Though Friday morning started slow and choppy, the afternoon was celebrated with substantial exuberance after the House passed a more than 700 billion dollar deficit spending bill. The tech giants led the rally as they surged higher, extending the index charts until the day’s close. Today we begin with reports from Empire State Manufacturing, followed by the Housing Market Index, some Fed speak, and short-term bond auctions as earnings inspiration slow. Expect the market to rest sideways from this extended condition or begin a pullback at any time.

During the night, Asian markets traded mixed as Chinese economic reports showed their economy continues to slow. European markets trade flat but mainly bullish this morning, trying to build on the cautions gains of last week. However, after a four-week winning streak, U.S. futures point to a modest gap down open with manufacturing and housing data pending.

Economic Calendar

Earnings Calendar

With the bulk of earnings behind us, we will see many more small-cap reports with a few possible market movers mixed in but expect them to continue to decline. Notable reports include BLND, COMP, FN, TME, TDUP, WEBR, WWE, & ZIP.

News & Technicals’

Retail sales grew by 2.7% in July from a year ago, the National Bureau of Statistics said Monday. That’s well below the 5% growth forecast by a Reuters poll and down from growth of 3.1% in June. Likewise, industrial production rose by 3.8%, missing expectations for 4.6% growth and a drop from the prior month’s 3.9% increase. In addition, investment in real estate fell at a faster pace in July than in June, while investment in manufacturing slowed its pace of growth. Medicare is gaining the power to negotiate prices for certain drugs and punish pharmaceutical companies that don’t play by the rules. The legislation represents a historic expansion of Medicare’s power that was fiercely opposed by the pharmaceutical industry. But the negotiation powers are limited in scope, and some lawmakers argue that legislation doesn’t go far enough. The fourth quarter will be “the challenge” for Malaysia’s economy if global headwinds such as Russia’s war on Ukraine and China’s zero-Covid policy persist, said Finance Minister Zafrul Aziz. Growth momentum for July to September should be strong, but this could result from an unfavorable base effect from the same time in the previous year, Zafrul said. On Friday, Malaysia’s central bank announced that the country’s economy grew 8.9% from April to June from a year earlier. Starbucks, Kraft Heinz and Mondelez, are among the companies focusing on premium products during the cost-of-living crisis. By “beefing up their premium proposition” as well as value products, companies can capture and retain trade-down audiences, says Paul Martin, KPMG’s head of retail. Tesla has made over three million cars, CEO Elon Musk tweeted on Sunday. “Congrats, Giga Shanghai, on making the millionth car! Total Teslas made now over 3M,” Musk tweeted. Treasury yields trade with little changed early Monday, with the 2-year at 3.25%, the 5-year at 2.96%, the 10-year at 2.83%, and the 30-year at 3.10%.

Trading on Friday started slow but picked up strongly in the afternoon, stretching the extended index charts with substantial exuberance. Big tech names surged upward after the news that another more than 700 billion dollar spending bill had passed in the House. The market loves deficit spending, while the T2122 indicator and bond inversions suggest a pullback could begin at any time. Of course, Fed members warn that inflation is still unacceptably high and rate increases will continue, but the excitement of the rally has allowed traders to ignore that inconvenient truth. Today we get a reading from Empire State Manufacturing, the Housing Market Index, some Fed speak, and short-term bond auctions.

On Friday, markets gapped up a half of a percent. After an hour of finding their footing, the bulls began a slow, steady, all-day rally that ran right into the close. This left all 3 major indices printing large white candles with small lower wicks. On the day, SPY gained 1.69%, DIA gained 1.23%, and QQQ gained 1.95%. All 10 sectors were in the green with Technology leading the charge again. The VXX also gained 1.66% to 22.05 and T2122 drove even higher into overbought territory at 97.41. 10-year bond yields fell to 2.842% and Oil (WTI) dropped back to $91.88/barrel. Clearly it was a risk on day.

This all capped the fourth straight week of gains, with SPY gaining 3.30%, DIA gaining 3.01%, and QQQ gaining 2.69% for the week. It also cut the losses of the longer-term pullback in half, which may be a key indicator. (No bear market rally since 1950 has halved its losses from the highs and then returned to new lows. In other words, if the past is a good indicator, the bottom is now in and the bulls have history on their side.) With that said, the Fed is still expected to continue raising rates (in smaller increments) for at least another six months. This means it may still be too early for the broader market to pivot into a “Fed Bull” mode of chasing growth again (at least according to GS as reported by CNBC).

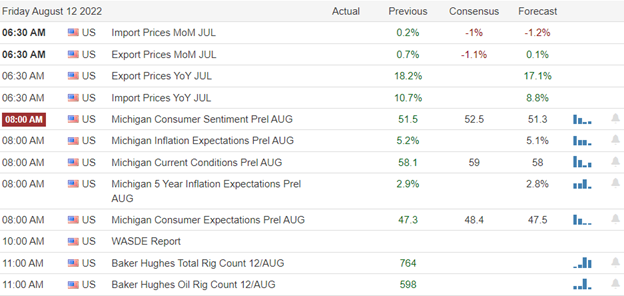

In economic news, both Imports and Exports were down more than expected in July (possibly indicating a global economic slowdown). However, it was Exports that were much lower than expected (-3.3% vs -1.1% forecast). The market took this to mean the Fed will have less reason to continue big rate hikes as we move forward. On the plus side, Michigan Consumer Sentiment and Expectations both came in well above the consensus estimate as well as the June numbers. This indicates that the public is now more comfortable with the economy and that policies are working as inflation falls and no huge recessionary impacts (mass layoffs) have started in this cycle. And, as always, a relatively happy consumer is good for corporate profits.

