Over-speculation created a wild ride on Tuesday, and all that emotion could explode in another round of extreme price volatility with Powell in focus. Will he deliver the hoped-for pivot comments at the press conference allowing Santa to party with a rally into the year’s end? Or will he continue the hawkish tough talk on inflation and unleash the Grinch? With so much uncertainty, plan for a choppy morning session as we wait, followed by another wild ride of volatility this afternoon that may set the market direction for the remainder of the year.

Asian markets rallied with modest gains after a relaxing read on inflation with all eyes on Powell. European markets, however, trade in the red this morning, with energy prices easing their inflation slightly. With Powell’s press conference on tap, U.S. futures have reversed some overnight bullishness to suggest a flat to slightly bearish open. However, anything is possible with market emotion high, so plan your risk carefully!

Economic Calendar

Earnings Calendar

We have a few more reports on the Wednesday earnings calendar, but the market-moving reports are falling by the wayside. Notable reports include LEN, MITK, NDSN, REVG, & TCOM.

News & Technicals’

A Bahamas judge denied FTX founder Sam Bankman-Fried bail and said he should be remanded to custody until February 2023, citing a heightened flight risk for the onetime billionaire. Bankman-Fried claimed he was down to just $100,000, a stark comedown for the former crypto titan. The Digital Commodities Consumer Protection Act is among the solutions lawmakers will consider as they probe the implosion of crypto exchange FTX and try to implement industry safeguards. The legislation would give the Commodity Futures Trading Commission more oversight. However, some crypto advocates say it doesn’t go far enough to protect certain kinds of exchanges.

The Federal Reserve is expected to raise interest rates by a half percentage point Wednesday yet signal it will continue its battle against inflation. However, economists expect Fed Chair Jerome Powell to tilt toward the hawkish side in an effort to impress on markets that the central bank is not ready to give up its rate-hiking stance. CNBC’s Jim Cramer on Tuesday outlined what needs to happen for the Federal Reserve to finally beat inflation. “Without a well-deserved crash in crypto and a sign of higher unemployment acknowledged by [Federal Reserve Chair] Jay Powell, this CPI reading has to be treated as a one-off number,” he said.

Tuesday was a wild ride of over-speculation and over-hyped emotion, with Powell in focus! Investors continue to hope for an FOMC pivot, but Powell is expected to raise rates by another 50 basis points today. However, it is not likely that the act of raising rates will cause market volatility this afternoon; the press conference will light up the eratic market emotion after that. Nevertheless, if Powell continues his tough stance on inflation and tamps down the idea of a quick pivot, it will likely disappoint the market and diminish the hope of an end-of-year Santa rally. However, if he is perceived to be ready to back off and become more dovish, the market will celebrate, and the Santa rally could party until the end of the year! Although it may be a choppy morning session, as we wait, the pent-up emotion will likely explode in wildly volatile price action this afternoon. Plan carefully amid the massive uncertainty of what comes next.

Tuesday was the definition of “Whipsaw” as traders loved the CPI data and turned what had already looked like a gap up into a massive gap higher. (The SPY gapped up 2.8%, the DIA gapped 2.14% higher, and the QQQ gapped up a whopping 3.82% at the open.) However, then the bears showed up, driving a strong and persistent selloff until 1 pm. That selloff had completely faded the opening gap in all 3 major indices (and more than faded it in the DIA). By that point, the bulls were rested and began a slow rally back in the other direction until 2 pm, when another selloff began. This volatile action gave us very large, gap-up, black candles with lower wicks in the DIA, SPY, and QQQ.

On the day, eight of the ten sectors are in the green with the Energy (+1.75%) sector leading us higher while the Communication Services (-0.13%) and Consumer Defensive (-0.11%) sectors were the laggards. Meanwhile, the SPY was up 0.76%, the DIA was up 0.35%, and the QQQ was up 1.08%. This action took place on greater than average volume. The VXX fell by 4.14% to 14.58 and T2122 remains in the mid-range at 65.67. 10-year bond yields were also volatile but now down to 3.507% and Oil (WTI) was up more than 2.8% to $75.25 per barrel. So, overall, it was an extremely volatile day that saw a range that was many times the close-to-close move.

