The July Fed Minutes Are Out Today

On Tuesday, markets gapped very modestly lower at the open and continued to follow through to the downside for the first hour. The exception to this was the DIA which was held up by WMT and HD and recovered the gap in the first 5 minutes. From 10:30 am the bulls stepped into rally strongly at least refilling the gap and reaching the highs of the day at about 2:20 pm. However, at that point, we sold off hard for half of an hour, then waffled for 30 minutes before starting back up. This is left us with modest gap-down indecisive (Spinning Top) type candles in the SPY and QQQ, as well as a breakout white candle with a significant upper wick in the DIA.

Seven of the ten sectors were in the green, with Consumer Defensive, Basic Materials, and Consumer Cyclicals out in front on strength of those WMT and HD earnings pops. Healthcare and Technology were the biggest losing sectors Tuesday. SPY and DIA are testing their 200 smas and all 3 major indices are extended from their T-line. The VXX is down one percent again to 21.29 and T2122 is telling us we remain well overbought at 96.97. 10-year bond yields are up into the 2.817% area and Oil (WTI) is down more than 3.27% to the $86.49/barrel area.

In economic news, we got mixed housing data. July Building Permits came in a bit above forecast (1.674mil vs. 1.650mil estimated), but still below the June number (1.696mil). However, July Housing Starts came in below forecast (1.446mil vs. 1.540mil average estimate). Elsewhere, July Industrial Production came in significantly stronger than was expected (+0.6% vs +0.3% forecast and -0.2% in June). Finally, at the close, President Biden signed the Inflation Reduction Act, setting a minimum 15% corporate tax rate, allowing Medicare to negotiate prices on 10 specific drugs, and setting up roughly $400 billion in money for automakers who produce “clean vehicles” while removing tax credits for consumers who buy such cars.

SNAP Case Study | Actual Trade

In earnings news, after the close, A and JKHY both reported beating on the revenue and earnings lines. So far this morning, TECHY, ADI, and PFGC all reported beats on both the top and bottom lines. Meanwhile, LOW and TJX missed on revenue while beating on earnings. On the other side, CABGY beat revenue while missing on the earnings line. However, TGT and ZIM both missed on both lines.

In stock news, on Tuesday AAPL started positioning for the recession by laying off 100 contract recruiters, thus signaling they will do far less hiring in the next six months. For the second day in a row, BBBY traded in a massive range (an 87% range Tuesday) as retail, and especially meme stock traders, got excited by CME Chairman Ryan Cohen placed another bet on the retailer by buying deep OTM January 2023 call options (with an exercise price at least 3-4 times the stock’s current $20 price). This wild action also caused BBBY stock trading to be halted several times Tuesday.

In supply chain news, President Biden’s Rail Emergency Board delivered its rail contract recommendations Tuesday. The board’s creation put a stop to potential national rail strikes and the delivery of their advice now starts a 30-day clock before any strikes can legally happen. The White House expressed hope that these new recommendations will break the stalemate between CSX, UNP, BRKB’s BNSF, and over 115,000 rail workers. In related news, UNP reported that Q3 freight volumes are up 2% from one year ago. The rail company also reported less congestion at freight terminals (fewer delays) and improved staffing levels compared to earlier in 2022.

In mortgage news, the average 30-year fixed-rate, conforming loan interest rate fell slightly from 5.47% to 5.45%. Nonetheless, applications for home purchase loans fell 1% for the week (18% lower than the same week in 2021). Refinance applications also fell 5% for the week (82% lower than a year ago). This meant an overall 2% lower loan application volume for the week.

