Tech Giants Reverse

The stock market displays some optimism on Wednesday morning, with futures pointing upwards, after the tech giants reverse and the AI hype returns. Investors and analysts alike are now turning their gaze towards the upcoming release of May’s personal consumption expenditures price index on Friday, a key indicator of inflationary trends. Additionally, the traders anticipate earnings from General Mills and Paychex, scheduled for Wednesday morning, while Micron Technology is set to report its earnings later in the day. These events are poised to provide further insights into the economic landscape and potentially influence market trajectories.

European markets experienced a rebound on Wednesday, with stocks climbing and shaking off the pessimism from the previous session’s downturn. However, economic indicators suggest caution; German consumer sentiment is projected to decline in July, halting a four-month streak of gains. Concurrently, French consumer confidence dipped to 89 in June, as reported by the country’s national statistics office.

Australia was lower on the day as the headline inflation rate increased, reaching 4%, a notable rise from April’s 3.6%. However, industry giants like Taiwan Semiconductor Manufacturing Company, SK Hynix, and MediaTek also saw their shares climb by 1.38%, 4%, and 3.25% respectively. These gains underscore the robust demand for semiconductor technology, which is a critical component in a wide array of consumer and industrial products, amidst a challenging inflationary environment.

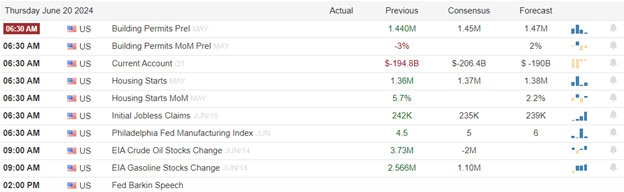

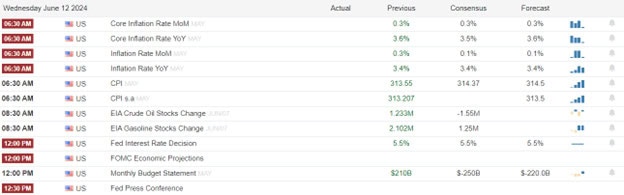

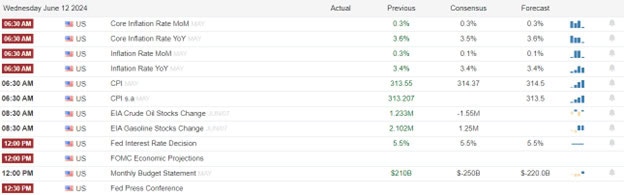

Economic Calendar

Earnings Calendar

Notable reports for Wednesday before the bell include GIS, PAYX & UNF. After the bell include MU, AVAV, CNXC, FUL, LEVI, MLKN, & WD.

News & Technicals’

FedEx’s stock experienced a remarkable surge, climbing over 15% after the market closed on Tuesday, following the announcement of their fiscal fourth-quarter results. The company not only exceeded analysts’ expectations in terms of earnings and revenue but also highlighted its ongoing $4 billion cost-cutting initiative, which includes merging its air and ground operations. This strategic move is aimed at streamlining processes and improving efficiency. The positive financial report, coupled with a reduction in capital expenditure, reflects FedEx’s commitment to optimizing its business model and strengthening its market position amidst challenging economic conditions. The after-hours leap in share price is a testament to investor confidence in FedEx’s restructuring efforts and future prospects.

Volkswagen’s strategic move to invest up to $5 billion in the electric vehicle startup Rivian marks a significant shift in the automotive industry’s transition towards sustainable transportation. The initial commitment of $1 billion underscores the confidence Volkswagen has in Rivian’s potential to disrupt the market. The subsequent investment of $4 billion, contingent upon the successful formation of a joint venture, reflects a long-term vision for collaboration and innovation. However, despite this substantial financial backing, Rivian’s stock performance has been underwhelming, with a decline of approximately 49% in 2024. This juxtaposition of robust corporate support against market skepticism highlights the volatile nature of the EV sector and the challenges that new entrants like Rivian face in a rapidly evolving market landscape.

Ooredoo’s recent partnership with Nvidia represents a landmark development for technology in the Middle East. This collaboration, Nvidia’s first significant foray into the region, involves the deployment of thousands of Nvidia’s GPUs across 26 data centers spanning Qatar and five other countries: Kuwait, Oman, Algeria, Tunisia, and the Maldives. While the financial details remain undisclosed, the strategic implications are clear. These powerful GPUs will be instrumental in processing vast quantities of data, fueling AI chatbots and various tools that are crucial to the AI infrastructure of these nations. This move not only enhances Ooredoo’s data capabilities but also signifies the growing importance of AI technology in global telecommunications and the pivotal role of the Middle East in the tech industry’s future.

The QQQ celebrated on Tuesday as the tech giants reverse lead by the AI darling NVDA. Unfortunately, the DIA and IWM also reversed as the rush back into tech reversed taking way the nice gains of Monday. I suspect the price volatility will continue as the market focus will soon turn to the looming market-moving data coming Thursday and Friday. Plan your risk accordingly.

Trade Wisely,

Doug