Not only will investors have a full plate of earnings reports to grapple with this week, but they will also have a huge week of economic data such as CPI, PPI, and retail sales, keeping them guessing and uncertain. Although the DIA seems stuck in consolidation, the SPY, QQQ, and IWM remain in bullish patterns. Big point index swings are possible this week, and I would not rule out significant intraday whips or overnight reversals to challenge us in the week ahead. All eyes will be on Tuesday morning’s BLS sessional adjustments to the CPI number, so plan your risk carefully as we wait.

Asian markets started the week mostly lower with a volatile yen as uncertainty increases on the BOJ nomination report. However, European markets trade with modest bullishness this morning, trying to gauge monetary policy ahead of crucial economic data. While off overnight lows, U.S. futures suggest a flat, mixed open as they wait on a market-moving CPI report Tuesday morning.

According to NBC News, the U.S. military shot down a fourth unidentified object Sunday and expects to recover it. The White House on Friday announced a second object had been shot down over Alaska, and Canadian Prime Minister Justin Trudeau said Saturday a U.S. fighter jet shot down a third “unidentified object.” Officials have yet to release details about the objects that were downed on Friday, Saturday, and Sunday.

U.K. semiconductor bosses are pleading with the government for subsidies amid fears that some chip firms will be forced to move overseas. The U.S. and EU have announced multibillion-dollar packages to boost domestic chip production, and industry executives worry that the lack of a similar strategy from the U.K. is harming the country’s competitiveness. Prime Minister Rishi Sunak’s administration is under pressure to publish its planned chip strategy, which has faced delays due to political instability.

Life Insurance Corporation, India’s largest insurer, said it ‘might’ review its stake in the embattled Adani Group after meeting with the management. LIC chairman M.R. Kumar said the state-owned insurer plans to discuss with the Adani management soon to get a better picture of the crisis engulfing the conglomerate. “As an investor, it’s not often that we have this kind of a situation. But then we have reached out to the management of Adani,” Kumar told CNBC’s Tanvir Gill in an interview.

The modest profit-taking of last week underscores the uncertainty investors face this week we readings on CPI, PPI, and Retail Sales numbers. Nevertheless, having relieved much of the overbought condition, the SPY, QQQ, and IWM remain in bullish patterns, with the DIA seminally stuck in consolidation. The seasonal adjustments from the BLS will have all eyes on the Tuesday CPI report setting up a morning of considerable price volatility. However, as we wait, don’t be surprised to see a choppy, low-volume price action today. All the economic data will, of course, be complicated with another big of economic data to keep traders guessing and emotions high. Plan carefully and prepare for some big point index swings with the possibility that the overnight reversals experienced last week may continue as the data rolls out.

Markets opened modestly lower Friday (down 0.31% on the SPY, down 0.09% in the DIA, and down 0.70% in the QQQ) well up off the premarket lows. From that point, we had a bit of divergence as the SPY roller-coastered its way sideways, the DIA had a very modest uptrend, and QQQ put in a volatile bearish trend. However, during the afternoon all three synced up and trended modestly bullish the rest of the day. This action gave us gap-down indecisive Doji candle in the QQQ and gap-down white-bodied candles in the two large-cap indices. All three remain close below their T-line (8ema) and the DIA has held above its 50sma after another retest.

On the day, seven of 10 sectors are in the green as Energy (+3.43%) led the way higher and Consumer Cyclical (-1.27%) lagged behind the other sectors. At the same time, the SPY was up 0.23%, the DIA was up 0.49%, and QQQ was down 0.66%. At the same time, the VXX gained 1.25% to 12.18 and T2122 rose but remains in the midrange at 47.75. 10-year bond yields spiked up to 3.745% and Oil (WTI) is up by 2.23% to $79.80 per barrel. So, on the day, we saw a gap lower and then indecisive action the rest of the day. All of this happened on less-than-average volume again.

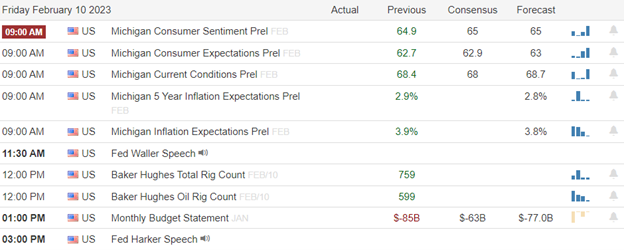

In economic news, the Michigan Consumer Sentiment Index came above expectations a bit at 66.4 (compared to a forecast of 65.0 and the January reading of 64.9). Later in the day, the January Federal Budget Balance came in much better than expected at -$39.0 billion (a deficit, versus the forecast of -$63.0 billion and also much better than the December reading of -85.0 billion). After the close, Philly Fed President Harker said that the strong January Payrolls Report has not changed his view that moving to small (quarter percent) rate hikes was the correct strategy for the FOMC. Specifically, Harker (a voting member this year) said, “At this point, we can go at a pace of 25 (basis-point rate hikes) and get inflation under control without doing undue damage to the labor market.” He also added that moving to smaller rate increases is a “risk management” issue for the Fed. Finally, he opened the door to rate cuts in 2024. On that topic, he said, “I don’t think that’ll happen this year,” but in 2024 “we could start to see movement downward in the federal funds rate that is likely to be gradual.”

In stock news, TSLA reversed course in China by raising prices that it just recently cut. Later, the US Army announced Friday that OSK had lost a $7 billion contract for a tactical vehicle. At the same time, MGA warned about profits in 2023 citing margin pressure from US automakers. Along those same lines, WMT publicly warned vendors (companies that sell products through WMT stores) that it can no longer take price hikes and will be pushing their own private-label products more as less-expensive alternatives. This is normal business for WMT, but it is not common for the company to make public proclamations on the topic. This move could impact the likes of PG, UL, KHC, CPB, KMB, CLX, and PEP (who all see billions of dollars of products through WMT). Meanwhile, F announced it had cut its stake in EV company RIVN from 11.4% to 1.15% as part of a predetermined plan. Elsewhere, Florida Governor DeSantis gained effective control over the board which oversees the DIS special district surrounding DIS theme parks. I won’t go into the background, but the move cost Florida taxpayers about $1.2 billion and may cause DIS trouble related to its Florida theme park unit. After the close Friday, F announced a new $3.5 billion battery plant to be built in Michigan as part of a joint venture with a Chinese battery company. Elsewhere, HOOD won a dismissal of an investor lawsuit claiming the company had misled investors ahead of its 2021 IPO. Finally, Reuters reported that FIS is preparing to break up its business, spinning off the payment processing unit it had acquired four years ago for $43 billion.

In miscellaneous news, on Saturday, Indian Finance Minister Sitharaman said that G-20 countries are exploring collective regulation on cryptocurrencies. No timetable or specifics were offered, but Sitharaman said the discussions are active. At the same time, Reuters reported that META is not releasing departmental budgets internally as the company plans another round of layoffs. Meanwhile, major TSLA investor Ross Gerber has launched a campaign to gain a seat on the company board. His agenda is to reign in Elon Musk (addressing spending too much time on other companies, not having succession plans, and his stock sales). Oddly, Gerber launched his bid on a Twitter Spaces call. He said “I’ve kind of had enough…TSLA needs to build its image around Tesla, and not just Elon. I think it’s time for TSLA to grow up.” Finally, the balloon story won’t seem to go away as three more (much smaller and more likely weather-related according to analysts guesses) balloons were shot down Friday, Saturday, and Sunday in the ocean off Alaska, over Canada, and over the US side of Lake Huron respectively). Meanwhile, China says that US balloons crossed its own airspace 10 times during 2022. So, that talk will continue.