In stock news, on Friday, PTON announced it will cut 800 jobs, shut stores, and raise prices as the “High-End Bike/Treadmill as a subscription” business struggles to remake its business. After the close Friday, BA announced it has patched a vulnerability that could have allowed hackers to take control of on-board flight system (air speed, gauge readings, etc.) of some BA manufactured aircraft. On Saturday, activist hedge fund Starboard Value announced it has slashed its KSS holdings by 80% in Q2 after the fund’s proposed acquisition of KSS was rejected.

In Energy news, Germany has taken measure to cut natural gas consumption by at least 2%. The new law requires strict cutbacks by both public and private entities. These include only heating public buildings to 66 degrees, not allowing pools to be heated, as well as building and monument illumination turned off. Illuminated advertising will also be prohibited between 10 pm and 6 am. Elsewhere, in a surprise move, Mexico (which now imports 100% of the natural gas it uses) announced plans to become the world’s largest exporter of nat. gas. This includes 8 new exploration projects not far South of the US border that are expected to have a combined output of more than 50 million tons annually and are expected to come online as soon as 2023. (Those 8 projects alone would make Mexico the #3 global producer of LNG and produce 55% of the US total production.) Notable current LNG producers include CQP, LNG, SHEL, and TTE.

President Biden will sign the Inflation Reduction Act this week. Among the provisions is giving the HHS Dept. the authority to negotiate drug prices for the first time. (This was a huge loss for big pharma, which spent over $144 million lobbying and made more than $16 million in campaign contributions to defeat this measure.) Among the companies potentially impacted by negotiations are BMY ($11.5 billion in drugs now likely negotiated), MRK ($7.3 billion in drug sales impacted), JNJ ($5 billion in drug sales now to be negotiated), and ABBV ($3 billion in drug sales impacted) among others. **Note that these are not the sales amounts to be lost, but which are likely to be reduced by actual negotiated prices.

Overnight, Asian markets were mixed but leaned to the green side on mostly modest moves. Japan (+1.14%) and Taiwan (+0.84%) led the gains while Hong Kong (-0.67%) and Singapore (-0.38%) paced the losses. In Europe, a similar picture is taking shape at mid-day. The FTSE (-018%), DAX (-0.01%), and CAC (+0.01%) show a mixed, modest-move atmosphere while smaller exchanges show slightly stronger moves. For example, Denmark (+1.36%) leads the gains and Norway (-1.00%) paces the losses in early afternoon trade. As of 7:30 am, US Futures are pointing toward a down start to the day. The DIA implies a -0.45% open, the SPY is implying a -0.46% open, and the QQQ implies a -0.26% open at this hour. However, 10-year bond yields are down to 2.828% and Oil (WTI) is off over 5% to $87.48/barrel in early trading.

The major economic news events scheduled for Monday include NY Empire State Mfg. Index (8:30 am) and June TIC Net Long-Term Transactions (4 pm). The major earnings reports scheduled for the day include LI, NUI, WEBR, and WES before the open. Then, after the close, COMP, FN, GSM, NU, and TME report.

In economic news later this week, on Tuesday we get July Building Permits, July Housing Starts, July Industrial Production, and API Weekly Crude Oil Stock. Then Wednesday we get July Retail Sales, June Business Inventories, June Retail Inventories, EIA Crude Oil Inventories, a 20-year Bond Auction, and Fed Member Bowman speaks twice. Thursday Weekly Initial Jobless Claims, Philly Fed Mfg. Index, and July Existing Home Sales are announced and Fed Member George speaks. Finally, on Friday there is no major economic news.

In earnings later this week, on Tuesday we hear from ESLT, HD, SE, WMT, A, and JKHY. On Wednesday, ADI, LOW, PFGC, TGT, TJX, ZIM, AMCR, BBWI, SQM, CSCO, KEYS, SNPS, and ZTO report. Then Thursday, we get reports from BJ, CSIQ, EL, KSS, NICE, SPTN, TPR, AMAT, and ROST. Finally, on Friday we hear from DE, FL, and VIPS.

After the last 4 strong weeks and Friday’s strong move by the bulls, major indices look extended from their T-lines and according to T2122. In addition, China’s Central Bank surprised markets overnight with a rate cut last night. However, it was a small cut of 10 basis points on the 7 and 10-year lending rates. (Indicating they are concerned the Chinese and global markets are cooling too fast.) With that backdrop, we can expect another low volume, yet volatile, day. So, either look for longer horizons (loose stops and ability to ride fluctuations) or tighten up on the bat and take smaller, faster swings. Overall the trend remains bullish, but remember those stocks are extended/overbought…do not chase.

Remember that trading is our job. So, do the work and follow the process. Stick with your trading rules, trade with the trend, and take those profits when you have them. Demonstrate patience and wait for confirmation. Don’t be stubborn. If you have a loss, just admit you were wrong, respect your stop, and take the loss before it grows. When price does move in your direction, always move your stops in your favor (remember the “Legend of the man in the green bathrobe“…it is NOT HOUSE MONEY, it’s all OUR MONEY!). Lastly, remember that you get rich slowly and steadily in Trading…not by striking it rich on one or two trades. So, give up that lottery ticket mentality.

See you in the trading room.

Ed

Swing Trade Ideas for your consideration and watchlist: TWTR, MCD, ARKK, AMD, GRWG, NVDA, X You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

The improved CPI and PPI reports produced significant morning gaps but produced little to no buying follow-through momentumless low-volume chop. However, there is no question that the bulls are in control and own the current uptrend. Yesterday’s bearish topping candle patterns may be of no consequence because they also lacked conviction, and the overnight futures are already pumping for another gap up open. With a light day for earnings, inspiration traders may look to the Import/Export and Consumer Sentiment reports to keep the party going into the weekend.