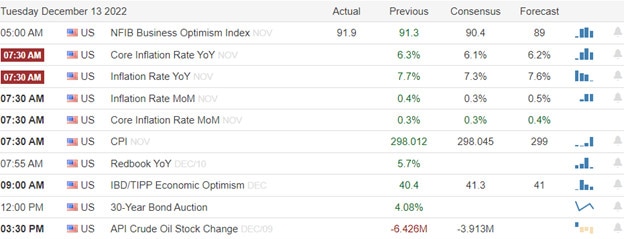

In economic news, the November CPI showed a much smaller-than-expected increase of +0.1% (compared to the forecast of +0.3% and the October reading of +0.4%). This was the smallest increase since August of 2021. It also translates into an annualized consumer inflation of 7.1% (compared to 7.3% that was forecasted and the 7.7% annual CPI was sitting at last month. As mentioned, the market loved this news since it is strong evidence that Fed moves to date have started to bring inflation down. (And traders expect this to translate into a smaller rate hike and softened tone in the Fed announcement and presser today.) Later, after the close, API reported that oil inventories unexpectedly rose by 7.8 million barrels this week (versus the forecast of a 3.9-million-barrel drawdown and last week’s 6.4-million-barrel drop). This was particularly unexpected given the midwest pipeline shutdown that is depriving a major storage hub of 662k barrels per day.

In stock news, BA reported that its plane deliveries rose in November to 48 (up from 35 in October). Meanwhile, STLA recalled 1.4 million 2019-2022 Dodge Ram pickups over faulty tailgate latches. In other auto news, F announced it is adding a third “crew” to its Dearborn F-150 Lightning electric vehicle assembly plant (increasing production capacity by 50%). In the health industry, Reuters reports the MRNA Covid-19 vaccine has been now shown to work against the melanoma type of cancer. This news drove MRNA stock massively higher, closing up 19.63% on the day. Elsewhere, RTX has announced a $6 billion stock repurchase program. Finally, the CEO of UAL told the media on Tuesday that UAL and its main competitors are preparing for a “mild” recession in 2023. He went so far as to say that “if he didn’t read the Wall Street Journal or watch CNBC the word recession would not even be in his vocabulary right now.” Along those same lines, DAL said Wednesday morning that it expects to double earnings in 2023 due to “rebounded and robust” travel demand.

In anti-trust news, according to Bloomberg, AAPL will allow alternative app stores onto iPhones by the end of 2023…but only in the EU (where it is being forced to do so by anti-monopoly law). This may end up a boon for MSFT, META, AMZN, and any other company with a major app store. Meanwhile, ILMN began pre-emptively defending its purchase of Grail, by pledging to keep selling its DNA sequencing services to other firms. This comes ahead of an FTC commissioner’s vote on the deal, which is the final US hurdle. Still, the EU antitrust regulators have already temporarily blocked the deal and are set to make a final decision in early 2023. Finally, on Tuesday, MSFT President Smith said the company has offered to agree to a legally-binding FTC Consent Decree that would force MSFT to continue providing the “Call of Duty” game franchise to rival game platforms if the FTC would allow the acquisition of ATVI to proceed. (The EU is still investigating the deal and has promised to decide whether or not they’ll allow it by March 2023.)

In miscellaneous news, part of the reason behind Tuesday’s big rally in oil was that the Dollar dropped hard against all its major pair partners. The expectation of less hawkish action and verbiage out of the FOMC would have a weakening effect on the dollar. Yet another impact of the good inflation news was a drop in mortgage rates. A 30-year fixed-rate mortgage has dropped to 6.28%, which is nearly half a percent lower than the rate at the end of November. Elsewhere, on Tuesday the Pentagon switched course and recommended that the US give Patriot Missile systems to Ukraine for air defense. (Those are made by RTX, LMT, and BA.) President Biden still needs to approve the shipments, but if it is done, it would be a major increase in capability for Ukraine to keep their country’s power grid online as repaired.

