Tuesday’s early bullish hopes faded before the open, with disappointing economic numbers inspiring the bears as slowing economic conditions raise recession worries among investors. Though we have primarily tried to ignore the clues of a stressed consumer, the compounding impacts are becoming more evident as LOW adds to the chorus of retail companies uncertain about the path ahead. With the majority of 1st quarter earnings in the rearview poor economic numbers will be harder to ignore as we face another rate increase later this month. Plan for overnight reversal and significant intraday whipsaws to continue as the uncertainty grows.

While we slept, China reported a pickup in factory activity, with the tech-heavy HSI surging 4% while the ASX declined slightly. However, the European market’s trade decided bullish this morning, hoping to relieve the recent selling. With several pending and potentially market-moving economic reports and a bevy of retail earnings, U.S. futures push for a positive open, hoping to relieve the recent downturn and hold technical index supports.

Lowe’s sales in its fiscal fourth quarter fell short of Wall Street’s expectations. The home improvement retailer issued a conservative outlook as the sector comes under pressure from a shift in consumer spending.

General Motors is cutting hundreds of salaried positions as it follows other major companies, including competitors, in downsizing headcounts to preserve cash and boost profits. The cuts affect about 500 positions, according to a person familiar with the plans, announced Tuesday internally.

In November, Rivian reaffirmed its full-year guidance of an adjusted loss before income, taxes, depreciation, and amortization of $5.4 billion. For 2023, Rivian forecast vehicle production of 50,000 vehicles. That would be roughly double last year’s amount but below analysts’ expectations of around 60,000. Rivian is focusing on ramping up its R1 truck and SUV production and an electric delivery van it builds for Amazon, its largest individual shareholder.

The Tuesday pre-market pump faded before the beginning of trading as disappointing economic numbers that point to a slowing economy and an inflation-stressed consumer change their spending habits. As we kick April trading, worries of a pending recession continue to grow amongst traders and investors, breaking recent index uptrends. Still, I would not expect the bulls to give up easily, and after testing technical support, now would be the time to step up and defend. Unfortunately, they face another round of economic reports with PMI Mfg., ISM Mfg, Construction Spending, and mortgage and petroleum data. Once again, they are working to pump up the pre-market, so expect the wild intraday whipsaws to continue as the bulls and bears battle for directional control of the indexes.

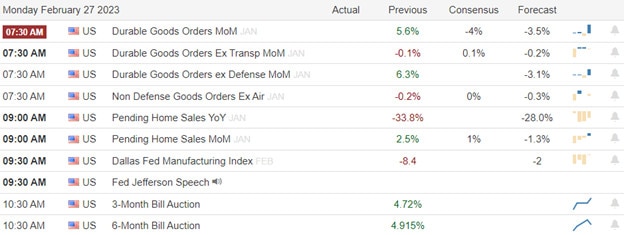

After mainly ignoring the terrible durable goods report, the bulls surged higher by more than 350 Dow points, only the quick reverse taking most of it back in a considerable intraday whipsaw. The good news is last Friday’s index lows held as support, but facing another big day of earnings and economic data on this last trading day of February, expect more of the same wild volatility. A recession seems inevitable, with slowing economic reports stacking up evidence of changing consumer habits and record credit card debt with more rate increases on the way. So, plan your risk carefully as we slide into March and the market comes to grips with the challenging path forward.

Asian markets closed mostly higher but with modest gains and losses after Japan’s factory output fell. European markets edge slightly higher this morning despite the accelerating inflation in France and Spain. U.S. futures, once again, pump higher, the premaket facing a big day of earnings and economic data, but anything is possible by the open on this last trading day of February.

A bill to revise legal protections that have shielded TikTok from U.S. sanctions is expected to pass a key House committee on Tuesday, paving the way for a broader ban on the popular short video app. Sponsored by House Foreign Affairs Committee Chairman Mike McCaul, the bill would strip longstanding protections from companies that transfer Americans’ “sensitive personal data” to entities or individuals based in, or controlled by, China. The bill would likely pass the Republican-controlled House easily. However, its fate in the Democratic majority Senate is unclear.

After the U.S. shot down an alleged Chinese spy balloon this month, China’s defense ministry declined a call with its U.S. counterpart, according to statements from both sides. Chinese culture is why, said Shen Yamei, deputy director and associate research fellow at state-backed think tank China Institute of International Studies’ department for American studies. The default U.S. view is quite different.

Ukraine President Volodymyr Zelenskyy acknowledged Monday that the situation is deteriorating around Bakhmut. Russian forces and private military contractors belonging to the Wagner Group have been trying to capture Bakhmut for months as they look to cut Ukraine’s supply lines in Donetsk. On Monday, one Russian official claimed Russian forces now controlled all roads into Bakhmut, stopping Ukrainian supplies of ammunition and forces into the city.

We kicked off the week with a considerable intraday whipsaw, but despite the bearish reversal, the bulls defended last Friday’s index lows as support. TGT squeaked out an earnings beat this morning but appeared to have the same slowing consumer concerns as HD and WMT. We not only have a big day of earnings reports but also face several economic reports, including trade, PMI, Housing prices, and Consumer Confidence. Reversal and intraday whipsaws seem likely to continue to stay focused on support and resistance levels as the big point range of price swings on the last trading day of the month.

On Monday, markets gapped higher at the open (up 0.89% in the SPY, up 0.78% in the DIA and up 1.11% in the QQQ). All three major indices then shopped sideways for just over an hour. However, at that point, a slow selloff took hold for the rest of the day with price closing not far up off the bottom in all three. This action left us with gap-up, black-bodied, indecisive Spinning Top candles in the SPY, DIA, and QQQ. All three very nearly touched their T-line (8ema) at the high of the day. In addition, the SPY closed up above its 50sma…but just barely above. This all happened on less-than-average volume in all the major indices.

On the day, eight of the 10 sectors were in the green with Consumer Cyclical (+0.79%) and Basic Materials (+0.77%) leading the way higher and Utilities (-0.50%) lagging behind the other sectors. At the same time, the SPY was up 0.34%, the DIA was up 0.29%, and QQQ was up 0.72%. The VXX fell 3.59% to 11.81 and T2122 climbed up out of the oversold territory to 39.22. 10-year bond yields fell back a bit to 3.928% and Oil (WTI) fell three-quarters of a percent to $76.75 per barrel. So, overall, Monday was a gap-up, indecisive day where the bears seemed to have more strength than the bulls after the first hour.

In economic news, January Durable Goods Orders came in below expectation at -4.5% (compared to a forecast of -4.0% and far below the December reading of +5.1%). The bulls took this as good news, probably under the theory that bad economic data may give the Fed a reason not to raise rates as much in March. However, later in the morning, January Pending Home Sales came in extremely hot at +8.1% (versus a forecast of +1.0% and a December value of +1.1%). This news may have helped the bears during the mid-morning start to the selloff. However, the staying power was not long-lived and seemed to dissipate quickly. Meanwhile, Treasury Sec. Yellen made a surprise trip to Ukraine. She called for a “fully funded and appropriately conditioned” (meaning funded by Russian asset seizures and conditioned to avoid/limit corruption) IMF bailout plan for Ukraine by the end of March. However, she did acknowledge a significant set of legal hurdles to accessing those assets being held in the US and Europe. Yellen also called for sanctions on the Russian uranium commodity, which had escaped sanctions thus far.

In stock news, PLTR announced they are cutting 2% of their workforce. (However, this only amounts to 75 jobs.) Elsewhere, car maker STLA announced it has purchased a 14.2% stake in MUX (a copper mine located in Argentina, whose largest shareholder is RIO). In other auto news, FSR told Reuters on Monday that it has increased orders for its “Ocean” sport utility EV and was on track to produce 42,400 vehicles in 2023. (The Ocean EV starts at $37,500 compared to TSLA Model Y which starts at $54,990.) At the same time, the Wall Street Journal reported PFE is in talks to buy cancer drugmaker SGEN. However, there are many hurdles for the deal to clear including a potential major antitrust review. Meanwhile, WMT, TGT, BABA, HD, LOW, COST, DLTR, IP, DOLE, and NKE are benefitting from plummeting ocean shipping prices (as the largest importers or exporters of containers). At its peak, the cost was $20,000 per TEU and now the price is $1,150. However, shipping firms (pink sheet listed) are now canceling voyages and storing containers in a frantic effort to prop up prices.

