As solid beat by NFLX and early morning news of a draft Brexit

deal is making the bulls very happy this morning. The QQQ now looks ready to lead the way and challenge

all-time highs in the index. Still ahead

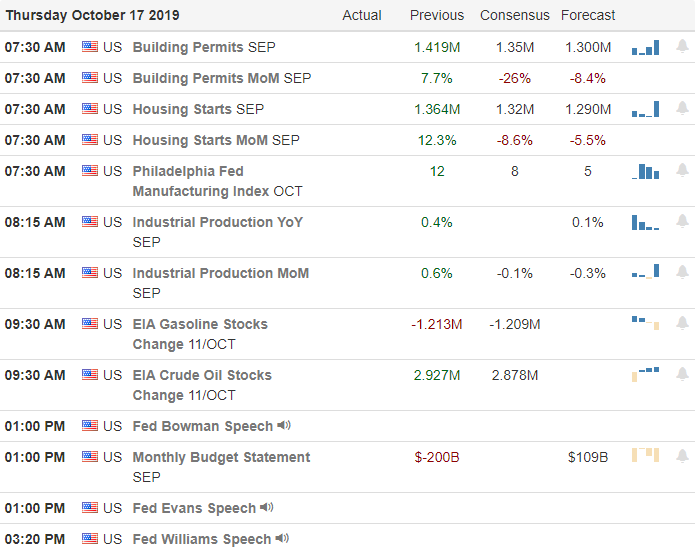

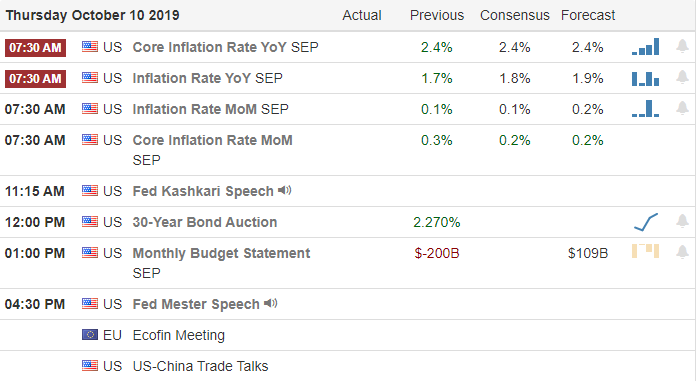

is our biggest day of earnings reports this week with a busy morning of Economic

reports for the market to digest before the open. Though I’m rooting for the bulls, we have to

remember that the bears are unlikely to give up easily. Traders should be careful not to chase

morning gaps into resistance highs with the fear of missing out and remember

pop and drop pattern can occur in this area.

During the night, Asian markets closed mostly lower as China issued threats of no deal if December tariffs are not removed. However, European markets are green across the board this morning after news of a draft Brexit raises hopes. US Futures also quickly responded higher this morning on the Brexit news pointing to a bullish open ahead of a big day of possible market-moving events.

On the Calendar

On the Thursday Earnings Calendar, we have our biggest day

of reports this week, with over 75 companies reporting results. Notable reports include ETFC, BBT, DHR, DOV,

EXPO, GPC, HON, ISRG, IVZ, KEY, MTB, MS, PM, SKX, SNA, STI, TSM, & UNP.

Action Plan

After what the UK is calling a last-ditch effort, a new

Brexit deal has emerged lifting hopes as October 31 deadline approaches. Now the question to be answered will Parlement

ratify the deal? European markets surged

higher on news of the draft agreement as did the US Futures. Yesterday the market languished in a sideways

chop after a disappointing Retail Sales number that showed even online sales had

declined. On the bright side, builder

stocks sharply rallied along with building material providers.