In energy news, for the first time in eight weeks, Natural Gas gained ground. The front-month Natty rose 4.3% for the week to close at $2.5140/mmBtu. At the close of the week, US gas storage stood at 2.366 trillion cubic feet, which is up 10.9% from one year ago. Elsewhere, CVX said Friday that it has agreed to sell its assets in Myanmar and will exit that country. Meanwhile, Bloomberg reports that XOM is quietly walking away from a decade-long project intended to create environmentally-friendly biofuels from algae. XOM had already invested $350 million in the project. At the same time, the US Treasury Dept. said that it had warned countries and companies located in Turkey and UAE that the US will start cracking down on the facilitators who are helping Russia avoid Western oil sanctions. Finally, on Saturday, a meeting was held to discuss conditions at the Freeport Texas LNG export facility that was idled by an explosion and fire last June. Area residents are complaining that regulators are not providing enough oversight and control over the facility as it moves toward coming back online. (When fully operational, the facility processes 2 billion cubic feet of natural gas per day and is the largest LNG export facility in the US.)

Overnight, Asian markets were mixed but leaned to the downside. Singapore (-1.07%), Japan (-0.88%), and South Korea (-0.69%) lead the larger number of exchanges lower. Meanwhile, Shenzhen (+1.14%) and Shanghai (+0.72%) were the only appreciable gainers on the day. In Europe, stocks are mostly in the green at midday. The FTSE +0.40%), DAX (+0.43%), and CAC (+0.86%) lead all but two exchanges to the upside in early afternoon trade. As of 7:30 am, US Futures are pointing toward a green start to the week. The DIA implies a +0.15% open, the SPY is implying a +0.35% open, and the QQQ implies a +0.66% open at this hour. At the same time, 10-year bond yields are flat a 3.74%, and Oil (WTI) is also flat at $79.74/barrel in early trade.

There are no major economic news events scheduled for Monday. Major earnings reports scheduled for the day include CX, CHKP, DDL, and THS before the opening bell. Then after the close, ASTL, AMKR, ACGL, ANET, CAR, CDNS, ES, FE, IAC, MKSI, MRC, PLTR, and SEDG report.

In economic news later this week, on Tuesday, we get January CPI and the API Weekly Crude Oil Stock Report and we also get a Fed speaker (Williams). Then on Wednesday, NY Fed Empire State Mfg. Index, January Retail Sales, January Industrial Production, December Business Inventories, December Retail Inventories, and EIA Weekly Crude Oil Inventories are reported. On Thursday, we get January Building Permits, January PPI, January Housing Starts, Weekly Initial Jobless Claims, Philly Fed Mfg. Index, and a couple of Fed speakers (Mester, Bullard, and Mester). Finally, on Friday, January Import Price Index and January Export Price Index are reported.

In terms of earnings later in the week, on Tuesday we hear from CAE, CLF, KO, ECL, ENTG, EXC, FELE, GTX, GEO, GFS, HRI, HWM, LCII, LDOS, MAR, BTU, PKI, QSR, TRU, WCC, ZTS, ABNB, AKAM, ANDE, CLW, CRK, CNDT, DVN, WIRE, ENLC, GDDY, GXO, HLF, MCY, NU, SCI, SU, TX, and WFG. Then Wednesday, ADI, AVNT, GOLD, BIIB, CHEF, FIS, GNRC, ICL, KHC, LAD, MLM, OC, PSN, RPRX, RBLX, R, SABR, SITE, SAH, SUN, TMHC, TTD, WAB, WAT, ALB, ALSN, AMED, AEE, AIG, AWK, AR, CF, CSCO, SYH, CPA, ET, EQT, EQIX, HST, INVH, KGC, MRO, NEX, NUS, NTR, QDEL, RSG, REZI, RNG, ROKU, ROL, RGLD, RUSHA, SGEN, SHOP, SUM, SPWR, SNPS, TNET, TROX, TWLO, WCN, WELL, and Z report. On Thursday, we hear from ARCH, BLMN, CVE, CEG, CROX, CNB, ETR, EPAM, FOCS, GGR, GVA, HAS, HSIC, H KBR, KELYA, LH, NSRGY, NGD, NMRK, DNOW, NRG, OGN, PARA, PBF, POOL, POR, RCM, RS, STNG, SO, SCL, SYNH, TOST, USFD, VC, VNT, VMC, WSO, WST, WE, ZBRA, AEM, AL, AEL, COLD, AMN, AMAT, ATR, BIO, BFAM, ED, CLR, DASH, DKNG, DBX, FBIN, GLOB, IAG, TDS, TXRH, USM, and VALE. Finally, on Friday, ASIX, AMCX, AXL, AN, CNP, CRBG, DE, MD, and PPL report.

So far this morning, FIS, CHKP, and TDC have reported beats on the revenue and earnings lines. Meanwhile, THS and DDL both reported a miss on revenue while they beat on the earnings line. (CX has not reported yet.) It is worth noting that FIS and THS both lowered forward guidance. However, TDC raised its forward guidance.

With that background, it looks like the bulls are taking all three major indices back up to retest their T-line (8ema) from below this morning. However, neither the SPY or QQQ is to the point of retesting the Bull Flag downtrend they are in (at least in premarket). bears have the momentum coming off yesterday’s candle and with an overnight assist from the Russians. We do have another big earnings week with KO and KHC headlining that group. However, the big driver is likely to be CPI data on Tuesday. Do not be surprised if we drift today as traders wait on that report before betting big this week. The risk remains to the downside as markets are betting on a pause in hikes by the Fed (not March, but soon), inflation to keep coming down, AND the economy to hold up (no hard landing).

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

The daily index swings continued Thursday, but this time produced a big intraday whipsaw leaving behind some possible topping candle patterns. The price action suggests the bears are hungry, but I would not expect the bull to give up easily. The VIX hinted at some fear of returning to the market as it popped through a multi-month downtrend yesterday. The question for the day is, will the bears find the energy to follow through, or will the bulls rush back to defend? With this week’s significant daily reversals, I think anything is possible as we head into the weekend.

Asian markets closed the day mostly lower, with the tech-heavy HSI leading the way, down 2,01%. European markets trade decidedly bearish this morning as investors mull future central bank actions and the possibility of a recession. U.S. futures point to a lower open ahead of earnings, consumer sentiment, and more Fed speakers.

Economic Calendar

Earnings Calendar

We get a little break on the earnings calendar on Friday. Notable reports include AXL, ENB, FTS, IQV, NWL, SPB & WPC.

News & Technicals’

Adidas could lose around 1.2 billion euros ($1.3 billion) in revenue in 2023 if it cannot sell its existing Yeezy stock. Shares of Adidas were down 11% around 9 a.m. London time following the news. “The numbers speak for themselves. But, unfortunately, we are currently not performing as we should,” Adidas CEO Bjørn Gulden said in a press release.

Yahoo will lay off more than 20% of staff, or around 1,600 workers, and the company’s Yahoo for Business unit will be slashed in half. The company said about 1,000 of those cuts would occur by the end of the week.

Dan Schulman became PayPal CEO after the company split from eBay in 2015. He will remain a member of PayPal’s board of directors. “I’m proud of what we have accomplished at PayPal and of the incredibly talented and committed people I work with every day,” Schulman said in a statement.