In stock legal and regulatory news, TD has agreed to pay $1.205 billion to a court-appointed receiver (who will pay back victims) related to an infamous Ponzi scheme 10 years ago. The bank avoided admitting to doing any wrong, but paid since it repeatedly ignored red flags and funneled all of Allen Stanford’s ill-gotten gains to his offshore accounts in Antigua. Elsewhere, Politico reported late Monday that the FTC is going to challenge the ICE (owner of NYSE) $13 billion deal to buy BKI. This move comes after many months of investigation of the pricing power ICE would gain in the mortgage data market. In Ohio, residents have asked a judge to block NSC from doing cleanup (destroying potential lawsuit evidence) related to the February 3 train derailment and chemical spill. This came after NSC had only allowed 2 days for the inspection of dozens of rail cars. However, NSC is also under a tight deadline due to a March 10 deadline from the EPA to clean up residues. Elsewhere, a Delaware court ruled that it will hold a hearing on April 27 regarding the conversion of APE (AMC Preferred shares) into AMC common shares. AMC soared on the news, which implies the stock may not be diluted 10-1 on March 14. (This extends the time for a long APE / Short AMC trade by 1.5 months.) Meanwhile, LYV has asked a US federal judge in CA to throw out a class action lawsuit related to the sale of Taylor Swift concert tickets. LYV claims that the ticket buyers (plaintiffs) had all repeatedly agreed to the terms of service which call for confidential arbitration. After the close, DDD agreed to pay $27 million to the US government to settle its violations of export restrictions to China.

After the close, UHS, RRC, WDAY, CAPL, ZM, HHC, MKSI, TTEC, HEI, HY, and WMK all reported beats on both the revenue and earnings lines. Meanwhile, OKE, ARKO, PRGO, TWI, PRIM, and ICUI all missed on revenue while beating on earnings. On the other side, DAR, ACHC, BMRN, and OVV all beat on revenue while also missing on the earnings line. Unfortunately, OXY and ARGO missed on both the top and bottom lines. It is worth noting that OKE and ALC both raised forward guidance. However, MKSI, TTEC, and BMRN all lowered their own forward guidance.

Overnight, Asian markets were mixed and leaned to the downside. Hong Kong (-0.79%), Taiwan (-0.71%), and India (-0.51%) paced the losses. Meanwhile, Shenzhen (+0.70%), Shanghai (+0.66%), and Australia (+0.47%) led the gainers. In Europe, we see the opposite picture at midday with most of the bourses in the green. The FTSE (-0.43%), DAX (+0.17%), and CAC (+0.13%) lead the way with all but three of the other exchanges modestly green in early afternoon trade. As of 7:30 am, US Futures are pointing toward a green start to the morning. The DIA implies a +0.32% open, the SPY is implying a +0.36% open, and the QQQ implies a +0.43% open at this hour.

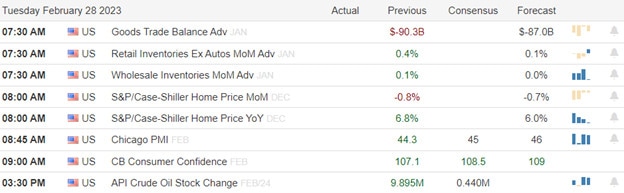

The major economic news events scheduled for Tuesday include January Trade Goods Balance and Jan. Retail Inventories (both at 8:30 am), Chicago PMI (9:45 am), Conf. Board Consumer Confidence (10 am) and API Crude Oil Stocks Report (4:30 pm). Major earnings reports scheduled for the day include AHCO, ADT, AAP, AMWD, APG, AZO, BMO, BNS, BLDR, CHS, CCO, CLOV, CBRL, DQ, DK, XRAY, IGT, SJM, JLL, KTB, NFE, NXST, NCLH, OMI, PLTK, PRVA, SRE, FOUR, TGT, VRTV, and VTNR before the opening bell. Then after the close, A, AMC, BGS, COMP, CPNG, EDR, EXPI, FSLR, FRG, GO, HPQ, ICFI, IHRT, JXN, MASI, MNST, RIVN, RKT, ROST, SKWD, SWX, URBN, VRSK, and VZIO report.

In economic news later this week, on Wednesday, Mfg. PMI, ISM Mfg. PMI, and EIA Crude Oil Inventory are reported. On Thursday, we get Q4 Nonfarm Productivity, Q4 Unit Labor Cost, and Weekly Initial Jobless Claims. Finally, on Friday, Services PMI, S&P Global Composite PMI, and ISM Non-Mfg. PMI are reported.

In terms of earnings later in the week, on Wednesday, ANF, BHG, CLVT, CLH, DLTR, DCI, DY, FWONK, HGV, HZNP, JACK, KSS, LSXMA, LOW, EYE, NIO, ODP, PBR, QRTEA, RY, SGRY, VST, WB, WEN, AAN, ADV, AGL, AEO, CANO, SQM, CODI, ERIE, GEF, JAZZ, LNW, OKTA, PFG, CRM, SNOW, SPLK, and VEEV report. On Thursday, we hear from AER, AMRX, BUD, BBY, BIG, BILI, BURL, CPG, GMS, HRL, KR, M, PDCO, SFM, STGW, TD, AVGO, COO, COST, DELL, HPE, MRVL, JWN, VVX, and VSCO. Finally, on Friday, HIBB reports.

So far this morning, TGT, BMO, AZO, AAP, APG, XRAY, IGT, KTB, PLTK, BLDR, CCO, FOUR, VTNR, and CLOV have all reported beats on both the revenue and earnings lines. Meanwhile, SRE, SJM, and NFE missed on revenue while beating on earnings. On the other side, BNS, OMI, ADT, NCLH, DORM, and FRO all beat on revenue while missing on earnings. Unfortunately, AHCO, AMWD, CHS, and DQ missed on both the top and bottom lines. It is worth noting that TGT, ADT, CHS, NCLH, and CLOV all lowered their forward guidance. However, CCO and KTB both raised their own forward guidance.

With that background, it looks like the bulls want to gap markets back up toward their T-lines (8ema) again this morning. This time, it is looking to be a less dramatic inside candle gap up. So, over-extension is not a problem either in terms of the T-line or T2122 indicator. Still, this leaves all three major indices in a downtrend. However, if they can reach yesterday’s highs again (and hold them) they will be testing that downtrend line. I see support just below (bouncing up off it in premarket) in the QQQ and SPY. However, I also see resistance just above in the DIA and probably in the SPY too. So, continue to respect trend and support and resistance. And beware of the recent tendency toward intraday reversals which might point toward a shorter/faster trade, longer/slower trade, and/or the ability to withstand the pressure (sized small enough).

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Although it was good to see the bulls defend critical moving average supports in the SPY, QQQ, and IWM, the lower highs followed by, the lower lows add some uncertainty with the mixed technical and price patterns. On the earnings calendar, we have a retail theme this week that may have been complicated by the weakening looked forward provided by HD and WMT last week. The first thing today is a potential market moving Durable Goods, with consensus estimates suggesting a substantial decline. Plan for the whipsaws and overnight reversal continues as the bulls fight to defend supports and bears line up to defend resistance levels.

Asian markets moved modestly lower during the night as they grappled with higher rates and slowing consumer activity. However, European markets want to shake off last weeks selling with a decidedly bullish bounce this morning. U.S. futures also want to bounce this morning, pushing upward in the morning pump but with the Durable Goods report pending, anything is possible by the open. Watch for whipsaws this morning.

Economic Calendar

Earnings Calendar

The earnings calendar this week has a heavy retail theme. Notable reports for Monday include AAON, ACAD, AES, DAR, FSR, FRPT, GRPN, JRVR, TREE, LI, RIDE, OSH, OXY, PNW, RRC, TTEC, UHS, WDAY, & ZM.

