Yesterday we were reminded that bears are still around and hungry. It was all big tech holding up the market yesterday as most everything else slipped sideways or south. Their market dominance is clear, but one must wonder how much longer tech can maintain this buying pressure as valuations soar and P/E ratios hit new record highs. If nothing else occurred yesterday, the bears gave us a warning not to become complacent. Stay with the trend but stay focused and flexible because bear attacks and price volatility could signal a top is near.

Asian markets closed mixed overnight in a choppy market session. European markets are primarily bullish this morning, keeping an eye on the muted global sentiment. Ahead of the JOLTS number and the FOMC minutes, U.S. futures are trying to shake off yesterdays selling as the QQQ gaps to yet another record high as the big tech party continues.

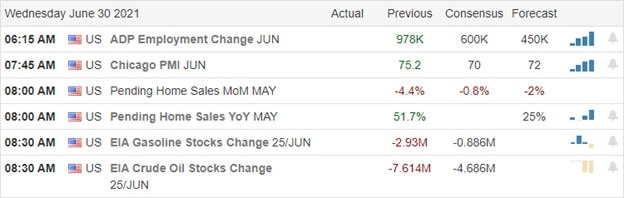

Economic Calendar

Earnings Calendar

On the Wednesday earnings calendar, we have just eight companies listed and only four verified reports. Notable reports include MSM, SAR & WDFC.

News & Technicals’

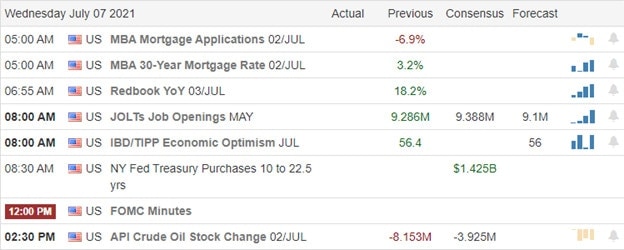

With mass pandemic vaccinations continuing across the country, health officials warn we could see a harsh flu season this winter due to the minor season in 2020. Biden is now suggesting door-to-door efforts to increase the number of vaccinations in areas where there are low acceptance rates. At the same time, France is preparing a new law to make the Covid vaccination compulsory for those in the health care industry. The European Central Bank is now raising its forecast to a 4.8% growth rate this year with 4.5% in 2022, raising some inflationary concerns. China’s crypto-crackdown called for the shutdown of a company “suspected” of providing software services for virtual currency transactions. With the FOMC minutes just around the corner, the 10-year Treasury yield dipped this morning to 1.338%, and the 30-year fell to 1.967%.

The bears reminded us yesterday that they are still around and hungry, with the IWM testing its 50-day average and the DIA suggesting a possible test. However, trends remain bullish, and the rally back yesterday afternoon raises the question if the bears have the energy to follow through on yesterday’s threat. That said, the VIX indicated a modest increase in fear, and the Absolute Market Breadth Index saw its first increase in days on the selling wave. So there may be a reason some caution but no reason to run for the door just yet. Instead, consider this a warning shot over the bow not to overtrade or become complacent with valuations so elevated. We know a correction is way overdue and could begin at any time but stay with the trend until then.

Markets opened flat Tuesday. However, then we saw a divergence. The large caps sold off for the first hour or so. Then the DIA ground sideways while the SPY slowly regained ground. Meanwhile, the QQQ climbed back to the morning highs. This left us with Hanging Man candles in all 3 major indices. The QQQ (+0.42%) closed at another new all-time high close, while the SPY (-0.18%) lost slightly (snapping a 7-day winning streak), and DIA (-0.61%) lagged. The VXX gained about two and one-quarter percent to 29.57 and T2122 fell back to 30.99. 10-year bond yields fell sharply to 1.351% and Oil (WTI) dropped almost 2% to $73.72.

During the day the Pentagon canceled the controversial $10 billion contract that had been contested between AMZN and MSFT (MSFT was awarded the contract during the last administration). However, as part of the announcement, it was stated that both companies had been asked to bid on another Multi-vendor Cloud Computing contract, where both companies are likely to get part of the pie. The market took this as a big plus for AMZN (assuming they will get a big chunk of the contract). AMZN gained 4.69% and MSFT was flat on the day.

