SNAP and STX have QQQ A Little Spooked

Stocks opened basically flat on Thursday, but then sold off for the first hour. This saw the two large-cap indices to bounce up off their 50sma. For the rest of the day, we had a series of whipsaws, ending on bullish swing right into the close. In a broader context, it was another volatile, whipsaw day where the action ended up being bullish…again, on low volume. 7 of the 10 sectors were in the green with Healthcare and Technology leading the winners. However, Energy and Communication Services were the biggest movers and they were both losing sectors. The day saw the QQQ drag the large-caps higher on a standout post-earnings move by TSLA.

This all left us with white-bodied candles with longer lower wicks. So, at this point, all three major indices are above their 50sma and sit a bit extended from their T-line (8ema) as well as in terms of their 4-week New High/Low Ratios. On the day SPY gained 1.01%, DIA gained 0.52%, and QQQ gained 1.44%. The VXX fell 1.7% to 21.20 and T2122 remains deep in the overbought territory at 96.24. 10-year bond yields also fell sharply, dropping back below 3% to 2.889%, and Oil (WTI) dropped about 3.44% to $96.43/barrel (which was actually a rally up off the session lows).

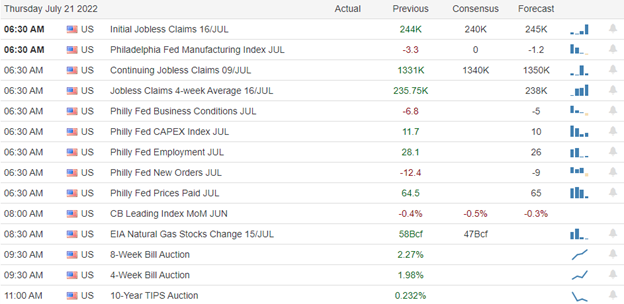

In economic news, Weekly Initial Jobless claims came in significantly higher than expected (251k vs 240k forecast). This was the highest level since mid-November. Meanwhile, the Philly Fed Mfg. Index fell to -12.3, down 9 points from the prior month and much worse than the expected 1.6 value. This was the lowest rating since May 2021. Elsewhere, the ECB raised rates by half a percent (but for perspective, only to zero now since they were negative rates). This was their first rate hike for 11 years and the largest hike since 2000. As a result, the Euro strengthened against the Dollar.

SNAP Case Study | Actual Trade

In business news, after the close, AMZN agreed to buy primary care provider One Medical for $3.49 billion as the e-commerce giant continues its push into the healthcare sector. Elsewhere, in a shock, Chinese chipmaker Semiconductor Manufacturing International (located in Shanghai) has advanced its chipmaking technology by more than 2 generations. They are now shipping 7-nanometer chips to Bitcoin miners. This essentially guts US sanctions. It could also make China a serious new competitor to western chipmakers like TSM, INTC, AMD, NVDA, QCOM, and SSNLF (import sanctions permitting). Finally, AXP raised its guidance on what it called resilient credit card usage.

On the Russian invasion story, Turkey announced that Ukraine and Russia will sign a deal today to reopen Ukraine’s Black Sea ports for grain exports. Meanwhile, Ukraine asked its creditors for a two-year freeze on bond payments (in order to use its diminished resources on war efforts). BLK is the largest holder of such bonds, holding $1.2 billion across its various funds. AB is the second largest Ukrainian bond holder with $580 million while Pimco and Eaton Vance both hold around $300 million of the bonds. Elsewhere, the EU announced another round of sanctions which included freezing the assets of Russia’s largest lender Sberbank.

After the close, MAT, UFPI, and WAL reported beats on both the top and bottom lines. Meanwhile, WRB, PPG, RHI, and THC, missed on revenue while beating on earnings. However, SNAP, STX, SIVB, SAM, and ISRG all missed on both lines.

Overnight, Asian markets were mixed again on modest moves. South Korea (-0.66%) and Shenzhen (-0.49%) were the only appreciable losers. On the other side, Malaysia (+1.07%), Singapore (+0.92%), and India (+0.69%) led the gainers. In Europe, stocks are mostly green on modest moves at mid-day. The FTSE (+0.22%), DAX (+0.32%), and CAC (+0.22%) are leading the region higher with only Belgium (-0.11%) and Finland (-1.22%) showing red at this point in early afternoon trading. As of 7:30 am, US Futures are pointing toward a mixed open that leans toward the red. The DIA implies a +0.10% open, the SPY is implying a -0.27% open, and the QQQ implies a -0.50% open at this hour. 10-year bonds are continuing that sharp fall at 2.809% and Oil (WTI) is off another 1.76% to $94.70/barrel in early trading.

The major economic news events scheduled for Friday are limited to Mfg. PMI and Services PMI (both at 9:45 am). The major earnings reports scheduled for the day include AXP, ALV, CLF, GNTX, HCA, NEE, NHYDY, RF, ROP, SLB, TWTR, and VZ before the open. There are no major reports after the close.

So far this morning, HCA, AXP, ALB, RF, and DNKEY all reported beats on both the revenue and earnings lines. Meanwhile, ALV, NEE, and ROP reported misses on the revenue line while beating on earnings. On the other side, CLF and VZ beat on revenue while missing on earnings.

Once again, earnings remain the primary focus of markets today. Last night’s terrible miss by SNAP on horrific ad sales has the high-tech QQQ spooked. So, despite generally good results, the 3 major indices are looking leery in the premarket. PMI numbers may have an impact after the market opens. However, as of now, we look to open flat to modestly bearish again. Don’t be surprised if the intraday whipsaw action continues. Still if we look at the daily chart, it is clear the bulls have the momentum in the short-term with part of a gap still left to fill to the upside in the large-cap indices.

Remember that trading is our job. So, do the work and follow the process. Stick with your trading rules, trade with the trend, and take those profits when you have them. Demonstrate patience and wait for confirmation. So, don’t be stubborn. If you have a loss, just admit you were wrong, respect your stop, and take the loss before it grows. Always move your stops in your favor (remember the “Legend of the man in the green bathrobe“…it is NOT HOUSE MONEY, it’s all our money!). Lastly, remember that you get rich slowly and steadily in Trading…not by striking it rich on one or two trades. So, give up that lottery ticket mentality.

See you in the trading room.

Ed

Swing Trade Ideas for your consideration and watchlist: No trade ideas today. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service