News & Technicals’

The two top retailers issued cautious U.S. consumer outlooks for 2023 last week. Walmart said consumer spending would start the year strong but fade. Home Depot expects revenue to be flat this year but bolstered by home equity. The retail sector had its worst week since July 2022, yet the latest inflation and retail sales data show consumer spending to be stronger than economists forecast.

Several big economies are gearing up for the mass rollout of electric vehicles. As the number of EVs on the road increases, a workforce with the knowledge to fix and properly maintain them will be needed. There are concerns, however, that a skills gap may emerge in the near future, creating a big headache for both the automotive sector and drivers.

In a joint statement Sunday, Sunak and von der Leyen said they had “agreed to continue their work in person towards shared, practical solutions for the range of complex challenges around the Protocol on Ireland and Northern Ireland.” The U.K. may have left the EU on Jan 31, 2020, but the Northern Ireland Protocol has caused persistent disagreement ever since.

Mixed technical and price patterns could make for some uncertainty as the indexes try to bounce back from last weeks selling. Though the SPY and QQQ held above critical technical supports, they also confirmed downtrends inking lower highs and lower lows in price action. We will start the week with possible market-moving Durable Goods, then begin a big week of retail earnings data. Will they also foresee the same weakening in the consumer and a slowing economy in the last half of this year, like HD and WMT? If so, it would be wise to watch downtrends, and overhead resistance levels as the bulls work to defend the bears and may entrench themselves to fight for the downtrend. So stay sharp and expect the big price swings of late to continue.

Markets gapped lower at the open Friday (down 1.29% in the SPY, down 1.14% in the DIA, and down 1.76% in the QQQ). However, at that point, Mr. Momentum seemed to take off for the weekend. After that open, all three major indices traded the rest of the day in a tight range bobbing around above and below the open. This action gave us gap-down, indecisive Doji or Spinning Top candles in all three major indices. The SPY crossed below its 50sma and then both the SPY and QQQ retested their 200sma from above…and held (at least for the day). DIA is not far above (and looks headed toward) its own 200sma.

On the day, nine of the 10 sectors were in the red as Technology (-1.89%) led the way lower and Energy (+0.13%) held up better than the other sectors. At the same time, the SPY was down 1.07%, the DIA was down 1.07%, and QQQ was down 1.67%. The VXX climbed 3.90% to 12.25 and T2122 has dropped back down just into the oversold territory at 19.66. 10-year bond yields are back up to 3.947% and Oil (WTI) rose 1.50% higher to $76.52 per barrel. So, overall, on Friday we saw a strong gap lower at the open, but then indecision the rest of the day. All this took place on a greater-than-average volume.

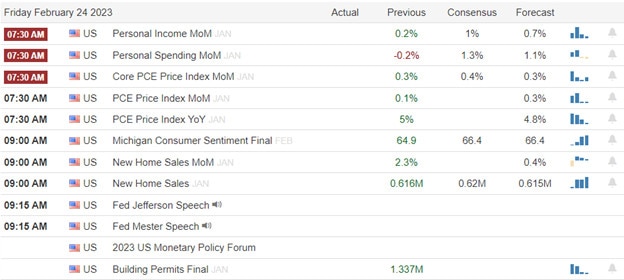

In economic news, the January PCE Price Index (the Fed’s favorite inflation indicator) came in hotter than expected at 5.4% (compared to a forecast of 5.0% and the Dec. reading of 5.3%). At the same time, January Personal Spending also came in much hotter than expected at +1.8% (versus a forecast of +1.3% and the December value of -0.1%). This was the biggest monthly gain since March 2021. Together these two readings were seen as indications that inflation may still be increasing (or at least is not falling) and the consumer is spending like crazy. Both of those are more likely to lead the Fed to tighten more and faster, raising the probability of a half percent hike in March. Hence, our gap down to start the day. Later in the morning, the Michigan Consumer Sentiment came in slightly better than forecast at 67.0 (compared to an expectation of 66.4 and decently improved from the January value of 64.9). At the same time, January New Home Sales came in significantly better than expected at 670k (versus a forecast of 620k and a December value of 625k)

In stock news, on Friday META announced its own AI named LLaMA (short for Large Language Model Meta AI). The new AI is aimed at researchers and academia and is the first step in META figuring out how it can use AI in its products. Meanwhile, Reuters reported that several more companies are cutting dividend sizes in an effort to save cash. As of Friday, these include HBI and VFC. Elsewhere, Reuters also reported on food companies culling slow-selling product lines as another way to cut expenses. These companies include KHC, CAG, UL, K, and MDLZ and will affect product selection and especially different sizes (smaller and larger quantities) of the same products available at WMT (Sam’s Club) and COST. The food companies claim it will save them billions of dollars over the year. At the same time, sources have told Bloomberg that GM has cut the production of pickup trucks due to growing inventories at dealerships and despite a continued increase in car sales this month. This implies that, while sales are good now, GM is expecting a downturn. Finally, hedge fund mgr. and major TSLA investor Ross Gerber told Reuters he was ending his bid for a TSLA board seat two weeks after his very public announcement of running for a seat in order to “reign in” Elon Musk.

In stock legal and regulatory news, the 2nd US Circuit Court rules that a tiny ($11,000) fine, which OSHA had levied on WMT for requiring pallets of boxes to be improperly stored, causing serious injury to an employee. (The multiple appeals over a minuscule fine have been an attempt by WMT to avoid liability in a lawsuit filed by the employee.) Elsewhere, WBD filed a lawsuit against PARA over the streaming rights to the animated comedy show South Park. At the same time, the US CDC hit PFE, BNTX, and MRNA when it said Friday afternoon that there isn’t enough evidence to recommend multiple annual (ongoing) COVID-19 booster shots. This comes as the government funding for such shots has or is expiring and the companies had announced major increases in the price of those vaccines. Meanwhile, GS announced Friday that it expects to incur $2.3 billion more in losses from legal proceedings during the remainder of the year. However, a CA Judge dismissed an antitrust suit that had been filed against CSGP by a rival real estate firm. After the close, MS told Reuters that it was cooperating with investigations by the US District Attorney for the Southern District of NY into block trading practices. At the same time, BLK told reporters it was cooperating in SEC investigations into electronic communications among its investment advisors (i.e. using encrypted communications to collude).

In miscellaneous news, US equity funds suffered massive outflows in the seven days ending last Wednesday. Lipper data shows investors withdrew almost $7 billion during that week. Meanwhile, Lipper data shows that investors exited US bond funds as well as they withdrew $1.67 billion during the week. Elsewhere, the US Dollar closed Friday at a seven-week high after hotter-than-expected inflation data. This came as we saw the largest weekly gain (0.6%) by the Dollar since September. On Saturday, Warren Buffett sent out his annual BRKB shareholder letter. In it, he said the company will continue to hold “a boatload of cash and treasury bonds.” He went on to report BRKB earnings were down 54% year-on-year for Q4 and down 125% year-on-year for all of 2022 (to a net loss of $22.819 billion). So, if you think you had a rough trading year in 2022, consider that BRKB reported a $53.6 billion loss from investments and derivative trades. BRKB share repurchases were down from $27 billion in 2021 to $8 billion in 2022. No new plan for 2023 was announced, but BRKB is sitting on $130 billion in cash.

Overnight, Asian markets were red across the board. Australia (-1.12%), South Korea (-0.87%), Shenzhen (-0.73%), and Taiwan (-0.71%) led the region lower. Meanwhile, in Europe, with the lone exception of Greece (-0.53%), the entire region is strongly green at midday. The FTSE (+0.77%), DAX (+1.52%), and CAC (+1.57%) are typical and lead the region higher in early afternoon trade. As of 7:30 am, US Futures are pointing toward a modest gap higher. The DIA implies a +0.43% open, the SPY is implying a +0.50% open, and the QQQ implies a +0.61% open at this hour. At the same time, 10-year bond yields have climbed to 3.959% and Oil (WTI) is down by a fraction of a percent to $76.18/barrel in early trading.