Asian markets closed Friday mixed through the Nikkei bounced back up 2.62% by the end of trading. European markets trade with modest gains, cautious about future monetary policy and global growth concerns. However, with a light day of earnings U.S. point to another gap up ahead of economic reports. So, expect a push to close the week bullish but don’t rule out another pop and drop if the reports cannot generate some follow-though momentum in this short-term extended condition.

Economic Calendar

Earnings Calendar

Though we have about 60 companies listed on the earnings calendar for today, many of them are very small-cap or unconfirmed. Notable reports include BR, HNST & SPB.

News & Technicals’

According to market strategists, the Federal Reserve is unlikely to pivot from its hawkish interest rate hikes despite positive signs this week that inflation in the U.S. could be easing. As CPI and PPI soften, markets have started to moderate their expectations for Fed rate hikes. But that doesn’t mean it is “mission complete” for the Fed, said Ben Emons, managing director of global macro strategy at Medley Global Advisors. Victoria Fernandez, the chief market strategist at Crossmark Global Investments, said the Fed is nowhere near putting the brakes and turning dovish on rate hikes, given the current data. The chief financial officer of German energy firm RWE said it would burn more coal in the short term — but insists its plans to be carbon neutral in the future remain in place. Greenpeace has described coal as “the dirtiest, most polluting way of producing energy.” “To be very clear, it doesn’t change our strategy,” Michael Muller told CNBC of its carbon neutral plans. Retailers rushed to enter the subscription space, curating boxes of clothing and other items. But consumers are showing signs they’re no longer interested. Trunk Club, which Nordstrom acquired for an undisclosed amount in 2014, no longer exists. Stitch Fix, launched in San Francisco in 2011, is struggling to be profitable. Electric vehicle maker Rivian Automotive maintained its full-year guidance for deliveries Thursday. The automaker reported second-quarter revenue that was higher than Wall Street expected. But it trimmed its full-year financial outlook, saying investors should now expect a wider loss and lower capital expenditures than it had previously forecast. Treasury yields edge lower in early Friday trading, with the 2-year at 3.19%, the 5-year at 2.96%, the 10-year at 2.86%, and the 30-year at 3.13%. The 12-month bond remains inverted over the 2, 5,10,30-year bonds trading at 3.20%.

Though the CPI and the PPI generated significant morning gaps, the rest of Wednesday and Thursday lacked momentum in low-volume-chop. Yesterday produced a pop and drop but of very little significance as volume ruled the day, and the T2122 indicator barely budged from its extreme overbought condition. The premarket pump is already working for another morning gap up, so the bearish topping candle patterns left behind on Thursday may mean nothing with the bullish desire to hold this run into the weekend. Today we get readings on Import/Export prices and will take the temperature of the consumer with a look at their sentiment. With the bulk of the earnings season behind us, traders will have to weigh the overall results within a rising rate environment with weakening world economic conditions as we slide into fall.

With the month-over-month inflation rate decline, the market celebrated, but traders should keep things in perspective. An 8.5% inflation rate is still unacceptably high, and the Fed’s 2% target means we are still in a rate-increasing cycle, and the balance sheet reductions will continue. Today we will find out if the Producer Prices also enjoyed an inflationary reduction and get the latest reading on Jobless claims. The pace of market-moving earnings reports will quickly decline during the next couple of weeks, removing some of the current wild speculation risks. Watch for clues of a pullback should the bears find inspiration from these elevated levels.

Asian markets mostly rallied overnight after the better-than-expected U.S. inflation, with Hong Kong up 2.40% at the close. However, European markets don’t seem to share in the excitement of the 8.5% inflation rate trading flat to slightly lower this morning. U.S. futures look to continue the celebration pointing to a gap up open ahead of PPI and Jobless Claims. It seems odd, but the market loves the consumer punishing 8.5% inflation. Buy, Buy, Buy!

Disney plans to raise streaming prices after the service posts a significant operating loss. The no ads service is increasing $3 per month to $10.99, with the ads service priced at $7.99 per month. A bundle of Disney+ and Hulu, both with ads, will be $9.99 per month. Analysis by CNBC shows Beijing’s new trade blocks against Taiwan affect only about 0.04% of their two-way trade. Beijing’s retaliations against U.S. House Speaker Nancy Pelosi’s visit to Taiwan earlier this month include suspensions of imports of Taiwanese citrus, frozen fish, sweets, and biscuits and exports of natural sands to Taiwan. While mainland China and Taiwan’s trade should be largely unaffected by the new measures, heightened military drills in the Taiwan Strait may delay shipments, analysts say. Deliveries of Boeing 787 Dreamliners had been paused for much of the past two years. American Airlines said it received one of its 787 planes from Boeing’s South Carolina factory. Ethereum is moving closer to adopting a proof-of-stake model for its network, which is less energy intensive than the existing proof-of-work method. The network ran its last dress rehearsal before the major upgrade, which is expected to take place next month. Treasury yields traded mixed early Thursday, with the 2-year at 3.17%, the 5-year at 2.89%, the 10-year at 2.76%, and the 30-year at 3.03%.

With inflation declining to 8.5%, the market celebrated though Fed member Evens stated rate increases would continue. While it’s good news that inflation declined month over month, the Fed’s 2% target is still a long way off though it may give the committee some breathing room to decrease their aggressive pace. Today we get the latest read on jobless claims and will find out if the PPI also enjoyed a decline in inflationary produce costs. Volume remains strangely low, so watch for clues of a pullback if the bears happen to find some inspiration.