Recent IPO company DIDI suffered another blow overnight. Chinese regulators had removed the DIDI app from app stores in China late Friday. However, last night the app was also removed from major messaging and payment services. These include Tencent, WeChat, and the Alipay payment service (spun off from BABA). While existing users of the app and who had previously used DIDI through the message platforms or payment system can continue to use it, these moves effectively stop all future growth for DIDI in China.

Mortgage applications fell to their lowest level since before the start of the pandemic this week. The decline was 1.8% and took the total back to the lowest level since January 2020. Counter-intuitively, this fall came as mortgage rates fell over the same period. This, combined with the massive April, May, and June mortgage numbers may mean that the massive housing market boom has peaked.

Overnight, Asian markets were mostly in the red. Singapore (-1.54%), Japan (-0.96%), and Thailand (-0.93%) paced the loses. Meanwhile, Shenzhen (+1.86%) and Australia (+0.90%) led the gainers. In Europe, markets are green across the board as of mid-day. The FTSE (+0.39%), DAX (+0.82%), and CAC (unchanged) are typical of the spread across all European bourses. As of 7:30 am, US Futures are pointing to a green open. The DIA is implying a flat +0.06% open, the SPY implying a modest +0.18% open, but the QQQ is implying a +0.60% gap higher. 10-year bond yields are lower again at 1.345% this morning and the dollar is down slightly, which means commodities are higher at this point.

Major economic news scheduled for Wednesday includes May JOLTS (10 am), June FOMC Minutes (2 pm), and a Fed speaker (Bostic at 3:30 pm). The only major earnings reports scheduled for the day is MSM before the open.

The bulls clawed back from what had been a bad start to Tuesday. It looks like they might be trying to follow through to start off the day Wednesday. The lack of any movement on OPEC+ negotiations may help bulls today, especially in the Oil sector. However, be careful here. The large caps feel a little toppy and the QQQ has been on a heck of a run, which implies a need for at least some rest if not pullback.

All trends reverse at some point and every S/R level is breached eventually. So, don’t just assume trend, support, or resistance will always hold. However, The odds favor following the trend and, as always, respect both support and resistance levels. So, follow those trading rules and stick to the trade plan. Keep taking your profits, moving your stops, and maintaining your discipline. Remember that consistency is the key to long-term trading success. So, book those singles and doubles. Base hits win championships, not the occasional home run.

Ed

Swing Trade Ideas for your consideration and watchlist: No Tickers today. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

With the DIA in striking distance of new highs and the SPY and QQQ closing at new records, there was a lot to celebrate this weekend as the economy recovers. Unfortunately, as the old saying goes, what goes up must come down. Maybe not today, this week, or even this month, but it’s tough to ignore the extraordinary valuations with the SP-500 P/E Ratio’s 93% above the historical 10-year average. Stay with the trend but avoid overtrading and have a plan to protect your capital should the bears come roaring back.

Overnight Asian markets closed mixed but mostly lower as Australia holds rates unchanged. European markets trade flat to slightly lower this morning as oil prices surge to a six-year high after OPEC talks fail to reach a production deal. After a week of daily record highs, U.S. futures are a bit muted this morning, suggesting a mixed to a flat open. Keep in mind volume could be light as traders extend their vacation.

Economic Calendar

Earnings Calendar

As we begin a short week of trading, we have 13 companies listed on the calendar with only three verified reports. The only notable report for the day is the earnings from SGH.

News & Technicals’

After a very bullish run, the SPY and the QQQ begin the week at new record highs, but according to Chris Harvey from Wells Fargo Securities, a ‘day of reckoning is coming for high flying tech stocks. The reasoning for his call is the very high multiples for growth stocks in an inflationary environment. Oil prices jumped to a six-year high after a contentious OPEC meeting that yielded no production deal. Former U.S. Energy Secretary Dan Brouillette, “you could easily see oil hitting $100 a barrel and potentially even higher.’ As we wait for the FOMC minutes coming out on Wednesday afternoon, Treasury Yields moved slightly higher in early morning trading. The 10-year ticked higher to 1.434%, and the 30-year advanced to 2.055%.

