in SPY, down 0.50% in DIA, and down 0.16% in QQQ). The large-cap indices then wandered sideways with a slightly bearish trend and the QQQ just flat meandered sideways until 2 pm. However, when the Fed announced, we saw volatility to the upside and then to the downside over the next 30 minutes. Yet, as soon as Fed Chair Powell began speaking, we got a strong bullish rally for 75 minutes. Finally, we saw profit-taking in the last 15 minutes of the day. This action gave us white-bodied candles with wicks on both ends. Only the DIA would be seen as a candle signal as it printed an indecisive Spinning Top candle. IT is worth noting that SPY closed right up against a resistance level.

On the day, nine of the 10 sectors were in the green as Technology (+2.72%) lead the way higher and Energy (-1.52%) lagged behind the other sectors. At the same time, the SPY was up 1.06%, the DIA was up 0.01%, and QQQ was up 2.14%. Meanwhile, the VXX was down 3% to 10.98 and T2122 is even higher, deep in the overbought territory to 98.74. 10-year bond yields plunged down to 3.417% and Oil (WTI) was off 2.75% to $76.70 per barrel. So, on the day, we saw a drift sideways until the Fed Chair began speaking. At that point, the bulls rallied very hard only to take profits the last 15 minutes of the day. This all happened on heavier-than-average volume.

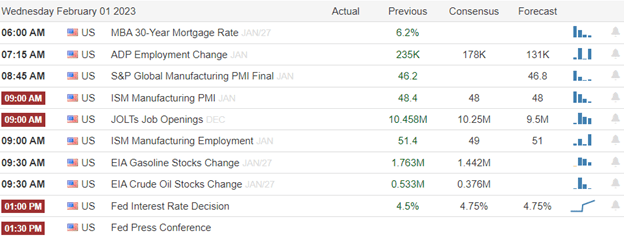

In economic news, the January ADP Nonfarm Employment Change came in well below forecast at +106k (compared to an expected +178k and a Dec. reading of +253k). Later, January Mfg. PMI came in slightly above expectation at 46.9 (versus a forecast of 46.8 and the Dec. value of 46.8). Then the January ISM Mfg. PMI came in below what was expected at 47.4 (compared to the forecast of 48.0 and December’s reading of 48.4). At the same time, the December JOLTs Job Openings report showed a much higher reading than expected at 11.012 million (versus the forecast of 10.250 million and the Nov. value of 10.440 million). All of these tend to indicate the Fed policies are having the impacts they had hoped.

However, the main event of the day was the Fed and in Fed news, the FOMC hiked rate 0.25% to 4.50% – 4.75%, which is the highest since October 2007. During his press conference, Fed Chair Powell repeatedly referred to the “disinflationary process that has started.” However, he also said “we’re going to be careful about declaring victory” and “we’ve got a long way to go.” Powell said the labor market is still out of balance and the Unemployment Rate will need to rise from its low 3.5% level to complete the journey back to 2% inflation. Finally, in a side note to one question, Powell said “a couple more” (rate hikes were likely to come). That last note was exactly the music the bulls wanted to hear.

In stock news, FDX announced it was cutting more than 10% of management as part of the overall 2% workforce reduction. The company said it had already reduced staff by 12,000 since June. Elsewhere, AMGN launched a direct competitor drug to ABBV’s blockbuster arthritis offering (Humira). Competition is expected to lower customer prices, but analysts are expecting the savings to be limited (~ 5%) since it is in the interest of both companies to keep margins as high as possible. Meanwhile, Reuters reports that RIVN is laying off 6% of its workforce in an effort to cut costs. At the same time, the Polish competition watchdog (Office of Consumer Protection) has accused AMZN of misleading consumers via its sales and delivery practices on its website. In other news, Reuters reports that RPD is considering strategic options after attracting acquisition interest. (RPD spiked 23% Wednesday afternoon on this report.) Finally, AMC has requested stockholder approval to increase its shares outstanding by 10 times. However, it has coupled that proposal with a second very popular one that would convert deeply discounted preferred shares into common stock and the two ideas will be decided on a single vote. The vote is scheduled for March 14.

In energy news, natural gas continued its relentless march downward, closing down 8% to $2.46/mmBtu on Wednesday. The front-month natty has lost more than 20% so far this week alone. This appears to be a consumption-led decline since natural gas inventories are only 4% higher than they were a year ago. Elsewhere, the midday EIA Crude Oil Inventories showed a much larger-than-expected build in oil stocks. US Inventories went up 4.140 million barrels (compared to a forecast of +0.376 million barrels and following last week’s build of +0.533 million barrels). This was the sixth straight week of oil inventory builds in the US. As mentioned above, WTI closed down 2.75% at $76.70/barrel (which was actually after recovering from an afternoon low of $76.08/barrel).

After the close, ALGN, ALGT, ALL, AFG, AVT, CCS, CTVA, ENVA, THG, HOLX, MCK, MTH, META, MAA, QRVO, TTEK, and UGI all reported beats on both the revenue and earnings lines. Meanwhile, AFL, BHE, CHX, DXC, GL, LFUS, MOD, and RRX missed on revenue while beating on earnings. On the other side, PTC and SLM both beat on the revenue line while missing on earnings. However, CHRW, HTHIY, LSTR, MET, and MUSA missed on both the top and bottom lines. It is worth noting that ALGN, AVT, GL, HOLX, MCK, PTC, SLM, and TTEK all raised their forward guidance. Unfortunately, BHE, CCS, CHX, CTVA, DXC, LSTR, LFUS, and QRVO all lowered their own forward guidance.

