Virus Runs Wild and Tech Guidance Mixed

Thursday saw a run-and-fade move in the wake of Wednesday’s huge selloff. The bulls gapped the indices about half a percent, rallied all day until 2 pm, and sold off hard at the end of the day. This left all 3 major indices will large upper wicks and indecisive candles. On the day, DIA gained 0.43%, SPY gained 10.5%, and QQQ led the way up 1.73%. The VXX lost almost 8% to 35.60 and T2122 rose but remains in oversold territory at 15.71. 10-year bond yields rose sharply to 0.83% and Oil (WTI) fell nearly 3% again to $36.30/barrel.

During the day, Speaker of the House Pelosi said she wanted to restart stimulus talks. However, she sent a letter to Treasury Sec. Mnuchin saying she is still waiting to hear replies to several items of critical importance. Sec. Mnuchin responded that she had released the letter to the press at the same time it was delivered to him and therefore he concludes it was not a serious attempt to restart talks, but just a stunt. In reality, negotiations are moot until after the election since the Administration, Senate and House are all focused on electioneering.

After the close, AMZN, AAPL, FB, GOOG, and TWTR all reported beats on both the top and bottom lines. AAPL and TWTR both were both punished in extended trading on disappointments of one kind or another, while FB was flat and GOOG popped. It appears that overnight this led to worry among the tech-heavy QQQ traders.

Virus numbers continue to run wild with unrelenting growth amidst current local-only and half measures. The numbers show we now have 9,216,077 confirmed cases and 234,207 deaths. This comes after yet another record number of 91,530 new cases on Thursday with a 7-day average daily new case count spiking again to 77,773/day. Deaths also ticked up with 1,047 reported while the average daily deaths lag behind at 828.

Globally, the numbers rose to 45,429,027 confirmed cases and the confirmed deaths are now at 1,187,582 deaths. With this said, beyond the US, Europe is the epicenter of the virus. Belgium reports an “absolutely critical” situation where the country is not only short of ICU beds but also health workers. In fact, the EU is now funding patient transfer between European countries in order to find beds and ease staff shortages. France’s new national lockdown begins today and runs through at least December 1. (They estimate this new lockdown will curb economic output by 15%.) Germany, who has reported a record number of new cases each of the last 3 days, has also implemented a partial national lockdown for the next 4 weeks. However, the wildfire spread is not limited to Western Europe as Russia, the Czech Republic, Poland, Slovenia, and most of the former Soviet Block see huge infection rates (if not huge populations).

Overnight, Asian markets were sharply red across the board. South Korea (-2.56%), Shenzhen (-2.29%), and Hong Kong (-1.95%) led the losses. Meanwhile, India (-0.24%) and Australia (-0.55%) faired best. However, in Europe, markets are leaning to the green side at this point in the day. Among the big 3 bourses, the CAC (+0.56%) leads while the DAX (-0.01%) and FTSE (+0.02%) are flat. Spain (+1.46%) is the only one percent mover with Russia (-0.24%) and Norway (-0.23%) being the only red on the board. As of 7:30 am, US futures are pointing to a gap lower at the open. The large-cap indices are pointing to an open down half a percent while the NASDAQ points to a 1% gap down at the moment.

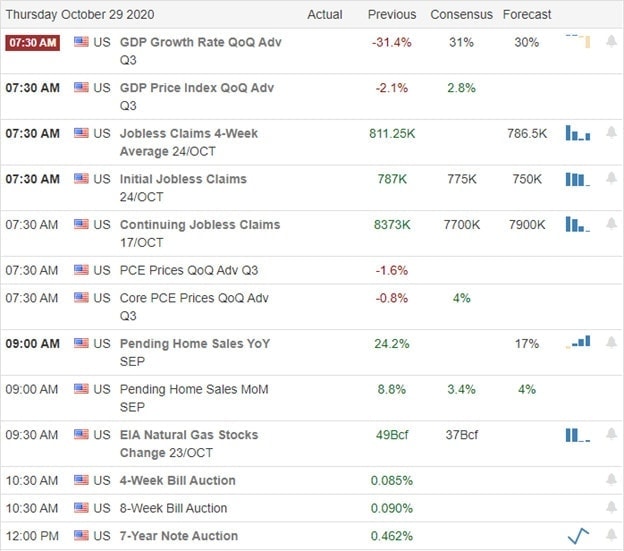

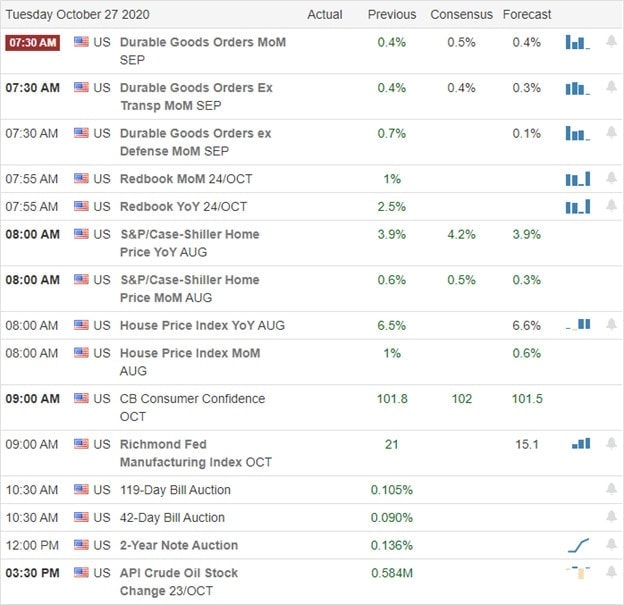

The major economic news for Friday includes Sept. PCE Price Index, Sept. Personal Spending, Sept. Employment Cost (all at 8:30 am), Chicago PMI (at 9:45 am), Mich. Consumer Sentiment (10 am). Major earnings reports include ABBV, MO, AXL, AON, BAH, BR, CHTR, CVX, XOM, FTS, GT, HON, LHX, LEA, LYB, NWL, PSX, PNW, PEG, SJR, UAA, and WY all report before the open. However, there are no major reports after the close.

The virus, the election, and earnings (or more importantly future guidance) are the main sources of volatility. With stimulus apparently a dead idea until after elections are held (and probably until results are known), this is a risky environment for investors. So, expect and plan for the volatility if you’re trading. Also, remember that this is Friday and Friday in front of what is likely to be the most political news filled weekend in years at that.

Think carefully if you want to be carrying risk into this weekend or perhaps even through the election. Also remember that if you do want to lighten up and haven’t done so, there is a good chance a lot of other traders have the same idea. Be careful, nimble, and bear in mind you don’t have to trade every day or even week. Lock-in profits whenever you can and maintain your discipline. Stick to your rules, follow the trend, and don’t chase moves you have missed.

Ed

Swing Trade Ideas for your consideration and watchlist: CLF, FCX, KRE, INFO, OKE, HOLX, SCHW, NTNX, JD. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service