Another big day of buying the relief rally set new record highs in the SPY and QQQ on Monday. In just 3-trading days, the SP-500 rallied 110 points, and the Nasdaq surged 519 points, a massive of 3.60%. With the U.S. House poised to deliver two more massive deficit spending bills with reclaimed bullish trends, it seems the sky is the limit for how high the indexes can go. Debit, consumer sentiment, inflation, and rising pandemic impacts seem to have no impact on the willingness to push prices higher. So stay with the trend, and let’s continue to party as long as it lasts.

Overnight Asian markets continued to recover, with the Hong Kong leaping a whopping 2.46%, spurred on by the Pfizer vaccine approval. However, European markets are not so rambunctious this morning, mainly trading lower but with modest losses. That said, U.S. futures indicate a higher open and more new records as tech continues to reach for the stars. Don’t rule out the possibility of profit-taking, and be careful not to chase already extended stocks.

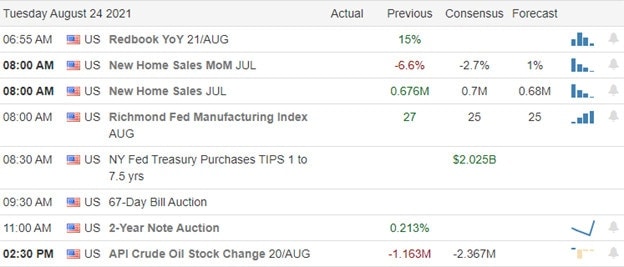

Economic Calendar

Earnings Calendar

This Tuesday, we have 33 companies listed on the earnings calendar, with several unconfirmed reports. Notable reports include BBY, AAP, INTU, MDT, JWN, PDD, TOL, & URBN.

News & Technicals’

The U.S. House has delayed voting to advance the massive spending plans as centrists pushed Speaker Nancy Pelosi to vote on the Senate-passed infrastructure bill before moving on the 3.5 trillion packages. The natural gas pipeline between Europe and Russia has recently slowed the delivery, raising questions about the potential cause and implications for global gas markets. Angela Merkel says further sanctions may be imposed if Moscow is using the gas supply as a weapon. Leaders will meet virtually for an emergency G7 meeting with countries pushing President Biden to extend the Aug. 31st deadline. However, Afghanistan delivered a redline to the U.S., saying it will not accept and extension raising tensions as efforts to get Americans and those who supported our efforts out of the country. Treasury yields rose slightly this morning, with the 10-year increase to 1.268% and the 30-year trading up to 1.888%.

The strong bounce that began on Friday surged to new record highs in the SPY and QQQ led by big tech giants. Microsoft, Google, and NVDA printed new record prices joined by others that rallied strongly yesterday. CNBC said the FDA’s full approval of the PFE vaccine was the impetus for the bullish surge, but most of the enthusiasm was tech-based. That said, there are still a significant number of stocks below their 200-day moving averages, creating a wide divide between the have’s and have not’s. The overall SP-500 P/E ratio is more than 94% above its 10-year historical average, and one has to wonder how much higher it could go. Of course, the U.S. House is moving forward with two huge spending bills, and we all know how much the market seems to love deficit spending. So stay with the trend but stay on guard should the bears find another reason to attack.

Markets gapped higher Monday and then kept rallying until about 1 pm. However, the rest of the day saw some persistent profit-taking that lasted into the close. This left us with strong white candles with upper wicks in all 3 major indices. On the say, SPY gained 0.87% (to a new all-time high close), DIA gained 0.64%, and QQQ gained 1.50% (to a new all-time high close). The VXX fell 3.4% to 26.81 and T2122 remained in the mid-range at 55.65. 10-year bond yields were flat at 1.257% and Oil (WTI) spiked higher 5.3% to $65.44/barrel as commodities across the board showed very strong gains on a very weak dollar.

The FDA gave “Full Approval” (as opposed to “Emergency Use Approval”) to the PFE Covid vaccine on Monday. President Biden then made a plea to those unvaccinated Americans, saying “Please get vaccinated now.” He went on to stress that the vaccine has now proven to be 91% effective at preventing infection and once vaccinated, there is a very low statistical probability of having a severe infection. As of Sunday, only 51% of American adults were fully vaccinated. In somewhat related news, DIS reached a deal with unions to require all employees be vaccinated.