The major economic news events scheduled for Monday are limited to Jan. Durable Goods Orders (8:30 am) and January Pending Home Sales (10 am). Major earnings reports scheduled for the day include AES, BRKB, WTRG, GLP, HSC, KOP, KOS, LI, PNW, and VTRS before the opening bell. Then after the close, ACHC, ARGO, BMRN, CAPL, DAR, HEI, ICUI, MKSI, OXY, OKE, OVV, PRGO, PRIM, RRC, TWI, TTEC, UHS, WDAY, and ZM report.

In economic news later this week, on Tuesday we get Jan. Durable Goods, Jan. Retail Inventories, Chicago PMI, Conference Board Consumer Confidence and API Crude Oil Stocks Report. The Wednesday, Mfg. PMI, ISM Mfg. PMI, and EIA Crude Oil Inventory are reported. On Thursday, we get Q4 Nonfarm Productivity, Q4 Unit Labor Cost, and Weekly Initial Jobless Claims. Finally, on Friday, Services PMI, S&P Global Composite PMI, and ISM Non-Mfg. PMI are reported.

In terms of earnings later in the week, on Tuesday, we hear from AHCO, ADT, AAP, AMWD, APG, AZO, BMO, BNS, BLDR, CHS, CCO, CLOV, CBRL, DQ, DK, XRAY, IGT, SJM, JLL, KTB, NFE, NXST, NCLH, OMI, PLTK, PRVA, SRE, FOUR, TGT, VRTV, VTNR, A, AMC, BGS, COMP, CPNG, EDR, EXPI, FSLR, FRG, GO, HPQ, ICFI, IHRT, JXN, MASI, MNST, RIVN, RKT, ROST, SKWD, SWX, URBN, VRSK, and VZIO. Then Wednesday, ANF, BHG, CLVT, CLH, DLTR, DCI, DY, FWONK, HGV, HZNP, JACK, KSS, LSXMA, LOW, EYE, NIO, ODP, PBR, QRTEA, RY, SGRY, VST, WB, WEN, AAN, ADV, AGL, AEO, CANO, SQM, CODI, ERIE, GEF, JAZZ, LNW, OKTA, PFG, CRM, SNOW, SPLK, and VEEV report. On Thursday, we hear from AER, AMRX, BUD, BBY, BIG, BILI, BURL, CPG, GMS, HRL, KR, M, PDCO, SFM, STGW, TD, AVGO, COO, COST, DELL, HPE, MRVL, JWN, VVX, and VSCO. Finally, on Friday, HIBB reports.

So far this morning, AES, KOS, HSC, and NE all reported beats on both the revenue and earnings lines. At the same time, VTRS missed on revenue while beating on the earnings line. On the other side, WTRG beat on the revenue line while missing on earnings. Unfortunately, LI missed on both the top and bottom lines. It is worth noting that HSC has also lowered forward guidance.

With that background, it looks like the bulls want to gap markets back up toward their T-lines (8ema) this morning. (At least prior to the durable good number.) Still, this leaves all three major indices basically in a downtrend although the premarket price is getting close to challenging the downtrend line (but certainly not starting a new uptrend at this point). Extension is not a problem either in terms of T2122 or the T-line. It looks like the bulls are trying to get back above a potential support level that was tested and appeared to fail Friday. Also, keep in mind that the norm recently has been to see large intraday swings. So, be prepared to weather such a whipsaw or look to shorter or longer trade horizons to handle that problem.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Thursday left more questions than answers with another whipsaw day, some hopeful hammer patterns just ahead of the Fed’s favored inflation number expected to rise according to consensus. To keep traders guessing, we will follow that up with New Home Sales, Consumer Sentiment, and more Fed jaw-wagging. Buckle up today’s data could encourage the bulls to defend support or inspire the bear to keep attacking as we head into the uncertainty of the weekend. Big price moves are possible, so plan carefully with critical technical and price levels in the index charts at stake.

Asian markets traded mixed during the night even as Japan’s inflation reached a 41-year high. European markets mixed, though cautiously waiting for market-moving economic reports. The hope hammer patterns of Thursday look to reverse with a gap down, showing ahead of the Personal Incomes and Outlay number that could change everything by the opening bell. Plan for big point moves as the reaction may determine who wins the battle to hold or break critical support levels.

Economic Calendar

Earnings Calendar

We have a much lighter day on the Friday earnings calendar. Notable reports include BRC, CRI, GTLS, CNK, LAMR, SSSP, TBLA, & SLCA.

News & Technicals’

Block stock rose in extended trading after the payments company reported fourth-quarter revenue and gross profit that beat Wall Street’s expectations. The company posted a (non-adjusted) net loss of $114 million, or 19 cents per share, for the quarter.

According to Fidelity’s analysis, retirement account balances in 401(k) plans lost nearly one-quarter of their value in 2022. In addition, amid ongoing high inflation and economic uncertainty, nearly half of the retirees expect to outlive their savings.

Warner Bros. Discovery reported fourth-quarter revenue that missed analysts’ estimates as the media industry contends with a soft advertising market. However, the company, which owns HBO Max and Discovery+ streaming services, said its global direct-to-consumer streaming subscriber base increased by 1.1 million during the quarter. In addition, more “Lord of the Rings” movies are on the way, CEO David Zaslav said.

Fueled by NVDA earnings, the bulls tried to resume the upside rally in the day, but the attempt quickly faded into another whipsaw day that left behind some hopeful hammer patterns and yet more questions than answers. Interestingly yesterday’s volume spike was huge, and VIX registered a substantial decline in fear despite the big ship in price. This morning it’s all about the Personal Incomes and Outlays report, the Fed’s favored reading on inflation. The result is likely to set the direction for the day and determine if the bulls will resume directional control of the market or if the bears will gain the upper hand heading into the weekend. Plan for a bumpy ride with New Home Sales, Consumer Sentiment, and more Fed speak to keep traders on edge.

Whipsaw was the word of the day on Wednesday as we gapped higher at the open (up 0.68% in the SPY, up 0.46% in the DIA, and up 1.26% in the QQQ). Then, after 25 minutes of finding their feet, the bears stepped in to drive a strong selloff that took all three major indices to the lows of the day (which was down 0.6% from the prior close) at noon. From there, the bulls stepped in to lead a long, slow, steady rally that got us back to the opening level by 3:30 pm. Finally, the last 30 minutes saw more selling in all three indices of note. This action gave us black-bodied, indecisive, Spinning Top candles in the SPY and DIA as well as a black-bodied Hammer candle in the QQQ. All three major indices remain below their T-line (8ema), but are close enough now that there is no question of over-extension at this point.

On the day, six of the 10 sectors were in the green as Energy (+1.78%) led the way higher (by eight-tenths of a percent) and Communication Services (-0.71%) lagged the other sectors. At the same time, the SPY was up 0.53%, the DIA was up 0.35%, and QQQ was up 0.87%. The VXX fell 3.52% to 11.79 and T2122 has climbed back into the mid-range at 45.40. 10-year bond yields fell again, this time to 3.888% and Oil (WTI) jumped 2.27% higher to $75.63 per barrel. So, overall, we saw a back-and-forth day where we gapped up, faded the gap and continued the same distance lower, and then reversed course again to end up just below where we opened. If that doesn’t say “INDECISION,” then I don’t know what does. All this took place on a greater-than-average volume, in fact, much larger-than-average in the DIA.

In economic news, the second estimate of Q4 Gross Domestic Product came in lower than expected at +2.7% (compared to a forecast of +2.9% and the Q3 final reading of +3.2%). This gave bulls the energy to gap higher at the open on the theory that slower Q4 growth will tell the Fed their measures are working and they can go with a smaller hike during their March meeting. At the same time, the second estimate of the Q4 GDP Price Index came in above expectation at +3.9% (versus the forecast of +3.5% but still improved from the Q3 value of +4.4%). Meanwhile, Weekly Initial Jobless Claims came in lower than expected at 192k (compared to a forecast of 200k and even slightly down from the prior week’s 195k number). Again, this all pointed to a goldilocks scenario in the bulls’ eyes. GDP was falling, but still growing, inflation was trending in the right direction, and yet fewer than expected jobs are being lost. To bulls, this suggests an economy that is not in serious trouble and a Fed policy that is still doing the job.