The wild chop continued on Thursday, tossing traders a big intraday whipsaw and leaving behind bearish engulfing candles with the VIX breaking a multi-month downtrend. That said, one day does not make a trend, and though the bears made an appearance, will they have the energy to follow through? Don’t expect the bulls to give up easily, and with the big point swings we have experienced this week, we can’t rule out another quick swing higher. We have more Fed speakers, consumer sentiment, a treasury statement, and a lighter day of earnings reports to provide inspiration. Keep an eye on price support levels because if they break, some quick selling to occur as traders rush to protect profits.

Markets gapped higher on Thursday (up 0.93% in the SPY, up 0.68% in the SIA, and up 1.51% in the QQQ). However, this was a bull trap as the bear immediately stepped in and sold off the market steadily all day long. Price had completely faded the gap in all three major indices by 12:30 pm and then continued its way South. Only a little bit of profit-taking by the bears during the last 25 minutes prevented us from going out on the lows. This action gave us black-bodied candles that engulfed Wednesday’s candle body. (However, these are not Bearish Engulfing signals because Wednesday’s candle bodies were also black.) All three major indices crossed back below their T-line.

On the day, all 10 sectors are in the red as Communications Services (-1.34%) led the way lower and Consumer Defensive (-0.41%) held up better than other sectors. At the same time, the SPY was down 0.87%, the DIA was down 0.69%, and QQQ was down 0.88%. At the same time, the VXX gained 3.00% to 12.01 and T2122 fell again to the bottom end of the midrange at 26.78. 10-year bond yields jumped up again to 3.667% and Oil (WTI) is down by 1.06% to $77.64 per barrel. So, on the day, we saw a bull trap where the overnight gap was met with an all-day selloff. Still, the bears did not break out of the decisive move. So, the bullish trend remains unbroken. All of this happened on less than average volume.

In economic news, the Weekly Initial Jobless Claims came in just above expectations at 196k (compared to a forecast of 190k but still an increase from the previous week’s reading of 183k). Meanwhile, the Continuing Jobless Claims were also higher than was forecasted at 1,688k (versus a forecast of 1,658k and well up from last week’s value of 1.650k). In Fed speak, Richmond Fed President Barkin said Thursday that tight monetary policy is “unequivocally slowing the US economy” which will allow the Fed to be “more deliberate” in any further interest rate increases. Barkin went further than most Fed speakers by saying that, “We all know what people care about. They care about food, gas, and shelter.” He went on to say that he is watching those three things as his indicator of when inflation is under control. Until they are, he said the FOMC has more work to do (implying more quarter-point hikes ahead).

In stock news, GM and GFS announced a long-term deal to secure US-made chips for GM vehicles. The deal will enable the carmaker to avoid the chip shortages that have plagued the auto industry since the start of the pandemic. In layoff news, GTLB has announced it will reduce its workforce by 7% due to the current economic environment. Meanwhile, pot company CGC announced it will cut 36% of employees and sell assets in Canada in an effort to reduce costs. The company cited black market competition as a significant hurdle. Elsewhere, after the close, BKI announced it will put its loan software business up for sale. The move is part of BKIs attempt to stem antitrust concerns after ICE’s proposed acquisition of BKI. Meanwhile, XOM announced it will be merging some business units as part of a cost-cutting plan (despite blowout record profits in its most recent report). The Wall Street Journal reported that the move was aimed at reducing a layer of management and concentrating the smaller units buying power and decision-making related to raw materials procurement.

In miscellaneous news, Thursday evening the Fed announced its 2023 bank stress test scenarios. This year’s test will include a new “extra market shock” in addition to various recession scenarios. The tests must be passed by the eight largest US banks, namely JPM, BAC, C, WFC, USB, PNC, MS, and GS. Elsewhere, Labor Sec Walsh and President Biden’s Top Economic Advisor Deese have both called executives of CSX, UNP, NSC, and BRKA’s BNSF railroads. The Administration officials pushed the companies to offer paid sick leave to rail workers represented by the 10 unions whose members are currently not offered any. Finally, after the close, technology industry research firm Mercury Research released a report on the state of the processor market. Overall, 2022 saw the worst downturn in the PC chip market since the 1980s. INTC got crushed, losing market share to competitor AMD (which now has nearly one-third of the processor market). AAPL and QCOM (both using chips from ARM) lost market share over the year as well.

In energy news, the front-month March contract for Natural Gas closed down again Thursday, settling at $2.43/mmBtu. This was up off the day’s low of $2.351 after a larger than expected inventory draw was reported by the EIA. A down US Dollar also helped all commodities on the day. Elsewhere, Russia announced plans to cut its oil production by 500,000 barrels per day as of March to Western price caps. This cut amounts to 5% of Russia’s daily oil output. This news has both oil prices spiking 2% and European stock markets lower this morning.

After the close, MSI, G, MTD, VTR, TEX, CBT, LGF.A, and DXCM all reported beats on both the revenue and earnings lines. Meanwhile, PYPL, MHK, NGL, BHF, FLO, and EQR all missed on revenue while beating on earnings. On the other side, CC, LYFT, USX, MODG, and OSCR all beat on revenue while missing on earnings. Unfortunately, NWSA, EXPE, YELL, and CNXN all missed on both the opt and bottom lines. It is worth noting that PYPL, MSI, MTD, and MODG all raised their forward guidance. However, MHK, CC, VTR, and LYFT lowered their forward guidance.

Overnight, Asian markets leaned to the red side. Hong Kong (-2.01%) was an outlier while Australia (-0.76%), Shenzhen (-0.59%), and South Korea (-0.48%) led the losses. Meanwhile, Malaysia (+0.68%), New Zealand (+0.50%), and Japan (+0.31%) paced the gains. In Europe, again with the sole exception of Norway (+0.19%), we see red across the board at midday. The FTSE (-0.71%), DAX (-1.49%), and CAC (-1.28%) are leading the continent lower in early afternoon trade. As of 7:30 am, US Futures are pointing toward a gap lower to start the day. The DIA implies a -0.47% open, the SPY is implying a -0.73% open, and the QQQ implies a -1.23% open at this hour. At the same time, 10-year bond yields are climbing again to 3.711% and Oil (WTI) is up 2% to $79.64/barrel in early trading.

The major economic news events scheduled for Friday are limited to the Michigan Consumer Sentiment (10 am) and January Federal Budget Balance (2 pm) reports. We also hear from Fed members Waller (12:30 pm) and Harker (4 pm). Major earnings reports scheduled for the day include ENB, FTS, GPN, HMC, IQV, MGA, NWL, SPB, and SLVM before the opening bell. There are no major reports scheduled for after the close.

So far this morning, NWL, GPN, TIGO, and FTS have reported beats on the revenue and earnings lines. Meanwhile, ENB and MGA both reported beats on the revenue line while missing on the earnings line. On the other side, IQV and HMC missed on the revenue line while beating on the earnings line. Unfortunately, SLVM and SPB missed on both the top and bottom lines. It is worth noting that MGA raised guidance while IQV and NWL both lowered forward guidance.

