Uncertainty has begun to raise its ugly head with a stark imbalance between the 7 to 9 tech giants doing all the heavy lifting with just 47% of stocks trading above their 200-day averages. So with an ECB decision pending and Jobless Claims before the bell, will the bulls find the inspiration to defend, or will the bears find an opening to attack? Your guess is as good as mine, but the surge that occurred yesterday into real estate, utilities, and consumer staples looking for some safety is noteworthy.

Overnight Asian markets traded mostly lower, with Hong Kong plunging 2.30% on the Chinese gaming crackdown worries. This morning, European markets see only red as they await the ECB decision, with inflation hitting a 10-year high. U.S. futures also hint at a lower open with eyes on the ECB and Jobless Claims that have become troublesome of late. So buckle up; it could be a volatile open.

Economic Calendar

Earnings Calendar

We have our busiest day of the week on the Thursday earnings calendar, with 31 companies listed, several unconfirmed. Notable reports include AFRM, PLAY, HOFT, JILL, LAKE, LOVE, RLGT, COOK, VRNT, ZS, & ZUMZ.

News & Technicals’

Chinese regulators summon Tencent, NetEase, and other game companies for interviews, reminding them about the restrictions on game time for children. As a result, Hong Kong plunged 2.30% as Tencent shares fell 8.48% and NetEase dropped 11%. According to the South China Morning Post, Beijing has temporarily frozen game approvals. Treasury Secretary Janet Yellen warned House Speaker Nancy Pelosi that the mere specter of a U. S. default could have drastic consequences. Yellen said lawmakers have until some point in October before the department runs out of funds in its extended efforts. Today, we will hear about the ECB’s plan to taper and battle inflation, which is now at a 10-year high. U.S. Treasury yields dip as we wait, with the 10-year trading down to 1.321% and the 30-year falling to 1.941%.

I don’t believe I’ve ever witnessed the stark imbalance between the haves and the have not’s in the market. Only 47% of U.S. stocks are above their 200-day moving averages as 7 to 9 tech giant companies continue to do all the heavy lifting. That said, the QQQ and SPY have maintained their bullish trends as long as those tech giants don’t stumble. The DIA, on the other hand, is beginning to show some technical damage falling below the uptrend and putting in a lower high. So the question to be answered today is will the bulls defend the DIA 50-day average as support? With Jobless Claims and an ECB decision just around the corner, your guess is as good as mine. There is no reason to be running for the doors just yet, but caution flags are flying as market internals continue to raise uncertainty.

Markets opened just on the red side of flat Wednesday and after a shaky first 5 minutes, the bulls rallied to test the small gap. However, that rally failed by 10:30 taking us to the lows by 11 am. The rest of the day was a whipsaw of small waves that closed up off the lows. This left us with indecisive Doji candles in the DIA and SPY and a long-wick Hammer (or Hanging Man) in the QQQ. This was also the third straight lower close in the large-cap indices and the first in the QQQ. On the day, SPY lost 0.13%, DIA lost 0.21%, and QQQ lost 0.35%. The VXX was flat at 25.51 and T2122 fell again to 33.33. 10-year bond yields fell significantly again to 1.338% and Oil (WTI) was up 1.5% to $69.36/barrel.

During the day Wednesday, the Fed JOLTS report showed that that were 10.9 million job openings in July. This was much higher than the 9.9 million estimated and was more than 2 million more openings than there were unemployed. Interestingly, the percentage of openings that saw hires fell from 4.7% to 4.5% while the percentage of workers who quit remained stable at 2.7% and the rate of new layoffs grew by 1%. Analysts say this indicates workers were confident and that wages for job openings were not high enough to overcome prospect expectations and inflation perceptions.

Overnight, Chinese regulators called the executives of Tencent, NetEase, and other game companies in to remind them of the new restrictions on game time for children. Those restrictions limit Chinese under age 18 to a maximum of 3 hours per week of online gameplay. China also announced a temporary halt to new game approvals. Finally, Chinese education authorities banned tutors and education companies from delivering lessons online or in any unregistered venue. These moves caused investors to run for the door on Chinese tech stocks and may well bleed over into China-related stocks listed in the US.

Treasury Sec. Yellen warned House Speaker Pelosi that the Treasury Department will have exhausted its “extraordinary measures” at some point in October. She called on Congress to raise the national debt ceiling before this happens, otherwise the country will default on debts. This comes as the Democratic party is infighting over more progressive or more centrist versions of the national budget and as Republicans are saying “no” to both groups of proposals as all sides seek to appeal to their political bases (or principles if you prefer). While this is on the fiscal side, it comes as the monetary taper debate intensifies and markets are grasping for direction.