In earnings news, the retail sector continues to impress as BBY posted a beat on revenue and 58% obliteration of earnings estimates. BBY stock was up 6% in pre-market trading on the news. AAP also beat on both lines, but PDD missed on revenue from the retail sector this morning. In other sectors, MDT and BNS beat on both lines as well. In fact, for the earnings season, 90% of the S&P500 have reported an average earnings gain of 95% year over year.

Related to the virus, new US infections are continuing to rise, but with analysts saying we may have reached the peak of this Delta surge. The totals rose to 38,814,596 confirmed cases and deaths are now at a total of 646,667. Remember that these numbers are now under-reported as many (mostly Southern) states have decided to stop reporting data on a daily basis. Nonetheless, on the data we do have, the number of new cases is increasing at an average of 147,693 new cases per day. Deaths, which lag, are also still rising and are now at 846 per day.

Overnight, Asian markets were green across the board as Chinese tech stocks rallied hard. Hong Kong (+2.46%) and Malaysia (+2.03%) were standouts. However, the major exchanges all saw about a 1% gain. In Europe, markets are mixed on modest moves so far today. The FTSE (-0.16%), DAX (+0.32%), and CAC (-0.39%) are typical of the region at mid-day. As of 7:30 am, US Futures are pointing to modest gaps higher at the open. The DIA is implying a +0.14% open, the SPY implying a +0.18% open, and the QQQ implying a 0.26% open at this hour. The dollar and 10-year bond yields are flat in early trading, but Oil (WTI) is showing another 1.8% gain to $66.84/barrel.

The major economic news scheduled for release on Tuesday is limited to July New Home Sales (10 am). The major earnings reports scheduled for the day include AAP, BNS, BBY, HTHT, MDT, and PDD before the open. Then after the close, VNET, HEI, INTU, JWN, SCSC, TOL, and URBN report.

In Asia, it seems the worries over Chinese Tech regulations and Covid have eased (China reported no cases for a second straight day after their draconian regional crackdown). Europe seems to also be in a better mood as the PFE-BNTX vaccine approval in the US eased some concerns and Fed tapering expectations have been calmed by recent statements. With breadth (T2101) up off its lows and back into the highs of the period since the Spring rally and stocks at all-time highs again, the bulls are looking for some follow-through this morning.

As always, manage your existing trades before you go chasing any new ones. Concentrate on the process and on managing those things you can control. Good trading rules and discipline is what separates long-term success from failure in trading. So, trade with the trend. If you miss a move, just admit it and move on to the next chart. Never chase price on an entry and remember to keep your losses small by using stops or hedges. And always consistently take profits when you have them.

Ed

Swing Trade Ideas for your consideration and watchlist: SPT, ARRY, DKNG, MS, AMRN, SWCH, GNOG You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

The choppy relief rally slowly gained strength on Friday, providing a considerable improvement on the technical front as the SPY and QQQ recovered price supports. Of course, we still have overhead resistance levels to deal with, but if the premarket surge holds through the pending economic report, the QQQ is easily within striking distance of new records. The small-cap IWM remains the weakest index, but with oil perking up this morning, look for some modest improvement. That said, the economic data may still put some stumbling blocks in the path forward, so prepare for the wild price volatility to continue.

Asian markets surged off last week’s lows, lead by the NIKKEI up 1.78%, as it recovered from last week’s bearishness. This morning, European markets trade in the green across the board, feeling some sweet relief after the recent selloff. Ahead of earnings and possible market-moving economic data, U.S. futures look to extend Friday’s rally, with the QQQ pushing for a record-breaking breakout.

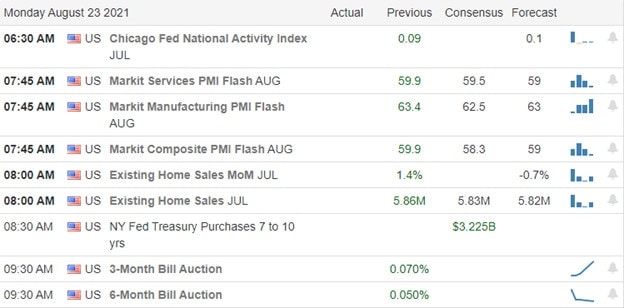

Economic Calendar

Earnings Calendar

We have 25 companies with several unconfirmed expected on the Monday earnings calendar. Notable reports include JD, MSGE, & PANW.