Technically speaking, we begin the holiday-shortened trading week in pretty good shape. The DIA is within striking distance of a breakout to a new all-time high while the SPY and the QQQ rest confidently at new records. However, after such a massive 3-week rally, it may not be all sunshine and roses. Valuations are incredibly high, with the SP-500 sitting at a P/E ratio 93% above the historical 10-year average. Big tech-led this rally, and perhaps there is an argument that due to all the money, printing companies can support these lofty valuations. However, it is also easy to argue that a substantial correction is overdue and that the recent rally is nothing more than a blowoff top. My suggestion is to stay with the trend but be very careful not to overtrade because drinking too much of this Kool-aid could be costly should sentiment shift. Don’t become complacent and have a plan to protect your capital should the bears come roaring back.

Markets gapped higher Friday on blowout June Payrolls (+850k and accompanied with an increase in the unemployment rate) and then all 3 major indices slowly trekked higher at varying rates. This left the SPY and QQQ with strong white candles and new all-time high closes. Meanwhile, the DIA printed a nice white gap-up Spinning Top and also eked out a new all-time high close. On the day, QQQ gained 1.15%, SPY gained 0.76%, and DIA gained 0.46%. VXX fell slightly to 28.90 and T2122 actually closed in the mid-range at 69.06 (after being near 100 earlier in the day). 10-year bond yields fell sharply to 1.431% and Oil (WTI) was flat at $75.20/barrel.

Bloomberg reported Saturday that a massive ransomware attack has hit more than 1,000 companies. While the list of victim companies continues to expand, so far it appears the targets have been small-to-medium-size companies who use IT service providers. The service providers (gateway for attack) include SNX, a major (and listed) provider out of Miami.

OPEC+ voted to increase production by roughly 400,000 barrels per day each month for the remainder of 2021 (starting in August) and extend the rest of the production cuts that are in place through the end of 2022. (Analysts had expected the number to be about +500,000 barrels/day.) However, UAE rejected both proposals that block them from taking place. After 2 days of negotiations, talks broke down Monday. No date has been set to resume negotiations, but in the meantime, the OPEC+ meeting scheduled for Tuesday has been canceled. Analysts see oil prices rising in the short-term if OPEC+ fails to reach a deal, but future oil prices are uncertain without a deal as the group members may ramp up production in an effort to capture market share and fill budget deficits from last year. Regardless, WTI Oil is up 1.5% to a 6 year high in the premarket.

Recent IPO DIDI, the Chinese ride-sharing giant that dwarfs UBER in China, is down sharply in premarket. Late on Friday China announced it was forcing all app stores in their country to remove the DIDI app (while still allowing those who already have the app on their phones to continue using it). This comes after the Chinese regulators had “advised” the company to postpone its US listing…and the company did not heed that advice. The reported problem is that the Chinese government needs to “review DIDI app network security.” As of 7:40 am, DID was down 18% from Friday’s close.

Overnight, Asian markets mixed on mostly modest moves. Singapore (+1.58%) was an outlier, with South Korea (+0.36%), Shenzhen (-0.35%), and Hong Kong (-0.25%) being more typical. In Europe, the day has also started mixed. While most of the smaller exchanges are modestly, but firmly green at mid-day, the FTSE (-0.20%), DAX (-0.39%), and CAC (-0.32%) are just as firmly in the red. As of 7:30 am, US Futures are pointing to a mixed and flat open. The DIA is implying a -0.11% open, the SPY is implying a -0.07% open, and the QQQ is implying a +0.09% open.

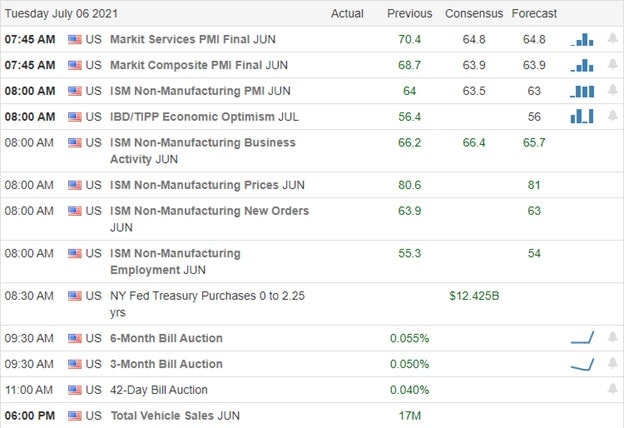

Major economic news scheduled for Tuesday includes June Services PMI (9:45 am), June ISM Non-Mfg. PMI (10 am). There are no major earnings reports scheduled for the day.