Last night solid earnings beat my NFLX may clear the path

for the QQQ to reach out and test record highs in the index even though IBM

disappointed investors. With the NASDAQ

surging and a possible Brexit deal, the US Futures are suggesting a gap up open

ahead of the biggest day of earnings reports this week and a busy Economic

Calendar with several possible market-moving reports occurring before the

opening bell. That means anything is

possible this morning, but as of now the bulls are in control and seem determined

to test all-time market highs.

With a solid kickoff to earnings season, JPM and UNH inspired

the bulls to test price resistance levels in the indexes. Hopeful reports of a Brexit deal yesterday has

now stalled according to reports as the deadline quickly approaches. We have a busy morning of earnings reports and

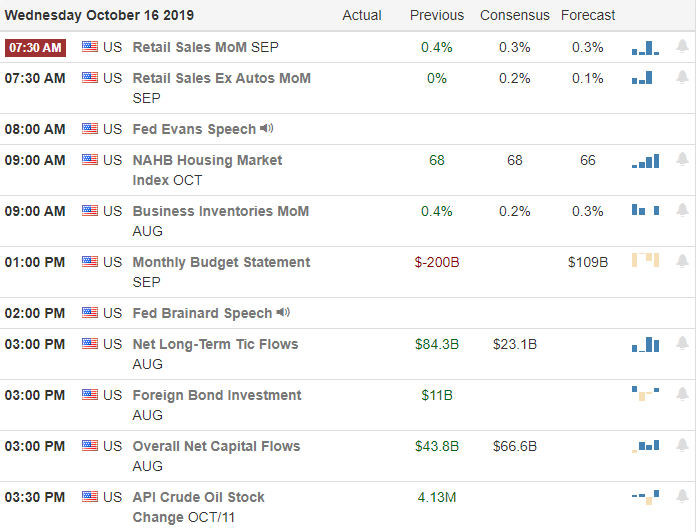

a very important Retail Sales number at 8:30 AM Eastern for the market to digest

before the open today. BAC got the ball

rolling this morning with an earnings beat, but the futures seem a bit cautious

this morning with all the political uncertainty.

Asian market closed trading mixed but mostly higher as hope

news of a draft Brexit deal lifted spirits.

European markets bounce between negative and positive this morning as they

weigh the possible outcomes of Brexit.

US Futures traded in the red most of the night, and this morning

continues to suggest a modestly lower open ahead of early morning earnings and

retail sales reports.

On the Calendar

We have more than 50 companies reporting earnings on the

second day of earnings season. Notable reports

include IBM, ABT, AA, ALLY, BAC, BK, CCI, CSX, KMI, NFLX, PYPL, PNC, STLD,

& USB.

Action Plan

Good earnings reports in JPM, UNH, hopeful Brexit deal news,

and tech analysts upgrades lead to a broad-based rally to challenge price

resistance in the indexes. After

climbing sharply throughout the morning session, upward progress stopped about

as suddenly as is began spending the remainder of the day in a narrow range

chop zone. This morning we’ve learned that

the Brexit negotiations have stalled, BAC had better than expected earnings,

and Moody’s declared a high risk of global recession in the next 12 to 18

months.

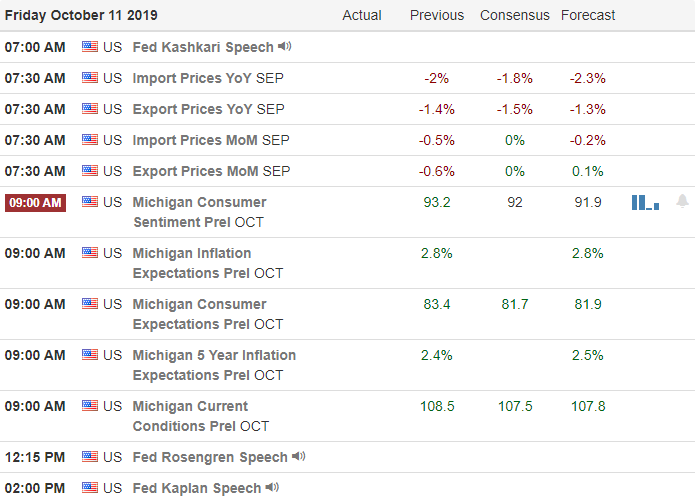

Ahead of a busy morning of earnings reports and a Retail

Sales report, futures point to a modestly lower open at the time of writing this

report. I think the big question remains

can companies produce earnings to support these high prices during an extended

trade war as economies slow around the world? The Big Banks are getting it done, so let’s hope