News & Technicals’

As evacuations continue from the Kabul Airport, a firefight broke out between Afghan security and unknown attackers. Once Afghan security personal was killed and three others wounded. Treasury yields begin the week slightly higher this morning, with the 10-year trading up to 1.273% and the 30-year trading at 1.889%.

On Friday, we saw considerable improvement on the technical front, with the SPY and QQQ surging above resistance levels. With futures surging this morning, the DIA will join them as the QQQ stretches toward a possible new record. However, we do have some possible stumbling blocks in this week’s economic reports. Which includes PMI, Durable Goods, GDP, housing data, and even some Fed speak from the chairman. Keep a close eye on the price action as we test record resistance highs, and with earnings reports winding down, it may not be as easy to ignore concerning economic data as we have seen of late. In addition, the sharply lower consumer sentiment may prove to be problematic for market gains if housing and durable goods orders continue to slip or inflationary numbers continue to rise.

Markets opened relatively flat on Friday. However, the dip-buyers showed up and led a choppy rally all day long. This left us with strong bullish candles in all 3 major indices that all closed very near their highs. On the day, SPY gained 0.77%, DIA gained 0.48%, and QQQ gained 1.04%. The VXX fell 7.5% to 27.75 and T2122 jumped back up into the mid-range at 41.61. 10-year bond yields rose a bit to 1.257% and Oil (WTI) fell 2.26% to $62.25. For the week, all 3 major indices gave us long-legged, indecisive, Doji-like candles with the SPY down 0.60%, DIA down 1.19%, and QQQ lost 0.30%.

The annual Jackson Hole Economic Policy Summit coming up at the end of this week. The recent talk (mostly from non-voting FOMC members in public events) has all been centered around starting the bond-buying taper soon. That’s assumed to be the main point of discussion among the global central bankers at the end of the week. However, it was interesting to note that on Friday, Fed hawk Kaplan (not a voter) who has been calling for quicker bond-buying taper changed his tune slightly. In a Friday interview, Kaplan told Fox News he may rethink his position on calling for a quick taper if it continues to look like the Delta variant spread is slowing economic growth. He went on to say “it’s in our interest to slow the spread and right now we’re in a negative trend.”

Bitcoin hit $50,000 on Sunday night, which was a 3-month high. This comes after a massive selloff in June and early July. The all-time high of $64,000 was reached in April prior to the selloff. Among the drivers of the recent rally was that COIN announced it would buy $500 million in crypto for its balance sheet and also allocate 10% of company profits to go into cryptocurrencies in future quarters.

In miscellaneous stock news, TGT announced they will triple the number of “shop in a shop” DIS stores they host in their stores. TGT will add 100 DIS shops in existing TGT stores before the holiday season. This seems to be a counter move to M announcing a few days ago that it will be adding Toys-R-Us “shop-in-a-shop stores. Both seem to be hopeful signs for the brick-and-mortar retail space and perhaps for the economy in general.

Overnight, Asian markets were almost exclusively green. Only Singapore (-0.49%) was in the red, while Taiwan (+2.45%), Shenzhen (+1.98%), and Japan (+1.78%) led the gainers. In Europe, PMI data out of the EU remains strong (59.5) for July. This has led to green across the board at mid-day in the region. The FTSE (+0.49%), DAX (+0.25%), and CAC (+0.93%) lead the way as usual, with most of the continent’s exchanges falling somewhere between the FTSE and DAX. As of 7:30 am, US Futures are pointing toward a modest gap-higher. The SPY is implying a +0.43% open, the DIA implying a +0.35% open, and the QQQ implying a +0.31% open at this hour. 10-year bond yields are up slightly to 1.275% and Oil is trading 3% higher in early trading as the dollar is trading down significantly this morning.

The major economic news scheduled for release on Monday is limited to Mfg. PMI and Services PMI (both at 9:45 am) and July Existing Home Sales (10 am). The major earnings reports scheduled for the day are limited to JD before the open. Then after the close, PANW reports.