Overnight, Asian markets were mixed on modest moves. Taiwan (+1.14%), South Korea (+0.70%), and Malaysia (+0.29%) led the gainers. Meanwhile, Hong Kong (-0.52%), Singapore (-0.41%), and Shenzhen (0.22%) paced the losses. In Europe, the bourses lean heavily to the green side at midday. The FTSE (+0.57%), DAX (+1.29%), and CAC (+0.22%) lead the way higher while only a couple smaller exchanges show any red in early afternoon trade. As of 7:30 am, US Futures are pointing toward a very mixed open. The DIA implies a -0.42% open, the SPY implies a +0.38% open, and the QQQ implies a +1.32% gap higher at the open. At the same time, 10-year bond yields continue to fall at 3.389% and Oil (WTI) is down six-tenths of a percent to $75.98/barrel in early trading.

The major economic news events scheduled for Thursday include Weekly Initial Jobless Claims, Q4 Nonfarm Productivity, and Q4 Unit Labor Costs (all at 8:30 am), and December Factory Orders (10 am). Major earnings reports scheduled for the day include FLWS, ABB, WMS, APD, ALFVY, ATI, AME, APTV, ARCO, ARW, ABG, AVY, BALL, BCE, BCX, BERY, BMY, BR, BIP, BC, CAH, CMS, CNHI, COP, DB, LLY, EL, RACE, FCFS, HBI, HOG, HSY, HON, ITW, ICE, LANC, LAZ, LEA, MMP, MKL, MRK, NJR, PH, PENN, DGX, RCI, SBH, SNDR, SIRI, SNA, SONY, SWK, TT, GWW, WNC, and WEC before the opening bell. Then, after the close, GOOGL, AMZN, AAPL, TEAM, BSMX, BZH, BYD, CVCO, CRUS, CLX, CTSH, COLM, DECK, F, GEN, GILD, GOOG, HIG, HUBG, KMPR, LPLA, MEOH, MCHP, MTX, OTEX, POST, QCOM, RGA, SIGI, SKX, SKYW, SBUX, and X report.

In economic news later in the week, on Friday, Jan Avg. Hourly Earnings, Jan. Nonfarm Payrolls, Jan. Participation Rate, Jan. Unemployment Rate, Services PMI, and ISM Non-Mfg. PMI are reported. In terms of earnings later this week, on Friday, we hear from AON, ARCB, AVTR, SAN, BSAC, BBU, BEPC, BEP, CBOE, CHD, CI, LYB, MOG.A, NFG, REGN, SAIA, SNY, and ZBH.

So far this morning, CAH, MRK, BMY, CNHI, ABB, BBVA, EL, BDX, BCE, LEA, APTV, AWK, PH, TT, BIP, RCI, DGX, MKL, HSY, WEC, CMS, AME, RACE, DNA, HOG, SBH, FLWS, VSTO, JHG, NJR, FCFS, SXC, DLX, and IMKTA all beat on both the revenue and earnings lines. Meanwhile, SHEL, SONY, HON, TAK, LLY, IFNNY, BERY, APD, ABG, SIRI, DASTY, BC, ALFVY, BR, ATI, and WNC all missed on revenue while beating on earnings. On the other side, COP, ICE, HBI, LAZ, and GOOS beat on revenue while missing on earnings. Unfortunately, APDSKFRY, AVY, PENN, WMS, and BALL missed on both the top and bottom lines. It is worth noting that BMY, LLY, BDX, PH, TT, HSY, RACE, NJR, and WNC all raised their forward guidance. However, MRK, EL, LEA, APTV, SWK, SIRI, AVY, HBI, WMS, and GOOS all lowered their own forward guidance.

With that background and more data ahead, it looks like the recent leaders (QQQ and SPY) are going to gap up and try to take markets higher this morning. However, the mega-cap DIA is looking to gap down and is languishing inside its recent wedge, just above its T-line. The SPY is completing its golden cross (50sma cross above 200sma) this morning. A certain group of traders will see that as a great sign and will get long. So, the trend, gaps, technical signs, and two broader market indices are all bullish this morning. Perhaps it is a rotation out of the safety mega-cap names that is weighing the DIA down. Regardless, the bias is bullish, but a lot of economic data is still showing a slowing economy. So, there will continue to be some headwinds.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Tuesday’s market extension shows a massive appetite for risk as we head into another rate increase and defiance of weak economic numbers. One thing is for sure the price action and emotion are at such a fevered pitch big point moves up or down are possible, making it a hazardous environment for retail traders. Will the market be right and Powell rolls over, or do the instructions have retail traders right where they want them? We will soon find out. Protect your capital, my friends.

Asian markets posted gains across the indexes, with the tech Hong Kong exchange leading the buying. European markets trade flat to slightly bullish this morning as they wait on the Fed’s next moves. After a considerable stretch into the Tuesday close, U.S. futures point to lower open ahead of a big day of earnings and economic reports that may make or break the current buying rally. So, buckle up; the stage is set for a wild price action day!