In stock news, BA announced it will stop production of its F/A-18 fighter jet in 2025. BA said this will free up resources to focus on winning the race to build the pentagon’s 6th generation fighter contract and building the MQ-25 autonomous refueling tanker. (LMT and NOC are also competing for the sixth-generation fighter contract.) Meanwhile, HUM announced it will exit the employer-based insurance business entirely to focus on government-backed programs such as Medicare and direct-to-individual insurance like medicare supplement insurance. Later, NEM said it sees significant value created for its shareholders in a deal and is in talks to buy NCMGF. Several of NEM’s competitors have said they are not interested in NCMGF, but the company still rejected NEM’s initial bid (which NEM said it is open to sweetening). Elsewhere, NFLX said Thursday that it has cut the prices of its subscription plans in some countries in order to boost the number of subscribers. The Wall Street Journal reported those cuts were in countries in sub-Saharan Africa, Latin America, the Middle East, and Asia.

In stock legal and regulatory news, NVS agreed to pay $30 million to healthcare plans and consumers to settle claims that it schemed to delay the US launch of generic drugs that would compete with its name-brand Exforge hypertension drug. This was part of a broader $245 million settlement. Meanwhile, a federal judge in Detroit moved more toward SBUX and dealt a blow to the NRLB ruling against the company. The judge narrowed his previous “cease and desist” order barring the company from firing pro-union employees. Originally, the order applied nationwide, but the just has now narrowed this to only cover a single store (in essence allowing SBUX to fire any pro-union employees elsewhere). This is critical since 280 SBUX stores have unionized in the last two years out of 9,000 US locations. Elsewhere, after the close, the FAA reported that BA has halted the delivery of 787 Dreamliner jets while it investigates a fuselage component. (BA has not delivered a 787 since January 26 and there is no timeline available for the resumption.) Finally, the US Dept. of Justice has asked a federal judge to sanction GOOGL after it claimed the company destroyed evidence by deleting internal corporate communications that had been subpoenaed as part of its antitrust case against GOOGL (related to internet search business).

In energy news, the EIA Weekly Crude oil Inventories saw stockpiles grow for the ninth-straight week. The report showed an inventory build of 7.648-million-barrels (compared to a forecast of a 2.083-million-barrel build). Crude inventories have grown by over 60 million barrels so far in 2023. In addition, refineries operated at 85.9% capacity over the week, down slightly from the prior week and well below the 90% average capacity for this time of year. Meanwhile, due to the reduced refining, the week saw a drawdown of gasoline inventories by 1.856-million-barrels (versus the forecast of a 0.108-million-barrel build and far less than the prior week’s 2.317-million-barrel build). However, distillate (diesel and heating oil) inventories rose by 2.698 million barrels (compared to a forecast of a drawdown of 1.126 million barrels and the prior week’s drawdown of 1.285 million barrels).

In miscellaneous news, the USDA released its forecast calling for a 26.8% fall in egg prices during 2023. The primary factor was that the agency is not seeing a rebound in bird flu after massive culling efforts in 2022. Meanwhile, a group of Republican states has filed suit against the SEC, challenging the SEC requirements that investment funds reveal how they vote on shareholder ballots (like pay packages). In the crypto space, the SEC and NY State’s top financial regulator both opposed Binance buying bankrupt crypto lender Voyager. Both announced the grounds for their opposition is the ”unregistered offer and sale of securities,” which essentially declares crypto to be a security and is just another step in government opposition to cryptocurrencies. Finally, the Biden Administration announced it will nominate former MA exec Ajay Banga to head the World Bank.

After the close, INTU, BKNG, MELI, ADSK, VICI, LYV, CHE, SWN, RHP, CWK, KWR, LUNMF, ACA, FTCH, SATS, EIX, and OPEN all reported beats on both the revenue and earnings lines. Meanwhile, FND, PRI, BWXT, INT, CENX, and ZEUS all missed on the revenue line while beating on earnings. On the other side, SQ, PBA, ASR, SEM, ATSG, and SPNT all beat on revenue while missing on earnings. Unfortunately, WBD, CE, BECN, OII, CVNA, and ACCO missed on both the top and bottom lines. It is worth noting that CE, FND, ACCO, and ATSG lowered their forward guidance. However, CHE and OII both raised their forward guidance.

Overnight, Asian markets were mostly in the red. Japan (+1.29%) and South Korea (+0.53%) were the only appreciable green in the region. Meanwhile, Hong Kong (-1.68%), Thailand (-1.12%), and Shenzhen (-0.81%) led the rest of the region lower. In Europe, we see a similar picture taking shape at midday. The FTSE (+0.21%) is among the handful of green bourses while the DAX (-0.60%) and CAC (-0.57%) are more typical and lead the region lower in early afternoon trade. As of 7:30 am, US Futures are pointing toward a gap lower to start the day. The DIA implies a -0.57% open, the SPY is implying a -0.63% open, and the QQQ implies a -0.90% open at this hour. At the same time, 10-year bond yields are up to 3.912% again and Oil (WTI) is up a half of a percent to $75.80/barrel in early trading.

The major economic news events scheduled for Friday include the January PCE Price Index and January Personal Spending (both at 8:30 am), Michigan Consumer Sentiment and January New Home Sales (both at 10 am). Fed member (non-voting, hawk) Mester also speaks at 10:15 am. The major earnings reports scheduled for the day include CM, GTLS, CNK, EOG, EVRG, FMX, FYBR, GTN, DINO, IEP, and LAMR before the opening bell. Then after the close, CRC reports.

So far this morning, FYBR, EVRG, CRI, GTN, and PNM have all reported beats on both the revenue and earnings lines. Meanwhile, CM, LAMR, and GTLS have missed on revenue while beating on earnings. On the other side, CNK and DINO both beat on revenue while missing on earnings. There are no major reports that have reported misses on both lines. (FMX, IEP, and SSP report closer to the open.) It is worth noting that CRI has lowered its forward guidance.

One year into the Russian War of Expansion against Ukraine, the war drags. The Russians continue to be willing to take hundreds of thousands of casualties (by most estimates more than 100,000 dead). On the other side, the West (and the US in particular) seems only willing Ukraine enough military aid to check the Russians. (As opposed to decisively throwing them out such that they will not come back after regrouping.) In terms of the business impacts go, according to US News and World Reports, these are the biggest losses. PM generated 8% of its revenue from Russia and Ukraine prior to the war and that has taken a hefty hit. PEP was generating 4.4% of total revenue from those two countries prior to the 2022 invasion. MCD lost 4.2% of its revenue and also took a significant haircut on the assets it sold at fire sale prices to exit Russia. Less obvious losers are MHK (which lost 4.3% of its revenue which came from Russia and Ukraine), EPAM (which used to generate 4% of revenue from the two countries, CCL (which previously got 3.5% of its revenue from Russia and Ukraine), PVH (lost 3.6% of its revenue), and WAB (which lost 3.5% of its revenue from those two countries). The biggest corporate winners from the war are LMT, RTX, NOC, and GD, all of which have received new multi-billion dollar orders for everything from Javelin missiles (LMT), to HIMARS rocket systems (LMT), to Stinger missiles (RTX), to Stryker fighting vehicles (GD), to Abrams tanks (GD), to heavy-caliber ammunition (GD), to drones (AVAV).

With that background, it looks like the bears want to gap markets back lower in all three major indices. Still, this leaves all three major indices basically in a consolidation area of the recent downtrend. (At least at the current premarket prices.) Extension is not a problem either in terms of T2122 or the T-line. We’re sitting at a potential support level at the moment. However, all three major indices also face resistance just above after the last few days. The trend remains bearish in the short term while the basic character of the market has been “chop and thrash back-and-forth” in recent weeks. Yesterday, in particular, was a whipsaw day on the intraday chart. So, continue to show some caution and remember that it’s Friday (payday). So, lock in some profits where you can and prepare your account for the weekend news cycle.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

On Wednesday, markets opened just on the green side of flat. All three major indices say 20 minutes of modest rally followed by 45 minutes of a slightly stronger selloff. However, at 10:40 am, a slow, steady rally took over the market that eventually took us to new highs by 2 pm. Unfortunately, after buying the rumor all morning, traders sold the news after the Fed Minutes release. This selloff took us back down to new lows by 3 pm where we stayed until a bounce that last 15 minutes. This action is giving us black-bodied, indecisive Spinning Top candles in the SPY, DIA, and QQQ.

