Holding Their Breath

After another record-setting day, world markets seem to be holding their breath this morning as we wait for the Feds new policy speech. With all eyes focused on Jerome Powell, how the market perceives the new stance on inflation may well extend this rally higher or bring out the bears. If that’s not enough to digest, the market has a damaging hurricane to keep track of, significant day earnings reports, as well as GDP and Jobless data. Stay on your toes; today is not the time to become complacent.

Asian markets closed mixed but mostly lower overnight. European markets see red across the board this morning as they trade cautiously awaiting the Powell remarks. US Futures currently point to lower open, but anything is possible, so remain focused and flexible.

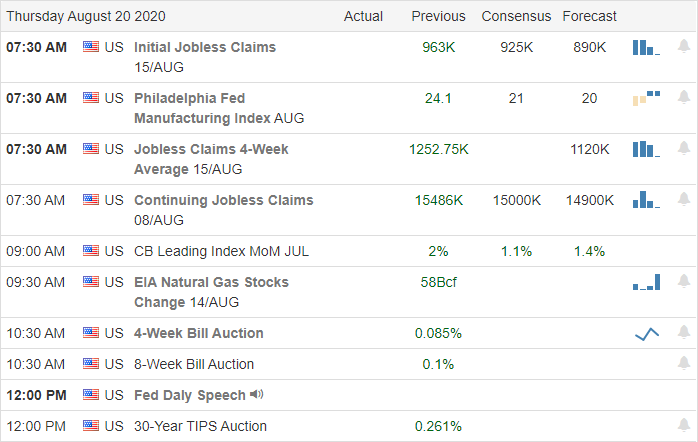

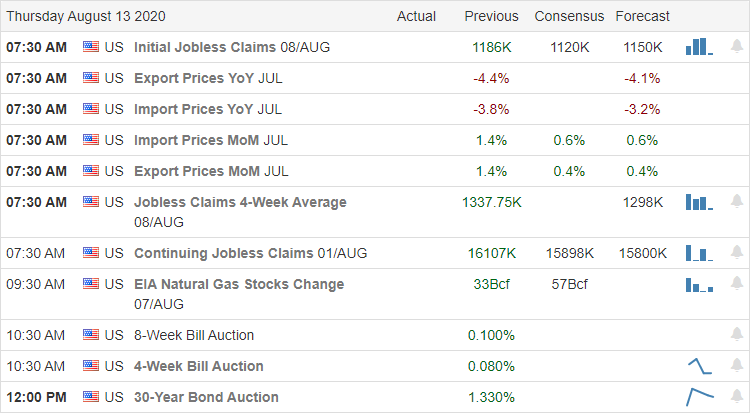

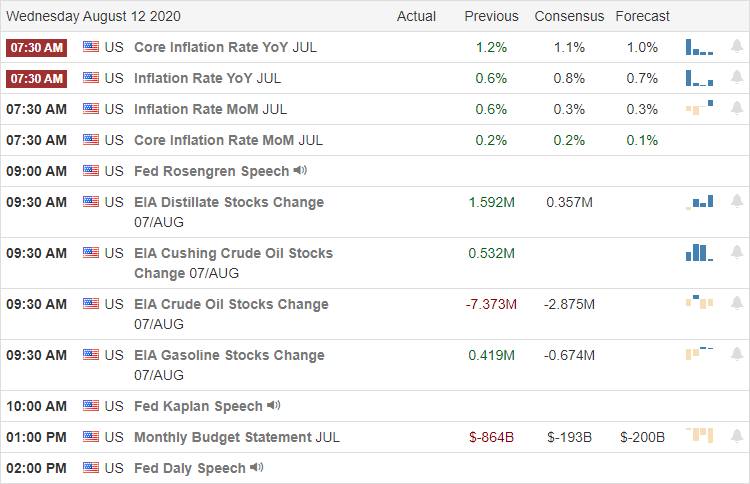

Economic Calendar

Earnings Calendar

On the Thursday earnings calendar, we have the biggest day of reports this week, with more than 40 companies fessing up to results. Notable reports include DG, FLWS, ANF, BILL, BURL, CM, COTY, DXLG, DLTR, GPS, HPQ, MRVL, OLLI, SAFM, TD, YLTA, VEEV, VMW, & WDAY.

News & Technical’s

The majority of the countries’ refining capacity has been shuttered and locked-down as hurricane Laura pummels the Lousiana and Texas coast. They are calling this an unsurvivable system with a storm surge estimate that could reach 30 to 40 miles inland, putting millions of homes at risk. While keeping an eye on storm damages, the market has a big day of information to digest, with the biggest being the Fed chairman’s speech at Jackson Hole, where its expected he will layout a new inflation policy. How the market perceives this speech could inspire the markets higher or bring out the bears should Powell fall short of expectations. That in its self is plenty to deal with, but before the speech, we will get a reading on the GDP and Jobless Claims, not to mention the biggest day of earnings results this week.

Bullish trends continued to stretch out yesterday with the SP-500 and NASDAQ once again setting new records. Markets around the world seem to be holding their breath this morning as we wait for the Fed speech. No pressure Jerome, only the future direction of the market is at stake. Stay focused and flexible, remembering that what goes up will eventually come down, so don’t become complacent.

Trade Wisely,

Doug