Annual gold demand jumped 18% to 4,741 tons (excluding over-the-counter or OTC trading) across the year. That’s the largest annual figure since 2011, fueled by record fourth-quarter demand of 1,337 tons. Key to the surge was a 55-year high of 1,136 tons bought by central banks across the year.

The Federal Reserve is expected to raise interest rates by a quarter point Wednesday, its smallest increase since it began hiking rates last March. Market pros expect Fed Chair Jerome Powell to sound hawkish, meaning he will lean toward tighter policy and keeping interest rates high. “Powell is more focused on inflation going down and staying down than trying to help the S&P 500,” said one strategist. “His legacy is not going to be determined by where credit spreads are or where the S&P is going. It’s going to be determined by whether he slayed inflation and it stayed down.”

CNBC’s Jim Cramer on Tuesday told investors that the market is in bull mode, so declines represent opportunities to buy on a dip. Stocks rose on Tuesday, with the S&P 500 reaching its best January performance since 2019 on strong corporate earnings and softer-than-expected inflation data.

The appetite for risk in defiance of economic numbers heading into another Fed rate increase is astonishing as the market continues to surge. So it seems one of two things is possible over the next couple of days. First, the markets are correct; Jerome Powell rolls over, and the market rallies despite the weakness of the consumer. Or, the institutions have the retail traders right where they want them as Powell continues his inflation fight, fleecing their accounts as the market extension falls. If that is not clear enough, there is a tremendous danger for the retail trader over the next few days! Protect your capital and plan for some big point moves up or down as the drama unfolds.

Markets just on the green side of flat Tuesday. All three major indices then chopped sideways for the first 40 minutes of the day. At that point, the bulls led a modest rally for about 45 minutes. Then another sideways move (within a very tight range this time) took over until 12:20 pm when the bulls started another modest move higher most of the afternoon. However, at about 3:10 pm, the bears stepped back in to start some end-of-day profit-taking. This action gave us large, white-bodied candles, with modest upper wicks and with only the DIA having a lower wick. All three major indices are back above their T-line, the QQQ is back above its 200sma, and the DIA is back above its 50sma.

On the day, all 10 of the sectors are in the green as Basic Materials (+1.50%) leading the way higher and Communications Services (+0.15%) lagging behind the other sectors. At the same time, the SPY was up 0.81%, the DIA was up 0.53%, and QQQ was up 0.86%. Meanwhile, the VXX was down almost 2% to 11.36 and T2122 is right back up deep in the overbought territory to 97.61. 10-year bond yields are down to 3.523% and Oil (WTI) was up 1.20% to $79.08 per barrel. So, on the day, we saw some support from the T-lines as the bulls took control for the day. This all happened on light volume as the markets wait on big-name earnings and especially the Fed news on Wednesday.

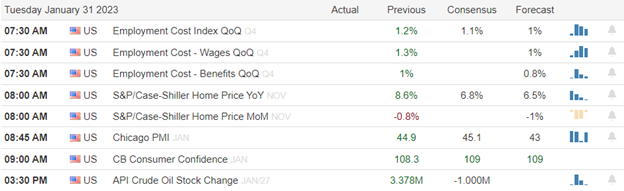

In economic news, the Q4 Employment Cost Index came in lower than expected at +1.0% (compared to a forecast of +1.1% and a Q3 value of +1.2%). This was the smallest increase in labor costs in a year and is more evidence that inflation is heading in the right direction. Later, the Chicago PMI came in worse than expected at 44.3 (versus the forecast of 45.0 and the December value of 45.1). This shows that businesses (purchasing managers), at least those in the Midwest, have a declining outlook for the economy. Then at 10 am, the Conference Board Consumer Confidence Index also came in a bit below expectation at 107.1 (compared to a forecast of 109.0 and the December reading of 109.0). This too shows a declining outlook for the economy, this one from consumers. Finally, after the close, the API Weekly Crude Oil Stocks Report came in with a huge, surprise inventory build. The report showed an inventory increase of 6.330 million barrels (versus an expected drawdown of -1.000 million barrels and following last week’s 3.378 million barrel crude oil stock build). This is just another in a string of huge inventory builds in recent weeks in the US.

In miscellaneous news, as we start a new month, we look back at a nice January in the stock market. SPY gained 6.29%, DIA gained 2.87%, and QQQ led the rally, up 10.64%. Even small-caps participated as the IWM was up 9.82% for January. In terms of sectors, Consumer Cyclical was up a whopping 15.80% with several other areas up 12-13%. Lowly Energy (+0.25% for the month) lagged the other sectors. However, all was not rosy in January as an NYSE computer system glitch prevented 250 major stocks from opening on time on January 24. This resulted in unknown losses, but the NYSE has said the claims made already are likely to exceed the pool of funds set aside to cover such losses.