After the close, ABM reported beats on both the revenue and earnings lines. However, ABM also lowered its forward guidance. So far this morning, REVG has posted a beat on both the top and bottom lines.

Overnight, Asian markets leaned heavily to the green side. Taiwan (+1.49%), South Korea (+1.13%), and Malaysia (+0.89%) led the rally while Chinese exchanges lagged. Meanwhile, in Europe, exactly the opposite is taking shape at midday. The only green on the European board is Athens (+0.18%) and Denmark (+0.20%). At the same time, the FTSE (-0.24%), DAX (-0.51%), and CAC (-0.38%) are typical and lead the region lower in early afternoon trade. As of 7:30 am, US Futures are just on the green side of flat. The DIA implies a +0.15% open, the SPY is implying a +0.15% open, and the QQQ implies a +0.10% open at this hour. 10-year bond yields are just south of flat at 3.503% and Oil is up 1% to $76.21/barrel in early trading.

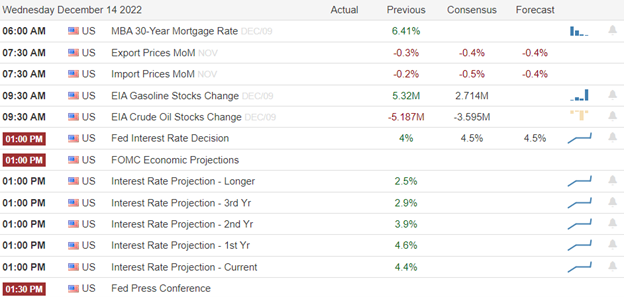

The major economic news events scheduled for Wednesday include the November Import/Export Price Index (8:30 am), EIA Crude Oil Inventories (10:30 am), Fed Q4 Interest Rate Projections, Fed Economic Projections, FOMC Statement, and the Fed Interest Rate Decision (all at 2 pm), and FOMC Press Conference (2:30 pm). (Note that Fed Futures have priced in an 80% probability of a 0.50% rate hike today.) The major earnings reports scheduled for before the open are limited to REVG. Then after the close, LEN, NDSN, and TCOM report.

In economic news later this week, on Thursday, we get November Retail Sales, Weekly Initial Jobless Claims, NY Fed Empire State Mfg. Index, Philly fed Mfg. Index, Nov. Industrial Production, Oct. Business Inventories, and Oct. Retail Inventories are reported. Finally, on Friday, Mfg. PMI and Services PMI are reported.

In earnings later this week, on Thursday we get reports from JBL and ADBE. Finally, on Friday, we hear from CAN, DRI, and WGO.

As all eyes look toward the Fed today, Bloomberg implies that somebody knew something early about CPI data which led to yesterday’s strong rally. Bloomberg says that there were massive bullish bets made in the minute prior to the release of CPI information. This magnified the premarket action and led to the huge gap-ups at the open. Only time will tell whether this will be investigated and whether the SEC could prove any inside info was acted upon.

With that background, the short-term trend is bullish after yesterday’s rollercoaster ride. Premarket prices are now essentially flat and there is no problem with over-extension, either in terms of the T-line (8ema) or the T2122 indicator. So, both the bulls and the bears have room to run once the FOMC gives its current verdict. Be ready for more whiplash as we are getting economic and interest rate projections in addition to the Fed release (and that statement’s verbiage will be parsed nine ways to Sunday). Then, a half hour later, Powell speaks AND answers questions. So, there will be something (probably several things) for both camps the latch onto today. And that is how you get the violent jerks back and forth as “average sentiment” gets worked out over an hour or two. (Also, beware that it is quite possible we then have another reassessment overnight and yet another market reaction to the news on Thursday morning.)