The OPEC+ negotiation breakdown (Saudi Arabia vs UAE primarily) is the main market driver this morning. Oil names continue to soar under the feeling that no deal by OPEC+ means that oil production caps will remain in place in the middle-east (leading to higher oil prices). However, the dollar is also up significantly this morning, which will have a muting effect on commodities. For what it’s worth, Treasury yields are just on the red side of flat so far this morning, which would suggest the oil situation has not spawned greater inflation/Fed fear in markets yet.

Follow those trading rules and stick to the trade plan. The odds favor following the trend and, as always, respect both support and resistance levels. However, all trends reverse at some point and every S/R level is breached eventually. So, don’t just assume trend, support, or resistance will always hold. Keep taking your profits, moving your stops, and maintaining your discipline. Remember that consistency is the key to long-term trading success. So, book those singles and doubles. Base hits win championships, not the occasional home run.

Ed

Swing Trade Ideas for your consideration and watchlist: DNMR, LKQ, OKE, RIOT, MARA, UBER, COP, JKS, ZNGA, BP, COF. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

After setting the 35th record high in the SP-500 this year, all eyes will turn their attention to the Employment Situation number released an hour before today’s open. Analysts estimates target 702,000 new jobs and a 5.6% unemployment rate as companies rush to fill open positions. After the reaction to the data, don’t be surprised if the volume quickly declines and price action becomes light and choppy as computers shut down and fireworks begin to light up for the 3-day weekend.

Overnight Asian markets traded mixed with Hong Kong falling 1.80% by the close. Across the pond, European indexes cautiously inch higher this morning, waiting on the U.S jobs data. With bullish anticipation, U.S. futures try to inspire more buying as they trade with modest gains across the board. I wish you all a safe and wonderful weekend as we celebrate Independence Day. Let’s all take a moment to reflect on the sacrifices of those that came before us to win our freedom and those standing in harm’s way today protecting us and ensuring that blessing!

Economic Calendar

Earnings Calendar

The Friday calendar is a light one with just five listed companies and only one verified report coming from WTER, which is not particularly notable unless you happen to own the small-cap stock.

News & Technicals’

According to reports, a new Tesla Model S Plaid caught fire while operating with the driver behind the wheel. Apparently, the driver noticed smoke coming from the rear of the car and had to force his way out of the vehicle because the locks malfunctioned. The fire required two firefighter crews more than three hours to put the fire out. Billions of venture capital dollars flowed into online grocery start-ups in 2021, attempting rapid delivery services. With more than $10 billion invested in all the start-ups, some suggest the sector is now overcrowded. We have a new space race underway with Richard Branson aiming to beat Jeff Bezos to space with plans to launch his own Blue Origin rocket on July 20th with himself aboard. Micron CEO sees immense growth ahead for semiconductors as electric vehicles become what he called ‘data centers on wheels.’

Today is all about the Employment Situation report with analysts targets of 702,000 new jobs and the unemployment rate falling to 5.6%. The question to be answered is if that will keep the bulls engaged, or will the bears see that as a sign of an overheating economy? There is no doubt that the bulls are in control, with the SP-500 setting its 35th record high this year! With the FOMC continuing to print, the melt-up continues even as the Absolute Breadth Index continues to decline. A growing number of analysts and large investors warn of a substantial correction, so don’t become complacent but stay with the trend as long as it lasts. After we get past today’s reaction to the jobs, data volume is likely to drop like a rock as everyone’s attention will turn toward the 3-day weekend. I wish you all a safe and happy 4th of July!