In stock news, TSLA filed updated 10-K risk assessments with the SEC which now includes the risk of Elon Musk needing to sell more stock (to satisfy his other financial commitments). Elsewhere, PYPL announced it will lay off 7% of its workforce (2,000 employees) as it braces for an economic slowdown. BA delivered the last of its 747 jets to AAWW on Tuesday afternoon. The company’s replacement (the 777X) will not be ready to ship until 2025. After the close, the EU said it is now studying whether the major tech companies (GOOGL, AMZN, AAPL, META, NFLX, and MSFT) should be charged to subsidize telecom network costs. (Currently, those costs are government subsidized and implemented by Eu-based Telcos like TEF.) The reasoning is that the six major tech firms account for well more than 50% of Internet traffic. The tech giants say the idea amounts to an internet traffic tax and would violate the EU “net neutrality” rules requiring all users to be treated equally.

In stock legal and regulatory news, TSLA disclosed Tuesday that the US Dept. of Justice has sought all its internal documents related to the “Full Self-Driving” and “Autopilot” driver-assist systems. This seems to be related to a criminal investigation over claims the company made about the vehicle driving itself and deaths that resulted from drivers relying on those systems. Meanwhile, the National Labor Relations Board is issuing a complaint after its investigation found that AAPL workplace rules violate US labor law. This would just be another among several complaints pending against AAPL for anti-union actions. Further down the action chain, a US judge found AMZN guilty of illegally threatening New York warehouse workers if they voted to unionize.

After the close, AMD, DOX, AMGN, CENT, CENTA, MDLZ, OI, RNR, SYK, and SMCI all reported beats on both the revenue and earnings lines. Meanwhile, CB and UNM both beat on revenue while missing on earnings. On the other side, CP, EW, JNPR, SNAP, ASH, and HA all missed on revenue while beating on earnings. However, WDC, EA, and MTCH missed on both the top and bottom lines. It is worth noting that OI raised its forward guidance. At the same time, WDC, EA, and SNAP lowered their forward guidance.

Overnight, Asian markets leaned heavily to the upside. Shenzhen (+1.31%), Hong Kong (+1.05%), South Korea (+1.02%), and Taiwan (+1.01%) led the gains but the increases were widespread. Only Malaysia (-0.93%) and India (-0.26%) showed any red in that region. In Europe, we see a similar story taking shape at midday. The FTSE (+0.20%), DAX (+0.23%), and CAC (+0.25%) lead the way in early afternoon trade. However, the only red on the continent is Switzerland (-0.46%). As of 7:30 am, US Futures are pointing toward a modestly down start to the day. The DIA implies a -0.36% open, the SPY is implying a -0.22% open, and the QQQ implies a flat -0.04% open at this hour. At the same time, volatile 10-year bond yields are down to 3.488% while Oil (WTI) is up 0.71% to $79.43/barrel in early trading.

The major economic news events scheduled for Wednesday include ADP January Nonfarm Employment Change (8:15 am), Jan. Mfg. PMI (9:45 am), ISM Mfg. PMI and Dec. JOLTs (both at 10 am), EIA Crude Oil Inventories (10:30 am), the FOMC Rate Decision and FOMC Statement (both at 2 pm), and FED Chair Press Conference (2:30 pm). Major earnings reports scheduled for the day include MO, ABC, ATKR, BSX, EAT, GIB, EPD, EVR, FTV, GSK, HUM, IEX, JCI, MHO, NVS, ODFL, OTIS, PTON, SMG, SR, TMUS, TMO, WRK, and WM before the opening bell. Then, after the close, AFL, ALGN, ALGT, ALL, AFG, AVT, BHE, CHRW, CCS, CTVA, DXC, ENVA, GL, THG, HOLX, LSTR, LFUS, MCK, MTH, META, MET, MAA, MOD, MUSA, QRVO, RRX, TTEK, and VSTO report.

In economic news later in the week, on Thursday, we get Weekly Initial Jobless Claims, Q4 Nonfarm Productivity, Q4 Unit Labor Costs, and December Factory Orders. Finally, on Friday, Jan Avg. Hourly Earnings, Jan. Nonfarm Payrolls, Jan. Participation Rate, Jan. Unemployment Rate, Services PMI, and ISM Non-Mfg. PMI are reported.

In economic news later in the week, on Wednesday, ADP January Nonfarm Employment Change, Jan. Mfg. PMI, ISM Mfg. PMI, Dec. JOLTs, EIA Crude Oil Inventories, the FOMC Rate Decision, FOMC Statement, and FED Chair Press Conference are reported. On Thursday, we get Weekly Initial Jobless Claims, Q4 Nonfarm Productivity, Q4 Unit Labor Costs, and December Factory Orders. Finally, on Friday, Jan Avg. Hourly Earnings, Jan. Nonfarm Payrolls, Jan. Participation Rate, Jan. Unemployment Rate, Services PMI, and ISM Non-Mfg. PMI are reported.

So far this morning, ABC, GSK, TMO, MO, OTIS, GIB, EVR, EAT, ATKR, SMG, and SR have all reported beats on both the revenue and earnings lines. Meanwhile, HUM, NVS, EPD, NVO, JCI, and ODFL all missed on revenue while beating on earnings. On the other side, BSX, PTON, WM, and IEX beat on revenue while missing on earnings. However, HTHIY (Hitachi) and WRK missed on both the top and bottom lines. It is worth noting that HUM, PTON, and EAT all raised their forward guidance while none of the reporting companies lowered guidance at this point.