Good global economic data should give the bulls a little tailwind early today. However, US PMI data for July comes out at 9:45 am, and with few earnings or other data expected, that is likely to drive the tune for the remainder of the day. Breadth picked up in the rally the last few days. However, this is still far from what could be called a broad-based bull charge. So, continue to trade carefully and focus on the trend in your trading horizon.

As always, manage your existing trades before you go chasing any new ones. Concentrate on the process and on managing those things you can control. Good trading rules and discipline is what separates long-term success from failure in trading. So, trade with the trend. If you miss a move, just admit it and move on to the next chart. Never chase price on an entry and remember to keep your losses small by using stops or hedges. And always consistently take profits when you have them.

Ed

Swing Trade Ideas for your consideration and watchlist: RIOT, CAN, MRVL, SWCH, MARA, DLTR, EBAY. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Looking at the daily index charts, one could quickly think the relief rally looks underway but look deeper, and you will see another challenging day of price action. The bears have gained some confidence, much more willing to fight for dominance than we have seen recently. With a light day of earnings and economic data to provide inspiration and markets around the world experiencing selling pressure, the bulls have a challenging task ahead to defend price support heading into the weekend. Plan your risk carefully!

With more Chinese regulatory scrutiny in tech and now real estate, Asian markets sold off strongly led by Hong Kong, with the HSI dipping into bear territory. European markets currently see red across the board, and the weekend nears. Finally, with a light day of earnings and economic data, U.S. futures point to a bearish open that may test the bull’s willingness to defend yesterday’s low in the Dow. Expect volatility as the bulls and bears fight for dominance.

Economic Calendar

Earnings Calendar

We have a light day on the earnings calendar to round out the trading week with only 7-verified reports. Notable reports include BKE, DE, and FL.

News & Technicals’

Another challenging day of price action with buying in big tech, health care, and defensive stocks proving some safe-haven spots for traders. However, the divide between winners and losers continues to grow as more and more stocks fall below their 200-day averages. The VIX pulled back from its intraday high but ended the day above a 20 handle, suggesting more price volatility in the days ahead. Although the DIA, SPY, and QQQ experienced a bit of a relief rally, the 4-week new high/new low ratio surprisingly remained in a short-term oversold condition. China passed new tech regulations and looked to expand its crackdown to real estate. As a result, Hong Kong markets fall into bear territory to close out the week.

Yesterday’s rally was nice, but it was not nearly enough to recover broken support levels. Moreover, with the premarket action threatening a bearish open, the risk of severe technical damage is growing. Should the bears find the energy to push prices below yesterday’s lows, we could experience a very rough day of a pile on selling into the weekend. With a very light day of earnings and economic data, the bulls will have to work hard to find enough inspiration to encourage buy the dip traders to take the weekend risk. That’s a big ask, with Asian markets closing decidedly bearish and European markets seeing red across the board in the worst week of trading since February. As the bulls and bears battle for dominance, expect the price action to remain challenging with the VIX elevated.

Despite better-than-expected Initial Jobless Claims, markets gapped down hard at the open Thursday. This took us to or near the 50sma in all 3 major indices. However, the bulls stepped in immediately and rallied stocks into the highs just lunch. From there we saw another down wave and rally as the volatility took us on a final down leg at the close. This all left us with large-body, white candles with upper wicks amid small overall moves. On the day, SPY gained 0.17%, DIA lost 0.18%, and QQQ gained 0.48%. The VXX gained 3.2% to 30.00 and T2122 dropped deeper into the oversold territory at 5.71. 10-year bond yields fell again to 1.242% and Oil (WTI) dropped 2.15% to $64.05/barrel.

Thursday night, TSLA CEO Elon Musk announced plans to build a “Humanoid Robot” he dubbed the “Tesla Bot.” The stated goal of the robots will be to eliminate the need for humans to do “dangerous, repetitive, and boring tasks.” As with most of Musk’s “inventions,” robots have been a widely-known concept for centuries and an actual product for decades. However, I’m sure the TSLA robot will be “world changing.” In either case, the news and related tweets are giving TSLA stock a little boost in premarket trading.