we see that trend continue with big tech reports beginning this afternoon when

NFLX and IBM reports. Technically speaking,

the bulls are in control with all four major indexes above their 50-averages. However, they remain challenged by downtrend and

price resistance levels that have proved tough to breach with so much political

uncertainty weighing heavily on the market.

Although there seems to be swirling political uncertainty everywhere the market will not turn its primary focus to the beginning of the 4th quarter earnings season results. JPM has already let the way this morning with a solid beat gaping the stock higher and emboldening the bulls in the futures market. Let’s hope the other big banks can do as well this week as earnings ramp-up in the weeks ahead.

Overnight Asian markets closed mixed as traders remain cautious on the proposed Phase 1 deal that many are now calling a temporary cease-fire. European markets are mixed but mostly higher as EU negotiator gives hope of Brexit deal this week. US Futures are currently green across the board as big bank earnings roll in this morning. As of now, futures point to gap up of more than 100 Dow points, but that could easily improve or sharply diminish so expect volatility and stay focused on price action for clues forward.

On the Calendar

Today begins 4th Quarter earnings with 42

companies on the Earnings Calendar expected to report. Among the notable reports are C, JPM, KEY,

BLK, SCHW, TACO, GS, JBHT, JNJ, PGR, PLD, SNBR, UAL, UNH, WFC & WIT.

Action Plan

How we deal with today depends very much on how the market

responds to the early morning earnings reports.

Futures seem to have considerable confidence that the results from the

big banks this morning pointing to more than a 100 point gap up open. According to reports very early this morning,

one of the Brexit negotiators says a deal is still possible this week, creating

a rally in the sterling. We, of course,

will have to watch closely for developments in the Phase 1 deal is being renamed

by some as merely a temporary cease-fire in the trade war. Tariffs on China will increase to 30% in

December if the deal fails. Attempting

to punish Turkey for its Syrian invasion the President has raised steel tariffs

on the country to 50% and cleared the administration to pursue all available economic

sanctions.

Though all this political uncertainty has made for very challenging price action focus will likely turn to earnings results as 4th quarter reports ramp up this week. With the DIA, SPY, and QQQ holding above their 50-day averages with significant gaps below, we will need some sold results to prevent prices from sliding into the gap. As I write this, JPM has reported positive earnings results and is gaping higher. Let’s hope the other big banks can do the same settling frayed trader’s nerves and put some structure back into the chart technical’s without all daily reversals and whip.

Friday’s huge short squeeze rally seems the market seems to

be struggling this morning with the very vague so-called Phase 1 deal as China

now says they need more discussion before signing anything. Over the weekend, we’ve also learned that the

Brexit deal is once again proving elusive with the Sterling reversing Friday’s

hopeful gains. We also know the conflict

between Turkey and Syria has escalated and that Hong Kong protesters are

talking about scaling back on their activities.

What a difference a weekend can make!

Asian markets closed green across the board overnight, but

that sentiment has not translated into bullish notions in Europe, which are

currently seeing red across the board this morning. US Futures have recovered from overnight lows

as the vague Phase 1 deal may be harder to close than the hopeful market initially

thought. With today being a banking

holiday and 4th quarter earnings beginning Tuesday a light and

choppy day would not be out of the question after a what could be a volatile

open.

On the Calendar

Because it’s the national holiday Columbus Day banks and

bond markets will be closed today. As a

result, we have no Economic Calendar reports today.