Overnight, Asian markets were mixed but leaned to the downside. Hong Kong (-2.30%) was hit hardest due to being the main exchange for Chinese tech stocks. However, Australia (-1.90%) and South Korea (-1.53%) were also at the top of the list of exchanges in the red. Shanghai (+0.49%) was one of the few green exchanges in the region. In Europe, markets are red across the board so far today as the region prepares for the European Central Bank meeting later today. The FTSE (-1.15%) is an outlier with the DAX (-0.22%) and CAC (-0.20%) being more typical of the region at mid-day. As of 7:30 am, US Futures are pointing to a modestly down open. The DIA is implying a -0.23% open, the SPY implying a -0.24% open, and the QQQ implying a -0.20% open at this hour. The Dollar and 10-year bond yields are down slightly while Oil (WTI) is up two-thirds of a percent in early trading.

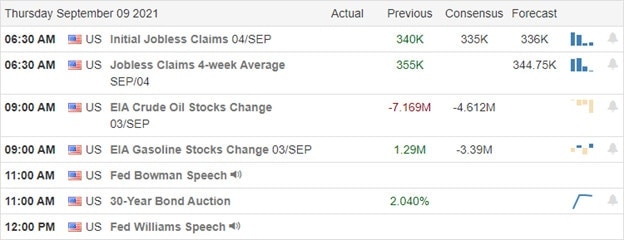

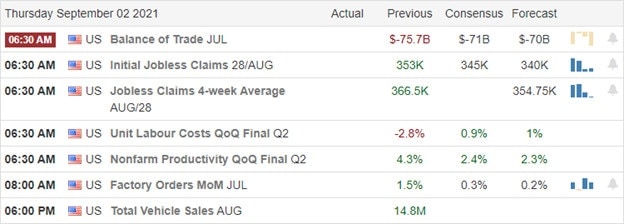

The major economic news scheduled for release on Thursday is limited to Weekly Jobless Claims (8:30 am), Crude Oil Inventories (11 am), and 3 Fed speakers (Daly at 11:05 am, Bowman at 1 pm, and Williams at 2 pm). The major earnings reports scheduled for the day include ASO and HOV before the open. Then after the close, AMRK reports.

US Markets will likely take its early cue from Weekly Jobless Claims. However, the ECB will begin debating their taper later and Fed speakers will add to that storyline. So, expect some volatility, but Mr. MArket coming to a conclusion is still not likely today. The trend remains bullish, and the chart looks like a normal pause/pullback in all but the Dow. However, the signs of bearishness are clear in the DIA, where even the 50sma has been breached.

Remember you don’t have to trade every day. So, consider whether this market suits your trading style or not before blindly trading. As always, manage your existing trades before you chase any new ones. Focus on the process and on managing the things you can control. Don’t worry too much about the things outside of your control. Good trading rules and discipline is what separates long-term success from failure in trading. However, above all, consistently take profits when you have them. A good trader just won’t let greed turn their winners into losers.

Ed

Swing Trade Ideas for your consideration and watchlist: SPRT, CLOV, T, AAPL, NVAX, BTCM, FUTU, SKLZ. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Markets opened flat on Tuesday and proceeded to sell off the first hour of the day. From that point, the large-cap indices ground sideways, and the QQQQ rallied before grinding sideways. Another selloff the last half-hour took us out down off the highs. As a result, the QQQ printed a Doji (at an all-time high close) while the SPY printed a black candle that stayed above the 8ema (and lows of the consolidation range of the last week) and the DIA was the weakest of the group printing an ugly black candle that closed not far up off the lows. On the day, SPY lost 0.34%, DIA lost 0.76%, and QQQ gained 0.14%. The VXX rose about 2.4% to 25.53 and T2122 dropped but remains in the mid-range at 41.48. 10-year bond yields were up sharply to 1.371% and Oil (WTI) fell 1.3% to $68.38/barrel. Perhaps this reflected the Saudi oil price cut from Sunday.

After having reached almost $53,000 on Monday night, Bitcoin fell hard Tuesday. The largest cryptocurrency closed down over 11% to $46,354. This came as El Salvador became the first to begin using Bitcoin as legal tender in the country. Oddly, that country bought only about $20 million worth of Bitcoin, even though it has a GDP of over $27 billion. Bitcoin-related stocks such as MSTR and COIN also took heavy hits on the day. COIN also announced this morning that the SEC has notified it that the regulator intends to sue the company over an interest-earning product the company has planned to launch as soon as next week.