With that background, it looks like the bears have the momentum coming off yesterday’s candle and with an overnight assist from the Russians. As markets prepare for the weekend, all three major indices are showing a bearish trend overnight that has flattened out after 6:15 am. This will give us that gap lower at the open unless something changes dramatically in the next two hours. This will break the uptrend line in the QQQ and move us close to retesting that uptrend line in the SPY. DIA is back inside its wedge but still has more ground to cover before retesting its own uptrend line. (When I say uptrend lines, I’m talking about those dating back to the start of the year.) Earnings were generally good last night but are more mixed this morning. So, it may be up to Consumer SEntiment and Fed Speak to turn things around if you’re a bull.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

The theme of this week looks to continue as Thursday is shaping up for another overnight reversal of direction as earnings speculation drives the index price swings. While the DIA has chopped in a significant point consolidation, the SPY, QQQ, and IWM remain in an extended condition. Today we have a reading on Jobless Claims and another big day of reports, so expect more volatile price action as we slide toward the end of the week.

Asian markets concerned about future rate increases traded mixed overnight with modest gains and losses. However, European markets see only green this morning as earnings results drive trading, with economic conditions taking a backseat. With earnings and Jobless claims, the U.S. futures point to a bullish open to once again reverse the previous trading day.

Disney said it would reorganize into three divisions: Entertainment, ESPN, and parks and experiences. Disney will slash 7,000 jobs from its workforce and plans to cut $5.5 billion in costs, including $3 billion in content savings. CEO Bob Iger said the company isn’t considering a spinoff of ESPN.

PepsiCo’s fourth-quarter earnings and revenue topped Wall Street’s estimates. The food and beverage giant’s price hikes to mitigate inflation buoyed sales for snacks and drinks, but the strategy has also hurt demand. Nevertheless, looking to 2023, Pepsi is projecting a 6% increase in organic revenue and 8% growth in its core constant currency earnings per share.

The Credit Suisse quarterly result was worse than analyst projections of a net loss attributable to shareholders of 1.32 billion Swiss francs. It took the embattled Swiss lender’s full-year loss to 7.3 billion Swiss francs. Credit Suisse in October announced a plan to simplify and transform its business in an effort to return to stable profitability following chronic underperformance in its investment bank and a litany of risk and compliance failures.

Every day this week has begun with an overnight reversal of direction, and it looks as if Thursday is shaping up to follow the same pattern. SPY, QQQ, and IWM charts remain extended, while the DIA has primarily consolidated in a substantial point range. Both volume levels and the VIX also have flip-flopped daily while earnings speculation and uncertainty drive the volatility. Today we have another big round of earnings reports and the Fed inflation nemesis, the strong jobs sector, as we wait for the weekly claims reading. Expect the whippy price action week to continue, so plan your risk carefully.

Markets gapped modestly lower on Wednesday (down 0.48% in the SPY, down 0.33% in the DIA, and down 0.47% in the QQQ). All three major indices took the first hour to find their footing and then a selloff began at about 10:30 am and lasted until about 11:45 am. However, at that point, the bears took a rest and all three indices just meandered sideways along the bottom of their range the rest of the day. This action gave us black-bodied Bearish Harami candles in the QQQ, SPY, and DIA with the latter two being more indecisive (Spinning Top type candles). All three indices have held their T-lines (8ema) as support so far.

On the day, all 10 sectors are in the red as Technology (-1.79%) led the way lower and Communication Services (-0.20%) held up better than other sectors. At the same time, the SPY was down 1.10%, the DIA was down 0.61%, and QQQ was down 1.78%. At the same time, the VXX has shot up 3.74% to 11.66 and T2122 fell back out of the overbought territory and into the midrange at 66.30. 10-year bond yields are down to 3.625% and Oil (WTI) is up by 1.63% to $78.40 per barrel. So, on the day, we saw an indecisive bearish leaning inside day, but support may be holding and there was not a ton of strength shown by the bears.

In economic news, EIA Weekly Crude Oil Inventories came in just a bit below expected at 2.423 million barrels (compared to a forecast of 2.457 million barrels and last week’s +4.140 million barrels). That was the only data. However, there were several Fed speakers. For example, Fed Governor Cook told an audience that the strong January Jobs Report coupled with moderating Wage Growth has increased the chances of a soft landing. Elsewhere, NY Fed President Williams told a Wall Street Journal event that financial conditions are roughly in line with what the FOMC wants to see, but “we still have work to do (on raising rates).” He went on to say “Moving to a federal funds rate of between 5.00% and 5.25% “seems a very reasonable view of what we’ll need to do this year in order to get the supply and demand imbalances down.” At the same time, Minneapolis Fed President Kashkari told a Boston group that “there are some hopeful signs” but also “in my judgment…we need to bring the labor market into balance so that tells me we need to do more.” Meanwhile, Fed Governor Waller told Arkansas State University that “There are signs that food, energy, and shelter prices will moderate this year….and the Fed’s rapid increases in interest rates have begun to pay off.” However, he went on to say he is not seeing signs of a quick decline and he is “prepared for a longer fight.” Finally, he said, “Though we have made progress reducing inflation, I want to be clear today that the job is not done.”

In stock news, bucking trend among big banks, JPM said Wednesday that it will be HIRING 500 new small business bankers between now and the end of 2024. Later, a US federal judge dismissed a lawsuit against WMT that had claimed the company had deceived customers by selling their Walmart brand “Fudge Mint Cookies” which contain neither fudge nor mint. Meanwhile, the California New Car Dealers Association said that the TSLA Model Y and Model 3 were the two top-selling cars in that state for 2022. However, TM retained its top spot for overall vehicle sales in the state, selling 17.3% of all cars sold in 2022 across all its various models. At the same time, CNC has reached a $215.4 million settlement with the state of CA to resolve accusations of overcharging a state program in 2017-2018. After hours, AFRM announced it is cutting 19% of its workforce after the CEO said the company deliberately over-hired the last few years to avoid missing product opportunities that were too compelling to miss. In similar news, DIS said it will cut 7,000 jobs (3.6% of the workforce) as it reorganizes after the recent leadership change. Finally, GOOGL and GOOG shares took a nosedive on the day as its new AI Chatbot Bard shared wrong information replies during a live-streamed company event to promote the new tool. The company also failed to provide details on how and when it will incorporate Bard with existing offerings.

In energy news, the front-month March Natural Gas contract fell 7.3% Wednesday. This erased gains from the prior two days and took the commodity to a level not seen since September 2020, closing at $2.3960/mmBtu. This was up off the session low of $2.3690. Meanwhile, Oil (WTI) closed up for the third day in a row as a weakening dollar helped offset what the EIA Weekly report said was a seventh consecutive week of US crude inventory builds, reaching a 20-month high of more than 37 million barrels. At the same time, the EIA report said Gasoline inventories grew by 5 million barrels to almost 16 million barrels. That same report said distillate (diesel and heating oil) stocks grew by 2.932 million barrels, which was an increase of 2.8 million barrels more than expected.

After the close, DIS, MOH, DCP, ORLY, RE, MGM, DBOEY, AB, EFX, MMS, ASGN, FLT, SONO, NVST, WTS, CXW, NLY, AEIS, and UVV all reported beats on both the revenue and earnings lines. Meanwhile, GT, PPC, TSE, WYNN, and APP all beat on revenue while missing on earnings. On the other side, XPO IFF, SON, STC, ENS, ULCC, AVB, TTMI, and MPWR all missed on revenue while beating on earnings. Unfortunately, PAA, LNC, EQH, MAT, STE, HI, FWRD, and UHAL all missed on both the top and bottom lines. It is worth noting that IFF, MAT, EFX, STE, TTMI, CXW, and FWRD all lowered their forward guidance. However, MMS, ENS, and APP raised their forward guidance.