We have just nine companies reporting earnings today, but none

are particularly notable and unlikely to be market-moving. However, keep in mind, the official beginning

of the 4th quarter earnings begins Tuesday morning with several big

banks reporting.

Action Plan

What a difference a weekend can make. After a huge short squeeze rally that closed

the Dow over 300 points higher on news of a partial trade deal. This morning the news seems to have reversed,

suggesting that China needs more discussion before a possible deal can be

signed. Details of the so-called Phase 1

deal have been few and far between; in fact one could argue extremely vague. By the way, how many Phases are there? In other news, the conflict between Turkey

and Syria has escalated over the weekend with Turkey preparing to invade a northern

Syrian city.

The positive news of Brexit progress seems to have also

shifted as many not suggest Britain will need to ask for another extension which

the Prime Minister is not in favor of doing.

On a technical basis the DIA, SPY, and QQQ are now well above their

respective 50-day averages but have left significant gaps behind as well as not

so confident shooting start candle patterns behind. As I write this report, futures are pointing

to lower open but rallied to cut the overnight lows almost in half. I would not be at all surprised to see the

overnight lows tested after the open.

With today being a banking holiday with the bond markets closed, I’m

expecting a light and choppy price action after the morning rush as we wait for

the official kick-off the 4th quarter earnings on Tuesday.

Abounding optimism of a trade deal has the market surging higher this morning even though we have not seen any details as to what negotiations have produced. Will there be a deal, a partial deal or could this morning gap be irrational exuberance? Could this trigger a huge short squeeze that drives short traders of the market, or might this create a big pop and drop pattern if we learn there is no deal and tariffs increase next week? The bigger question is, how will you manage your risk as we head into the weekend if we have no answers to these questions by the close of today?

Overnight Asian markets closed the week green across the

board on trade optimism. European markets

are also decidedly bullish this morning amid rising hopes of a Brexit deal

coming together. US Futures point to a

wildly bullish gap up open of more than 250 Dow points as the President, and

the Vice-Premier conclude the 2-day meeting today. With such an emotionally charged market, remain

flexible and prepare for volatile price action in reaction to trade

developments.

On the Calendar

We have 14 companies expected to report on the Friday

Economic Calendar. Notable reports include

FAST and INFY before the open today.

Action Plan

Looking at the US Futures this morning, I’m honestly speechless

at the huge bullishness this morning after positive comments on negotiations

with early today. It seems we’ve been

down this road before that ended with no deal, but the market is wildly this

morning even though there have been no details released. Perhaps we’ll know more later today but be prepared

for potential violent volatility as the news rolls out. There is also hopeful news from across the

pond that the British Prime Minister and the EU have found some common ground after

reporting a path to a Brexit deal is improving.

Today’s huge gap up could trigger a big short squeeze

forcing the market even higher. T2122

could easily swing from short-term oversold to short-term overbought all at

once, making a mess of the chart technical.

We should also not rule out the possibility of a pop and drop pattern

that could quickly develop if the trade news happens to spin the opposite direction. The big question for me is, what happens if

we hear no details on trade negotiations until after the market closes? How much risk are you willing to hold into

the weekend? Plan carefully and remain

focused on price as the emotionally charged market could provide a very wild

ride today.

During the evening and night, we saw just how sensitive to

news reports and how emotionally charged the market has become over China’s trade

developments. While the markets seem to hold

on the notion of a partial deal coming together in the high-level talks, reports

suggest the 2-day meeting may have shortened to just today. Stay tuned, stay focused, and stay very

directionally flexible as each new report could substantially move the market violently. Plan your risk carefully.

Asian markets recovered early losses by the close of the day

on conflicting reports regarding trade.

European markets are trade cautiously mixed as negotiations resume in

Washington DC. US Futures recovered from

steep losses during the evening and indicated just how quickly market sentiment

could shift as news on progress or non-progress of the negotiations rolls

out. Remember, an October tariff

increase to 30% will happen unless something changes with the US/China

relationship.