Late in the afternoon Tuesday, F announced it had hired the AAPL executive that has been leading the “Apple Car” project. Doug Field was also a former TSLA executive (led the development of the TSLA Model 3) and is slated to become the “Chief Advanced Technology and Embedded Systems Officer” at F as part of the company’s turnaround effort. While AAPL confirmed Doug Field’s exit, they still refuse to confirm the existence of the project and analysts say this would be a blow to the AAPL project that is supposedly now focused on software to support autonomous driving, having abandoned the idea of becoming an auto-maker itself.

Mortgage rates remained unchanged this week (3.03% for a 30-year fixed, conforming loan). This saw loan demand fall as home refinance applications were down 3% for the week (4% lower than a year ago). New home purchase applications were flat last week, but down a full 18% from a year ago.

Overnight, Asian markets were mostly red in Asia. Indonesia (-1.41%), Singapore (-1.27%), and Taiwan (-0.91%) saw the largest losses. Meanwhile, Japan (+0.89%) and Malaysia (+0.89%) were the only real gainers on the day as China remained flat. In Europe, with Russia the only outlier, the rest of the continent is in the red at mid-day. The FTSE (-0.45%), DAX (-0.62%), and CAC (-0.32%) are typical of the continent, but a couple of the small exchanges are down a full percent in early afternoon trading. As of 7:30 am, US Futures are pointing toward another flat open. The DIA is implying a -0.02% open, the SPY implying a -0.01% open, and the QQQ implying a -0.05% open at this hour. 10-year Bond yields are also just on the red side of flat, but Oil (WTI) is up 1.3% in early trading.

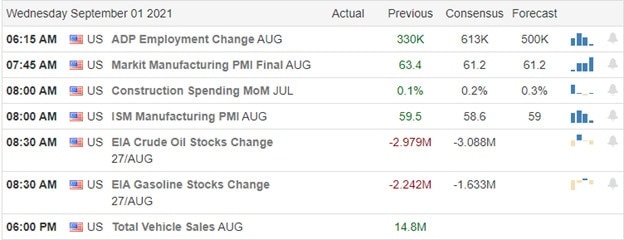

The major economic news scheduled for release on Wednesday is limited to July JOLTs (10 am), 10-year Bond Auction (1 pm), Fed Beige Book (2 pm), and a Fed Speaker (Williams at 1:10 pm). The major earnings reports scheduled for the day include KFY and REVG before the open. Then after the close, ABM, CPRT, GME, LULU, and RH report.

Markets seem to be uncertain at the moment. With inflation fears, a diminishing economic growth rate, and a lack of clarity around both the taper timeline and the fiscal spending/taxation plans, traders appear to be waiting on more direction. Hopefully, some of that will become more clear the next few days with several Fed speakers on tap. In the meantime, beware of volatility and a waffling market. The mid-term trend remains bullish, but we are in a clear consolidation in the SPY and QQQ, while the DIA is pulling back and testing its 50sma in premarket trading.

Remember that the trend is your friend until it ends. So, don’t try to predict market direction changes. However, you should also consider whether market conditions are right for your trading. They say a rising tide lifts all ships, but it’s not a great idea to be out there rowing against the tide when you have a choice. You don’t have to trade every day.

As always, manage your existing trades before you go chasing any new ones. Concentrate on the process and on managing those things that you can control, while not worrying too much about the things you can’t control. Good trading rules and discipline is what separates long-term success from failure in trading. However, above all, consistently take profits when you have them. A good trader just won’t let greed turn their winners into losers.

Ed

Swing Trade Ideas for your consideration and watchlist: CPB, XSPA, PENN, AMC, RIG, EDU, PDD, CLOV, VIPS, NKLA, TELL, HSIC, GOGL. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

The market chose to ignore the disappointing jobs numbers and the unemployment benefits cliff as we slid into the holiday weekend with the assumption this will allow the Fed to continue printing. As a result, the index trends remain very bullish, with the DIA, SPY, and QQQ consolidating within striking distance of new record highs. With a light week of economic and earnings data, the market may become more sensitive to geopolitical news, or we may see a light and choppy week of price action.