On Wednesday, July CPI numbers came in much better than expected and this led to the bulls gapping markets higher. The DIA gapped up 1.42%, the SPY gapped up 1.79%, and the QQQ gapped up a massive 2.39% at the open. This broke the market out of its pullback from the last couple of days. However, after the open, all the heavy partying was over, as the bulls failed to give us follow-through with prices chopping sideways with a slightly bullish trend most of the day. With that said, a rally at the end of the day took us out near the highs. This left us with gap-up, indecisive, Spinning Top or Hangman type candles in all 3 major indices.

All ten sectors were green with Technology and Consumer Cyclical up more than two and three-quarters percent. So, we definitely saw a risk-on day. With that said, all 3 major indices are also now fairly extended from their T-line (8ema). On the day, SPY closed up 2.04%, DIA was up 1.57%, and QQQ was up 2.79%. The VXX fell to 21.44 and T2122 (4-week New High/Low Ratio) is back up deep into the overbought territory at 95.18. Interestingly, 10-year bond yields were flat on the day at 2.785% and Oil (WTI) is back up 1.13% to $91.51/barrel on the session.

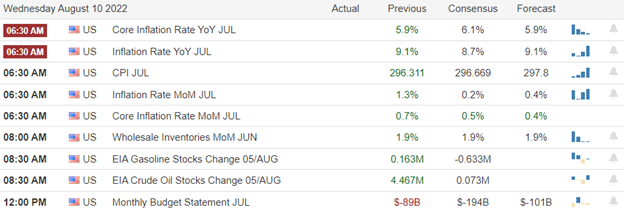

In economic news, as mentioned, July CPI came in a +8.5% annually. This was much better than the +8.7% expected and a lot better than June’s +9.1% annual reading. EIA Crude Oil Inventories followed Tuesday night’s API data came in dramatically higher than expected. The reading was +5.458 million barrels compared to a flat +0.073 mil barrels expected. The 10-year note auction came in at a lower than current 10-year yields (2.775% versus 2.785% open market) and significantly lower than the last auction (2.960%). Finally, the July Federal Budget Balance came in at 211 billion, which is down 30% from the same period in 2021.

In energy news, Russian oil deliveries to Hungary. Slovakia, and the Czech Republic after a Hungarian group agreed to pay Ukraine in dollars for the pipeline transit fees. This is a solution only for the month of August. Elsewhere, on Wednesday, LNT, WEC, NI, and PNM all announced that they are delaying the closure of coal-fired power plants in the US. This is seen as a political gesture in response to the climate provisions of the recently passed Inflation Reduction Act. All the companies cited delays or potential delays in the rollout of renewable energy projects when announcing the decision. In a follow-up to the EIA Crude report, they also announced a drawdown of 4.978 million barrels for the week. This indicates an increase in travel for the week.

After the close, DIS, AVT, and STN all reported beating on both the top and bottom lines. Meanwhile, CPNG, CACI, ENS, MFC, and VZIO all missed on revenue while beating on earnings. However, APP missed on both the revenue and earnings lines.

In stock news, APP made an all-cash offer to acquire U. This came the same day that U announced it has won a US government contract in partnership with CACI to provide simulation software. ACHR has received a $10 million pre-delivery payment from UAL in relation to UAL’s order for 100 of the ACHR electric vertical takeoff and landing aircraft. During its earnings reports, DIS announced that Disney+ subscriber growth was much higher than expected. Analysts had forecast 147 million, but DIS reported 152.1 million subscribers. Finally, JPM gold traders were found guilty of manipulating gold commodity prices by issuing bogus orders (canceled just before execution). They join traders from DB and BAC who were previously convicted for the same “order spoofing” crimes.

Overnight, Asian markets were almost green across the board. Only Japan (-0.65%) showed any red. Meanwhile, Hong Kong (+2.40%), Shenzhen (+2.05%), Taiwan (+1.73%), and South Korea (+1.73%) led the region higher. In Europe, most exchanges are on the green side, with the exception of the majors, at mid-day. The FTSE (-0.33%), DAX (-0.07%), and CAC (-0.19%) lag the rest of the region in early afternoon trade. As of 7:30 am, US Futures are pointing toward a green start to the day. The DIA implies a +0.42% open, the SPY is implying a +0.31% open, and the QQQ implies a +0.21% open at this hour. 10-year bond yields are back down to 2.772% and Oil (WTI) is up three-quarters of a percent in early trading this morning.

The major economic news events scheduled for Thursday include July PPI and Weekly Jobless Claims (both at 8:30 am). The major earnings reports scheduled for the day include AER, AIT, AZUL, BAM, CAH, DDS, HBI, KELYA, EYE, PRMW, SIX, and USFD before the open. Then, after the close, AQN, BAP, EDR, FLO, ILMN, OSCR, PFHC, RMD, RYAN, TOST, and VET report.

So far this morning, DTEGY, BAM, BFRS, USFD, DDS, AER, AIT, DDL, EYE, PRMW, and SLVM have all reported beats on both lines. Meanwhile, CAH, KELYA, and TAST all missed on earnings while beating on revenue. However, AEG, HBI, and SIX missed on both the top and bottom lines.

In economic news, later this week, on Friday the July Import/Export Price Index, Michigan Consumer Sentiment, and WASDE Ag Report are released.

After yesterday’s happy CPI news (if 8.5% inflation can be called happy news), traders are hoping for a similar story from PPI. (We know inflation is high, but we want to see Producer Prices coming in a bit to indicate that inflation has already peaked.) That sets up a binary even (similar to earnings, but in this case covering the entire market). If PPI comes in lower than expected, look for traders to gap stocks higher again. However, if PPI does not show the improvement we saw in CPI, I’d expect traders to believe they were overly optimistic yesterday and sell the market in a knee-jerk reaction. With that backdrop look for another low volume, volatile day. So, either look for longer horizons (loose stops and ability to ride fluctuations) or tighten up on the bat and take smaller, faster swings. Overall the trend remains bullish, but stocks are extended again relative to their T-lines and T2122.

