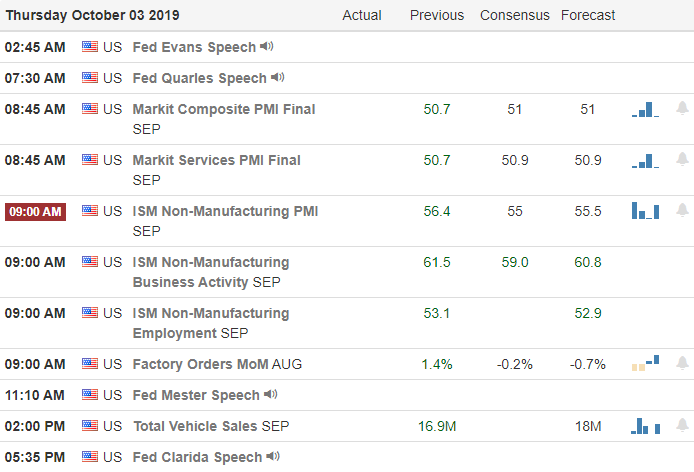

After a punishing selloff, the market will face an expected

decline in Factory Orders and the ISM Services Sector report this morning the worry

that the global slowdown has expanded into the US economy. Following a win where the WTO agreed with the

Whitehouse, the President has scheduled 7.5 billion in European new tariffs on

OCT. 18th, opening a new front on the trade war and raising concerns

of recession.

Asian markets closed mixed but mostly lower on the ramp-up of trade tensions in Europe. Across the pond, European markets also trade mixed as concerns about how the new tariffs will affect there already weakening economy. Currently, US Futures point to a modestly bullish open ahead of economic reports. Remember we have the Employment Situation report before the open Friday, so plan your risk carefully and don’t be surprised if the price action becomes stale and choppy as we wait.

On the Calendar

On the Thursday Earnings Calendar, we have 12 companies reporting

results. Notable reports include STZ,

COST, and ISCA.

Action Plan

Following an ugly 2-day selloff after a disappointing ISM Manufacturing

report, we will get a reading on the service sector with the ISM Non-Mfg report

at 10:00 AM eastern along with Factory Orders.

The consensus is expecting only a small decline in the services number and

an expectation that orders will slip negative that could raise fears of a spreading

global slow down. After the World Trade

Organization ruled that European government subsidies on aircraft is an unfair

trade practice; they cleared the way for the US to impose new tariffs. The President has scheduled 7.5 billion in tariffs

to increase on OCT 18th widening the trade tensions and raising

concerns of a US recession.

Technically speaking T2122 suggests a short-term oversold

condition, but it will be interesting how the market responds to the opening of

another trade war front in Europe. After

two strong days of selling the Dow continues to hover above its 200-day average

as does the QQQ and SPY. Unfortunately,

any market relief rally must come under scrutiny as a possible lower high that may

confirm the beginning of a market downtrend.

Of course, with the Employment Situation number on Friday, 4th

quarter earnings just around the corner, and trade talks with China to resume

soon traders will have to prepare for just about anything.

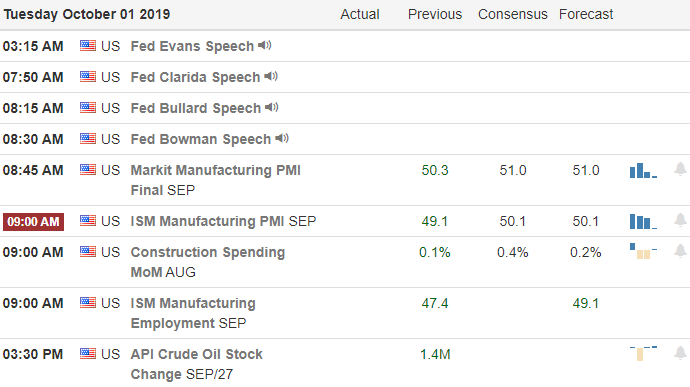

An unexpectedly poor manufacturing number quickly reversed early

bullishness yesterday creating a nasty whipsaw and leaving behind some worrisome

price patterns. The major indexes all

dipped below their 50-day averages by the close as they each left behind

bearish engulfing patterns in the process.

Most troubling was the notable reversals in the financial, transport,

and technical sectors. Technical

failures in an already uncertain market will likely spark some fear in the

market so prepare for higher volatility in the days ahead.