Overnight Asian markets mostly rallied as Chain’s exports topped expectations. However, European markets trade modestly bearish this morning, concerned about the declining jobs and consumer activity. Here in the U.S., futures point to a flat mixed open that could prove to be a light volume day as traders extend their holiday with a bit of vacation time.

Economic Calendar

Earnings Calendar

We have a light day on the Tuesday earnings calendar with 18 companies listed and several unconfirmed reports. Notable reports include AMBA, AMWD, CHS, CRWD, DBI, NTES, & PVA.

News & Technicals’

Though a little surprising, the market chose to ignore the massive miss of the employment situation, likely due to the hope that the Fed will keep printing 120 billion a month rather than tapering. As a result, Goldman has cut its GDP forecast for the second time in the last 30 days, citing pandemic impacts and the fading of fiscal stimulus. Moreover, yesterday was the end of the unemployment bonuses, and apparently, millions have exhausted their unemployment benefits in total, raising concerns with the declining consumer sentiment and confidence. However, the U.S. Treasury yields seem to have shrugged off the disappointing jobs data, with the 10-year rising to 1.353% and the 30-year trading up to 1.97%.

Technically speaking, the price action of the index charts appears to have no concern at all about the unemployment benefits cliff or the lackluster jobs numbers. On the contrary, the DIA, SPY, and QQQ remain bullish, all within striking distance of new record highs. Over the last two weeks, the IWM has improved dramatically yet still has significant overhead resistance to overcome. With a holiday-shortened trading week, light earnings calendar, and an economic calendar with no significant market-moving reports, it may be difficult for the bulls and bears to find inspiration. In addition, please keep in mind volume could be noticeably light today as many traders may have extended their long weekend with additional vacation time. As I keep repeating, stay with the trend but guard against complacency if the market suddenly decides to care about the weakening economic data.

August Nonfarm Payrolls increased far less than (one-third of) expected, but the July increase was also revised up significantly. This happened while the participation rate increased (indicating more job seekers) and August wages grew twice as much as expected. Analysts said this all indicates the impacts of Delta on hiring in the much more numerous lower-wage jobs (like travel/hospitality and restaurant/retail) and a commensurate percentage shift toward more jobs being filled in the higher-paying services and consulting sectors.

Regardless, of the reasoning, this caused a quarter percent gap down at the open on Friday. However, the bulls were not giving in so easily, and led by the Tech sector the major indices saw a slow rally that lasted all day long. Only the DIA faded at day end. This left us with a Spinning Top candle in the DIA, and strong white candles in the SPY and especially QQQ. On the day, QQQ gained 0.31% (to another new all-time high close), SPY lost 0.02%, and DIA lost 0.21%. The VXX rose slightly to 24.94 and T2122 dropped just outside of the overbought territory to 78.60. 10-year bond yields rose t o1.326% and Oil (WTI) fell 1.27% to $69.10/barrel.

In miscellaneous news, MTCH soared after the close Friday when it was announced that ticker will be added to the S&P500 as of September 20. MTCH will replace PRGO, which will be moved down the S&P MidCap 400 on that date. On Sunday, Saudi Arabia cut oil prices for sale to Asia by between $1.30/barrel and $1.70/barrel. The Saudi state oil company price reduction (on all grades of crude) comes after 3 straight months of increases. This happens as OPEC+ is increasing production limits and the country is looking to capture market share. This morning, GS lowered its Q4 GDP estimates by a full percent (6.5% to 5.5%) and now expects 5.7% growth for the year. GS cited fading fiscal stimulus, a slowing service sector, and inflation worries as impediments to consumer spending.

On Friday, Senate Finance Committee Democrats prepared a number of new tax proposals. One of these could impact the market by potentially reducing share buybacks. The proposal was to add an excise tax on all share buyback programs. These programs have been widely seen as a buoy to the market, putting large buyers under price and preventing major pullbacks. However, Wall Street shrugged off the news Friday. likely because it was only proposed, by only one party, a year before mid-term elections, and that means the proposal is a very long way from being made into law.

Overnight, Asian markets were mixed again on data that Chinese exports in August beat expectations. (The average estimate called for a 17.1% year-on-year increase, while they reported a 25.6% year-on-year increase.) Shanghai (+1.51%), Shenzhen (+1.07%), and Japan (+0.86%) led the gainers. Meanwhile, Thailand (-0.72%) stood out among the losses. In Europe, markets are red across the board in morning trading. The FTSE (-0.31%), DAX (-0.28%), and CAC (-0.08%) a decent gauge to the region, but most of the smaller exchanges are further in the red, perhaps waiting on more direction from the ECB meeting on Thursday. As of 7:30 am, US Futures are pointing toward a flat open. The DIA is implying a +0.10% open, the SPY implying a +0.03% open, and the QQQ implying a -0.07% open at this hour. However, 10-year bond yields are up sharply to 1.368% and Oil (WTI) down over 1% in early trading.