Markets opened essentially flat Thursday, with a sideways grind that followed showing a slight uptrend in the large-caps. All 3 of the major indices closed near the highs of the day. The QQQ printed a sort of Spinning Top or Doji, while the DIA printed a sort of Hanging Man candle, and the SPY printed a strong white almost Marubozu. On the day, SPY gained 0.57% (to close at another all-time high close), DIA gained 0.41% (now less than half a percent below the all-time high close), and QQQ gained 0.04%. The VXX fell 1.5% to 28.99 and T2122 jumped higher, but remains just outside the overbought territory at 75. 10-year bond yields rose to 1.466% and Oil (WTI) gained over 2% to $74.96.

During the day, Treasury Sec. Yellen announced that 130 countries have agreed to the Biden Administration proposal of a global minimum corporate tax of at least 15%. It was not announced whether low-tax havens such as Ireland have come around. However, this momentum could have large repercussions for stocks, as many of the stock market names pay far less than the proposed minimum. For example, AMZN, AAPL, FB, GOOG, NFLX, BA, INTC, PFE, GM, and many others pay far less than even the bottom (15%) number being discussed.

Most of the major car makers reported Q2 sales Thursday. GM reported a 40% increase year-on-year and a 7% increase from Q1. This was a little shy of analyst expectations. TM saw a 73% increase year-on-year and a 14% increase from Q1, which was above estimates. This marks the first time ever the Toyota has outsold GM for a quarter. F will report their numbers today. The question then will be whether F retains the crown as the best-selling automaker in the US.

In miscellaneous stock news, SPCE has bumped up its launch date for its first passenger flight into space to July 11. (The idea is for Richard Branson to beat Jeff Bezos to become the first civilian in space.) SPCE is soaring in premarket on the news. Despite Wednesday’s record fine, Robinhood has filed for an IPO and will trade on the Nasdaq under the ticker HOOD.

Overnight, Asian markets were mixed yet again, with China showing huge moves to the downside relative to a muted rest of the region. Shenzhen (-2.45%), Shanghai (-1.95%), and Hong Kong (-1.80%) were outliers to the downside as the rest of the region saw modest moves in either direction. In Europe, markets are green except for a could small outliers (Greece and Denmark). However, this is also on modest moves as the world waits on US Payroll data. The FTSE (+0.18%), DAX (+0.37%), and CAC (+0.07%) are typical of the continent. As of 7:30 am, US Futures are pointing to an open on the green side of flat an hour. The DIA is implying a +0.05% open, the SPY implying a +0.08% open, and the QQQ implying a +0.19% open at this hour. In addition, 10-year bond yields are down to 1.446%, the dollar is slightly positive, and commodities are mostly in the green in front of the big data dump.

Major economic news scheduled for Friday includes Jun Avg, Hourly Earnings, Jun Nonfarm Payrolls, Jun Participation Rate, Jun Unemployment Rate, and May Trade Balance (all at 8:30 am), and May Factory Orders (10 am). There are no major earnings reports scheduled for the day.

The big Payroll data is likely to call the tune for Mr. Market this morning. Economists are expecting that 706k jobs were added, that unemployment fell to 5.6% , and that average hourly earnings rose 0.3% in June. We’ll have to see how close to the mark those forecasts end up being. The trend remains positive, but it is looking weary. (Or is it just resting in the climb?). Regardless, in front of a long weekend, it might be wise to take profits, move stops, lighten up, and/or put hedges in place. Trade smart, it’s your money whether you hold the cash or leave the bet on the table.

Follow those trading rules and stick to the trade plan. The odds favor following the trend and, as always, respect both support and resistance levels. However, all trends reverse at some point and every S/R level is breached eventually. So, don’t just assume trend, support, or resistance will always hold. Keep taking your profits, moving your stops, and maintaining your discipline. Remember that consistency is the key to long-term trading success. So, book those singles and doubles. Base hits win championships, not the occasional home run.

Ed

Swing Trade Ideas for your consideration and watchlist: HES, CTLT, BYD, FB, BOX, GRWG, FOLD. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Though the DIA has struggled as the weakest index of late, the bulls went to work yesterday defending its 50-day average, and the technical picture improves. Big tech continues to dominate with the SPY, closing at its 34th record high of the year. The Absolute Breadth Index shows a substantial divergence from the indexes and suggests we stay focused and avoid complacency. However, stay with the bullish trend as long as this buying frenzy continues.