With that background and a heavy day of data (especially the afternoon) ahead, it looks like all three major indices are moving back toward flat in the premarket. All three remain above their T-line (8ema), although the DIA is close above. Once again the SPY is right at the point of a golden cross, with its 50sma kissing up against its 200sma. The QQQ and DIA have resistance levels just above. However, the trend remains bullish in the QQQ, SPY, and to a lesser “inside a wedge” extent in the DIA. Again, remember that 99% of futures bets are expecting a 0.25% rate hike (i.e. the market is certain it knows what the FOMC will do). That means the risk is that the Fed does something unexpected (like a 0.50% rate hike). If that were to happen, I’d expect the bears to roar into action. However, the more likely scenario is that we drift into the report and then look to continue the trend on the comfort of having known what the Fed had been signaling. Another quite possible scenario would have the FOMC do a 0.25% hike, but the statement and Fed Chair Powell both sound very hawkish to dissuade talk of a “March pause” which has been in the financial news the last couple of days. Personally, I won’t try to predict what will happen by trading one way or the other ahead of the Fed.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

Swing Trade Ideas for your consideration and watchlist: No Trade Ideas today. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

The bears relived some of the short-term overbought conditions on a light volume day as the uncertainty of what comes next inspired a bit of profit-taking as we wait for the FOMC. The selling created no technical damage, but the market appears on the cusp of a big decision. With the massive amount of pending economic and earnings data support the current bullish trend, or will it bring the bear back to work, resuming the longer-term bear trend in the SPY and QQQ? One thing is for sure were likely to see price volatility in the next few days that will challenge even the most experienced traders.

Asian markets traded modestly lower overnight, led by Hong Kong, down just 1.03%. Though a preliminary GDP report topped estimates, European markets trade lower across the board this morning. Facing a big day of earnings and economic reports on the eve of an FOMC decision, U.S. futures point to a lower open. Still, I would not expect the bulls to give up easily, so expect substantial price volatility as the data rolls out.

Preliminary Eurostat data released Tuesday showed the euro zone grew 0.1% in the fourth quarter. According to Reuters, economists had pointed to a 0.1% contraction over the same period. Energy prices cooled off in the latter part of 2022, bringing some relief to the euro zone’s broader economic performance.

Norway’s Government Pension Fund Global, among the world’s largest investors, returned -14.1% last year. “The market was impacted by war in Europe, high inflation, and rising interest rates. This negatively impacted both the equity and bond markets simultaneously, which is very unusual,” said Norges Bank Investment Management CEO Nicolai Tangen.

UBS reported $1.7 billion of net income for the fourth quarter of last year, bringing its full-year profit to $7.6 billion in 2022. “The rate environment is helping the business on one side, and that offsets some of the lower activity that we see on the investment side,” CEO Ralph Hamers told CNBC’s Geoff Cutmore Tuesday. The Swiss bank said it would purchase more shares this year.

As we approach the FOMC, uncertainty about what comes next brought some profit-taking on Monday, reliving some of the overbought conditions on another light volume day. However, the selling created no technical damage, and though the VIX registered an increase in fear, the bulls still controlled the overall trend. The intensity of market-moving reports picks up sharply today, hitting a fevered pitch by Thursday when GOOGL, AMZN, and AAPL earnings. If that’s not enough, toss in a slew of economic reports that include an FOMC rate decision and likely hawkish press conference from Powell. Plan for intraday whipsaws, overnight reversals, and fast, challenging price action to test even the most experienced trader.

Markets gapped down Monday (0.73% in the SPY, 0.34% in the DIA, and down 1.21% in the QQQ). All three major indices rallied for 45 minutes but then began a selloff that lasted the rest of the day. We closed very close to the lows. This action gave us gap-down black-bodied candles with upper wicks. It would be possible to call the SPY and DIA Inverted Hammer candles, with both of them sitting on the T-line (8ema). The DIA is also sitting on its 50sma again after the session. This all happened on average volume in the SPY and QQQ while DIA had lower-than-average volume.

On the day, nine of the 10 sectors are in the red as Technology (-2.02%) leading the way lower and Communications Services (+0.03%) holding up better than the other sectors. At the same time, the SPY was down 1.25%, the DIA was down 0.75%, and QQQ was down 2.02%. Meanwhile, the VXX was up 2.48% to 11.56 and T2122 dropped out of the overbought territory to 76.04. 10-year bond yields were up to 3.542% and Oil (WTI) was down almost 2.5% to $77.81 per barrel. So, on the day, we saw a gap-down bearish candle that closed near the lows.

In stock news, SNY has fired all employees at two vaccine manufacturing plants in India after the company failed to win a UNICEF contract. At the same time, Reuters reported that CFG cut back on auto lending last year and now plans to further reduce its exposure to this segment of the business as a risk management move. The plan is to reduce the auto loan portfolio to $5 or $6 billion (from a $14.5 billion peak). A bit later in the day, UL announced a new CEO (former Heinz exec) Hein Schumacher. Meanwhile, F announced they are cutting prices on their “Mustang Mach-E” by as much as $5,900. This follows the lead of TSLA and is the harbinger of an EV price war according to industry analysts. Not to be outdone, TSLA also announced it is now offering more new discounts and added feature incentives to entice buyers. Elsewhere, Reuters reported that BA will be adding a third production line for 737 Max planes in mid-2024. In union news, 8,200 UAL Teamster members have ratified a new two-year contract. Then, after the close, JBLU pilots also approved a two-year contract extension.