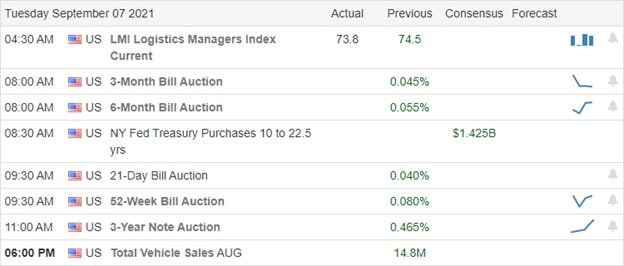

There is no major economic news scheduled for release on Tuesday as we ease back in after the long weekend. There are also no earnings reports scheduled for the day.

After the holiday weekend, traders return with continued concerns about the impacts of the Delta variant and inflation. Sitting at the all-time highs and with no planned news drivers (none today and few the rest of the week except many Fed speakers), it’s quite possible that we see consolidation continue today. The trend remains bullish, but we’ve seen indecision among the large-caps for at least a week as high tech has been leading the rally for some time.

Good trading rules and discipline is what separates long-term success from failure in trading. Concentrate on the process and on managing those things that you can control, while not worrying too much about the things you can’t control. As always, manage your existing trades before you go chasing any new ones. However, above all, consistently take profits when you have them. Simply don’t let greed turn your winners into losers.

Ed

Swing Trade Ideas for your consideration and watchlist: PDD, EDU, CAN, EBAY, XHB, KR, HPQ, VIAV, AMC, VIPS. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Economists expect a solid Employment Situation number; however, some worry the pandemic impacts could diminish its shine. The premarket pump would like us to believe all is well but should the bears find a reason to attack; the open could change dramatically. Index trends are bullish, but with the recent extension in prices, a stumble could be painful. So stay focused and flexible. After the morning reaction, look for the volume to decline and choppy price action to ensure as traders escape early to begin their 3-day weekend.

Asian market closed Friday trading mixed with the Nikkei surging on news the Prime Minister Suga is leaving office. However, European markets are taking a wait-and-see approach as they wait on the U.S. jobs data. U.S. futures are waiting for nothing, putting on a brave face ahead of the critical jobs data implying new record highs. That said, anything is possible, so buckle up the reaction is just around the corner.

Economic Calendar

Earnings Calendar

There may be no earnings reports this Friday. Though we have 13 companies listed on the calendar, all of them are unconfirmed. So we have no notable reports.

News & Technicals’

Though the Fed maintains that the recent spike in inflation will be transitory, Niall Ferguson, the top economic historian, has called that thesis into question. He went on to say we could see a repeat of the 1960’s when the Fed lost control. In addition, the former IMF chief suggested that the perfect storm of factors could lead to 70’s style high inflation. This morning Treasury yields rose slightly, with the 10-year tradings at 1.295% and the 30-year rising to 1.91%.

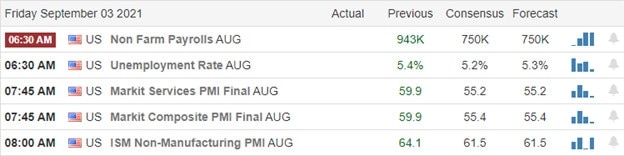

With a 3-day weekend pending, all eyes will be on the Employment Situation report coming out an hour before the bell. The consensus is looking for 740,000 Nonfarm payrolls and 693,000 Private Payrolls, down from 943,000 and 703,000, respectively. They are also looking for the unemployment rate to decline from 5.4% to 5.2%. Although fingers are cross for a firm number, some are worried the rising pandemic numbers could mute the outcome. Undeterred, the premarket pump is underway, trying to project to more record highs at the open. Index charts remain very bullish, but anything is possible by today’s open so stay focused and flexible. After the morning volatility, there is a high probability that traders will shut down early to begin their 3-day weekend early with light and choppy price action as the remainder of the day. Have a wonderfull weekend, everyone.