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

Swing Trade Ideas for your consideration and watchlist: XLE, FNGU, GSK, HAL, APA, NEM, GEO, FIVN, ARDX, and AMAT You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

My expectation of a hurry-up and wait day turned into a big surprise as the market surged higher in the last hour of trading, with investors chasing risk with market-moving data the rest of the week. Oddly, at the same time, the fear spiked as the VIX spiked to 25 handles, with the SPY and QQQ suffering from anemic volume. Clearly, the appetite for speculative risk is alive and well despite the FOMC’s efforts to bring valuations down. I’m not confident that’s a good thing with a world recession on the horizon. Expect big price moves with morning gaps and possible intraday whipsaws with all the data coming our way the rest of the week.

Asian markets traded with mixed results as China relieves pandemic travel restrictions. European moved higher this morning with all eyes on U.S. inflation data. U.S. futures so tremendous confidence in the pending CPI number and the coming FOMC decision extending Monday’s buying surge, suggesting a gap up ahead of the data. Plan for considerable price volatility as the market reacts.

Economic Calendar

Earnings Calendar

Notable reports for Tuesday include ABM, CNM, & PLAB.

News & Technicals’

Following his arrest in the Bahamas on Monday, FTX founder Sam Bankman-Fried faces the potential of a lengthy prison sentence. FTX collapsed last month following a liquidity crunch at the crypto exchange. “It is inconceivable to me that the Justice Department would have charged this case unless they were confident they could extradite him,” Renato Mariotti, a former federal prosecutor, told CNBC. In addition, FTX CEO John J. Ray III plans to tell the House Financial Services Committee on Tuesday that the cryptocurrency exchange under Sam Bankman-Fried had “unacceptable management practices.” Ray said in his remarks that FTX went on a “spending binge” from late 2021 through 2022 when approximately ”$5 billion was spent buying a myriad of businesses and investments, many of which may be worth only a fraction of what was paid for them.” He also said, “loans and other payments were made to insiders in excess of $1 billion.”

Binance, the world’s largest cryptocurrency exchange, said Tuesday it is pausing withdrawals of the stablecoin USDC while it carries out a “token swap.” Changpeng Zhao, CEO of Binance, tweeted on Tuesday that the exchange is seeing an increase in withdrawals of USDC. The move comes as investor concerns grow about Binance’s stability following the collapse of rival exchange FTX as well as a report of a potential criminal investigation from the U.S. government.

Without question, Monday was a big surprise for me as the bulls raced forward, heading into the very uncertain data points of the CPI and the FOMC rate decision. The bullishness was again focused on the Dow while the SPY and QQQ continued to suffer from anemic volume. As the indexes surged the last hour of the day, the VIX simultaneously spiked to 25 handles suggesting fear expanded during the rush to buy. An extraordinary occurrence, indeed, that one might infer only increased the danger as we wait for the market moving reports. One thing that seems evident after yesterday’s surge is that wild speculation still exists despite the Fed’s efforts to tamp it down. I’m not sure that’s a good thing facing a worldwide recession in 2023. Fasten your seat belts tightly for the next few days are likely to include significant opening gaps and big point whipsaws, so plan your risk carefully!

On Monday, stocks gapped slightly higher at the open (less than a quarter of a percent in the large-cap indices and essentially none in the QQQ). From that point, the bulls stepped in to lead a very slow and steady rally that lasted right into the close. (The QQQ rally really kicked into high gear at 2:30 pm, while the other indices saw the rally speed up just before 3 pm.) This action gave us white-bodied candles that remained inside the range for the last few days. It also should be noted that the SPY, DIA, and QQQ all crossed back above their T-line (8ema) from below. All-in-all, it seems like Monday was a modest melt-up that finally kicked into gear late as traders wait on the CPI tomorrow and the FOMC announcements Wednesday.