Overnight Asian markets closed in the red across the board in

reaction to global slowdown fears. Market

in Europe is also looking lower this morning as they wait for the Prime Minister

to unveil a revised Brexit proposal for the UK.

US Futures have bounced off of overnight lows but still point to substantial

gap down this morning and a possible short-term oversold condition according to

the T2122 indicator. Expect price action

to be volatile, news sensitive and, challenging even for very experienced

traders.

On the Calendar

On the Wednesday Earnings Calendar, we just 12 companies fessing

up to quarterly results. Among the

notable reports, today are BBBY, LEN, AYI, LW, and PAYX.

Action Plan

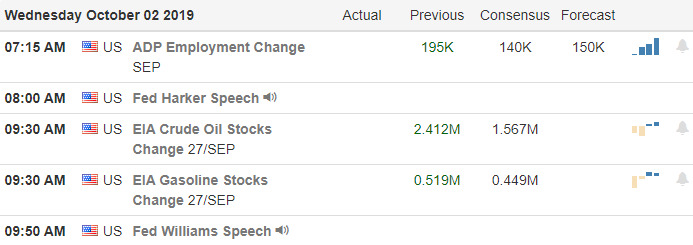

On the day after JNJ pays a large fine to settle their roll

in the opioid crisis, traders might be

looking for something to relieve the pain of yesterday’s selloff and the

substantial gap down setting up this morning.

By the close on Tuesday all the major indexes slipped below their 50-day

moving averages leaving behind some worrisome technical damage in the

charts. A surprisingly disappointing

manufacturing number created an ugly whipsaw that left bearish engulfing

candles all over the place yesterday.

Notable reversals in the financial sector and transports and

the technical damage in the tech sector are particularly troubling. At the time of writing this report, US Futures

have bounced off of their overnight lows but still suggest a gap down of

nearly 150 Dow points at the open. According to the T2122 indicator this will

create a short-term oversold condition so be careful not to chase bearish

positions already well into their move lower.

Remember this is a very emotional news-driven market, so plan your risk

carefully and be willing to take profits quickly as they can be very fleeting in

this environment.

As this frustrating range-bound consolidation continues, we can thank our friends down under for the possibility of the second day of bullishness as Australia cuts interest rates to just 75 basis points. Of course, we can’t rule out the possibility of a pop and drop pattern by the end of the day, but at least for now the bulls seem inspired to follow-through on yesterday’s rally. With the uncertainty of 4th quarter earnings and China trade negotiations scheduled in the new 2-weeks, I wouldn’t be all surprised to see the price action remain choppy and range-bound.

Overnight Asian markets recovered from early bearishness to

close mostly higher in reaction to the Australian rate cut. European markets are not sharing in the bullishness

currently flat to mostly lower this morning.

US Futures point to a modestly bullish open ahead of PMI, ISM, Construction

spending reports as well as a parade of Fed speakers. It would seem October will continue to face

considerable uncertainty and likely to remain news-driven with enough daily gaps

and overnight reversals to keep traders guessing, What comes next?

On the Calendar

The Tuesday Earnings Calendar says we will hear from just seven

companies reporting results. Notable

reports include MKC and SFIX.

Action Plan

We can thank Australia for slashing its interest rates to a

new record low of just 75 basis points inspiring the possibility of a seconded

day in a row of bullish price action.

During the night, Asian markets were struggling until the rate cut but

closed the trading day mostly higher on the news. US indexes remain locked in a choppy range-bound

consolidation that but except for the QQQ’s have successfully held their 50-day

morning averages. On the whole, I would

have to count that a win for the bulls considering all the swirling uncertainty

the market faces.

With 4th Quarter earnings just 2-weeks away, it’s

sadly possible; the market could continue in this choppy and challenging consolidation. With Washington politics in utter chaos and

pending China Trade negotiations set to begin in a couple of weeks, we should

expect October to remain a challenging news-driven market with enough gaps and

overnight reversals to test the discipline of even the most experienced

traders.

