Market Mulls A Lot of Gov’t News Today

Wednesday saw another gap higher (about 3 or 4 tenths of a percent) in spite of an August Retail Sales number that missed estimates by 40%. The roller coaster ride followed with the climax being a strong rally at 2pm (after the Fed said interest rates will remains near zero for at least 3 years) and an even stronger selloff at 3pm. On the day SPY was down 0.38%, DIA up 0.16%, and QQQ down 1.59% as the techs continued to get hammered. This gave us big bearish candles in the QQQ and SPY as well as an ugly high wick in the DIA. Oddly enough VXX also fell on the day, ending at 24.96 and T2122 climbed to 71.71. 10-year bond yield rose slightly to 0.697% and Oil (WTI) was up over 5% to $40.24/barrel.

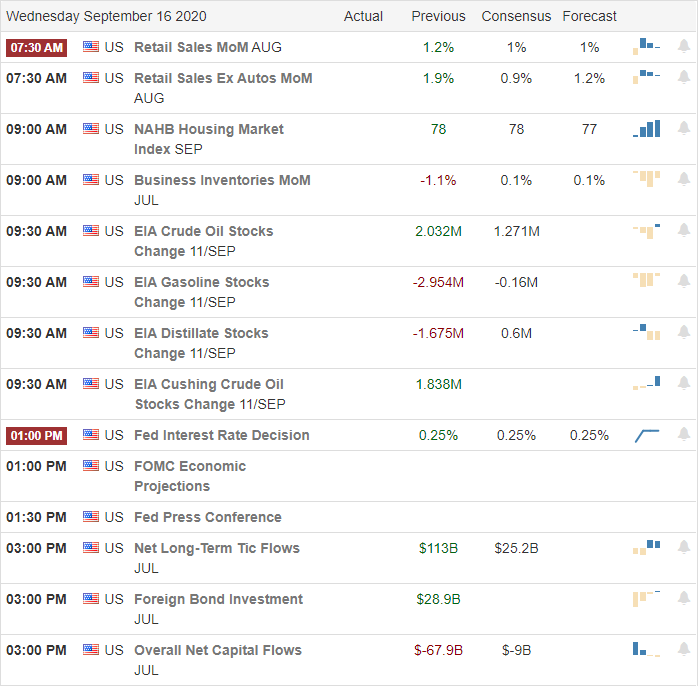

As mentioned, the big news on the day was the Fed confirming what individual Fed voters have been saying for quite some time. The FOMC will hold rates essentially at zero percent for years to come, specifically at least through 2023. Nonetheless, they also improved their GDP forecast to a 3.7% contraction (when the last forecast was for a 6% contraction as recently as June). However, on the other side, they also reduced the 2021 GDP forecast from 5% growth to 4% growth. Chair Powell also said the Fed is working on changes to the Main Street Lending Program (which has been a flop with less than one-quarter of one percent of available funds being requested as loans as of now) to make it more widely accessed.

President Trump took a step back from his former position and called on the GOP to support a much larger stimulus package than either the Administration or the Senate Republicans had previously said they would accept. He didn’t mention a specific amount, but White House Chief of Staff Meadows later told the press that $1.5 trillion could be acceptable. (This number is halfway between the Republicans original $1 trillion and the Democrats most recent offer of $2 trillion. However, it’s a full trillion dollars over what Senate Republicans had wanted in their “Skinny Bill” as late as last week.) Both Meadows and House Speaker Pelosi said they are more hopeful of a deal now than they have been in 3 months. Senate Majority Leader McConnell refused to comment. For his part Fed Chair Powell reiterated that he still feels more fiscal support is likely needed with 11 million people out of work, small businesses struggling and local government revenues having dropped. In an unrelated story, House Republicans are moving to force a vote to re-issue the $138 billion of PPP program funds that went unrequested from the last stimulus bill. It’s unclear if there would be more demand now than earlier, but it is a sound political move and the market loves stimulus whether real or paper.