Economic data was mixed in the premarket Thursday. Jobless Claims came in very slightly below expected and the July Trade Balance improved a bit. However, nonfarm productivity for Q2 came in three-tenths of a percent lower than expected. Markets seemed to like the news as stocks opened a third of a percent higher. At that point, the large-cap indices ground sideways in a tight range until 1 pm, while the QQQ sold off steadily until 2 pm. There was market-wide selling from 1-2 pm and then a very late rally into the close. This left the SPY and DIA as indecisive Doji and the QQQ as a gap-up black candle with a significant lower wick (also indecisive). On the day, SPY gained 0.32% (to a new all-time high close), DIA gained o.38%, and QQQ lost 0.05%. The VXX fell to 24.77 and T2122 rose slightly, further into the overbought territory at 89.38. 10-year bond yields fell to 1.287% and Oil (WTI) was up 1.6% to $69.72/barrel.

During the afternoon, F announced that its August sales had declined by over 33% due to the global chip shortage. This was its worst month since June 2020 at the height of the pandemic shutdown. Worst of all, August is historically one of the strongest car sales months. For reference, US car dealers have 942k cars in inventory now compared to an average inventory of 3 million cars before the pandemic. This chip shortage is quite obviously a problem across the auto (and other) industry, not just for F.

A new study reported by Bloomberg says that more than 1 billion Asians will join the middle class by 2030. This includes 76 million in Indonesia and even 24 million of that billion being in the US. However, 75% of the number will be located in China and India. The same study said that the changing demographics will lead to middle class shrinking in countries like Japan, Western Europe, and the US. Obviously, this shift will impact corporations across the globe. In possibly related news CNBC reports that Chinese stock investing volumes continue to surge, despite recent government crackdowns on the Chinese Tech Giants. CNBC says that the average daily volume has held steady above $154 billion per day.

After the close, news came that the Democratic $3.5 billion budget bill is running into infighting problems. Essentially Democratic Senator Manchin asked his party to “pause” the budget while both he and another Democratic Senator also said they will not support a budget anywhere near that size. On the other side of the same party, progressives will not support a budget much smaller. This puts the President’s domestic agenda at risk and may also imperil the $1 Trillion Infrastructure Bill that Democrats have been trying to bundle as a pair with the Budget Bill.

Overnight, Asian markets were mixed, with a widespread on the bullish side. Japan (+2.05%) surged as current PM Suga dropped out of his governing party’s leadership race. Taiwan (+1.14%), Indonesia (+0.80%), and South Korea (+0.79%) were the real leaders to the upside. Meanwhile, Hong Kong (-0.72%) and Shenzhen (-0.68%) paced to the downside. In Europe, markets are also mixed but lean heavily toward the red as they wait on US data as a guide. The FTSE (+0.23%) and DAX (+0.14%) are outliers, but the CAC (-0.42%) is typical of the broader continent. As of 7:30 am, US Futures are pointing toward an open just on the green side of flat an hour ahead of the August Payroll Data. The DIA is implying a +0.16% open, the SPY implying a +0.18% open, and the QQQ implying a +0.12% open at the moment. 10-year bond yields and Oil (WTI) are also up slightly in early trading.

The major economic news scheduled for release on Friday includes Aug. Nonfarm Payrolls, Aug. Avg. Hourly Earnings, Aug. Participation Rate, and Aug. Unemployment Rate (all at 8:30 am), Aug. Service PMI (9:45 am), and ISM Non-Mfg. PMI (10 am). MAKE NOTE: we have a 3-day weekend ahead for US and Canadian markets. There are also no earnings reports scheduled for Friday or Monday.

August Payrolls data are very likely to call the tune today. However the Payroll data is interpreted by the traders, this is likely to be reinforced by mid-morning PMI data as Mr. Market begins to look ahead a couple of weeks to the Fed meeting. With that said, we do have an upcoming 3-day weekend, which many traders may try to stretch. So, be ready for early volatility with the potential for volume to begin drying up at some point mid-day.

Concentrate on the process and on managing those things that you can control, while not worrying too much about the things you can’t control. Good trading rules and discipline is what separates long-term success from failure in trading. As always, manage your existing trades before you go chasing any new ones. However, above all, consistently take profits when you have them. Simply don’t let greed turn your winners into losers.