In stock legal and regulatory news, a US court has rejected the JNJ attempt to offload liability from tens of thousands of talc product lawsuits via the Chapter 11 Bankruptcy of its healthcare subsidiary. Meanwhile, in Philly, the US Third District Court of Appeals has ruled that drug manufacturers can limit healthcare providers use of outside pharmacies for dispensing drugs under a federal discount program. The ruling is a win for SNY, NVO, and AZN. At the same time, the NHTSA has hit VLVLY (Volvo) with a $130 million civil penalty after an investigation found the company failed to recall defective vehicles in a timely fashion.

In energy news, Natural Gas dropped another 6% Monday, falling to nearly a two-year low at $2.646/mmBtu. This is despite forecasts calling for East Coast temperatures below freezing this week (and nearing 10 degrees Friday). Meanwhile, Oil (WTI) fell almost 2.5% as analysts are expecting a Wednesday rate hike, which should make the Dollar stronger and therefore lower commodity prices. Another factor is that despite the European ban and the G-7 price cap, oil analysts say Russian exports remain strong.

In miscellaneous news, Bloomberg reported that last week was the first week where more than 50% of workers returned to the office across all major US cities. Meanwhile, US Treasury Sec. Yellen told an interview Monday that “persistently low inflation” is likely to return as a long-term challenge for the economy once the pandemic-era distortions are worked out. Finally, both the US and Germany said they will not be supplying fighter jets to Ukraine. However, according to LMT announced the US will continue to supply the planes to European countries (who in-turn may supply the F-16s to Ukraine). For example, Poland said Monday it was willing to supply F-16s in coordination with other European allies.

After the close, SANM, ARE, GGG, HP, and CADE all posted beats on the revenue and earnings lines. Meanwhile, WHR and PFG both missed on the revenue line while beating one the earnings line. On the other side, NXPI and WWD both beat on revenue while missing on earnings. It is worth noting that WHR and SANM both raised their forward guidance.

Overnight, Asian markets were red across the board with the sole exception of India (+0.07%) which clung to the green. Meanwhile, Taiwan (-1.48%), Hong Kong (-1.03%), and South Korea (-1.00%) led the region down. In Europe, markets are mixed but lean heavily to the downside at midday. The FTSE (-0.85%), DAX (-0.56%), and CAC (-0.53%) lead the region lower while only Russia (+0.33%) is appreciably in the green in early afternoon trade. As of 7:30 am, US Futures are pointing to a down start to the day. The DIA implies a -0.27% open, the SPY is implying a -0.30% open, and the QQQ implies a -0.44% open at this hour. At the same time, 10-year bond yields are down to 3.523% and Oil (WTI) is off 1.16% to $76.99/barrel in early trading.

So far this morning, MPC, GM, UBS, MCD, IP, PHM, GLW, DOV, AOS, LII, ST, KEX, and MSCI have all reported beats on both the revenue and earnings lines. Meanwhile, XOM, UPS, PFE, PII, MCO, and PNR missed on revenue while beating on earnings. On the other side, PSX, CAT, MPLX, OSK, and MDC all beat on revenue while missing on earnings. Unfortunately, SPOT missed on both the top and bottom lines. It is worth noting that GM, SPOT, PII, and DOV all raised their forward guidance. However, UPS, PFE, GLW, and OSK all lowered their forward guidance.

The major economic news events scheduled for Tuesday we get Q4 Employment Cost Index (8:30 am), Chicago PMI (9:45 am), Conference Board Consumer Confidence (10 am), and the API Weekly Crude Oil Stocks Report (4:30 pm). Major earnings reports scheduled for the day include AOS, CAT, GLW, DOV, XOM, GM, HUBB, IMO, IP, KEX, LII, MDC, MAN, MPC, MCD, MCO, MPLX, MSCI, NYCB, OSK, PNR, PFE, PSX, PBI, PII, PHM, ST, SPOT, SYY, UBS, and UPS before the opening bell. Then, after the close, AMD, DOX, AMGN, ASH, BXP, CP, CENT, CENTA, CB, EW, EA, HA, HLI, JNPR, MTCH, MDLZ, OI, RNR, SNAP, SYK, SMCI, UNM, and WDC report.

In economic news later in the week, on Wednesday, ADP January Nonfarm Employment Change, Jan. Mfg. PMI, ISM Mfg. PMI, Dec. JOLTs, EIA Crude Oil Inventories, the FOMC Rate Decision, FOMC Statement, and FED Chair Press Conference are reported. On Thursday, we get Weekly Initial Jobless Claims, Q4 Nonfarm Productivity, Q4 Unit Labor Costs, and December Factory Orders. Finally, on Friday, Jan Avg. Hourly Earnings, Jan. Nonfarm Payrolls, Jan. Participation Rate, Jan. Unemployment Rate, Services PMI, and ISM Non-Mfg. PMI are reported.