On the day, six of the 10 sectors were in the red as Energy (-0.60%) led the way lower and Consumer Cyclical (+0.50%) held up better than the other sectors. At the same time, the SPY was down 0.12%, the DIA was down 0.22%, and QQQ was up 0.07%. The VXX fell 2.86% to 12.22 and T2122 has climbed but remains well into the oversold territory at 13.72. 10-year bond yields have fallen slightly to 3.916% and Oil (WTI) is down 3.23% to $73.89 per barrel. So, we saw a “wait and see” open (despite good earnings reports) and then a slow, but steady rally into the Fed Minutes. However, at that point, we sold off to take all three major indices out near the lows. All this took place on a little below-average volume.

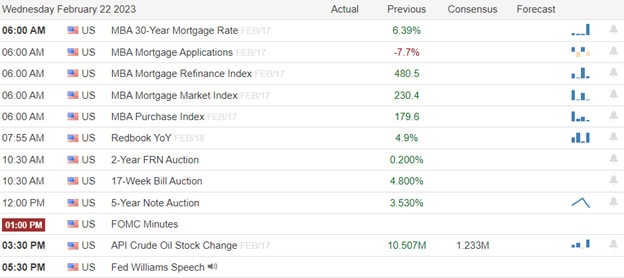

In economic news, the FOMC Minutes from the Feb 1 meeting was the only show in town Wednesday. As mentioned, their release moved markets lower, despite us not learning anything we didn’t know before the release. All participants expressed that they welcomed the signs of moderating inflation leading up to the meeting. However, the sentiment that “substantially more evidence of progress on inflation” would be required before they were confident inflation was on a downward path toward 2%. The vast majority favored a 25-basis-point hike (which is what they announced). However, three members (including non-voters uber-hawk Bullard and Mester) were in favor of a continuation of 50-basis-point hikes (or at least said they could support a 0.50% hike). We knew those two had been in favor of a 50-basis-point hike prior to the minutes because they flat-out told us as much last week. With that said, the minutes also gave us a clue that there was concern over financial stability, both from increasing rates too quickly and potentially from the upcoming Federal Debt Ceiling showdown. The most heated exchanges were related to the risk of recession with a few attendees seeing an “increased likelihood” of recession while the majority pointed to the labor market which has remained hot implying that businesses still see demand and are working to hold onto or in some cases increase their number of employees and also pointed to excess savings, even noting that some local governments have “sizable budget surpluses.”

In stock news, Reuters reported that the CEO of MKC told them during an interview that the company is seeing pushback from retailers on price increases for its products. Specifically, WMT and KR (two largest grocery chains) were mentioned as fighting any increase in prices. Elsewhere, Reuters also reported that CMCSA took advantage of the recent “AI craze” to sell more than 11 million shares of BZFD so far in the month of February. This came after BZFD has announced it was partnering with OpenAI on ads. Later, Bloomberg reported that AAPL has made a breakthrough in non-invasive (no blood sample) glucose monitoring. This would allow the phone maker to compete with current blood or prick required solutions from ABT, PODD, DXCM, and TNDM. At the same time, INTC announced a cut to its dividend by 65% (to the lowest level since 2007) in an effort to save cash. INTC has been losing ground to AMD in key markets, had many delayed and mediocre product launches in the last year and is currently facing the worst semiconductor market in a decade coming off the boom pandemic years of high sales and higher prices. Meanwhile, after the close, TM announced it has accepted union demands for the largest base salary wage hike in 20 years as well as an increase in bonuses. Shortly after the TM announcement, HMC said it also has agreed to a deal with unions. However, the HMC deal was only for a 5% pay increase. Finally, in early evening, GOOGL told “cloud employees and contractors” that they will be sharing desks (on alternate days) in order reduce real estate costs at its five largest locations. Workers will be in-office two days per week (Monday/Wednesday or Tuesday/Thursday) which is actually down from the currently required 3 days in-office. There was no word on the amount of expected savings or whether the workers will be 33% more productive on their two days in-office.

In stock legal and regulatory news, CRL shares plunged Wednesday after news broke that the company was subpoenaed by the US Justice Dept. in relation investigations of Cambodian supplier of monkeys for research. At the same time, AMZN completed its purchase of One Medical (primary care provider) a day after receiving FTC approval for the deal. Elsewhere, the US Supreme Court ruled that HLX is liable to pay overtime for an oil rig supervisor who earns $200k per year. The 6-3 majority ruled the person was being paid at a daily rate of $963 and was not on salary. The ruling could have serious implications for corporations employing non-contract staff. Meanwhile, NSC made several announcements Wednesday that it will take responsibility for the cleanup (as had been ordered Tuesday by the EPA. After the close, the CDC advisory panel recommended a BVNRY monkeypox vaccine be approved for use in all adults at risk. Such recommendations usually lead quickly to approval and if approved this would give BVNRY an advantage over EBS whose smallpox vaccine was competing for that market but which causes severe side effects. Finally, in non-specific corporate news, the NLRB ruled that laid-off workers cannot be required to sign confidentiality or any other (non-compete) agreements that could deter them from exercising their rights to find other employment as a condition for receiving severance pay. This overturned a pair of Trump-era rulings that had made non-compete and confidentiality contracts a valid condition for receiving severance.

In energy news, after the close the API Weekly Crude Stocks Report came out. This week saw another very large and unexpected rise in stocks. The report said crude oil inventories grew 9.895 million barrels (compared to a forecast of a 1.233-million-barrel build and following on the heels of the prior week’s 10.507-million-barrel build). The report also saw a 0.894-million-barrel build in gasoline inventories as well as a 1.374-million-barrel increase in distillate (diesel and heating oil) stocks. This report followed a day when crude prices fell 3.3% on fears of upcoming Fed rate hikes and a weakening of the China rebound. In addition, the Fed minutes also supported a strengthening dollar which rose against sterling, the yen and euro. (A stronger dollar reduces the price of nearly all dollar-denominated commodities.)

After the close, NVDA, PXD, EBAY, APA, CTRA, PARR, FIX, PDCE, RXT, ANSS, MYRG, CCRN, TDOC, PK, RUN, EXR, COKE, KALU, ICLR, VMI, OGS, STN, SUI, and SM all reported beats on both the revenue and earnings lines. Meanwhile, DVA, NTAP, CAKE, CDE, DVA, GSM, WES, and UCTT reported misses on revenue while beating on earnings. On the other side, MOS, OPAD, ETSY, CPE, CHDN, CHRD, BTG, DOOR, RYI, and PR all beat on revenue while also missing on earnings. Unfortunately, ATUS, SNBR, FNF, VAC, MATV, and OUT missed on both the top and bottom lines. It is worth noting that RYI raised its forward guidance. However, NTAP, VAC, OPAD, RXT, UCTT, and SUI all lowered their forward guidance.

Overnight, Asian markets were mostly in the red. Taiwan (+1.28%) and South Korea (+0.80%) were strong but the only green in the region. However, Japan (-1.34%) and Singapore (-1.06%) led the region lower with the rest of the exchanges down less than half of a percent. Meanwhile, in Europe, the regional bourses are mostly green at midday. FTSE (-0.18%) is one of three exchanges in the red while the DAX (+0.63%) and CAC (+0.48%) lead the region higher in early afternoon trade. As of 7:30 am, US Futures are pointing toward a gap higher to start the day. The DIA implies a +0.30% open, the SPY is implying a +0.54% open, and the QQQ implies a +1.00% open at this hour. At the same time, 10-year bond yields are back up to 3.947% and Oil (WTI) is up 1% to $74.75/barrel in early trading.