Ed

Swing Trade Ideas for your consideration and watchlist: FGEN, SKLZ, PDD, MMAT, BIDU, IQ, STEM, BILL, JMIA, LOW, AG, MGM, WYNN, RIG, CLOV, KR, SPT. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

With another morning chalked full of data, we have the typical premarket pump up, but anything is possible at the open as the market reacts to the data. However, with the pending Employment Situation number Friday morning, it would not be unusual to slide into choppy price action after the morning gyrations as we wait. Nevertheless, the index trends remain bullish, although the extension in the SPY and QQQ by the surge of buying in big tech is a bit worrisome that a profit-taking wave could begin anytime. That said, stay with the trend but avoid complacency should the data shift current sentiment.

Overnight Asian markets traded mixed with Australia, recording a higher than expected trade surplus in July. European indexes trade flat this morning as they wait on the pending jobs data here in the U.S. However, that is not the case in the U.S. future as the push for a bullish open ahead of trade and jobless claims numbers. So expect some morning price volatility as the market reacts.

Economic Calendar

Earnings Calendar

We have our busiest day on the earnings calendar this week, with 35 companies listed this Thursday. Notable reports include SIG, AEO, AVGO, CIEN, CCEP, DLTH, GIII, GCO, HPE, HRL, JOAN, KIRK, LE, & TLYS.

News & Technicals’

The ECB will meet on Sept. 9th, but analysts think the central bank will wait until maybe December to announce a taper. One possible reason for the wait is to see what happens with the pandemic in the coming months. According to the WHO, a new variant called “mu” has mutations that can evade a previous infection or vaccination immunity. MU was first spotted in Colombia but is now being tracked in at least 39 countries. New York and New Jersey have issued emergencies after the remnants of Hurricane Ida dropped record rainfall between 6 to 10 inches bringing transit to a near standstill and shutting down parts of the subway system. This morning Treasury yields are moving lower, with the 10-year slipping to 1.2970% and the 30-year dipping to 1.9174%.

After the typical premarket pump up, the indexes spent most of the day chopping, although the QQQ did squeak out a new record high by the close. However, the technicals of the index charts remain very bullish albeit somewhat extended in the SPY and QQQ. The substantial decrease in oil reserves also helped to support the price action in IWM, which turned in the most robust performance of the day. With a busy morning of economic data that includes Jobless Claims, international trade, productivity, and factory orders, we should expect price volatility at the open. That said, don’t be too surprised after the early morning reaction if the price action returns to choppiness as we wait for the Employment Situation Friday morning. Though we see the typical premarket pump up, the open makes anything possible as the market reacts to the data.

The ADP private payrolls report came in very soft (374k vs 600k est.) before the Open Wednesday, but bulls didn’t seem to care with a slight gap up to start the day. At that point, QQQ rallied hard for 30 minutes, DIA sold off for an hour, and SPY ground sideways in a very tight range. All 3 major averages then moved sideways until a long selloff started at 2 pm and ran right into the close. This left us with a Shooting Star-type candle in the QQQ, a Bearish Engulfing of a Doji in the DIA, and just a black candle in the SPY. On the day, SPY gained 0.07%, QQQ gained 0.17%, and DIA lost 0.10% as its consolidation continued. The VXX fell to 24.81 and T2122 rose back into the overbought territory at 88.43. 10-year bond yields started the month unchanged at 1.302% and Oil (WTI) fell slightly to $68.28/barrel.

At the Close Wednesday, F announced it will once again be cutting F-150 pickup production (as well as other highly profitable vehicles) due to the global chip shortage. The company will leave the currently closed Kansas City plant closed at least another week. It will also cut shifts at the Kentucky truck plant and run only one of three shifts at the Michigan truck plant. In a related story, Bloomberg reports this morning that TSLA’s Chinese plants were “closed for days” last month due to the same cause, the chip shortage.

AAPL announced yesterday that 8 states will now allow their citizens to use electronic IDs such as their iPhone or Apple Watch as valid for security checks, including airports. The states include AZ, CT, GA, IA, KY, MD, OK, and UT. This comes after AAPL announced last month that it was working with the TSA to gain approval of ID by electronic device approval. AAPL also announced plans to make slight tweaks to App payment policy. This is an attempt to avoid or mitigate moves to force massive changes to the App Store policies and revenue.

So far this morning, CCEP and PDCO reported a beats on both lines while HRL beat on revenue and came in fractions of a cent below estimates on earnings. In other business news, QSR (Burger King) announced a customer loyalty program, matching recent moves by MCD, WEN, and longer-standing programs from SBUX and CMG.