China has passed a major “personal information protection law,” somewhat similar to the laws in place in the EU since 2018 and the recent AAPL vs FB “consent changes” for iPhone users. This set of regulations lays out strict guidelines related to the collection, storage, and use of personal information by companies. While the law has passed on Friday and goes into effect on November 1, the final draft has not been made public yet. This is all part of the recent sweeping regulation of the technology sector, in particular, focused on phone apps and websites.

Japan’s massive auto companies were all down sharply following the Thursday evening announcement by Toyota that it is slashing global production for September by 40%. The reason for the cuts is a lack of chips and no more room to store partially completed vehicles. Toyota did stress that it still believes it can hit its annuals production and sales targets. Toyota was down 4.09%, Nissan dropped 7.25%, and Honda fell 4.84% on the day. This news may have hurt US automakers Thursday and is not likely to give them any help today. So, keep an eye on F, GM, STLA, and major parts suppliers.

Overnight, Asian markets were mostly in the red again. Hong Kong (-1.84%), Shenzhen (-1.61%), and Shanghai (-1.10%) led the region lower. In fact, the Hong Kong Hang Seng moved into the Bear territory, down more than 20% from the February highs. In Europe, markets are red nearly across the board in the early afternoon. The FTSE (-0.24%), DAX (-0.48%), and CAC (-0.52%) are typical of the continent mid-day. As of 7:30 am, US Futures are pointing to another gap lower. The DIA is implying a -0.47% open, the SPY implying a -0.47% open, and the QQQ implying a -0.30% open at this hour. 10-year bond yields are also lower to 1.233% and Oil (WTI) off eight-tenths of a percent in early trading with the dollar showing a little early strength.

The only major economic news scheduled for release on Friday is a Fed speaker (Kaplan at 11 am) and Options Expiration (after the close). The major earnings reports scheduled for the day include DE and FL before the open. There are no earnings reports scheduled for after the close.

With markets looking at the first appreciable weekly loss in a month, the bears are continuing to draw strength from the fear of Fed bond tapering and the Covid-19 resurgence. As mentioned above, today is also options expiration Friday. So, expect a little volatility and perhaps some pinning in the afternoon. Just remember that we are sitting at or near the 50sma (potential support) and are only 2% off the all-time highs. So, don’t go all-in either direction just yet, especially in front of the weekend news cycle. Trade carefully.

As always, manage your existing trades before you go chasing any new ones. Focus on the process and on managing what you can control. It is good trading rules and discipline that separates long-term success from failure in trading. So, trade with the trend. If you miss a move, just admit it and move on to the next chart. Never chase price on an entry and remember to keep your losses small by using stops or hedges. And always consistently take profits when you have them. Lastly, remember it’s Friday…and Friday is payday.

Ed

Swing Trade Ideas for your consideration and watchlist: GTBC, EBAY, CHRS, HUT, X, NUE. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

The thought that the Fed is considering tapering easy money policies brought out the bears yesterday afternoon. The selling is starting to create some technical damage in the DIA, SPY, and QQQ and likely shake the uber bulls’ confidence. With Jobless Claims and Philly Fed numbers before the bell, we could have a challenging price action open depending on the results. However, with the overall market, so helplessly addicted to money printing, I would not be too surprised if the taper tantrum withdrawal symptoms create more challenges on the path forward.

Asian markets traded in the red across the board last night, with Hong Kong leading the way as it plunged 2.13%. European markets also see nothing but red across the board due to the taper talk and falling oil prices. U.S. Futures continue to fall as earnings roll out with potential market-moving data before the bell that worsen or significantly improve the open depending on the results. So, buckle up; it could be a wild ride this morning.

Economic Calendar

Earnings Calendar

The Thursday earnings calendar has indicates 46 companies expected to report, with about half of them unconfirmed. Notable reports include AMAT, BZUN, BILI, BJ, EL, GFI, KSS, M, MSGS, NCMYGY, WOFF, QIWI, ROST, SDRLF, TPR,& VSCO.

News & Technicals’

We learned from the FOMC minutes that the committee is talking about tapering easy money policies this year. But, with the market so incredibly addicted to money printing, the bearish reaction pushed all the indexes lower with selling into the close. Treasury yields, surprisingly, traded lower this morning despite the taper talk. The 10-year fell four basis points to 1.233%, with the 30-year also dropping four basis points to 1.87%. Tesla is apparently struggling with vehicle delivery as customers are told they will have to wait for weeks or even months as delivery dates keep slipping. According to sales staff, they are not being told what is causing the delays and cannot answer customer’s questions. However, Toyota says it will cut global production by 40% due to the pandemic impacts of semiconductors and other parts shortages.