Remember that trading is our job. So, do the work and follow the process. Stick with your trading rules, trade with the trend, and take those profits when you have them. Demonstrate patience and wait for confirmation. So, don’t be stubborn. If you have a loss, just admit you were wrong, respect your stop, and take the loss before it grows. Always move your stops in your favor (remember the “Legend of the man in the green bathrobe“…it is NOT HOUSE MONEY, it’s all OUR MONEY!). Lastly, remember that you get rich slowly and steadily in Trading…not by striking it rich on one or two trades. So, give up that lottery ticket mentality.

See you in the trading room.

Ed

Swing Trade Ideas for your consideration and watchlist: UAA, DIS, CVX, Z, BA, AMD, BAC, COF, GRWG, SBUX. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

The hurry up and wait low volume chop we’ve seen this week will be over once the CPI number is revealed. So, plan for premarket price volatility, likely creating an opening gap. After that, what happens next is anyone’s guess. The bulls hope this data will finally break the overhead resistance clearing the path for more upside. On the other hand, the bears hope for inspiration to defend the resistance with hopes for more market lows. Let’s hope we finally get some better volume providing directional conviction no matter what happens! Buckle up the drama is about to begin.

While we slept, Asian markets sold off as China’s inflation rose, with the Hong Kong tech selling off nearly 2%. European markets trade mixed and primarily flat, waiting on the U.S. inflation data and what it means for future FOMC actions. However, U.S. futures show the standard premarket pump-up we have seen during this relief rally, pointing to a bullish open ahead of the CPI report. Of course, after the reveal, anything is possible as traders and investors react.

Economic Calendar

Earnings Calendar

On this hump day, we have more than 170 companies listed but less than 100 confirmed, as is usual when small-cap reports ramp up. Notable reports include AAP, BMBL, COHR, CPNG, CYBER, BROS, DIS, FOXA, FNV, JACK, MFC, MTTR, PAAS, RRGB, SONO, COOK, WEN, & WWW.

News & Technicals’

Earlier this year, the Tesla and SpaceX CEO said on social media that he had “no further TSLA sales planned” after April 28. However, after Musk’s latest stock sales were revealed, Tesla fans and promoters asked the celebrity CEO if he was done selling shares in the electric vehicle business and if he might repurchase shares in the future. Asked if he was done selling Tesla shares, Musk replied: “Yes. In the (hopefully unlikely) event that Twitter forces this deal to close and some equity partners don’t come through, it is important to avoid an emergency sale of Tesla stock.” There have been mixed messages this quarter about streaming’s growth potential. If Disney+ meets or exceeds 10 million net adds, investors bullish on streaming will sigh relief. If it falls short, investors will question if CEO Bob Chapek can hit his target of 230 million to 260 million subscribers by 2024. Coinbase’s revenue declined almost 64% in the quarter as cryptocurrency prices fell. The exchange operator lowered its full-year forecast for transacting users. Coinbase said it was trimming 18% of its headcount during the quarter. Legal and General’s CEO Nigel Wilson described the UK’s cost-of-living crisis as “a tragedy for many, many people.” The typical household is expected to spend the equivalent of £4,266 on energy each year from January. Prime Minister Boris Johnson’s spokesperson said it would be up to his successor to make decisions on the matter. Sweetgreen lowered its 2022 forecast, citing weaker sales that began around Memorial Day. The chain said it laid off 5% of its support center workforce and will downsize to a smaller office building to lower its operating expenses. Shares of the company fell about 20% after hours. Deliveroo reported a pretax loss of £147.3 million in the first six months of the year, up 54% from the same period a year ago. The U.K., food delivery firm, said it is consulting on plans to exit the Netherlands, the latest withdrawal from a major European market following its retreat from Spain and Germany. Deliveroo said it would initiate its first-ever stock buyback program, purchasing up to £75 million in shares from investors. After President Biden ratified Finland and Sweden’s NATO membership, Russia halted U.S. nuclear inspections. Treasury yields moved slightly lower in early Wednesday trading, with 2-year at 3.26%, the 5-year at 2.96%, the 10-year at 2.78%, and the 30-year at 3.00%. However, the 6-month and the 12-month bonds are now inverted over the 5,10, and 30-year bonds painting a troubling picture of recession.

Markets chopped in a narrow range Tuesday as traders and investors waited for the CPI number that could inspire the bulls or the bears, depending on the result. However, the wait is almost over, and with indexes pressed against significant overhead resistance, expect considerable premarket price volatility likely to create an opening gap. In addition, depending on the outcome, we should expect considerable movement in the U.S. dollar and bond markets, adding some volatility to commodity prices after the report. After that, a Petroleum report, a Fed Speaker, a 10-year bond auction, and a Treasury Statement round out the day. Anything is possible, so buckle up and get ready for the show!

On Tuesday, the large-cap indices opened flat while the QQQ gapped down about six-tenths of a percent. From the open, both the SPY and QQQ sold off for about an hour. Then the entire market ground sideways in a tight range the rest of the day. This gave us indecisive, black-bodied (Spinning Top type) candles that are testing whether they can stay above their T-line (8ema). With that said, we are just seeing a pullback in an otherwise in-tact uptrend.

On the day, SPY fell 0.40%, DIA fell 0.16%, and QQQ dropped 1.13%. In terms of extension, VXX fell slightly to 21.94 and T2122 is back in the mid-range at 68.60. 10-year bond yields are up slightly by remaining at 2.779% and Oil (WTI) is also up very slightly to $90.50/barrel. So, overall, it was just another roller-coaster, “much ado about nothing” day on Wall Street.