Overnight, Asian markets were mixed with China in the green and the rest of the region in the red. Shenzhen (+1.64%), Hong Kong (+1.60%), Shanghai (+1.18%), and India (+0.12%) posted the only green. Meanwhile, Singapore (-0.86%), Australia (-0.53%), and Malaysia (-0.42%) paced the losses. In Europe, with the lone exception of Norway (-0.08%), the entire region is well into the green at midday. The FTSE (+0.73%), DAX (+1.29%), and CAC (+1.28%) are leading that region higher in early afternoon trade. As of 7:30 am, US Futures are pointing toward a gap higher to start the day. The DIA implies a +0.60% open, the SPY is implying a +0.73% open, and the QQQ implies a +1.11% open at this hour. At the same time, 10-year bond yields are down to 3.599% and Oil (WTI) is off fractionally to $78.31/barrel in early trading.

The major economic news events scheduled for Thursday is limited to Weekly Jobless Claims (8:30 am). The major earnings reports scheduled for the day include ABBV, APO, MT, ARES, AZN, BN, BAX, BWA, BRKR, CIGI, DBD, DUK, FAF, GTES, HLT, HII, NSIT, NSP, IPG, ITT, K, LITE, MSGE, MAS, MDU, PATK, PTEN, PEP, PM, RL, SPGI, SEE, TPR, TU, TIXT, TPX, THC, TRI, TM, WMG, WEX, and WTW before the opening bell. Then, after the close, BHF, CBT, CC, BAP, DXCM, EQR, EXPE, FLO, G, LYFT, MTD, MHK, MSI, NGL, OSCR, PYPL. CNXN, TEX, MODG, USX, VTR, and YELL report.

Later this week, in economic news Friday, we get the Michigan Consumer Sentiment and Jan. Federal Budget Balance reports and we hear from Fed members Waller and Harker. In terms of earnings on Friday, ENB, FTS, GPN, HMC, IQV, MGA, NWL, SPB, and SLVM report.

So far this morning, TM, PEP, PM, MT, CRARY, DUK, THC, BWA, IPG, WTW, HLT, TRI, VWDRY, ITT, BRKR, MSGE, PTEN, and WEX all beat on both the revenue and earnings lines. Meanwhile, AZN, ASX, TPR, SEE, TPX, ARES, DBD, TIXT, and BN all missed on revenue while beating on earnings. On the other side, CS, BAX, HII, and KIM all beat on revenue while missing on earnings. Unfortunately, SIEGY, FAF, MAS, and CIGI missed on both the top and bottom lines. It is worth noting that PM, WTW, TPR, and CIGI all raised their forward guidance. However, BAX and MAS lowered their forward guidance.

In late-breaking news, in addition to its earnings miss, CS reported massive and unprecedented client outflows (customers withdrawing their money) while warning there may be more losses in 2023. Elsewhere, Bloomberg reports that funds have closed more than $300 billion in short positions (according to data from JPM and DB). This move brought the market closer to its 10-year average neutral position. While this may seem bullish on its face, it could also mean that there are fewer shorts to squeeze and markets may have a harder time climbing unless the funds get outright bullish and start buying.

With that background, it looks like all three major indices are looking to gap higher while remaining inside the recent trading range (no breakouts). DIA’s gap will take it right back up to a potential resistance level. The trend remains bullish with even the DIA having slipped out of its Wedge formation modestly to the upside. With only the Weekly Jobless Claims scheduled today, look for generally strong earnings (better than had been expected), LUV being grilled by the Senate, and oddball news like yesterday’s GOOG AI demonstration failure to drive markets.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

The markets quickly exploded with bullishness reversing the day as Jerome Powell’s comments encouraged buyers, then triggering two huge point whipsaws as emotion spilled across the index charts. Though it is currently in vogue to chase parabolic index charts and already extended charts, be warned the danger of doing so is high. Today we will hear from more fed speakers and another big day of earnings reports to continue inspiring price volatility. Yesterday proved that the reversal speed of the market is high, so plan your risk carefully as indexes continue to increase.

Asian markets traded mixed while we slept, seemly keying in on the more work-to-do comments of the Fed. However, this morning, European markets surged higher in reaction to Powell’s words, with the FTSE hitting record highs! On the other hand, U.S. futures point to a gap down open ahead of another big day of earnings. Trade wisely and avoid the fear of missing out as the indexes extend.

Economic Calendar

Earnings Calendar

The number of earnings reports ramped up today with just over 100 companies listed on the calendar though there are a number of them unconfirmed. Notable reports include AFRM, AB, APP, APPS, CPRI, CME, COHR, COTY, CVS, D, DIS, ETN, EMR< EFX, FOXA, GT, HI, HPP, IFF, MAT, MGM, MOH, NYT, ORLY, PTEN, PAG, PFGC, RDN, RDWR, REYN, REXR, HOOD, SONO, THC, TRMB, UBER, XPO, YUM.

News & Technicals’

Chipotle Mexican Grill reported weaker-than-expected earnings and revenue for its fourth quarter. However, CEO Brian Niccol maintained the company hadn’t seen a backlash to higher prices for its burrito bowls and tacos, despite declining transactions. The company plans to open between 255 and 285 new locations in 2023 and said last month it is looking to hire 15,000 workers by this spring.

CVS said it would pay $39 per Oak Street Health share, a nearly 16% premium to the stock’s last closing price. With Oak Street’s acquisition, CVS will control over 160 primary care centers that serve those insured under the U.S. government’s Medicare program.

Federal Reserve Chairman Jerome Powell said Tuesday that disinflation “has begun” but is going to take time. Markets latched onto Powell’s words and briefly turned positive before flipping back to negative after he cautioned about stronger-than-expected economic data. “If we continue to get, for example, strong labor market reports or higher inflation reports, it may well be the case that we have to do more and raise rates more than is priced in,” he said.

Intended or not, Jerome Powell’s words brought out the bulls yesterday, which triggered two huge point whipsaws to strongly positive finish the day. The VIX saw fear diminish, and the T2122 indicator zoomed up again, nearing an overbought condition. Chasing extending stock prices and parabolic indexes is currently in vogue, but the risks of doing so are also very high. Plan carefully and avoid overtrading, as the reversal speed of an overextended condition can punish retail accounts harshly. We have more Fed speak today, along with some very anticipated potentially market-moving earnings reports, so buckle up for another wild day of volatility.

The SPY and QQQ opened essentially flat on Tuesday while the DIA gapped down a half of a percent at the opening bell. All three major indices then meandered sideways until Fed Chair Powell began to speak at 12:40 pm. At that point, the bulls spiked the market higher for 15 minutes, only to see the bears sell off all three indices hard for 35 minutes. However, the bulls stepped back in at 1:40 pm to lead nearly as strong of a rebound rally lasted the rest of the day. This action gave us large white candles with small upper and lower wicks. The SPY and QQQ both held support at their T-line and DIA climbed back above its own T-line. This took place on greater than average volume.

On the day, seven of the 10 sectors are green as Energy (+2.42%) led the way higher and Consumer Defensive (-0.42%) lagged the other sectors. At the same time, the SPY was up 1.31%, the DIA was up 0.90%, and QQQ was up 2.07%. Meanwhile, the VXX was down 3.10% to 11.24 and T2122 climbed back up inside of the overbought territory at 84.67. 10-year bond yields were higher again to 3.681% and Oil (WTI) just spiked higher by 4.53% to $77.47 per barrel. So, on the day, we saw a blah day that got very volatile and eventually bullish after Fed Chair Powell gave his speech to the Washington Economic Club.