Asian markets traded in the red across the board overnight as a private survey shows Chinese factory activity slowed in June. European markets trade mixed but near the flatline this morning as they wait on the jobs data. U.S. futures are trying to kick off the second have of the year bullishly as we wait on Jobless Claims, PMI, ISM, & Construction Spending numbers.

Economic Calendar

Earnings Calendar

We have a light day on the earnings calendar as we begin the 3rd quarter with just 11 companies listed on the earnings calendar with several unconfirmed. Notable reports include WBA, AYI, &MKC.

News and Technicals’

As China celebrates the anniversary of its Communist regime, it will not accept sanctimonious preaching from others. FINRA said it fined Robinhood $57 million and ordered the stock trading app to pay nearly $13 million in restitution to thousands of clients. FINRA considered the widespread and significant harm suffered by customers, including millions of customers who received false or misleading information from the firm. Due to semiconductor shortages, analysts estimate automakers sold about 4.5 million vehicles in the second quarter as signs of a slowdown continue. Treasury yields are slightly higher this morning ahead of the Jobless claims, with the 10-year trading up to 1.475% and the 30-year advancing to 2.101% early this morning.

The technical picture of the indexes continues to improve, with the bulls defending the 50-day average as support on the DIA. Although the QQQ suffered a little selling, the index remains exceeding strong, as is the SPY, with the tech giants leading the way. That said, momentum continues to be a bit of a concern, with more stocks stuck slipping sideways down than those moving bullishly as the Absolute Breadth Index declines as the indexes push upward. This glaring divergence may mean nothing, but it should serve as a warning not to overtrade or become complacent if the bulls stumble or simply run out of energy. However, until that occurs, stay with the trend and ride this buying frenzy as long as it lasts. Remember, as you plan forward, we have a three-day weekend ahead, and volumes could become light, and price action could become choppy rather quickly after economic data releases as traders hit the road to celebrate the 4th.

Markets opened flat on Wednesday as we saw another sideways grind all day in the SPY and QQQ. The DIA did similar, but managed a slightly positive trend to its grind. This action left us with a Doji Harami in the QQQ, a small Bullish Engulfing with upper wick in the SPY, and a larger Bullish Engulfing in the DIA. On the day, DIA gained 0.60%, SPY gained 0.09% (to a new all-time high close), and QQQ lost 0.16%. It is worth noting that all the major indices closed Q2 at or very near all-time highs The VXX fell a percent to 29.46 and T2122 rose slightly to 44.12 (still in the mid-range). 10-year bond yields fell to 1.465% and Oil (WTI) gained a tad to $73.51/barrel.

In economic news, ADP Nonfarm Employment came in almost 100,000 higher than expected. However, it was the May Pending Home Sales that was the big news. It had been forecast to fall almost 1%, but came in up 8.0%. That massive beat was very unexpected and may inform the much lower than expected mortgage demand recently. In short, the sales may have already been booked in April and May.

During the day Wednesday, Robinhood was fined a record $70 million by FINRA. This covered $57 million for misleading advertising and another $13 million in restitution to customers for outages that prevented them from exiting trades. Other news during the day included F announcing that it was cutting production in 8 North American plans (6 in the US) for various periods starting next week and lasting at least into August. The cause of the shutdown was a lack of semiconductor chips for F-1150, Bronco, Mustang, and Explorer models.

The major automakers report their Q2 sales today (at unscheduled times). The lone exception is F, which will report the same information Friday. Analysts are expecting to see a 52% year-on-year increase in sales. This would bring Q2 sales totals to 4.5 million vehicles, despite the factory shutdowns and incomplete assembly caused by the global chip shortage.

Overnight, Asian markets were mixed, but leaned to the red side on modest moves. Shenzhen (-0.81%), Australia (-0.65%), and Hong Kong (-0.57%) paced the losses. In Europe markets are also mixed, but lean to the green side as of mid-day, also on relatively small moves. The FTSE (+0.45%), DAX (-0.14%), and CAC (-0.03%) are a good indication of European range. As of 7:30 am, US Futures are pointing to a dead flat open. The DIA is implying a +0.07% open, the SPY implying a +0.021% open, and the QQQ implying a -0.18% open. In addition, 10-year bond rates are moved up with some strength overnight, now at 1.48%. This comes amid Dollar weakness, which is also helping commodities.