On the Calendar

On the Thursday Earnings Calendar, we have our biggest day

of reports this week, with 25 companies fessing up to results. However, there is only one DAL, which is

reporting before the opening bell that’s notable.

Action Plan

Conflicting news reports created a wild night of price

action that saw futures collapse more than 200 points but recovered to near

falt this morning. That’s a clue to just

how emotionally charged and sensitive the market has become over any news on the

high-level talks today. It sounds as if

the China negotiations may start and end today rather than the planned 2-day

schedule. What we know as of now is that

tariffs on 250 billion dollars of Chinese products will increase from 25% to

30% on October 15th.

Traders should prepare for the possibility of very violent

price moves as news comes out concerning the progress of the talks. Technically, speaking the indexes are at a

critical crossroads, with prices hanging just below declining 50-day moving

averages and substantial price resistance just above. With such unstable price moves, this can

become a day-traders market due to will price action fluctuation and the

overnight reversal risks. Carefully plan

your risk and remain very directionally flexible as we wait for news on trade

negotiation developments throughout the day.

The markets gap down and run south as tough talk between US

and China dims the chances of a trade deal Tuesday. However, Wednesday morning, an unnamed

official says China is willing to make a partial deal, but unwilling budge on

any of the core issues and, the market gaps up as this ridiculous price whip continues

to chop trader’s account to pieces. Before

you jump into this morning’s gap keep in mind the indexes continue to show current

downtrend with 50-day averages in decline.

Fool me twice, shame on me!

Asian markets closed mixed and mostly lower on the uncertainty

of trade talks that begin on Thursday.

Responding to the Bloomberg report and hopefulness of a partial trade deal

European markets are higher across the board this morning. US Futures rose sharply after the 6 AM news

story and indicate the Dow will gap up between 150 and 200 points at the open

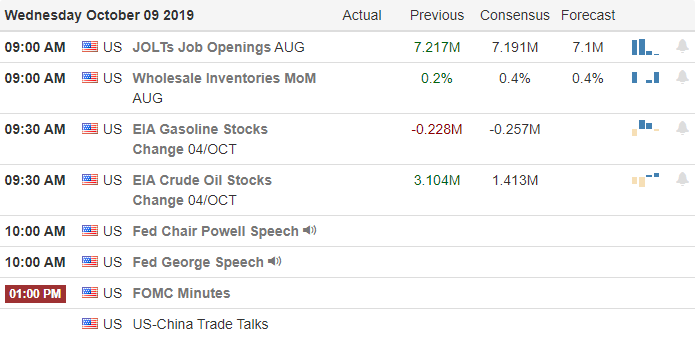

as we wait for the release of the FOMC minutes later today.

On the Calendar

On the hump day Earnings Calendar, we have just eight

companies reporting their results today, but none are market-moving or

particularly notable.

Action Plan

At 6 AM, Bloomberg reported that an unnamed official close

to trade negotiations that China is willing to make a partial deal. The news quickly spiked the Dow Futures higher

at one point, suggesting a 200 point gain at the open. Apparently, China is willing to commit to purchasing

of farm products if the US stops tariff increases. However, they are unwilling to budge on any of

the major sticking points. The President,

in the past, said tariffs are to increase on OCT.15th if no progress

is made on a bilateral deal. I guess the

good news is that at least today’s gap is to the upside! Trade negotiations begin this Thursday, stay

tuned for future gaps and whips in price.