After the late afternoon selloff yesterday, some technical damage is beginning to show in the index charts. The DIA, SPY, and QQQ closed below support levels. With the premarket activity currently pushing lower, the damage could worsen this morning unless the bulls go to work and defend. Nevertheless, a little ray of sunshine with the 4-week new low/ new high ratio suggests we are near a short-term oversold condition and could bounce soon. However, that will likely depend on the Jobless claims results, which will come out before today’s open. Economists estimate 365,000 claims filed, which would be a modest improvement over last week’s reading. Please keep your fingers crossed because should it miss, the bears could keep going selling pressure.

Markets just ground sideways Wednesday…right up until the July FOMC minutes came out. From that point onward the bears just hammered the bulls as stocks went out on the lows. This left us with nasty black candles with upper wicks and short-term downtrends in all 3 major indices. On the day, SPY lost 1.07%, DIA lost 1.04%, and QQQ lost 0.96%. The VXX gained almost 7% to 29.05 and T2122 dropped well into the oversold territory at 8.47. 10-year bond yields held steady at 1.265% and Oil (WTI) dropped over 2.6% to $64.83/barrel.

The cause of that sharp afternoon selloff was the July Fed Minutes. As had been signaled by recent Fed member statements (but apparently not believed), the FOMC has had discussions about tapering its bond-buying program this year. In fact, most of the participants noted that if the economy continues to evolve as expected, they’d support tapering bond purchases before year-end. Not today, but perhaps announcing a timetable at the September meeting and then slowly beginning the taper in October.

Strong Retail earnings continue to be the theme of the week. So far this morning, M absolutely crushed their report (beating by $668 million dollars on revenue and coming in 11 times higher than the average estimate on earnings, $1.29 vs $0.18 expected). KSS also more than doubled the average analyst estimate on earnings and raised guidance for the full year. Finally, while TPR beat, it was a pedestrian beat by comparison to the other two retail names reporting this morning.

In other retail-related news, CNBC reports that AMZN is planning to open large retail locations, starting in CA and OH. The stores will be similar to department stores but on the small side of size, similar to a KSS store. Meanwhile, in addition to their earnings, M also reported that they have partnered with “Toys R Us” and will offer that brand via “shop within a shop” areas in 400 of the M stores starting in 2022.

Overnight, Asian markets were strongly in the red again as even more Chinese regulations were announced. Taiwan (-2.68%), Hong Kong (-2.13%), and South Korea (-1.93%) led the parade, but losses were widespread and significant. Only New Zealand (+1.87%) bucked the trend as its national 3-day lockdown continues. In Europe, markets are down sharply across the board at this hour. The FTSE (-1.98%), DAX (-1.75%), and CAC (-2.44%) are typical for the continent at mid-day. As of 7:30 am, US Futures are pointing to gap-down follow-through of yesterday afternoon’s selloff. The DIA is implying a -0.91% open, the SPY implying a -0.83% open, and the QQQ implying a -0.69% open at this hour. 10-year bond yields are also falling, now at 1.23% and Oil (WTI) is off almost 4% to $62.98/barrel in early morning trading.

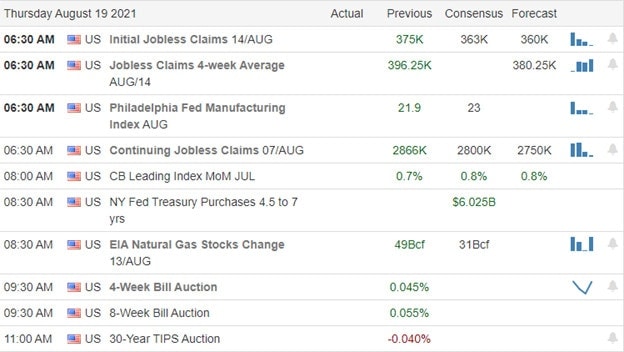

The major economic news scheduled for release on Thursday is limited to Weekly Initial Jobless Claims and Philly Fed Mfg. Index (both at 8:30 am). The major earnings reports scheduled for the day include BILI, BJ, EL, KSS, M, PFGC, and TPR before the open. Then after the close, AMAT, FTCH, and ROST report.