Major economic news scheduled for Thursday includes Weekly Initial Jobless Claims (8:30 am), Mfg. PMI (9:45 am), and ISM Mfg. PMI (10 am). Major earnings reports scheduled for the day include AYI, MKC, and WBA before the open. There are no earnings releases scheduled for after the close

With the Dollar falling and both interest rate and commodity prices rising early, the stock market may rediscover some inflation fear today. For example, Crude is back to 2018 levels ($75/barrel). While most of the reallocation trade is done, there may be some retail trader shuffling still to do. So, keep an eye on rotation again. That said, the trend is still decidedly bullish, if a bit weary at this point.

Keep taking your profits, moving your stops, and maintaining your discipline. Follow those trading rules and stick to the trade plan. The odds favor following the trend and, as always, respect both support and resistance levels. However, all trends reverse at some point and every S/R level is breached eventually. So, don’t just assume trend, support, or resistance will always hold. Remember that consistency is the key to long-term trading success. So, book those singles and doubles. Base hits win championships, not the occasional home run. So, don’t try to stretch things and get burnt in the process.

Ed

Swing Trade Ideas for your consideration and watchlist: XPEV, OXY, BP, ERX, AR, XOM, TSLA, IQ, JMIA, RIOT, MARA. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

With a mighty shove by the tech giants, the SP-500 solidified a new record high for the 33rd time this year, with the QQQ set new closing records as well. Unfortunately, most of the move was again encapsulated in the morning gap as we spent the rest of the day choppy sideways in a narrow range. As the 2nd quarter comes to an end, watch for the possible end-of quarter-window dressing with jobs data in focus for the rest of the week.

Overnight Asian markets traded mixed in a choppy session. European markets trade with modest declines across the board this morning as inflation and the rising delta variant become widespread on the continent. Ahead of earnings and economic data, futures point to a modestly lower open as we wait on private payroll data. As you plan forward, keep in mind the Employment Situation number Friday morning and the upcoming 3-day holiday weekend that could see declining volumes.

Economic Calendar

Earnings Calendar

As we finish up the 2nd quarter, we have 11 companies listed on the earnings calendar, with a few that are not verified. Notable reports include BBBY, MU, STX, FC, GIS, and SJR.

News & Technicals’

On this last trading day of June and the end of the 2nd quarter jobs, data will come into focus for the rest of the week. Warren Buffett is one of the only big investors to recognize the highly uneven impact on small businesses during the pandemic. Bailouts and massive amounts of federal money flowed to big businesses while the small on-street business was primarily ignored as regulators forced their closure. There have been calls to ban British visitors into the U.K. in order to stop the spread of the delta variant that is already widespread on the continent. HSBC says Asia faces a‘ bumpy road’ ahead as Covid cases remain high. Still, vaccine rollouts offer hope as countries like India, Indonesia, Malaysia, and Nepal continue to deal with elevated infection rates. Treasury yields are moving lower this morning, with the 10-year down slightly to 1.475% and the 30-year dipping to 2.087%.

For the 33rd time this year, the SP-500 closed at a new record high, with tech giants proving the majority of the lift. But, of course, the QQQ also set a new record while the DIA and IWM turned slightly lower but holding on to crucial technical support levels. The next three days’ jobs data will keep traders and investors on their toes and guess if the results will continue to support these high prices. The SP-500 P/E ratio is now 89% above its historical 10-year average, and one has to wonder just how high can we go with the Fed keeping the stimulus pipeline continuing to pump out 120 billion per month. Futures trade slightly lower this morning with ADP, Chicago PMI, Pending Home Sales, and Petroleum Status number on deck. Please don’t rule out the possibility of the end-of-quarter window dressing and plan your risk carefully as we slide toward the Employment Situation number and the holiday shutdown.