The main news of the day was Fed Chair Powell’s Speech and Question-and-Answer Session at the Economic Club of Washington DC. During his remarks, Powell said that “disinflation has begun…but it’s going to take a long time.” He specifically cited the good sector as where the disinflation is showing itself strongest. Later Powell said, “If we continue to get, for example, strong labor market reports or higher inflation reports, it may well be the case that we have to do more and raise rates more than is priced in (to markets).” He was short on specifics. However, he did say that “we need to be patient” and that rates will need to be held higher for a long time. Finally, he said he expects inflation to fall all year in 2023, but it was likely to take into 2024 before the Fed target of 2% inflation is hit. On the topic of the Fed Balance Sheet, Powell said he expects it will take a couple more years before the Fed is ready to end the shrinking of its balance sheet (selling bonds). Overall, the Dollar, Bonds, and the Stock Market all took Powell’s comments as less hawkish than expected.

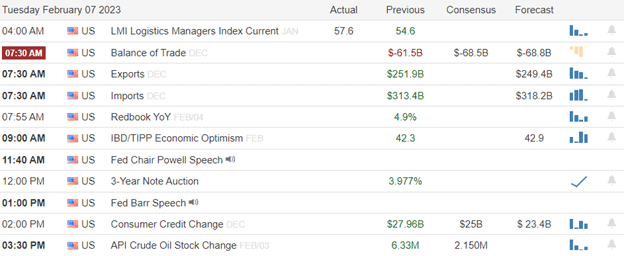

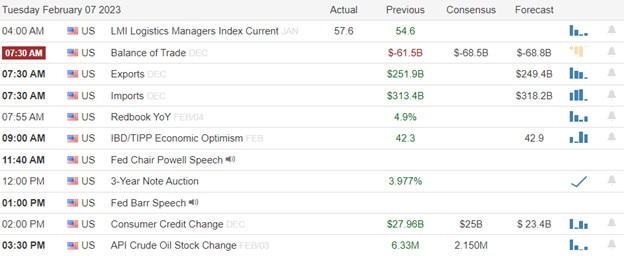

In other economic news, December Exports came in a $250.20 billion (down from $252.40 billion in November). Meanwhile, December Imports were up slightly, coming in at $317.60 billion (up from $313.40 billion in November). This also increased the Trade Deficit with a December balance of $67.40 billion (which was less than the forecast of $68.50 billion but also above the November value of $61.00 billion). Still, this was a record for the “trade gap.” Then, after the close, the API Weekly Crude Oil Stock Report showed an inventory drawdown of 2.184 million barrels (compared to an expected inventory build of 2.150 million barrels and last week’s 6.330-million-barrel build). Finally, during his “State of the Union” address, President Biden called for an unspecified additional tax on Billionaires and corporate stock buybacks. He also asked for more antitrust legislation, called for the passing of an act to stop companies from preventing workers from organizing unions, and lastly the broadening legislation to cap the cost of insulin, saying it needed to not be limited only to Medicare recipients.

In stock news, ZM announced it will lay off 15% of its employees (1,300 jobs). Later, EBAY said it would lay off 4% (400 employees) of its own workforce. ZM stock closed up almost 10% on the news. In quasi-related news, Bloomberg reported that META is poised to ask its Managers to become individual contributors (in addition to managing their teams) or leave the company. Meanwhile, DAL announced it was giving employees a 5% increase in pay across the board effective April 1. DAL cited strong travel demand and industry labor shortages as factors in the decision. Meanwhile, WFC agreed to pay $300 million to settle a shareholder lawsuit claiming the bank had hidden the fact it pushed unnecessary insurance on auto loan customers. Elsewhere, HTZGC made a regulatory filing Tuesday that showed it actually owns less than half of the TSLA cars it had planned to buy in 2022 (and TSLA releases had announced). Finally, after hours, BBBY said it has completed its last-ditch stock offering, saying that it had received $225 million and is expecting to receive another $800 million in future installments as HUD (lead investor in this offering) resells or keeps the new shares.

In airline industry news, a bankrupt South African airline (Comair) has filed suit against BA for fraud related to its agreement to buy eight 737 Max planes. The suit claimed BA failed to disclose problems within its flight control system that caused the two plane crashes in 2018 and 2019 leading to airline losses. BA refused to return the airline’s deposit on 737 Max planes after the crashes and 20-month groundings. This is nearly identical to a suit filed by a Polish airline PLL LOT in 2021, which is still pending. At the same time, BA competitor EADSY (Airbus) reported plane deliveries for January were down by a third, to 20 planes, according to Reuters. In other labor-related news, SPR announced Tuesday that it is experiencing disruptions in supplying parts for the BA 787 and the EADSY A350 due to labor shortages.

After the close, SNEX, LUMN, KD, OMC, AMCR, AIZ, VRTX, VOYA, FMC, EHC, CNO, ITUB, SSNC, WERN, QGEN, PLUS, PEAK, and ENPH all reported beats to the revenue and earnings lines. Meanwhile, VFC, CCK, CSL, and FTNT all missed on the revenue line while beating on the earnings line. On the other side, NCR, WU, ILMN, ATO, RXO, and NBR all beat on the revenue line while missing on the earnings line. Unfortunately, PRU, YUMC, CMG, VSAT, and JKHY all missed on both the top and bottom lines. It is worth noting that KD, VRTX, FTNT, QGEN, and ENPH all raised their forward guidance. However, CCK, EHC, SSNC, BKH, JKHY, and PEAK all lowered their own forward guidance.

Overnight, Asian markets were mixed again. Taiwan (+1.41%), South Korea (+1.30%), and India (+0.85%) led the gainers. Meanwhile, Shenzhen (-0.62%), Thailand (-0.60%), and Shanghai (-0.49%) paced the losses. In Europe, the picture is much greener at midday with only Russia (-0.55%) in the red. The FTSE (+0.72%), DAX (+0.76%), and CAC (+0.45%) lead the region higher in early afternoon trade. As of 7:30 am, US Futures are pointing toward a modestly lower start to the day after Tuesday’s rally. The DIA implies a -0.30% open, the SPY is implying a -0.32% open, and the QQQ implies a -0.18% open at this hour. At the same time, 10-year bond yields are back down to 3.64% and Oil (WTI) is up 1.22% to $78.09/barrel in early trading.

The major economic news events scheduled for Wednesday is limited to EIA Crude Oil Inventories (10:30 am) and WASDE Report (noon). However, we also have three Fed speakers (Williams at 9:15 am, Vice Chair for Bank Supervision Barr at 10 am, and Waller at 1:45 pm). The major earnings reports scheduled for the day include FOX, BDC, BAM, BG, CPRI, CDW, CME, COTY, CVS, D, ETN, EMR, EEFT, FOXA, GPRE, INGR, NYT, PAG, PFGC, REYN, RITM, TEVA, TRMB, UBER, UA, UAA, VSH, WFRD, WEN, and YUM before the opening bell. Then, after the close, AB, UHAL, NLY, APP, ASGN, AVB, EQH, ENS, NVST, EFX, RE, FLT, FWRD, ULCC, GT, HI, IFF, LNC, MAT, MMS, MGM, MOH, ORLY, PPC, PAA, SON, SONO, STE, STC, SLF, TSE, TTMI, DIS, and XPO report.

In economic news later in the week, on Thursday we get Weekly Jobless Claims. Finally, on Friday, Michigan Consumer Sentiment and Jan. Federal Budget Balance are reported and we hear from Fed members Waller and Harker.