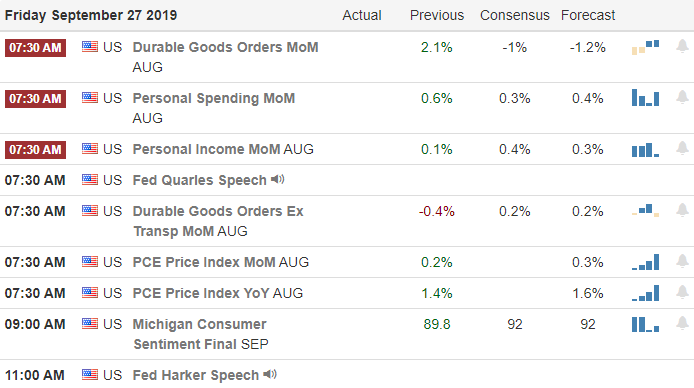

Yesterday’s whistle-blower hearing brought the buyers to a

screeching halt producing another pop and drop pattern. After the hearing, the bulls made a lackluster

attempt to rally that was frustratingly choppy as the partisan rhetoric rose to

a deafening roar of uncertainty. Traders

will have to weigh the risk of the weekend carefully considering that anything

is possible by Monday’s open.

During the night Asia markets closed mixed but mostly lower with

trade talks set to resume on Oct. 10th. The markets in Europe are green across the board

as trade hopes outweigh the US political turmoil. US Futures point to a modestly bullish open

ahead of the Durable Good & Personal Income economic reports. Expect more indecisiveness as we head into

the weekend.

On the Calendar

We have just 14 companies expected to report earnings on the

Friday calendar. Among those reporting,

I’m not seeing any particularly notable reports today.

Action Plan

The frustratingly choppy price action continued yesterday after

once again gaping up then finding more sellers than buyers during the whistleblower

hearing in Congress. The nonstop barrage

of partisan spin is hard to ignore, but it’s imperative that we stay focused on

price action to navigate this very difficult market.

After the close yesterday, we learned that US/China trade

negotiations would resume on Oct. 10th, only 5-day before the

tariffs are scheduled to increase. Let’s

hope the talk fast and that the President is correct when he said a deal is

closer than most think. We have a light

day on the earnings calendar but keep an eye on the Durable Good Orders as well

as Personal Income reports at 8:30 AM Eastern.

With so much uncertainty as we head into the weekend plan your risk carefully. Literally, anything is possible come Monday’s

open!

The mere mention by the President that a deal with China may be closer than everyone thinks and the market rallied shaking of the impeachment drama. More importantly, the SPY bounced off its 50-day average, and the QQQ recovered this key technical support with ease. As bullish as yesterday’s move appears, we must remember that one day does not make a trend and that we still have significant price resistance above for the bulls to overcome.

Overnight Asian markets closed mixed but mostly higher on renewed trade hopes, and European see green across the board in response the Presidents comments on a trade deal. US Futures are pushing for a critical follow-through of yesterday’s rally pointing to a modestly bullish as I write this post. With several notable earnings reports ahead as well as a busy morning on the economic calendar anything is possible. Plan carefully and stay focused on the price action for clues as we approach price resistance levels.

On the Calendar

On the Thursday Earnings Calendar we have 21 companies reporting

results. Notable reports include CAN,

CCL, CAG, FDS, MU, and MTN.

Action Plan

The market shook off the impeachment inquiry yesterday after

the President mentioned a deal with China might come sooner than everyone

expects. Technically speaking yesterday’s

rally was a substantial win for the bulls with the SPY bouncing off its 50-day

average and the QQQ easily recovery this key psychological level. Now it’s important that we see some followthrough

bullishness or yesterday’s move looks more like a dead cat bounce within an

existing downtrend.

A one day rally does not make a trend, but I must admit it

does raise hopefulness of better days ahead assuming it can hold. Another thing the market could be betting on is

that the impeachment process will bring Congress to a halt. A gridlocked government is often seen as

bullish by the market. The impeachment

of President Clinton kept the Congress busy for about 18 months, and during

that time the market experienced a substantial rally. Will history repeat? Only time will tell so turn off the distracting

political drama news and stay focused on the price action of the charts.

As it turns out my caution of getting caught up and chasing

yesterday gap open proved to be correct, producing a pop and drop pattern at

price resistance levels. The President’s

tough talk on China trade practices at the UN only emboldened the bears pushing

indexes lower with the QQQ suffering the worst of the technical damage unable

to hold it’s 50-day average. Adding

insult to injury Congress began yet another political drama that’s likely to affect

the market well into the future opening an impeachment inquiry of the

President.