In economic news, Q2 Nonfarm Productivity fell 4.6%, but that was better than the consensus forecast of -4.7% and far better than Q1’s -7.4%. As is normal when productivity falls, Q2 Unit Labor Costs rose 10.8% which was worse than the forecast rise of 9.5%, but still better than Q1’s +12.7%. After the close, API reported Weekly Crude Oil Inventories rose far more than expected. The estimate was a flat +0.073 million barrels. However, the actual build for the week was +2.156 million barrels.

After the close, WELL, SMCI, HRB, AKAM, GO, TTEC, and ANGI all reported beating on both the top and bottom lines. Meanwhile, WYNN, ADV, and MAXR all missed on revenue while beating on earnings. On the other side, DAR, SWX, and LNW beat on revenue while missing on earnings. However, COIN and RBLX missed on both the revenue and earnings lines.

In stock news, META raised $10 billion from its first-ever bond offering, with the proceeds slated to be used for share buybacks and investments in revamping the business. (This follows recent AAPL and INTC bond offerings.) NCLH pre-announced a loss for the current quarter with revenue below previous estimates. The cruise line said they expect occupancy rates will not reach pre-pandemic levels for another year, not at 65% of the 2019 levels. In contrast, rivals RCL and CCL are both saying they expect to be over 100% occupancy this year.

In energy news, Russian oil shipments to Central Europe (Slovakia, Hungary, Czech Republic) via pipeline by Transneft were halted Tuesday by Ukraine. The reason is that due to sanctions, Russia is unable to pay the transit fees to Ukraine. This has shut down 250,000 barrels per day of oil flow. Elsewhere, Bloomberg reports that the UK has a plan in place for at least several days of organized rolling blackouts next winter. The British government forecasts that electricity capacity will fall short by one-sixth of peak demand on cold days due to natural gas shortages (even after coal-fired generation plants are brought back online). Finally, the National Avg. Gasoline price has fallen below $4/gallon for the first time since March. Gas prices have fallen more than $0.18 in the last week and $0.72 in the last month. In somewhat related news, the Rhine river (a massive logistics thoroughfare for Europe, including oil, natural gas, coal, etc.) has become unpassable as a changing climate has dropped the water level too low for barge traffic over much of the major river.

Overnight, Asian markets were nearly red across the board. Only Singapore (+0.47%) and India (+0.06%) managed to stay in the green. Meanwhile, Hong Kong (-1.96%), Shenzhen (-0.87%), and Taiwan (-0.74%) led the region lower. In Europe, stocks are mixed but lean slightly to the green side at mid-day. The FTSE (+0.05%), DAX (+0.16%), and CAC (-0.12%) are typical of the region with only Norway (-1.14) and Denmark (+0.80%) showing significant moves in early afternoon trading. As of 7:30 am, US Futures are pointing toward a modestly green start to the day (before data). The DIA implies a +0.20% open, the SPY is implying a +0.24% open, and the QQQ implies a +0.29% open at this hour. 10-year bond yields are up slightly to 2.799% and Oil (WTI) is off almost 2% to $88.83/barrel in early trading.

The major economic news events scheduled for Wednesday include July CPI (8:30 am), EIA Weekly Crude Oil Inventories (10:30 am), 10-year Bond Auction (1 pm), and July Federal Budget Balance (2 pm). The major earnings reports scheduled for the day include ARCO, BHG, CAE, FOXA, HMC, LTH, NOMD, WEN, and WWW before the open. Then, after the close, APP, AVAH, AVT, BRFS, CACI, CPNG, ENS, MFC, STN, VZIO, and ZIMV report

So far this morning, WEN and LTH have reported beats on both lines. Meanwhile, WWW, ADRNY, RKUNY, DNPLY, and BHG all missed on revenue while beating on earnings. On the other side, HMC and NOMD beat on revenue while missing on the earnings line. However, VWDRY missed on both the top and bottom lines.

In economic news later this week, on Thursday we get July PPI and Weekly Jobless Claims. Then on Friday the July Import/Export Price Index, Michigan Consumer Sentiment, and WASDE Ag Report are released.

With CPI data on the docket this morning, expect pre-market trading to get volatile at about 8:30 am. (The consensus estimate is that we will see 8.7% annual inflation.) On a related note, BAC told clients they expect the yield curve to invert more deeply (more than any time since the 1980s) on the Fed’s inflation-fighting actions. Elsewhere, Elon Mush has sold almost $7 billion worth of TSLA stock. (This brings his total sale of TSLA stock to $32 billion since November.) He claims this most recent sale was a preventative move, to avoid a massive sale of the stock if the court rules against him in the TWTR court case. However, he also said he would buy more shares of TSLA in the event he wins the case. With that backdrop look for another low volume, volatile day. So, either look for longer horizons (loose stops and ability to ride fluctuations) or tighten up on the bat and take smaller, faster swings. Overall the trend remains bullish, even if we are pausing or pulling back a tick to ease over-extension.

Remember that trading is our job. So, do the work and follow the process. Stick with your trading rules, trade with the trend, and take those profits when you have them. Demonstrate patience and wait for confirmation. So, don’t be stubborn. If you have a loss, just admit you were wrong, respect your stop, and take the loss before it grows. Always move your stops in your favor (remember the “Legend of the man in the green bathrobe“…it is NOT HOUSE MONEY, it’s all our money!). Lastly, remember that you get rich slowly and steadily in Trading…not by striking it rich on one or two trades. So, give up that lottery ticket mentality.

See you in the trading room.