Fear of Fed tapering, combined with slowing economic data and the Covid-19 resurgence are giving the bears plenty of ammunition. This might not have been helped when HOOD warned of a slowdown in trading volume. So, the long-awaited pullback is underway with the 50sma as the destination (possible support?) this morning. Beware of volatility, remember that the longer-term trend is still bullish, and remember that we are only 2.5% off the all-time highs as well as bear moves tend to happen faster than bull moves. So, trade carefully.

Today is the kind of day where it pays to remember two things. Cash is a position. And you don’t HAVE to trade every day. Always manage your existing trades before chasing new ones. Focus on the process and on managing what you can control. Trading rules and discipline are what separates long-term success and failure in trading. So, trade with the trend until the trend is broken. If you miss a move, just admit it and move on to the next trade. Never chase price on an entry and remember to keep your losses small by managing stops. And always consistently take profits when you have them.

Ed

Swing Trade Ideas for your consideration and watchlist: No trade ideas today. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

After a disappointing retail sales number, the bears woke from their summer hibernation to reverse the previous rally that set new records. Though the whippy price action likely shook trader confidence at the end of the day, the bullish trends in the DIA, SPY, and QQQ remain. However, with housing number before the open and the FOMC minutes later this afternoon, prepare for another day of volatile price action that likely favors quick intraday traders.

Asian markets mostly rallied overnight after the reserve bank of New Zealand keeps rates unchanged. However, European markets trade mixed but mostly lower as they monitor inflation data. The U.S. futures point to mixed open ahead of economic and earnings data, but that could quickly change depending on the housing numbers. So hang on tight; the ride is about to take another lap.

Economic Calendar

Earnings Calendar

We have 35 companies listed to report on the Wednesday earnings calendar, with many of them as unconfirmed. Notable reports include CSCO, ADI, BBWI, EAT, PLCE, NVDA, LITE, LOW, KEYS, RRGB, SNPS, TGT, TJX, VIPX, & ZTO.

News & Technicals’

Lowe’s beat on the top and bottom line this morning, and the stock is priced higher this morning, trying to recover some of yesterday’s losses. Target also topped earnings targets and raised forecasts, but the retailer is trading lower in the premarket. After the bell, CSCO, NVDA, and HOOD will report their results. Treasury yields rose this morning as we wait on the FOCM minutes later this afternoon. The 10-year gain nearly two basis points to 1.275%, and the 30-year rose to 1.933%. Europe is scrambling to formulate an Afghanistan refugee plan, trying to avoid repeating the 2015 crisis. An emergency meeting of the most affected countries did not invite the United States after the Taliban seized control of the country.

The bears woke from their summer hibernation yesterday after the very disappointing retail sales number. The pullback included some violent intraday whipsaws that ended the day printing bullish hammer patterns with the afternoon rally. Please remember that hammer patterns required a bullish follow-through to be valid, so be careful rushing in to buy the dip. Before the bell, we have another potential market-moving report with the Housing Starts and Permits, expecting a minor pullback in the consensus. Finally, after some moring price volatility, we could see price action become light and choppy as we wait for the release of the last FOMC minutes. I think it’s unlikely that we will learn anything more about the possibility of a Fed taper, but if we do, there could be another shot of wild price swings in reaction. That said, after yesterday’s selloff, the DIA, SPY, and QQQ bullish trend suffered little to no damage though I can’t say the same for trader confidence.

US markets gapped down two-thirds to three-fourths of a percent at the open Tuesday and then ground sideways until late morning. The bears took us a leg further down into the speech of Fed Chair Powell, but then the bulls stepped in and gave us a slow rally back up into the close. This left us will indecisive Doji-type candles in all 3 major indices, none of which fell outside the recent trading range. So, we have an indecisive pullback on greater than average volume. The VXX rose 3% to 27.20 and T2122 dropped down just outside the oversold territory at 21.86. 10-year bond yields held steady at 1.263% and Oil (WTI) fell three-quarters of a percent to $66.78/barrel.