During the night trade tensions and political uncertainty had

Asian markets seeing red across the board at the close of trading. Currently, European markets are of a like

mind and decidedly bearish across the board this morning. Not surprisingly US Futures are indicating a

lower open for the market but let’s keep an eye on the SPY & DIA key moving

average supports for a possible area of defense by the bulls. If they fail to hold as did the QQQ the technical

damage could greatly inspire the bears to continue lower. Stay focused and flexible as this news-driven

market continues to challenge traders.

On the Calendar

On the Hump Day Earnings Calendar we just 15 companies reporting

quarterly results. Notable reports

include KBH and FUL.

Action Plan

Tough talk at the United Nations from President Trump shook

the markets yesterday inspired the bulls to move the indexes quickly toward a

test of their 50-day morning averages.

The pop and drop price action left behind some pretty nasty looking

bearish engulfing candles with the QQQ experiencing the worst of the technical damage. Adding insult to injury later in the day it

was announced that Congress opened an inquiry of impeachment against the

President alleging abuse of power.

As the political drama continues to grow it only adds

another layer of what the market hates the most, uncertainty! Unfortunately, that big festering and

stinking pile of uncertainty is likely to continue making this market very

challenging for traders navigate. The

best we can do is stay focused on price, support, resistance, trend, and be

willing to take profits quickly when you have them to avoid the potential whip

of the news story.

The bulls did a good job defending yesterday’s modest gap

down open setting the stage for another possible attack of all-time highs. With several notable earnings reports today and

a reading on Consumer Confidence the bulls may find the inspiration needed breakthrough

the 3000 SPY resistance that has proven so difficult to hold.

Asian markets closed modestly green across the board as

trade uncertainty, and global growth concerns grow. A day after disappointing German economic

numbers European markets are flat to slightly bullish this morning. US Futures appear confidently bullish this morning

suggesting a nearly 100 point gap up to challenge resistance levels once

again. Consider your risk carefully and avoid

chasing gap up entries at or near price resistance levels.

On the Calendar

On the Tuesday Earnings Calendar we have 28 companies fessing

up to quarterly results. Notable

earnings include NKE, NIO, AZO, BB, KMX, CTAS, INFO, JBL and MANU.

Action Plan

Yesterday’s light and chopping price action saw the bulls working to defend the lows of the morning gap down. Index futures held positive throughout the night, suggesting a bullish open and perhaps another attempt by the bulls to attack the all-time market highs. The DIA will first have to deal with the price resistance around 271, and the SPY will have to breach the resistance at 300. The QQQ’s have a considerable amount of work to do before breaking out, but it is bullish that thus far the bulls have successfully defended its 50-day average as support.

A little concerning is that we had safe-haven plays such as Gold,

Silver, defensive sector stocks and even utilities were going up yesterday with

the overall market. Oil stocks continue to recover after the Saudi

oil field attack and yesterday saw a strong push in retail with stocks like

DLTR, TGT, and WMT rising. Currently,

futures point to a bullish open ahead of the Case-Shiller, and Consumer Confidence

reports as well as several notable earnings.

With trade talks scheduled to resume in a couple of weeks and new

tariffs increases scheduled for the 15th of October, markets will continue

to be news sensitive in the days and weeks ahead.

As we approach the end of the 3rd quarter, the index

charts are displaying technical contradictions that reflect the uncertainty faced

by the market. While holding above their

respective 50-day averages the DIA and QQQ have left behind low high failure

patterns, and the SPY is displaying a possible double top failure pattern. The technical contradiction makes for some

very difficult trading decisions in this very news-driven and emotional market.

US Futures open trading Sunday evening quite bullish but faded

as Asian markets struggled with US/China trade developments closing mostly

lower on the day. Weak German economic

data has the European indexes seeing red across the board this morning. US Futures point to a flat to open, and with

little on both the economic or earnings calendars to provide inspiration, expect

political news sensitivity and possible choppy price action.

On the Calendar

To begin the week on the Economic Calendar we have just 16 companies

reporting results but among those stepping up, I can no particularly notable reports.

Action Plan

Although Iran continues to deny the Saudi oil field attack the

President has decided to send troops into the Persian Gulf to bolster the Saudi

Arabian forces as tension continue to grow.