As for the ORCL- Byte Dance partnership deal for TikTok US operations, both Sec. of State Pompeo and President Trump said they don’t like what they have heard. While not an outright disapproval of the deal, it cannot be seen as a positive thing with just 3 days remaining until the White House-imposed deadline. On the positive side, the President did admit that he has given up on the government “getting a lot of money” for forcing the deal (government lawyers have explained to him that is not legal). Still, that was never a real obstacle to a deal. The crux of the issue is that the White House insists on a sale of the business and its technology assets while China has said it will not allow the sale of the technology (search and user interest tracking algorithms, etc.). On top of that, apparently no suitor has offered what Byte Dance feels is fair compensation for the entire business (the Oracle deal would leave Byte Dance with majority ownership in the new shell company).

On the virus front, in the US, the numbers show we now have 6,828,698 confirmed cases and 201,366 deaths. We saw another uptick to 40,154 new cases and 1,151 deaths. On Wednesday CDC Director Redfield told a Senate committee that masks are the most important tool we have and may well be more effective than a vaccine. In the same testimony, he said most people will not be able to access a vaccine until mid-2021 and the process would take 6-9 months to get enough people vaccinated twice to provide community herd immunity. (Beyond the supply issues, another hurdle will be the public. Two days ago, a non-partisan 1,200 respondent Kaiser Foundation poll found that only 42% of Americans will get vaccinated even when it is available.) In a different hearing, Dr. Fauci (NIH) told House lawmakers that while October data is theoretically possible, he expects data about the efficacy and safety of the early vaccine candidates to become available in November or December. (Oddly, he also said that US phase 3 trials are still only about two-thirds enrolled with approved healthy participants at this point.) However, as he often does, President Trump told reporters that the experts were wrong, large-scale vaccine distribution will begin about mid-October and 100 million vaccine doses will have already been distributed in the US by year-end.

Globally, the numbers rose to 30,073,744 confirmed cases and 945,817 deaths. The WHO came out against “Covid-19 passports” (passports that would allow test-free and quarantine-free travel for people with antibodies), because there are no studies on how universal immunity would be or how long immunity lasts. The renewed spread in Europe continues, but that is dwarfed by India, which reported a record high of 97,800 new cases today.

Overnight, Asian markets were red across the board, with the lone exception of Shenzhen which managed +0.08%. The biggest losers were Hong Kong, South Korea, and Australia which were all down over 1.2%. Europe has followed Asia so far today with red across the board. However, only the Netherlands is down more than a percent as of 7:30am. Speaking of that time, as of then the US futures are pointing to a gap lower. The Nasdaq implies a gap down of 1.63%, the SPY a dap down of 1.13%, and the DIA a gap down of 0.81%.

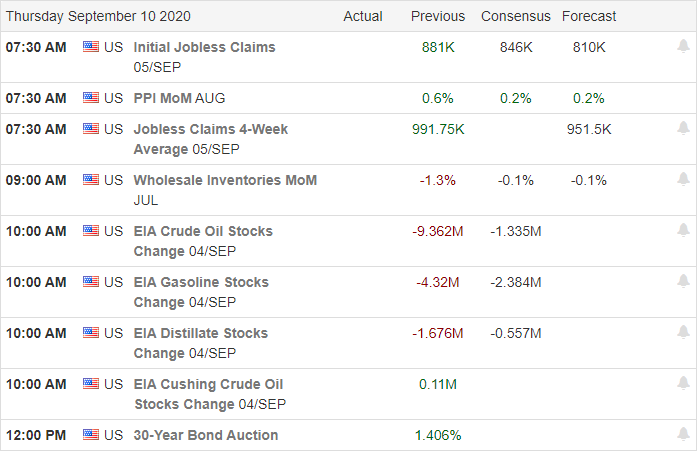

The major economic news for Thursday includes August Building Permits, August Housing Starts, Weekly Initial Jobless Claims, and Philly Fed Mfg. Index (all at 8:30 am). However, once again there are no major earnings reports on the day.

Be careful of volatility with gap and reverse being the norm recently in the mornings. Stick to your plans. Follow the trend and don’t chase moves you have missed…there will be another one soon. Hang in there with your rules and keep locking-in profits. Remember, trading is a job, not a lottery ticket.

Ed

Swing Trade ideas for your Consideration and Watchlist: TRUE, COF, MDB, MKC, HLT, ADSK, MMM, WFC, PYPL, AXP. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service