Overnight, Asian markets were mixed again, this time on modest moves as Australia reported a larger-then-expected (20% higher) trade surplus in July on commodity price strengths. On the red side, South Korea (-0.97%) and Taiwan (-0.88%) were by far the leaders. Meanwhile, on the upside, India (+0.92%), Shanghai (+0.84%), and Thailand (+0.81%) led the charge. In Europe, markets are mostly green at mid-day. The FTSE (-0.06%), DAX (+0.03%), and CAC (+0.09%) are flat, but most of the continent is a little more to the upside at noon in London. As of 7:30 am, US Futures are pointing to a modest green open. However, this is also an hour before a considerable economic data dump. The DIA is implying a 0+0.15% open, the SPY implying a +0.17% open, and the QQQ implying a +0.22% open at the moment. 10-year bond yields are down to 1.287% and Oil (WTI) is up two-thirds of a percent in early morning trading.

The major economic news scheduled for release on Thursday includes Imports/Exports, Weekly Initial Jobless Claims, Q2 Nonfarm Productivity, and Q2 Unit Labor Costs (all at 8:30 am), July Factory Orders (10 am), and 2 Fed speakers (Bostic at 1 pm and Daly at 3 pm). The major earnings reports scheduled for the day are limited to AEO, DOOO, CIEN, DCI, GCO, GMS, HRL, PDCO, SIG, and TTC before the open. Then after the close, AVGO, DOCU, HPE, JOAN, and SAIC report.

With a lot of data coming out this morning and the August Payrolls number due tomorrow, it is worth reminding ourselves that it’s not the data that matters. What matters is the way the market reacts to the news. For example, bad economic data could be interpreted as very bad for future earnings reports. However, it could also be interpreted as giving cover to the Fed to push the taper further out. The point is, don’t think you can forecast the data, let alone how the market will react. Just stick with the current trend until the trend breaks (ends).

As always, manage your existing trades before you go chasing any new ones. Concentrate on the process and on managing those things you can control, while not worrying too much about the things you can’t control. Good trading rules and discipline is what separates long-term success from failure in trading. Above all, consistently take profits when you have them. Don’t let greed turn your winners into losers.

Ed

Swing Trade Ideas for your consideration and watchlist: FNKO, CAN, MMAT, STEM, PLAY, USO, GEVO, NLOK, CDEV, CRSR, PWR, AMD. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

The bulls look ready to begin September by setting new records at the open to follow seven straight months of gains. With bonds rising this morning, we turn our attention to private payroll and manufacturing numbers for inspiration. However, the supreme court overturning the eviction moratorium and the end of unemployment bonuses on Sept. 6th could create some uncertainty and volatile price action as we progress through the month. Until then, stay with the trend but guard against complacency.

During the night, Asian markets rallied despite the Chinese factory activity shrank in August. Likewise, European markets trade green across the board this morning unconcerned about inflation data that showed consumer prices increased by 3%. Ahead of jobs and MFG. Data U.S. futures continue to march higher, suggesting new records are possible in the SPY and QQQ to kick off September trading.

Economic Calendar

Earnings Calendar

We have 21 companies listed on the Wednesday earnings calendar with several unconfirmed reports. Notable reports include ASAN, CHPT, CHWY, CPB, CONN, FIVE, NTNX, RYAN, SMTC, SWBI, VEEV, & VRA.

News and Technicals’

After seven straight months of gains, the bulls appear willing to push for more records as big tech continues to dominate. Historically September is a challenging month for the market, but that has not been true for three of the last five years. With growing evidence that the economy is slowing, the supreme overturning of the eviction moratorium, and the end of unemployment bonuses on Sept. 6th, there is undoubtedly a reason for uncertainty. Then on Sept. 22nd, the FOMC will show its hand for the taper of the easy money policies. Treasury Yields traded higher this morning, with the 10-year climbing to 1.327% and the 30-year rising to 1.945% as we slide into the last month of 3rd quarter trading.

The bulls run will now turn its attention to Private payroll and manufacturing numbers, with the Employment Situation report looming Friday morning. Though internals hint of an economic slowdown, the index chart technicals show no evidence of concern as the bulls power forward, suggesting tech could set more records at the open today. The VIX hinted at a bit of uncertainty rising slightly yesterday, but the slow, choppy price action showed no sign of panic yesterday. The only concern is that the SPY and QQQ are very stretched in the short term, but with the market seeming unconcerned about the extreme valuations, I’m not sure that currently matters. However, complacency is becoming a concern, so guard against overtrading and have a plan to protect yourself should the tide finally decide to go out.