The major economic news events scheduled for Thursday includes Q4 GDP, Q4 GDP Price Index, and Weekly Initial Jobless Claims (all at 8:30 am), and EIA Crude Oil Inventories (11 am). The major earnings reports scheduled for the day include BABA, AMR, AEP, AMT, HOUS, AMBP, AAWW, BBWI, BHC, CBRE, CQP, LNG, COMM, DPZ, DTE, EME, AG, FCN, GPC, GFI, IRM, KDP, LKQ, MRNA, MODV, NTES, NEM, NICE, NOMD, OPCH, PZZA, PCG, PRMW, PWR, RCII, SPTN, SRCL, FTI, TFX, BLD, TAC, VIPS, W, and YETI before the opening bell. Then after the close, ACCO, ATSG, ACA, ADSK, BALY, BECN, SQ, BKNG, BWXT, CVNA, CE, CGAU, CENX, CHE, CWK, EIX, ERIE, FTCH, FND, INTU, LYV, MTZ, MELI, OII, ZEUS, OPEN, PBA, PRI, RHP, SEM, SWN, VICI, WBD, and INT report.

So far this morning, BABA, LYG, GPC, PWR, BBWI, AMT, BLD, SHOO, MODV, DTE, AEP, CQP, EME, RCII, OPCH, FCN, PZZA, and SATS all reported beats on both the revenue and earnings lines. Meanwhile, CBRE, VIPS, DISH, ARKAY, COMM, DPZ, IRM, TFX, OGE, PCG, and NICE all missed on revenue while beating on earnings. On the other side, KDP, W, FTI, NEM, SPTN, NOMD, and GRAB have reported beats on revenue while missing on the earnings line. Unfortunately, MRNA, NTES, LKQ, and PRMW have reported misses on both the top and bottom lines. It is worth noting that VIPS, GPC, PWR, IRM, BLD, and GRAB have all raised their forward guidance. However, BBWI, SPTN, RCII, and NOMD lowered their forward guidance.

In economic news later this week, on Friday, the January PCE Price Index, January Personal Spending, Michigan Consumer Sentiment, and January New Home Sales are reported. In terms of earnings later in the week, on Friday, we hear from CM, GTLS, CNK, EOG, EVRG, FMX, FYBR, GTN, DINO, IEP, LAMR, and CRC.

In late-breaking news, Elon Musk met with CA Governor Newsom Wednesday. As a result, the new TSLA Engineering Headquarters will be built in CA instead of in TX where the company Headquarters were moved in 2021 (in tax abatement wrangling). Meanwhile, NY Fed President (and voter) Williams toed the company line last night. In his evening presentation, he said it was important that the Fed remain committed to its 2% inflation goal. (He did not speak to the most recent data, what he thinks would be the appropriate next hike, or where he sees the terminal Fed Funds rate reaching.) At the same time, a PIMCO subsidiary has defaulted on $1.7 billion in mortgage loans. An industry analyst claims the value of the commercial properties (nationwide) covered by those loans had fallen 20% since the start of the pandemic in 2020. Finally, he CME Fed Watch Tool shows that fewer traders are betting on a quarter-point hike in March now. Still, the futures imply a 73% chance of a quarter-point hike with the odds of a half-point hike rising to 27%.

With that background, it looks like the bulls want to gap markets higher (back toward the T-line) in all three major indices. This is especially true in the QQQ when most of the T-line extension will be eliminated IF we open where premarkets sit now. All three major indices also have potential support levels not too far below. However, they also face resistance just above after the last few days of losses. The trend remains bearish in the short term while the basic character of the market has been “chop and thrash back-and-forth” in recent weeks. So, continue to show some caution.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

The Tuesday selloff was overdue, and although a bit painful, it was finally a recognition of the inflation and the resulting pressure the consumer is dealing with in putting groceries on the table. As a result, the indexes experienced some price action damage-breaking trends and current support levels, but only the DIA suffered the technical damage of breaking its 50-day average. Today we have a big round of earnings with the FOMC minutes later to provide some potential price volatility. However, traders will quickly turn their attention to the Thursday GDP report, and the Feds favored PCE number on Friday.

Asian markets followed the U.S., selling off across the board overnight as New Zealand hiked rates to a 14-year high. European markets also feel some selling pressure this morning, pulling back after recording recent record highs. With earnings results rolling out, the U.S. futures suggest a flat to slightly bearish open with last month’s FOMC minutes release later this afternoon. Expect the wild price swings to continue as the bulls and bears fight for control.

The maker of Jeep and Dodge, Stellantis, post a record annual profit. The company also announced a 4.2 billion euro dividend payout to shareholders, equating to 1.34 euros per share, subject to shareholder approval. At the same time, the board approved a share buyback of 1.5 billion euros to be executed by the end of 2023.

Amazon employees continued to sound off Tuesday night over the company’s recently announced return-to-office mandate. A group of staffers spammed an internal website with comments expressing anger over the policy. An internal Slack channel showed concerns about parenting, caregiving, and commuting.

Sweden’s Foreign Minister Tobias Billström told CNBC Sweden, and Finland’s NATO membership was “just a matter of time,” with negotiations with ratification holdout Turkey set to resume. Billström said Sweden had “worked to fulfill everything” it agreed to in a memorandum of understanding between the countries last summer, and Swedish membership at the NATO summit in July was the goal. Sweden requested to join the military alliance after 200 years of non-alignment due to the Russian invasion of Ukraine. But it is embroiled in a long-running dispute with Turkey, which holds veto power.

Though yesterday’s selling may have been a bit painful, it was way overdue and an acknowledgment that rates are likely to rise to add pressure to an already stressed consumer. Technically there was some damage to the DIA breaking below its 50-day average. Still, the Tuesday decline reduced the overextended conditions in the SPY, QQQ, and IWM, only suffering from the break of support levels in price action. Today we have a busy earnings calendar while we wait for the FOMC minutes that could provide some price volatility at the end of the day. However, traders will quickly focus on the Thursday GDP report and the Friday PCE numbers. Remember, one day does not make a trend, so it will be interesting to see if the bears have the energy to follow through with a downside push to test the 50-day averages in the SPY, QQQ, and IWM. I would not expect the bulls to give up quickly, so expect the wild price swings to continue as the battle for control continues.

Markets were disappointed in lowered forward guidance from both WMT and HD on Tuesday. This caused a gap lower at the open (down 1.02% in the SPY, down 1.05% in the DIA, and down 1.30% in the QQQ). After 15 minutes of fading the gap (tempting the dip buyers), the bears took over for a long, slow selloff that lasted until 2:30 pm. At that point, prices ground sideways in a tight range near the low for the last 90 minutes of the day. This action gave us gap-down, big-bodied, black candles with little to no lower wick in all three major indices. All three are well below their T-line (8ema) with the DIA crossing down through its 50sma and SPY coming down close above its own 50sma by the close.

On the day, all 10 sectors were in the red as Consumer Cyclical Energy (-3.30%) led the way lower and Consumer Defensive (-0.65%) held up better than the other sectors. At the same time, the SPY was down 2.01%, the DIA was down 2.08%, and QQQ was down 2.37%. The VXX spiked higher by 7.8% to 12.58 and T2122 plummeted deep into the oversold territory at 7.52. 10-year bond yields spiked hard to 3.954% and Oil (WTI) is down fractionally to $76.05 per barrel. So, on the day, we saw a gap lower, a small bull trap, and then an all-day selloff on average volume (just greater than average in the SPY, and just below average in the DIA and QQQ).

In economic news, the Manufacturing PMI came in slightly above expectation at 47.8 (compared to a forecast of 47.1 and the January reading of 46.9). At the same time, the Services PMI came in above forecast too at 50.5 (versus the expected 47.2 and the January reading of 46.8). Meanwhile, the S&P Global Composite PMI beat the expectations too at 50.2 (compared to a forecast of 47.5 and a January value of 46.8). It is worth noting that any of these PMI reading above 50.0 indicates economic growth while numbers below 50 indicate contraction. Later in the morning, January Existing Home Sales came in below expectations at -0.7% (versus a forecast of +2.0% but still better than the December reading of -2.2%). This drop was the 12th straight monthly decline and also reached the lowest level (annually-adjusted 4.000 million units) in 12 years.