The main talk on financial news this morning is the fact GM blew away expectations. The company also told wall street it is expecting a stronger year in 2023 than industry analysts had been predicting. This would seem to bolster the idea of a consumer stronger than we thought in Q4 and perhaps a soft landing this year. Still, at the same time, MCD also easily beat expectations on both lines. They cited increased business in what it thinks is a sign of inflation-wary consumers opting for fast food rather than fine dining. Of course, that would point to a consumer under pressure.

With that background, it looks like all three major indices are retesting their T-line (8ema) for support during the premarket. DIA is also retesting its 50sma and the QQQ is falling further from its 200sma (which failed as support on Monday). The trend is still bullish in the QQQ and SPY. Meanwhile, the sideways meander inside a wedge continues in the DIA. Even though more than 99% of futures bets are expecting a 0.25% rate hike (i.e. the market is certain it knows what the FOMC will do), do not be surprised if we drift on lower volumes today and early on Wednesday. (There isn’t much advantage to be had “doubling down,” even when you are sure you know what will happen when everybody else in the market believes the same thing.)

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

Swing Trade Ideas for your consideration and watchlist: No Trade Ideas today. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Although there appeared to be a little profit-taking into Friday’s close, the bull’s relentless push continued struggling against index price resistance levels. Last week every selloff inspired the bulls the buy, as even disappointing earnings gaps were quickly bought up as the VIX fear gauge continued to decline. With we see more of the same with the bears stirring about this morning, perhaps window dressing the month end? Or, will bears show their teeth, relieving some of the overbought conditions with an FOMC rate hike just around the corner? We will soon find out with a huge week of earnings events to keep emotions and price volatility high!

Asian markets started Monday’s session higher but finished the day mixed, even as China’s outlook improves. European indexes only see red this morning with the uncertainty of the future of central bank rate decisions. With a week of earnings and economic calendar events U.S. points to a bearish opening as we slide into the end of a bullish January run. Plan carefully and expect some wild price gyrations this week, with earnings speculation creating the high drama.

Economic Calendar

Earnings Calendar

Notable reports for Monday include ARE, CADE, BEN, GEHC, GGG, HP, JJSF, NXPI, PHG, PCH, SOFI, & WHR.

News & Technicals’

Automobile giants Renault and Nissan have agreed to a sweeping restructure of their decades-long alliance since 1999. As part of the overhaul, Renault will transfer 28.4% of Nissan shares into a French trust.

Most Adani Group companies continued to see sharp losses for a third consecutive trading session as the company released its rebuttal on short seller firm Hindenburg’s report. Adani Enterprises’ stock price remains more than 25% lower in the month to date, Refinitiv data showed. Founder and chairman Gautam Adani’s net worth fell $27.9 billion in the year to date, according to the Bloomberg Billionaires index.

Dutch health technology company Philips said it would scrap 6,000 jobs on Monday to restore its profitability. Chief Executive Officer Roy Jakobs told CNBC it was a “necessary intervention to help us to become competitive and lean in the way we go forward in the market.” The company also says a new strategy simplified organization should improve patient safety and quality and supply chain reliability.

The bull’s relentless push continued on Friday but struggled with price resistance levels softening with perhaps some profit-taking heading into the weekend. As we finish up the last couple of days of January and move into February, expect a lot of price volatility as the pace of earnings quickens with some big tech names that can move the market. We will also face a busy economic calendar that includes an FOMC rate decision on Wednesday afternoon to keep traders and investors guessing what comes next. Unfortunately, the bears seem to be stirring this morning. Still, will the early selling continue to inspire the bulls to buy as we have experienced lately, or will the bears finally relieve some of the overbought market conditions with the uncertainty of the FOMC?

Markets diverged slightly at the open Friday with the DIA opening flat, the SPY gapping down a quarter of a percent, and the QQQ gapping down a half of a percent. From that point, we rode a roller coaster the first 90 minutes. Then the bulls stepped in to lead a steady rally in all three major indices that has lasted up to 3:30 pm. However, the bears came in as we saw a sharp selloff the last 30 minutes. This action gave us white-bodied candles with significant upper wicks in the SPY and QQQ as well as a white Doji-type candle in the DIA. The QQQ has crossed above its 200sma while the DIA bounced up off its T-line (8ema).

On the day, only four of the 10 sectors were in the green as Consumer Cyclical (+1.26%) lead the way higher and Energy (-1.23%) lagged the other sectors. At the same time, the SPY was up 0.23%, the DIA was up 0.07%, and QQQ was up 1.00%. Meanwhile, the VXX was down 1.31 to 11.30 and T2122 rose yet again and remains deep in the overbought territory at 97.15. 10-year bond yields were up to 3.509% and Oil (WTI) was down almost 2% to $79.40 per barrel. So, on the day, we saw a bullish move going into the weekend with heavy profit-taking going into the close. This all happened on less than average volume in the large-cap indices while the QQQ managed just over average volume.