Markets opened basically flat on Tuesday (the DIA did gap a third of a percent higher) and then the 3 major indices ground sideways with a slight trend. As a result, SPY printed a Doji (but at a new all-time high close), the DIA printed a black inside candle closing near the low with an upper wick, and the QQQ printed another nice white candle closing at the highs and at a new all-time high close. Semiconductors led the QQQ higher as SWKS, XLNX, AMD, CRUS, AAPL, QCOM, and AVGO all put in stellar sessions. On the day large-caps closed basically flat, as the SPY gained 0.05%, the DIA gained 0.02%, and QQQ gained 0.36%. The VXX gained 2% to 29.77 and T2122 fell again to 34.97. 10-year bond yields fell a bit to 1.475% and Oil (TWI) gained about three-quarters of a percent to $73.44/barrel.

CNBC reported this morning that Fed data released today indicates that markets may be past their peak level of inflation fear. The data (pulled from FRED by analysts) reinforces Fed member positions that inflation is likely transient and not structural. Specifically, the analysis looked at the 5-year break-even inflation rate (now at 2.45%) and the 10-year break-even rate (now 2.33%). (The break-even rate is the difference between the treasury yields and inflation-indexed bonds for a given period.) This tells us bond traders now anticipate inflation to be falling in a longer timeframe, despite it rising in the short term. Clearly, this is not gospel, but maybe an indication that stocks will continue to be attractive as longer-term safety trades can’t compete on return.

Home prices surged in April according to the Case-Shiller Price Index. The gained was 13.3% month-on-month and 14.6% year-on-year. This was the biggest gain in home prices in 30 years. While this does represent an increase in the value of the major asset of many American families, as with any average the gains were uneven. High-end homes saw the biggest gains while lower-end home prices saw single-digit gains. Charlotte NC, Cleveland OH, Dallas TX, Denver CO, and Seattle WA all saw their largest ever annual gains. However, data out this morning shows that mortgage demand fell 7% this week (and 17% from one year ago) as 30-year interest rates rise.

After the close Tuesday, RCL announced that any passengers sailing from US ports without being fully-vaccinated, will be required to have travel insurance. FL passed a law that exempts itself from this as of January 1, 2022, leaving the insurance burden on cruise operators for ships leaving their ports.

Overnight, Asian markets were mixed, but leaned to the green side. Shenzhen (+1.08%) and Singapore (+1.33%) led to the upside. Meanwhile, Malaysia (-1.01%) and Hong Kong (-0.57%) paced the losses. However, in Europe markets are decidedly in the red as of early afternoon. The FTSE (-0.59%), DAX (-0.93%), and CAC (-0.75%) are good indicators of the rest of the continent. As of 7:30 am, US Futures are pointing to a dead flat open. The DIA is implying a -0.02% open, the SPY implying a -0.01% open, and the QQQ implying a +0.01% open. In addition, 10-year bond rates are moving significantly lower, now at 1.454%.

Major economic news scheduled for Wednesday includes ADP Nonfarm Employment (8:15 am), Chicago PMI (9:45 am), May Pending Home Sales (10 am), Crude Oil Inventories (10:30 am), and a Fed Speaker (Bostic at 8 am). Major earnings reports scheduled for the day include BBBY, STZ, GIS, and SCHN before the open. Then after the close, MU and YUMC report.

Interest rates came down overnight, but Oil and Nat Gas prices surged, even as the dollar is a bit stronger. However, yesterday’s gains were not widespread as only two of the 10 major sectors were in the green (technology, of course, and Consumer Cyclical). So, markets are showing signs of being wary at these levels. Be careful, but it’s hard to fight a bullish trend until it breaks.

Keep taking your profits, moving your stops, and maintaining your discipline. Follow those trading rules, don’t chase, and stick to the trade plan. The odds favor following the trend and, as always, respect both support and resistance levels. However, all trends reverse at some point and every S/R level is breached eventually. So, don’t just assume trend, support, or resistance will always hold. Remember that consistency is the key to long-term trading success. So, book those singles and doubles. Base hits win championships, not the occasional home run. So, don’t try to stretch things and get burnt in the process.

Ed

Swing Trade Ideas for your consideration and watchlist: PLUG, UCO, NOK, KOPN, DPZ, XBI, RKT, UBER, SQ, INO, AI, APPS, QS, RIDE, BABA. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service