According to reports, Turkey is about ready to invade Syria,

as US troops pull back as the President attempts to fulfill a campaign promise

to bring our troops home. The UN has

reported they are in a desperate financial situation and may not be able to pay

staff by November because so many countries have failed to pay their dues,

making their peacekeeping operations impossible. Technically, speaking the indexes are in a

current downtrend with declining 50-day averages amidst so much swirling

uncertainty. Be careful not to chase

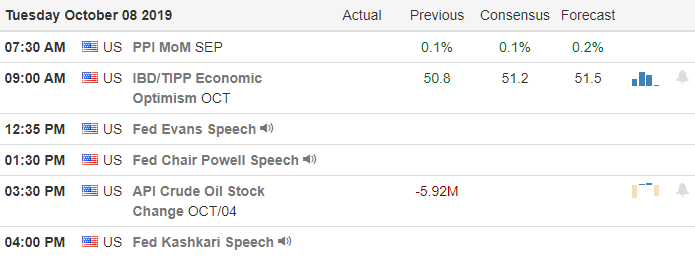

this morning’s gap, and remember we have the FOMC minutes release at 2:00 PM Eastern

this afternoon.

With the indexes leaving behind shooting star candle patterns

at price resistance levels yesterday seems to suggest that trader’s hopes of

progress in the coming trade talks have diminished. Reports that Brexit talks could be failing is

not helping as currencies fluctuate, and Oct. 31 deadline quickly approaches. Growing unrest between Turkey and Syria due to

the Presidents decision to withdraw US Troops and increasing tensions between

Iraq and Ecuador rising oil prices, it’s no wonder market prices continue to so

volatile and extremely challenging to trade.

It’s truly a day-traders market with all the unrest and news sensitivity

and changes market direction in half a heartbeat.

Asian market rallied to close green across the board last night

as China television banned NBA broadcasts over Hong Kong protest comments. European market are however decidedly bearish

this morning as trade hopes sink and a no-deal Brexit grows. US Future points to a substantial gap down

this morning as it faces so much uncertainty in the coming days.

On the Calendar

On the Earnings Calendar, we have 11 companies reporting

quarterly results today. Notable reports

include HELE, LEVI, and DPZ.

Action Plan

Reports this morning suggest Brexit talks are breaking down quickly

hit the currency markets as the sterling fell in reaction. The President’s decision to bring US Troops

home from Syria has drawn rebuke from his most staunch supports in Congress and

increasing the likelihood that Turkey will invade Syria further destabilizing the

region. Oil prices are on the rise this

morning, with increasing tensions between Iraq and Ecuador escalate. Ahead of trade negotiations, the US dollar is

pulling back, and gold is on the rise this morning, and the Chinese media

suspends NBA broadcasts over comments supporting Hong Kong protests.

Top off all this unrest with tough talk from China and hopes

of a productive outcome of this week’s talks seems to have greatly dimmed this morning. With the index charts testing price

resistance levels yesterday and leaving behind bearish shooting star patterns, a

pullback to is not a big surprise.

However, the futures seem to be painting a grim picture this morning with

a substantial gap down expected amidst all the swirling uncertainty. I continue to expect unruly and price action driven

by the news reports that can chop a trader’s account to pieces.

After a big short squeeze rally in reaction to the jobs

number that suggested a 2020 recession is less likely but left the door open for

more rate cuts, the US indexes are once again knocking on the door of price resistance. With trade talks set to resume this week and threatened

tariff increases scheduled next week, traders should prepare for a news-sensitive

market. As protests continue to disrupt

Hong Kong and amidst impeachment proceedings, perhaps an interim agreement could

be reached to at least delay future tariff increases by both countries, but I

wouldn’t hold my breath in anticipation.

Last night Asian markets closed down across the board with all eye on the forthcoming trade talks. European markets are, however, cautiously bullish this morning ahead of trade talks and a rapidly approaching Brexit deadline. US Futures have rallied substantially off of overnight lows but continue to suggest a slightly lower open as uncertainty swirls and with significant technical resistance levels just above. With little on either the earnings and economic calendar for the market to react to, I would not be surprised to see a choppy price action today.

On the Calendar

On the Earnings Calendar we have just eight companies expected

to report today, but none of them are particularly notable.