Friday the Chinese negotiations team abruptly cut their visit short, and

then during the night the US Justice Department warned companies that Chinese corporate

theft is rising. Attorney General Adam Hickey

reported that more cases are being open that implicate China for trade secret

theft and that 80% of the economic espionage cases since 2012 involve China.

US Futures opened last night very bullish but have sold-off

and currently indicate a flat to slightly bearish open. With little more than Fed speakers on today’s

economic calendar and no market-moving earnings report, the market will have to

find inspiration elsewhere. Technically the

DIA and QQQ are now showing lower high concerns and the SPY chart displaying an

uncomfortable double top failure forming.

On the bullish side, however, all the indexes remain above their 50-day

moving averages and continue to cling to a current uptrend. As of now the charts seem to reflect the political

uncertainties and difficult trading decisions.

While the DIA and SPY continue to hover just below around

all-time high resistance levels, yesterday’s price action left more concern

rather than confidence by the end of the day.

Technically speaking the current trends in major indexes remain bullish even

though the resistance above has proven to be difficult to penetrate thus

far. With very little on the earnings or

economic calendars today the market may struggle to find inspiration as we head

into a weekend that could include retaliation for the Saudi oil field attacks.

Asian markets closed the week mixed but mostly higher as

low-level trade talks begin. European

indexes are modestly green across the board this morning, and the US Futures currently

point to modest gains at the open. With contradictory

candle signals, trends and all-time resistance levels just above ahead of an uncertain

weekend anything is possible. Plan your

weekend risk carefully.

On the Calendar

On the Friday Earnings Calendar, we have just four companies

reporting results today. I see no particularly

notable reports today.

Action Plan

Vice President Mike Pence is now publicly calling the attack

on Saudi oil fields as an act of war.

According to reports, President Trump will be briefed on retaliation

options in the next couple days. What

comes next is anyone’s guess? The President

has also granted a few more tariff exemptions as US and China move into low-level

talks.

Although the indexes

were unable to sustain yesterdays rally the DIA and SPY continue to hover

around all-time high resistance levels. Current

trends are clearly bullish, but yesterday’s price action was not exactly confidence

inspiring by the end of the day. As we

head into a weekend with trade talks and a possible retaliatory response on the

oil fields it will be interesting to see how much risk traders will be willing

to hold. With only Fed Speakers on the

Economic Calendar and no notable earnings reports today, the market will have

to search or inspiration elsewhere. Plan

your risk carefully and have a wonderful weekend!

After cutting rates for the second time, the market seems a bit disappointed this morning the, FOMC didn’t clearly signal more rate cuts this year. With Powell pointing to strong US economic indicators and with three dissenting committee members on this cut, the path to future reductions looks challenging. During the night the BOJ held current rates, and this morning the Bank of England did the same. Unfortunately, there is still plenty of uncertainty with a possible Iran retaliation action, Brexit, US/China trade talks & scheduled tariff increases to make the weeks ahead challenging.

Asian markets closed mixed but mostly higher with Hong Kong

markets continuing to slide south as the unrest in the country continues. This morning European markets are all

modestly higher after the BOE decision to stand fast on interest rates. US Futures point to modest declines at the open

ahead of a busy morning on the economic calendar of possible market-moving

reports. Keep your seat belt fastened the

road ahead could still be very challenging to navigate.

On the Calendar

On the Thursday earnings calendar, we have just 11 companies

reporting results with DRI as one of the most notable on the day.

Action Plan

Evidence is growing from the remnants of the drones and cruise missiles used in the Saudi oil fields attack that Iran is the culprit. Saudi Arabia will present its evidence to the United Nations and framing the incident as a global community threat. The President has ordered much tougher sanctions against Iran but to this point has shown constraint for a military confrontation. A day after the FOMC decision US Futures point to a modestly lower open seemingly disappointed with the FOMC decision.

During the evening the Bank of Japan choose to hold rates

steady, and this morning Bank of England decided to stand pat on interest rates

even as Brexit uncertainty grows. With

that now out of the way the market will likely focus on the coming US/China

trade talks early next month, the issues surrounding the intensifying Brexit decision,

as well as the coming 4th quarter earnings. A possible retaliation attack on Iran remains

a wild card that could upset the applecart in the short-term.