In terms of earnings later this week, on Thursday, we hear from ABBV, APO, MT, ARES, AZN, BN, BAX, BWA, BRKR, CIGI, DBD, DUK, FAF, GTES, HLT, HII, NSIT, NSP, IPG, ITT, K, LITE, MSGE, MAS, MDU, PATK, PTEN, PEP, PM, RL, SPGI, SEE, TPR, TU, TIXT, TPX, THC, TRI, TM, WMG, WEX, WTW, BHF, CBT, CC, BAP, DXCM, EQR, EXPE, FLO, G, LYFT, MTD, MHK, MSI, NGL, OSCR, PYPL. CNXN, TEX, MODG, USX, VTR, and YELL. Finally, on Friday, ENB, FTS, GPN, HMC, IQV, MGA, NWL, SPB, and SLVM report.

So far this morning, CVS, PFGC, PAG, UBER, ETN, D, YUM, UAA, WFRD, BDC, COHR, RITM, UA, SCGLY, and FUJIY all reported beats on both the revenue and earnings lines. Meanwhile, TTE, EQNR, BAM, BG, CDW, TEVA, INGR, COTY, CME, TRMB, and EEFT all missed on revenue while beating on earnings. On the other side, CRTO beat on revenue while missing on earnings. Unfortunately, EMR, CPRI, REYN, and VSH missed on both the top and bottom lines. It is worth noting that COTY, UAA, and BDC all raised their forward guidance. However, INGR, CPRI, REYN, TRMB, VSH, and CRTO all lowered their own forward guidance.

In late-breaking news, interest rates dropped for a fifth consecutive week causing an 18% spike in refinance mortgage demand while new home purchase loan applications rose by 3%. However, demand was still much lower than one year ago. The average rate for a 30-year, fixed-rate, conforming mortgage fell to 6.18% with points also falling slightly. Meanwhile, in addition to their earnings, CVS announced it has agreed to buy OSH for $39/share in cash ($10.8 billion overall). This is CVS’s second acquisition in the healthcare provider space in a year. Elsewhere, there were 4 big dividend moves of note. DD hiked its dividend by 9.1% (to 2% annualized), VF cut its dividend by 41% to $0.30/share, MCRI declared a special dividend of $5.00/share, and MSBI hiked its dividend by 3.4% to 4.6% annualized.

With that background, it looks like all three major indices are looking to open as inside candles after yesterday’s strong move up. None of them appear to be retesting their T-lines (8ema) during premarket. However, DIA is not that far above its own T-line. The trend remains bullish (strongly bullish in the QQQ) in all three, but the DIA also remains in and upswing within its wedge. DIA and QQQ both have potential resistance just overhead with SPY dealing with a lesser level (from June ’22 highs and March ’22 lows). With only the EIA and Ag reports today, look for Fed speak as a potential volatility driver. However, in general, this should be a pure market sentiment day.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Monday started the day with bears milling about, but they could not wrestle control from the bulls despite the extremely extended condition of the SPY, QQQ & IWM. The VIX indicated a slight increase in fear, and volume declined, perhaps acknowledging last week’s exuberance. International trade numbers, a mid-day Powell speech, and a slew of earnings reports are likely to keep price volatility high and traders guessing what comes next. Testing support and resistance levels in the SPY, QQQ and IWM will require some big point moves, so plan your risk carefully.

Overnight Asian markets closed the day, mixed with modest gains and losses as Australia raised interest rates. As uncertainty continues to linger, European indexes trade in a relatively modest chop range this morning. U.S. futures have softened slightly from overnight highs, with earnings and a speech from Powell keeping traders apprehensive of the path forward.

Economic Calendar

Earnings Calendar

We have about 80 companies listed on the earnings calendar, although many are unconfirmed. Notable reports include AIZ, BP, CNC, CMG, DEI, DD, ENPH, ESS, FISV, FTNT, IT, GPK, HRB, HAIN, HTZ, ILMN, INCY, J, KKR, LIN PRU, RCL, SPR, VFC, VVV, WU, & YUMC.

News & Technicals’

BP posted underlying replacement cost profit, used as a proxy for net profit, of $27.7 billion for 2022. That compared with $12.8 billion for the previous year. The British oil major announced a further $2.75 billion share buyback and boosted its dividend by 10% to 6.61 cents per ordinary share. BP’s record annual profits follow bumper earnings from energy giants Shell, Exxon Mobil, and Chevron.

Microsoft on Monday announced plans to host a news event Tuesday that could be related to the AI chatbot ChatGPT. The company confirmed the event minutes after rival Google announced its answer to ChatGPT, called Bard. Microsoft’s event follows the company’s January announcement regarding its new multiyear, multibillion-dollar investment with ChatGPT maker OpenAI.

Binance will suspend U.S. dollar withdrawals and deposits for international customers beginning Feb. 8, the company said. Binance banking partner Signature Bank in January raised transaction minimums for dollar transfers. After it announced the suspension, millions of crypto dollars flowed out of Binance, but the company says it remains “net-positive.”

Although we saw a few bears milling about yesterday, there was no technical damage, with the SPY, QQQ, and IWM enormously elevated as the DIA rested at its 50-day average. Fortunately, index volume also contracted substantially yesterday, perhaps an acknowledgment of the over-exuberance last week and the uncertainty of the possible recession. Nevertheless, the bulls remain in control as we head into another big day of earnings reports and a mid-day speech from Jerome Powell. Prepare for more price volatility as the data comes out, keeping in mind some big index point moves are possible to test support or resistance in the SPY, QQQ & IWM.

Stocks gapped lower on Monday (down 0.61% in the SPY, down 0.39% in the DIA, and down 0.90% in the QQQ). From there, all three major indices rode the roller-coaster sideways all day long. This action gave us gap-down, indecisive Doji or Spinning Top type candles in the three major indices. The SPY held its T-line as support. Meanwhile, the DIA gapped down through and rallied up to retest its own T-line from below, not quite getting back above it while at the same time finding support off its own 50sma. This all happening on a much lower-than-average volume.

On the day, nine of the 10 sectors are red as Technology (-1.53%) led the way lower and Utilities (+0.46%) held up better than other sectors. At the same time, the SPY was down 0.61%, the DIA was down 0.10%, and QQQ is down 0.86%. Meanwhile, the VXX was up 2.39% to 11.59 and T2122 dropped back down into the midrange at 54.39. 10-year bond yields have spiked higher again to 3.655% and Oil (WTI) is up 1.38% to $74.40 per barrel. So, on the day, we saw a gap lower, but then indecision, perhaps meaning the bears are uncertain whether they really want to push the bulls. Basically, both sides need a little energy from some catalyst.

In stock news, DELL announced it is laying off 6,650 employees (5% of staff). At the same time, PSA made an $11 billion hostile takeover bid for LSI. This amounts to a bid of $129.30/share, but not in cash, in PSA stock instead. LSI was at $110.58/share at the time of offer, but it closed up 11.28% to $123.05 on the day. Elsewhere, after it reported beats on both lines, ON announced a $3 billion stock buyback program, which was double the size of the previous program. This is significant in the chip sector that had been weak with the exceptions of AMD. In other tech news, GOOGL announced it is planning to launch an AI Chatbot service called Bard (powered by GOOGL’s LaMDA which is a competitor to ChatGPT, which MSFT recently announced will be built into their products). The service has already been released to beta testers. Meanwhile, in the gold sector, NEM has made a $17 billion takeover bid for NCMGF. Bloomberg reports the offer is not likely to be challenged by NEM rival GOLD. Meanwhile, AMC announced a new ticket pricing structure where the ticket price will be based on seat location in tiers.