In stock news, TSLA announced it has paused some plans to produce entire batteries in Germany and will instead carry out some of the steps in the US to take advantage of new US tax incentives. Meanwhile, MSFT announced it will offer its PC games to the NVDA cloud gaming service. This is seen as a move to appease critics of the MSFT acquisition of ATVI, as one of the grounds was that the AVTI game franchise “Call of Duty” would only be available via XBOX. The deal with NVDA ensures Call of Duty will be available via XBOX, PCs, Macs, Chromebooks, Smartphones, and tablets. At the same time, HSBC announced that it has cut the employee annual bonus pool by 4% to $3.4 billion, citing a global slump in demand for bankers to finance M&A deals. Still, in the same release, HSBC also raised its CEOs pay by 14% to $6.7 million. Then, after the close, Reuters reported that T is looking to sell its cybersecurity division in an attempt to pay down debt that it has lumbered under since the $108.7 billion purchase of Time Warner (which it has since sold) in 2018. In similar news, C announced after the close that it has raised its CEO pay to $24.5 million (a 9% hike). Finally, AMZN is facing major pushback on its decision to force employees to return to the office as of May 1. Overnight, more than 5,000 employees signed a petition pushing CEO Jazzy to drop the return to office mandate. This came in addition, to thousands of internal office Slack system spam messages deriding the decision.

In stock legal and regulatory news, the EPA ordered NSC to clean up contaminated soil and water at the site of its East Palestine OH derailment wreck in early February. It also ordered the company to send representatives to every public meeting with local residents after the company skipped the most recent one, citing fear for the safety of company employees. Elsewhere, Swiss Financial Regulators are reviewing remarks made by the Chairman of CS. Chairman Lehmann apparently told a Financial Times interview that the “outflows from the company (by customers) stabilized by December 1 (time of interview),” going as far as to say they had “flattened out” and partially reversed”. However, the Swiss Regulator noted that customer outflows continued before, during, and after that interview. Meanwhile, AMC shareholders (led by a public employee retirement system) have sued the company over issuing new shares without shareholder consent, in violation of state law. Finally, the Biden Administration will not veto the US International Trade Commission ban on the US import of AAPL watches for infringing on patents owned by Alivecor. (This refusal to veto is normal as Presidential vetoes of ITC rulings are rare.)

In energy news, CHK sold 2,300 wells and 172,000 acres of drilling rights (a portion of its Eagle Ford basin holdings) for $1.4 billion. The deal is expected to close during Q2 2023. Meanwhile, the March front-month Natural Gas future closed down again (another 7.8%) to $2.057/mmBtu (another 2.5-year low). Analysts see minor support at $1.98/mmBtu, but below that prices are said to be likely to fall to $1.80/mmBtu. This comes as another couple of days of uncommonly warm weather is forecast for the Ohio Valley region and Mid-Atlantic states. Finally, the International Energy Agency (IEA) said Tuesday that the oil and gas industry could slash global methane emissions by 75% with an investment of just 3% of the industry’s 2022 income. The energy sector is the source of 40% of methane emissions and the reason this is important is that methane has 85 times more warming effect than CO2. Major oil companies have not (yet?) made a reply to the announcement.

After the close, CHK, CZR, CVI, FANG, AGR, TOL, PANW, MATX, KEYS, PSA, FLS, O, BKD, SBAC, LZB, IAA, WSC, CSGP, ALIT, and EXAS all beat on both the revenue and earnings lines. Meanwhile, COIN, CWH, GFL, CW, and IOSP all missed on the revenue line while beating on earnings. On the other side, UFPI, BXC, ESI, and MTDR beat on the revenue line while missing on earnings. Unfortunately, BCC, RIG, and UNVR missed on both the top and bottom lines. It is worth noting that PANW, SBAC, and EXAS raised their forward guidance. However, PSA, O, and CSGP have lowered their forward guidance.

Overnight, Asian markets were red across the board. South Korea (-1.68%), India (-1.53%), and Japan (-1.34%) led the region lower. Meanwhile, in Europe, we see the same picture taking shape at midday. The European bellwethers FTSE (-1.15%), DAX (-0.73%), and CAC (-0.89%) are leading the continent lower even as several of the smaller exchanges have larger losses in early afternoon trade. As of 7:30 am, US Futures are pointing toward a flat start to the day. The DIA implies a +0.04% open, the SPY is implying a -0.01% open, and the QQQ implies a +0.02% open at this hour. At the same time, 10-year bond yields are down a bit to 3.935% and Oil (WTI) is off 0.85% to $75.74/barrel in early trading.

The major economic news events scheduled for Wednesday is limited to the February FOMC Minutes (2 pm), the API Weekly Crude Oil Stock Report (4:30 pm) and Fed member Williams speaks (6:30 pm). The major earnings reports scheduled for the day include ALLE, BIDU, BLCO, BCO, CRL, CSTM, CRVN, GRMN, GIL, IBP, IQ, NI, OSTK, PRG, SBGI, TRGP, TJX, TNL, UTHR, VRT, and WWW, before the opening bell. Then after the close, ATUS, ANSS, APA, BTG, CPE, CAKE, CHRD, CDE, FIX, CTRA, CCRN, DVA, EBAY, ETSY, EXR, GSM, FNF, ICLR, LBTYA, VAC, DOOR, MATV, MOS, MYRG, NTAP, NVDA, OPAD, OGS, OUT, PAGS, PARR, PK, PDCE, PXD, PR, RXT, RIO, RYI, SNBR, SM, STN, SUI, RUN, TDOC, VMI, and WES report.

In economic news later this week, on Thursday, we get Q4 GSP, Q4 GDP Price Index, Weekly Initial Jobless Claims, and EIA Crude Oil Inventories. Finally, on Friday, the January PCE Price Index, January Personal Spending, Michigan Consumer Sentiment, and January New Home Sales are reported.

In terms of earnings later in the week, on Thursday, BABA, AMR, AEP, AMT, HOUS, AMBP, AAWW, BBWI, BHC, CBRE, CQP, LNG, COMM, DPZ, DTE, EME, AG, FCN, GPC, GFI, IRM, KDP, LKQ, MRNA, MODV, NTES, NEM, NICE, NOMD, OPCH, PZZA, PCG, PRMW, PWR, RCII, SPTN, SRCL, FTI, TFX, BLD, TAC, VIPS, W, YETI, ACCO, ATSG, ACA, ADSK, BALY, BECN, SQ, BKNG, BWXT, CVNA, CE, CGAU, CENX, CHE, CWK, EIX, ERIE, FTCH, FND, INTU, LYV, MTZ, MELI, OII, ZEUS, OPEN, PBA, PRI, RHP, SEM, SWN, VICI, WBD, and INT report. Finally, on Friday, we hear from CM, GTLS, CNK, EOG, EVRG, FMX, FYBR, GTN, DINO, IEP, LAMR, and CRC.

So far this morning, BIDU, NI, IQ, BCO, CRL, ALLE, FDP, GEL, QUAD, and PRG all reported beats on the revenue and earnings lines. Meanwhile, GRMN and TNL missed on revenue while beating on earnings. Unfortunately, CSTM, VRT, GIL, WWW, OSTK, UTHR, and DRVN all missed on both the top and bottom lines. It’s worth noting that VRT and ALLE both raised their forward guidance. However, GRMN and CRL both lowered their forward guidance. (TJX, TRGP, AGESY, IBP, and STLA all report later in the morning.)

With that background, it looks like the bulls have pushed premarket prices up off the lows and are now looking to gap higher by between a quarter and a half of a percent. If this holds into the morning, it will help with the extension (which was not “terrible” anyway) below the T-line (8ema) among the three major indices. However, T2122 still shows us well inside the oversold reversal zone. The Fed Minutes are the big news of the day, but it seems unlikely that we will hear anything that we don’t know already (hikes will continue with a preference to stay at a quarter percent hike…remember, the meeting took place before the hot January Payrolls and CPI reports came out). As of this morning, we still have 79% of the Fed Futures bets on a quarter-percent hike while 21% are looking for a half-percent hike in March. All three major indices also have potential support levels not too far below. However, the trend (and momentum as of Tuesday) are bearish in the short term while the basic character of the market has been “chop and thrash back-and-forth” in recent weeks. So, continue to show some caution.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service