Action Plan

The Employment Situation report Friday was strong enough to ease

concerns of a US recession in 2020 but not so strong that the market still

believes in another rate cut is on the way.

Combine that with a short-term oversold condition, and short squeeze trigger

huge rally right back into price resistance levels. As the US and China prepare to resume trade

talks this week, the news spin cycle it running at full speed likely to create

will price swings as they speculate on the outcome. Many are hoping for at least an interim agreement

to stop that would stop the possible tariff increases set to increase next

week.

With the ongoing Hong Kong protests and impeachment proceedings,

both countries have good reason to get this frustration behind them, but I would

not expect either side to give in easily.

Futures have rallied this morning off the overnight lows that had

suggested a substantial gap down. With

no notable earnings to react to and a very light economic calendar, expect the

market to be very new sensitive with choppy price action. The indexes have substantial price resistance

levels above to deal with, and after a 2-day rally of more than 800 Dow points,

a little rest or consolidation would not be a big surprise as we wait for trade

talks to resume.

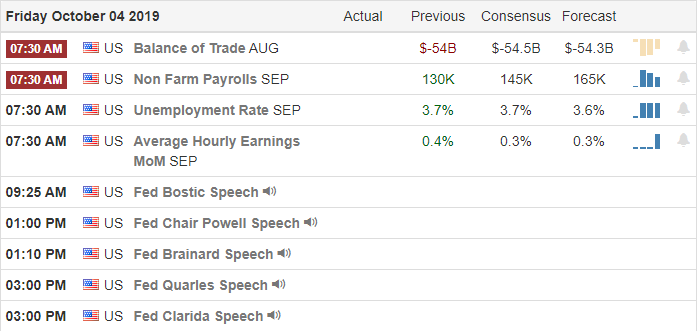

With the world is watching and inquiring minds wait in anticipation for the release of the Employment Situation number and how it will impact today’s open. Can it provide the bullish inspiration needed to follow-though on the hopeful bullish hammer patterns left behind yesterday, or will is disappoint adding fuel to the fire of a slowing US economy? How we end this trading week will greatly depend on this key metric and will shape how the market opens today.

Asian markets were mixed overnight as Hong Kong imposes emergency

law as anti-China protests continue to disrupt the city. As of the writing of this report, European markets

are mixed but mostly higher, but expect that also greatly fluctuate depending

on the result of the US Employment numbers this morning. US Futures are currently pointing to a lower open,

but that’s likely to change significantly after the 8:30 AM release of the

Employment number. Buckle up; it could

be a volatile end to a week of technically damaging and tumultuous price action.

On the Calendar

On Friday’s Earnings Calendar, we have just five companies

reporting results today with none that would say are market-moving or particularly

notable.

Action Plan

Our last notable earnings report for the week, COST,

slightly beat on estimates but seems to have disappointed investors that were

hoping for a strong showing for the quarter.

Interestingly that single report seemed to influence the trading of the

overnight futures. Protests continue to have

damaging impacts on Hong Kong after the city declared emergency law last

night. This morning’s total focus of the

market focus on the Employment Situation number that comes out an hour before

the market open. The consensus is

expecting 145K jobs with a low range of 120k and upper range of 179k. Of course a surprise beat or miss of the key

metric could have a profound impact on how the market opens today.

Yesterday the Dow briefly dipped below it’s 200-day moving

average while the SPY and QQQ managed to bounce before reaching this key support. Unfortunately, the IWM is well below the 200-day

average and will soon display the death-cross with the 50-day dipping below its

200-day. All the indexes experienced a

nice bounce rally yesterday leaving behind hammer candle patterns seen as

potential bullish. However, if price

action is unable to follow through to the upside today the significance and hopefulness

of the hammer pattern diminishes dramatically.

Thus, there is a lot at stake for the Employment Situation report, and

the world is watching.