Ed

Swing Trade Ideas for your consideration and watchlist: CVNA, X, IGT, WFC, UBER, BAC, NTR, AA, NVAX, QNST, AR. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

A low volume sideways chop won the day after an energic early rally that eventually found some cautions sellers likely considering the ramifications of the pending inflation data. Unfortunately, with the CPI on Wednesday morning, we still have another day to hurry up and wait, with the future direction of the indexes on the line. With the indexes tucked tightly against resistance, the stage is set for a possible significant move, but the direction is anyone’s guess. So, consider the risk and plan carefully as we head into the close of the day.

Asian markets traded mixed overnight with a 7% drop in SoftBank with the Nikkei leading the declines. European markets traded in the red across the board this morning focused on U.S. inflation and the outlook of the FOMC. Ahead of a busy earnings day, U.S. futures reversed early gains pointing to a flat open with the uncertainty of the CPI data looming. Watch for intraday whipsaws as prices chop while we wait on data that could secure or disrupt the relief rally in the blink of an eye.

Economic Calendar

Earnings Calendar

We ramp up the number of earnings today with over 250 companies listed with a large group unconfirmed. Notable reports include AKAM, ARMK, ARWR, BHC, BE, COIN, CPRI, CG, CRON, DIN, EBIX, EMR, GFS, GO, HRB, HGV, H, IAC, IRBT, MAXR, NCLH, PRGO, PLNT, RXT, RL, RBLX, SAVE, SMCI, SYY, TTD, TTEC, U, WMG, WWE, & WYNN.

News & Technicals’

Spirit Airlines reported a second-quarter loss after costs surged despite a jump in revenue. The airline agreed to sell itself to JetBlue for $3.8 billion late last month. Spirit executives are scheduled to discuss results with analysts on Wednesday morning. Trump said that the FBI raided Mar-a-Lago, former President Donald Trump’s resort home in Palm Beach, Florida. In a lengthy statement, Trump said his residence was “currently under siege, raided, and occupied by a large group of FBI agents.” The raid came after months of questions about whether Attorney General Merrick Garland was planning to pursue investigations into the former president. Novavax cut its 2022 sales outlook by about 50% and now expects to generate $2 billion to $2.3 billion in revenue. Novavax previously forecasts $4 billion to $5 billion in revenue. CEO Stanley Erck said Novavax expects no new sales in the U.S. market or from Covax, an international vaccine alliance, in 2022. Ezra Miller, who portrays Barry Allen, aka the Flash, as part of the DC Extended Universe, has been charged with felony burglary in Stamford, VT. The felony burglary charge against Miller comes almost a year before Warner Bros. is slated to release “The Flash,” a $100 million film that is part of the studio’s DC franchise. The news comes just days after Warner Bros. Discovery’s CEO praised the film during an earnings call. Bed Bath & Beyond and AMC Entertainment surged as meme traders were betting on the stock despite the lack of apparent catalyst. The heavily shorted stocks have been a part of the meme stock craze that has recently hit Wall Street. Allbirds cut its financial forecast for the year, citing a slowdown in consumer spending. The sustainable shoemaker said it was slowing hiring as part of its efforts to cut costs. For the second quarter ended June 30, Allbirds said its revenue rose 15% from a year ago. The U.S. Treasury’s blacklisting of Tornado Cash on Monday will do more than take down criminals. Many ordinary crypto investors are likely to be hurt, experts say. Treasury yields ticked higher in early Tuesday trading, with the 2-year at 3.22%, the 5-year at 2.94%, the 10-year at 2.79%, and the 30-year at 2.88%. Most surprisingly, the 12-month are currently inverted over the 2,5,10, and 30-year bonds, trading at 3.26%.

Yesterday’s early pop in the indexes met with caution, bringing in some sellers at price resistance and spending the rest of the day in a low volume sideways chop. However, no technical damage occurred, and the bulls remained in control of the relief rally despite the low volume and loss of momentum. Earnings continue to come in mixed, and the bond yields rise as the market waits in anticipation of the CPI and PPI inflation data. I would not rule out another day of choppy price action while waiting for the data. Speculation is high as meme stocks rose sharply yesterday without an apparent catalyst illustrating the high emotion around the recent run. There is a chance we are building up for a big move. Your guess in direction is as good as mine, so plan your risk carefully!

With the indexes stuck in consolidation at significant overhead resistance, the battle for the market’s future direction could be a bit choppy as we wait on the Wednesday CPI and Thursday PPI reports. Of course, we will also have to deal with another busy week of earnings reports keeping market emotion high. In light of the hot jobs numbers, the talking head narrative that inflation topped last month is now in question, so plan for another hectic week as the data rolls out. It would not be unreasonable to expect some wide-ranging choppy price action as we hurry up and wait.

As we slept, Asian markets trading in a muted, choppy session with Hong Kong tech stocks slid lower with Chinese expanded military drills around Taiwan. However, European markets trade modestly green across the board this morning. With a busy earnings calendar, U.S. futures have recovered from overnight losses pointing to a bullish open as the battle continues at resistance for the future direction of the market with inflation data waiting in the wings.

Economic Calendar

Earnings Calendar

We kick off a new trading week with more than 200 companies listed, but many of them are unconfirmed. Notable reports include DDD, ACAD, BIRD, AIG, GOLD, BNTX, BLNK, CBT, CARG, APPS, D, ELAN, ENR, FRPT, GBT, GDRX, GRPN, IFF, LMND, VAC, NWSA, NE, NVAX, OKE, PLTR, PUBM, QLYS, RDRW, SDC, SWCH, TTWO, SKT, TSN, UPST, & VRM.