In economic news, the Dec. PCE Price Index (Fed’s favorite inflation measure) came in lower than expected at +0.1% for the month and at a +5.0% year-on-year (compared to a forecast of +0.2% for the month and +5.5% y-o-y). That was the third consecutive fall in the number and the lowest annual number in over a year. December Personal Spending was also down more than was expected at -0.2% (versus a forecast of -0.1% and November’s reading of -0.1%). Both of those show slowing inflation and activity, which is what the Fed has been wanting to see. Later, Michigan Consumer Sentiment actually slightly beat expectations at 64.9 (versus a forecast of 64.6 and the December value of 59.7), showing that consumer outlooks are improving. Finally, December Pending Home Sales came in much better than expected at +2.5% (compared to a forecast of -0.9% and a November value of -2.6%).

In stock news, GS cut their CEO’s pay by 29% (to $25 million) following a down 2022. At the same time, BA announced it will be hiring 10,000 new workers in 2023 as it ramps up production. Elsewhere, the Netherlands and Japan joined President Biden’s Chinese export ban, which means ASML, NINOY, and TOELF joined the group of companies agreeing to not sell semiconductor manufacturing machinery to China. In other news, WMT and CVS both announced they are cutting the pharmacy hours at stores nationwide due to a shortage of labor. In bankruptcy news, Bloomberg reported Friday that BBBY has failed to find a buyer and is very likely headed to Chapter 11 bankruptcy. Finally, F recalled nearly half a million vehicles for rear camera display failures.

In stock legal news, on Friday, AMZN won its bid to have a 2021 lawsuit thrown out (the suit had claimed AMZN’s warehouse worker quotas were biased against older employees forcing them to be at greater risk of injury in order to meet the quotas). At the same time, Reuters reported that the SEC is now investigating Elon Musk’s role in the “self-driving” claims of TSLA. In a separate Reuters report, it was claimed that the US Dept. of Justice is again investigating V and MA related to anti-competitive debit card practices.

So far this morning, CAJ, PHG, ARLP, and SOFI have all reported beats on both the revenue and earnings lines. Meanwhile, RYAAY missed on revenue while beating on earnings. (BEN is scheduled to report at 8:30 am eastern.)

Overnight, Asian markets were mixed with Taiwan (+3.76%) as an outlier to the upside. Meanwhile, Shenzhen (+0.98%), India (+0.25%), and Japan (+0.19%) led the region higher. Hong Kong (-2.73%) was an outlier to the downside while South Korea (-1.35%), Singapore (-0.47%), and Australia (-0.16%) rounded out the area’s red exchanges. In Europe, markets are leaning heavily to the downside at midday. The FTTSE (+0.06%) is one of only three bourses that are managing any green while the DAX (-0.76%) and CAC (-0.58%) are more typical and are leading the region lower in early afternoon trade. As of 7:30 am, US Futures are pointing toward a significant gap lower to start the day. The DIA implies a -0.66% open, the SPY is implying a -0.93% open, and the QQQ implies a -1.23% open at this hour. At the same time, 10-year bond yields are up to 3.553% and Oil (WTI) is just on the red side of flat at $79.59/barrel in early trading.

There are no major economic news events scheduled for Monday. Major earnings reports scheduled for the day include ARLP, BEN, and PHG before the opening bell. Then, after the close, ARE, CADE, GGG, HP, NXPI, PFG, WHR, and WWD report.

In economic news later in the week, on Tuesday we get Q4 Employment Cost Index, Chicago PMI, Conference Board Consumer Confidence, and the API Weekly Crude Oil Stocks Report. Then Wednesday, ADP January Nonfarm Employment Change, Jan. Mfg. PMI, ISM Mfg. PMI, Dec. JOLTs, EIA Crude Oil Inventories, the FOMC Rate Decision, FOMC Statement, and FED Chair Press Conference are reported. On Thursday, we get Weekly Initial Jobless Claims, Q4 Nonfarm Productivity, Q4 Unit Labor Costs, and December Factory Orders. Finally, on Friday, Jan Avg. Hourly Earnings, Jan. Nonfarm Payrolls, Jan. Participation Rate, Jan. Unemployment Rate, Services PMI, and ISM Non-Mfg. PMI are reported.

In miscellaneous news, Sunday was the 30th anniversary of the first ETF (now called SPY), which began trading on the Amercian Stock Exchange (now NYSE-Market). It began with only $6.5 billion in assets, but now has $375 billion. It remains the largest ETF in what is now a $6.5 trillion market segment. In 2022, nearly $1 trillion was taken out of mutual funds, but at the same time $600 billion was added to ETFs.

With that background, it looks like the SPY and DIA are headed back to retest their T-lines (8ema) as support this morning. It is worth noting that the SPY is very near a “golden cross” (50sma crossing above the 200sma) which is a signal many funds and old-time traders will take heed of. And despite the gap lower at the open, the short-term trend remains bullish in all three major indices with the mid-term trend bullish in the SPY and QQQ while the DIA works in a wedge. Remember we have the Fed announcements on Wednesday and this is a heavy earnings week including many of the market’s big dogs (most active names), especially Thursday. As far as the Fed goes, almost everybody (literally 99.9% of CME Fedwatch probabilities) is expecting a 0.25% hike. While “the safety of the pack” is great, don’t forget that the risk is to the bearish side should the Fed decide to call an audible and do a bigger hike. Just be prepared.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

Swing Trade Ideas for your consideration and watchlist: No Trade Ideas today. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service