In economic news, July Retail Sales came in far below expectations before the open yesterday. This was the proximate cause for the gap down open. That said, WMT and HD beat on revenue Tuesday while TGT and LOW both beat on revenue already today. So, the slowdown appears to be happening at “Mom and Pop stores” rather than at the big-box chains. Beyond Retail, July Industrial Production almost doubled forecasts, and June Business Inventories came in just as expected.

As mentioned, markets were relieved when Fed Chair Powell spoke Tuesday. In his speech, he did not touch on either the economy or Fed monetary policy. Instead, he focused on Covid-19 and its impact on US students, saying the challenges will mold them into an “extraordinary generation.” During the Q-A portion of the event, he did decry the impact of Covid on economic activity and the pace of vaccinations slowing, as well as talking about how digital currencies are interesting and becoming a more important question that the Fed is considering.

Following up on the Retail theme from yesterday, it appears that big beats on both lines by TGT and LOW are resulting in both premarket volatility and punishment. TGT in particular reported blow-out numbers but was down well over 5% in premarket trading. (The cause of this divergence is reportedly fear of slowing sales growth and Covid resurgence hurting next quarter’s numbers.) Meanwhile, after HD’s post-beat smackdown (losing over 4% yesterday), this morning GS has raised their target for the company above the rest of the analysts covering the name.

Overnight, Asian markets were mostly green as the region rebounded a bit from the Tuesday news of Chinese Internet Antitrust regulations. Shanghai (+1.11), Taiwan (+0.99%), and Shenzhen (+0.72%) led the gainers, with typical gains more like half of a percent. In Europe, markets are mixed on modest trading. The “Big 3” exchanges are all modestly red, but the bulk of the rest of the region are in the green. The FTSE is down 0.29%, DAX down 0.11%, and CAC down 0.34% at mid-day. As of 7:30 am, US Futures are mixed and flat. The DIA is implying a -0.20% open, the SPY implying a -0.08% open, and the QQQ implying a +0.10% open. 10-year bond yields are up slightly to 1.275% and Oil is up almost a percent to $67.23/barrel in early trading on a flat US dollar.

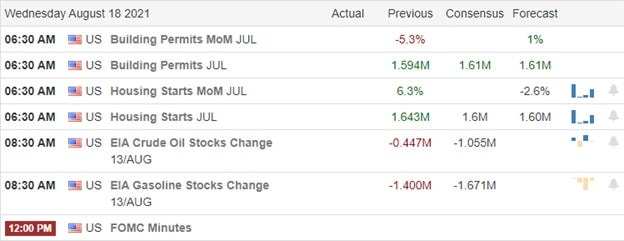

The major economic news scheduled for release on Wednesday includes July Building Permits and July Housing Starts (both at 8:30 am), Crude Oil Inventories (10:30 am), and FOMC Minutes (2 pm). The major earnings reports scheduled for the day include ADI, EAT, LOW, TGT, TJX, VIPS, WB, and ZIM before the open. Then after the close, BBWI, CSCO, YY, KEYS, NVDA, SPTN, and SNPS report.

Covid continues to make news as GS reinstituted mask mandates in the office, FB pushed out their return to the office date again, and the TSA extended travel mask mandates through mid-January. This is adding to market fears at the highs. However, we are not yet seeing any panic as we did in March 2020. Earnings continue to be stellar, but mortgage rates hit their highest level in a month (3.06% for a 30-year fixed) as both refinance and new mortgage demand dropped this week. All that said, despite the fear, yesterday’s candles in the major indices show that the bulls are simply not ready to roll over. All 3 major indices closed in the top third of their range, having driven price up off the lows following the gap-down. So, don’t mistake volatility for a changed trend just yet.

Trading rules and discipline are what separates long-term success and failure in trading. Focus on the process and on managing what you can control. Always manage your existing trades before chasing new ones. Trade with the trend until the trend is broken. If you miss a move, just admit it and move on to the next trade. Never chase price on an entry and remember to keep your losses small by managing stops. And always consistently take profits when you have them.

Ed

Swing Trade Ideas for your consideration and watchlist: ALKS, LSI, FOLD, FAS, WBA, NAVI, NVAX, AMRN. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service