News & Technicals’

SoftBank posted one of its biggest losses at its Vision Fund investment unit for its fiscal first quarter, as technology stocks continue to get hammered amid rising interest rates. As a result, the Japanese giant’s Vision Fund posted a 2.93 trillion Japanese yen ($21.68 billion) loss for the June quarter. This is the second-largest quarterly loss for the Vision Fund. According to a court document, Celsius has withdrawn its motion to bring back ex-CFO Rod Bolger at $92,000 a month, prorated over a period of at least six weeks. The notice of withdrawal came just ahead of a hearing scheduled for Aug. 8 to review it. The decision to dismiss the motion came three days after CNBC first reported on the request to enlist the help of Bolger as a consultant during the bankruptcy process. China’s Eastern Theatre Command said it would conduct joint drills focusing on anti-submarine and sea assault operations — confirming the fears of some security analysts and diplomats that Beijing would continue to maintain pressure on Taiwan’s defenses. Pelosi’s visit to Taiwan last week infuriated China, which regards the self-ruled island as its own, and responded with test launches of ballistic missiles over Taipei for the first time and ditched some lines of dialogue with Washington. The duration and location of the latest drills are unknown, but Taiwan has already eased flight restrictions near the six earlier Chinese exercise areas surrounding the island. Fed Governor Michelle Bowman said she supports the central bank’s recent 0.75 percentage point rate increases and believes they should continue until inflation is subdued. “I think similarly sized increases should be on the table until we see inflation declining in a consistent, meaningful, and lasting way,” she added in a Saturday speech. Markets anticipate a third big increase when the central bank meets again in September. Treasury yields declined slightly in early Monday trading, with the 2-year at 3.21%, the 5-year at 2.93%, the 10-year at 2.80%, and the 30-year at 3.03%.

As we begin a new trading week, the indexes remain in consolidation at significant as the bulls and bears battle for the future direction of the market. We have another big week of earnings to keep the price action volatile, but all eyes will likely be on the CPI and PPI later in the week. In addition, last Friday’s hot jobs number raised questions about the overall inflation narrative having topped. The Senate passage of another massive spending bill that levies taxes on companies and shareholders may have some adverse side effects in the fight against inflation. Only time will tell but expect some positive and negative reactions in targeted market sectors. With a two-day wait for the CPI report, it would not be surprising to see some wide-ranging chop due to the uncertainty. Plan carefully and avoid overtrading as we wait.

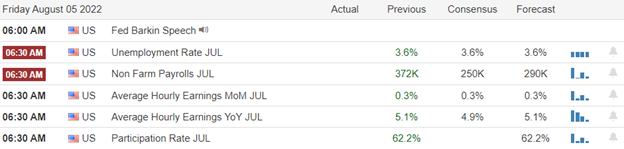

With jobless claims rising, Thursday was a choppy session as we waited for the Employment Situation report before today’s bell. Predictions range from solid job growth to a rather sharp decline over the last month, 372,000. With fewer market-moving earnings reports and the indexes tucked snugly against overhead resistance, today could be the bulls or bears decide breakthrough or pullback from this critical area. As we slide into the weekend, keep in mind that next week get to find out if inflation has topped with CPI and PPI reports.

Asian closed the Friday session green across the board as Taiwan stocks shook off the intimidation of China’s military drills off their coast. However, European markets trade slightly bearish this morning, waiting on U.S. jobs numbers. With the pending Employment Situation report and a much lighter day on the earnings calendar, futures trade mixed, but anything is possible by the open. Will the overhead resistance break or hold? We will soon find out!

Economic Calendar

Earnings Calendar

We get to take a breath and slow the pace of reports today with about 100 companies listed and quite a few not confirmed. Notable reports include AAWW, BEP, CGC, DKNG, GOG, GT, WDC, & WOW.

News and Technicals’

China sanctions Pelosi over her trip to Taiwan, calling it an egregious provocation. In addition, political analysts have warned that Pelosi’s decision to visit Taiwan could undermine U.S.-China relations. At the 2022 Tesla shareholder’s meeting, CEO Elon Musk touched on various topics, including macroeconomics and the possibility of share buybacks. He also said Tesla aims to produce 20 million vehicles annually by 2030 and thinks this will take approximately a dozen factories, each producing 1.5 million to 2 million units annually. Musk said that the Cybertruck is still slated for next year but won’t have the same specifications and pricing that were originally given when the company unveiled the experimental pickup in 2019. AMC on Thursday said it plans to issue a dividend to all common shareholders in the form of preferred shares. The company has applied to list these preferred equity units on the New York Stock Exchange under the symbol “APE.” The company said that the new class of shares carries the same voting rights as the existing common shares. Oil prices have fallen sharply from their recent peaks, but there’s still a case for buying oil stocks, according to Bill Smead, chief investment officer at Smead Capital Management. That’s because energy prices are likely to stay high or even increase further, he told CNBC’s “Street Signs Asia” on Thursday. A reopening of China’s economy would lead to a spike in demand for energy, and supply remains tight, Smead said. India’s central bank raised key rate by 50 bps to 5.40%, with inflation above 7% and over the RBI tolerance level in Q2 and Q3, and economists see more hikes in the coming months. Treasury yields ticked slightly higher in early Friday trading Witht eh 2-year at 3.06%, the 5-year at 2.80% the 10-year at 2.70% and the 30-year at 2.97%.

The pending Employment Situation report made for an uncertain choppy Thursday session, with index prices holding against overhead resistance levels. As a result, anything is possible through the open of Friday trading. The Econoday consensus suggests a decline, but an early CNBC report said the number could be strong this month and weakening in the future. Needless to say, all the predictions are meaningless its how the market reacts to the data that matters! Plan your risk carefully as we slide into the week with CPI and PPI inflation data coming next week.