In airline industry news, on Monday, the FAA said it is proposing a $1.1 million fine on UAL for conducting Boeing 777 flights without conducting the required preflight fire system warning checks. UAL has 30 days to respond to the charges. Elsewhere, the IATA (largest airline trade organization) said that many airlines will fail to meet the FAA deadline to retrofit altimeters to avoid 5G wireless interference. (Last summer, VZ and T voluntarily agreed to delay their use of some 5G spectrum to give airlines more time. However, now the FAA, VZ and T are negotiating again for another extension.) This is expected to have some small impact on the telecom companies’ expansion of 5G their networks. Meanwhile, the EU version of the FAA ruled Monday that it will not permit single pilot flights by 2030 as airlines had been seeking (to help with labor shortages).

In commodity news, the US Dollar rose to a 4-week high against the Euro Monday as the reverberations from last week’s January Payroll numbers continued. This caused a dampening effect on all commodity prices. Meanwhile, Bloomberg reports that the US will impose a 200% tariff on Russian Aluminum as soon as this week. (Reportedly, the final decision has not been made as the Biden administration talks to US Aerospace and Auto industry leaders, the main importers of Russian Aluminum, about the damage that might cause to their businesses.) Elsewhere, Reuters reports that US farmers are planning to boost corn acreage in 2023. This comes after a late-season drought crushed the 2022 harvest and has brought US corn supplies to near decade-low levels. This modest 2.5% shift in acreage use is likely to cause dramatic swings in everything from seeds and fertilizer to herbicides, and eventually to food prices.

In miscellaneous news, on Monday Atlanta Fed President Bostic told Bloomberg that unless last week’s Payrolls report turns out to be an anomaly, it would mean the Fed still has more work to do. Specifically, he said the FOMC would need to push the peak interest rate higher than he now projects (which is 5%-5.25% as a terminal rate). At the same time, late in the day Monday, GS cuts its odds of a recession in the next 12 months to 25% (down from 35%). GS cited a rapid reduction in inflation and wage growth as well as improving business sentiment as supporting a “soft landing” and the Fed stopping its tightening regime sooner. In an unrelated story, after hours Monday, Bloomberg reported that hedge funds tracked by GS trimmed their long positions at the fasted rate in two years over the last several market days. However, they are also not taking huge short positions either. Bloomberg also reported the JPM data on the matter concurred. They called this “de-grossing” move the largest move to cash and lower-risk trades since the day after the first Reddit-driven squeeze in January 2021. Then this morning, Minneapolis Fed President Kashkari told CNBC that the Fed has not done enough yet based on January’s explosive job growth and he is raising his terminal rate expectation to 5.4% (which is higher than what most of his peers have publicly announced). He also went further in saying “we need to raise rates aggressively to put a ceiling on inflation” (which the market will not like to hear.

After the close, ACM, NOV, SPG, SAVE, FN, SKY, DIOD, KMT, SSD, and GNW all reported beats on both the revenue and earnings lines. Meanwhile, CINF and SWKS both beat on revenue while missing on earnings. On the other side, PINS missed on revenue while beating on earnings. Unfortunately, ATVI, TFII, AMRK, LEG, and TTWO all reported misses on both the top and bottom lines. It is worth noting that SWKS, LEG, SPG, TTWO, and PINS all lowered their forward guidance. However, FN raised its own forward guidance.

Overnight, Asian markets were mixed on mostly modest moves. South Korea (+0.55%), Hong Kong (+0.36%), and Shanghai (+0.29%) led the gainers. Meanwhile, Malaysia (-0.95%), Australia (-0.46%), and India (-0.24%) paced the losses. In Europe, we see a similar picture taking shape at midday. The FTSE (+0.49%), DAX (-0.17%), and CAC (unchanged) are typical of the spread in the region. None of the European bourses have moved as much as one percent in either direction yet in early afternoon trade. As of 7:30 am, US Futures are pointing toward a mixed and mostly flat start to the day. The DIA implies a -0.09% open, the SPY is implying a +0.09% open, and the QQQ implies a +0.32% open at this hour. At the same time, 10-year bond yields are down a bit to 3.63% and Oil (WTI) is up more than 1.5% to $75.24/barrel in early trading.

The major economic news events scheduled for Tuesday December Imports/Exports, and Dec. Trade Balance (both at 8:30 am), and API Crude Oil Stocks (4:30 pm) are reported and Fed Chair Powell speaks at 12:40 pm. The major earnings reports scheduled for the day include ADNT, AGCO, ARMK, ARCC, BP, BV, CG, CARR, CTLT, CNC, CEIX, DD, FSV, IT, GPK, HAIN, HTZ, INCY, J, KKR, LIN, NTDOY, NVT, OMF, RCL, SCSC, SPR, TDG, and XYL before the opening bell. Then, after the close, AMCR, AIZ, ATO, CSL, CMG, CNO, CCK, EHC, ENPH, PLUS, FMC, FTNT, PEAK, ILMN, ITUB, JKHY, KD, NBR, NCR, OMC, PRU, RXO, SSNC, SNEX, VRTX, VFC, VSAT, WERN, WU, and YUMC report.

In economic news later in the week, on Wednesday EIA Crude Oil Inventories are reported and Fed member Williams speaks. On Thursday we get Weekly Jobless Claims. Finally, on Friday, Michigan Consumer Sentiment and Jan. Federal Budget Balance are reported and we hear from Fed members Waller and Harker.

In overnight news, BBBY announced last night that it will try a list-minute (last ditch) stock sale to raise the cash to avoid bankruptcy. They are hoping the new shares will raise just over $1 billion. Elsewhere, CS announced that it is canceling (at least for now) the company “Compensation Day” where employees were told their bonus amounts (and given the money) for 2022. The company had previously announced they were slashing the bonus pool in half this year due to the financial condition of the company.

So far this morning, CARR, DD, J, GPK, XYL, IT, OMF, INCY, NVT, BV, ARCC, FISV, and CEIX all reported beats on both the revenue and earnings lines. Meanwhile, BP, CNC, ARMK, ADNT, CTLT, FISV, and VVV all reported beats on revenue while missing on earnings. On the other side, LIN, CG, and HAIN reported a miss on revenue while beating on earnings. Unfortunately, NTDOY (Nintendo) missed on both the top and bottom lines. It is worth noting that FISV raised its forward guidance while BV lowered its own forward guidance.

With that background, it looks like the SPY and DIA are going to test their T-lines (8ema) again this morning. Meanwhile, QQQ looks to be trying to put a bottom into its two-day pullback (at least in premarket trade). The wedge pattern in the DIA and the bullish trends in the SPY and QQQ remain the main technical features of the market at this point. Do not be surprised if we wander around until Fed Chair Powell’s remarks this afternoon. I think that Bostic and Kashkari were presignalling his sentiments (preparing the market for his words today) and that Powell is likely to make sure the market realizes there will be no “March pause” (as several talking heads had predicted in the recent past). However, he is also likely to say the jobs numbers were a good sign that the Fed is walking a “Goldilocks path” where inflation is coming down and at the same time jobs are being created. In short, he’s likely to imply that we just need to “stay the course” with modest hikes for a while to definitely get inflation under control at the same time we stay on the soft-landing trajectory.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service