Overnight, Asian markets were mostly green. Only South Korea (-0.67%) printed any significant red. Meanwhile, Japan (+1.23%), Shenzhen (+1.00%), and India (+0.67%) led the region higher. In Europe, stocks are leaning heavily to the red side at mid-day. The FTSE (-0.40%), DAX (-1.39%), and CAC (-0.57%) are leading the region lower with only Denmark (+1.43%) showing any appreciable green in early afternoon trading. As of 7:30 am, US Futures are pointing toward a down start to the morning. The DIA implies a -0.55% open, the SPY is implying a -0.73% open, and the QQQ implies a -0.82% open at this hour. However, 10-year bond yields are up sharply to 2.88% and Oil (WTI) is on the red side of flat in early trading this morning.

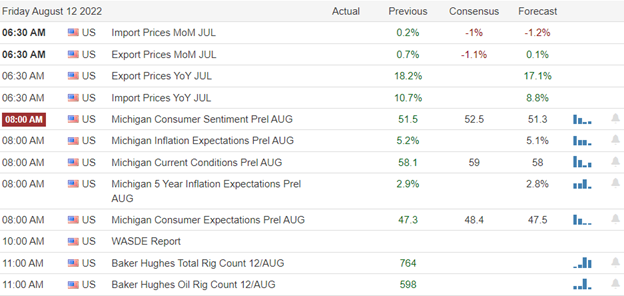

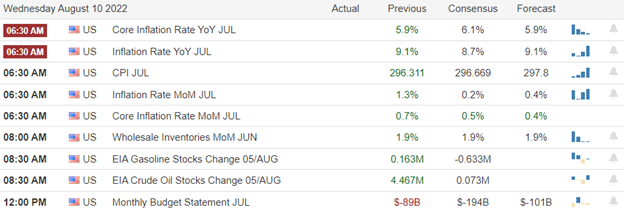

The major economic news events scheduled for Wednesday we get July Retail Sales (8:30 am), June Business Inventories and June Retail Inventories (10 am), EIA Crude Oil Inventories (10:30 am), a 20-year Bond Auction (1 pm), and July FOMC Minutes (2 pm). Fed Member Bowman also speaks twice (9:30 am and 2:20 pm). The major earnings reports scheduled for the day include ADI, LOW, PFGC, TGT, TCEHY, TJX, and ZIM, before the open. Then, after the close, AMCR, BBWI, SQM, CSCO, KEYS, SNPS, and ZTO report.

In economic news later this week, on Thursday, Weekly Initial Jobless Claims, Philly Fed Mfg. Index, and July Existing Home Sales are announced and Fed Member George speaks. Finally, on Friday there is no major economic news.

In earnings later this week, on Thursday, we hear from BJ, CSIQ, EL, KSS, NICE, SPTN, TPR, AMAT, and ROST. Finally, on Friday we get reports from DE, FL, and VIPS.

This morning, it looks like Mr. Market is looking to correct the bullish over-extended condition we find ourselves facing. A modest pullback would be very healthy for the rally, so don’t panic. However, it may also be a slow day until mid-afternoon as it seems like there is a lot of desire to read the minutes of the FOMC July meeting for clues on what will happen in September. The other story will be the bad report from TGT from its one-time hit taken from discounting to unload inventory. With that backdrop, we can expect another low-volume, perhaps dead morning, potentially followed by a volatile afternoon. Either way, the trend remains bullish, but remember those stocks are extended/overbought…so they need a pause/pullback.

Remember that trading is our job. So, do the work and follow the process. Stick with your trading rules, trade with the trend, and take those profits when you have them. Demonstrate patience and wait for confirmation. Don’t be stubborn. If you have a loss, just admit you were wrong, respect your stop, and take the loss before it grows. When price does move in your direction, always move your stops in your favor (remember the “Legend of the man in the green bathrobe“…it is NOT HOUSE MONEY, it’s all OUR MONEY!). Lastly, remember that you get rich slowly and steadily in Trading…not by striking it rich on one or two trades. So, give up that lottery ticket mentality.

See you in the trading room.

Ed

Swing Trade Ideas for your consideration and watchlist: QID, SDS, GE, WFC, GM, C, FUBO. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service