Jobless Claims, Stimulus, and Debate Lead

Wednesday was another roller coaster day for stocks as the opened before running up and down all day, closing on the lows. All 3 major indices printed ugly black high-wick, inverted hammer type candles. On the day the QQQ was flat (-0.08%), SPY was down 0.21%, and DIA was down 0.35%. The VXX was also down to 22.67 and T2122 fell back to almost exactly mid-range. 10-year bond yields rose again to 0.818% (the High since June) and Oil (WTI) fell over 4% to $39.97/barrel.

Stimulus (or the lack thereof) remained the main story during the day. The Senate failed to pass the $500 billion PPP loan/grant program Majority Leader McConnell had been pushing. At the same time, while negotiations continue, House Speaker Pelosi and Treasury Sec. Mnuchin failed to reach a deal. However, both sides announced that differences are narrowing and that they are optimistic for a deal. Talks will continue on Thursday. However, even if a deal is reached, it is still an open question if and when McConnell would bring the deal to a Senate vote or whether they could get a larger deal passed. FDA Head Hahn also said that while no timeline exists, the goal remains that all Americans will be able to begin a vaccine course by sometime next Spring.

Purdue Pharma has plead guilty to 3 federal criminal charges stemming from opioid marketing, will pay a $8 billion fine, and the Sackler family will close the company as an entity while the operations continue as a new company. Several State Attorney’s General objected to the deal, which would create a government-controlled business from the assets of the company (to continue making/selling Oxycontin). The objection is based on the states would likely have gotten more money from a private sale, because at least one other drug manufacturer has expressed interest in purchasing the business. However, the DOJ has completed the deal anyway.

On the virus front, in the US the numbers show we now have 8,585,748 confirmed cases and 227,419 deaths. After another day in excess of 63,600 cases, the 7-day average daily new case count has risen to 61,481/day, while the over 1,200 deaths only moved the daily average of deaths slightly to 794. With that background, the CDC reported an alarming trend with surging cases all across the country and particularly high transmission levels in the Midwest as national cases have risen 17% in the last week. However, NIH Director Collins says a viable vaccine should be approved in the next couple of months with wide availability sometime in Q2 of 2021. In related good news, the head of the “Warp Speed” program told Bloomberg that it is possible both the JNJ and AZN phase 3 trials would be allowed to restart this week.

Globally, the numbers rose to 41,568,570 confirmed cases and the confirmed deaths are now at 1,137,684 deaths. This includes the world seeing over 437,000 new cases Wednesday (a record high new case count). Global Covid deaths have also risen (almost 7,000 on the day), but on average remain about 5,640 per day. In the UK, the country saw another record number of new cases. In Poland, the daily death count has reached four times the count during the first wave as the country recorded another consecutive record number of new cases and has turned the national stadium into a field hospital. A similar situation runs throughout Europe, in particular the Eastern part of the continent including Russia, but also Italy, Belgium, Germany, and Ireland.

Overnight, Asian markets were mostly lower with South Korea (-0.67%) and Shenzhen (-0.49%) leading the modest losses. In Europe, markets are mixed so far today with very modest moves so far. Among the big 3 bourses, the FTSE is up 0.10%, the DAX flat +0.01%, and the CAC up 0.17%. The rest of European Exchanges are mainly in the red. As of 7:30 am, US futures are pointing to a modestly lower open with all 3 major indices showing -0.20% as of now.

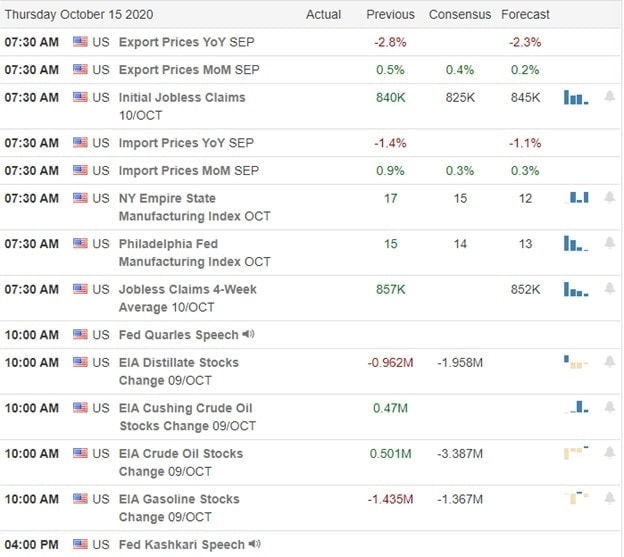

The major economic news for Thursday is limited to Initial Jobless Claims (8:30 am), Sept. Existing Home Sales (10 am), and a Fed speaker (Kaplan at 6 pm). However, there is also the final Presidential debate at 9 pm. Major earnings reports include AAL, AB, AEP, CTXS, DGX, DHR, DOW, EQT, FAF, FCX, FITB, GPC, GWW, HBAN, KMB, LUV, MTB, NOC, NUE, PAG, PHM, POOL, RCI, RS, SIRI, SON, STM, T, TSCO, UNP, and VLO all before the open. Then after the close, COF, INTC, MAT, RHI, SIVB, and TFII report.

Jobless claims or some tidbit from the stimulus negotiations are likely the only drivers today, in front of the last Presidential Debate. That being the case, we may see another day of rest in the markets as traders seek more clarity. The virus continues to surge, but markets seem to have baked that fact into the cake and are now more worried about political risk and stimulus. Of course, earnings reports remain the wildcard, with mixed but generally positive results reported so far against much-lowered expectations.

Continue to be careful and nimble in this whipping market. The short-term trend remains bearish and has broken the medium-term uptrend. However, all it takes is a whiff of a stimulus deal to turn the bulls loose. So, keep locking-in your profits and sticking to your trading rules. Don’t get too greedy, don’t chase the moves you have missed, and don’t predict. Be sure you respect potential support and resistance. Follow the trend and trade your plan.

Ed

Swing Trade Ideas for your consideration and watchlist: AA, BKR, WRB, HUN, SO, DIS, KSS. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service