On the day, all ten sectors ended in the green with Energy (+2.08%) leading us higher and the Basic Materials (+0.30%) and Consumer Cyclical (+0.46%) sectors being the laggards. Meanwhile, the SPY was up 1.43%, the DIA was up 1.57%, and the QQQ was up 1.26%. All of this action took place on less than average volume (although the DIA did manage to climb above average volume). The VXX fell by 0.59% to 15.21 and T2122 climbed back outside of the oversold territory at 53.75. 10-year bond yields were up to 3.615% and Oil (WTI) was up more than 3.5% to $73.52 per barrel.

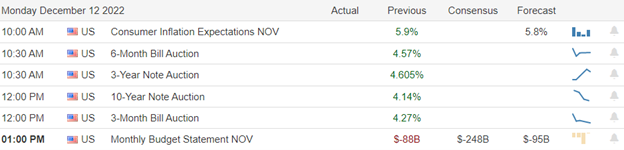

In economic news, it was interesting to see that both 3-year notes and 10-year notes were auctioned off by the Treasury Dept. on Monday. Both of these came in more than half a percent lower than the previous auction. Later in the afternoon, the November Federal Budget Balance came in $1 billion worse than expected at -$249.0 billion (as compared to the forecast of -$248.0 billion). Elsewhere, the US Senate is aiming to pass another stop-gap spending bill to keep the government open. A vote is expected Friday and will keep the government open for another week while details of a longer-term $1.5 trillion omnibus spending bill are hammered out (although the 2 parties agreed to generalities last weekend).

In stock news, the US Energy Dept. announced Monday that they have finalized a $2.5 billion low-cost loan for the lithium battery joint venture formed by GM and South Korean LG Energy Solutions. The loan will be used to finance manufacturing facilities in OH, TN, and MI. Elsewhere, in the afternoon, Bloomberg reported that GS is planning to cut at least 400 hundred more jobs as it restructures its retail consumer business. In other GS news, the company will stop making unsecured consumer loans according to a report from Reuters. In legal news, the US Supreme Court has ruled that the state of CA can ban flavored tobacco products in a case brought by BTI (which now owns RJ Reynolds).

In BA news, on Monday, Indian airline India Air announced a historically large new order for jet planes. Specifics were not shared other than it includes up to 500 jets delivered over the next decade from both BA and Airbus. Then early this morning, UAL and BA announced that the airline has placed orders to buy 100 of the BA 787 Dreamliner jets with deliveries scheduled between 2024 and 2032. (These planes will replace 100 existing BA 767s that United operates.)

In energy news, as of late Monday, TRP has yet to determine the cause of the 14,000+ barrel crude oil leak (from the Keystone pipeline) in KS. The pipeline normally delivers 622,000 barrels per day and has been down since Wednesday with no timetable for the resumption of operations. Oil trades indicate this was a driver behind Monday’s WTI rally and said if the outage lasts until the coming weekend, that could push the Cushing OK storage hub below the minimum required operating volume as well as crippling gulf region refineries.

After the close, ORCL beat on both the revenue and earnings lines. However, JOAN missed on both the top and bottom lines. ORCL also lowered its forward guidance.

Overnight, Asian markets were mixed on generally modest moves. Singapore (+0.98% was an outlier to the upside as Hong Kong (+0.68%) and India (+0.60%) led to the upside while Shenzhen (-0.66%) and Taiwan (-0.61%) led to the downside. In Europe, the exchanges are generally green at midday. The FTSE (+0.39%), DAX (+0.82%), and CAC (+0.67%) lead the region higher while only Russia (-0.64%) and Portugal (-0.07%) are in the read in early afternoon trade. Meanwhile, as of 7:30 am, US Futures are pointing toward a half percent gap higher to start the day. The DIA implies a +0.56% open, the SPY is implying a +0.48% open, and the QQQ implies a +0.46% open at this hour. 10-year bond yields are down again to 3.587% and Oil (WTI) is up a quarter of a percent to $73.37/barrel in early trading.

The major economic news events scheduled for Tuesday is limited to November CPI (8:30 am) and API Weekly Crude Oil Stocks (4:30 pm). The major earnings reports scheduled for before the open are limited to CNM. Then after the close, ABM reports.

In economic news later this week, on Wednesday, November Import/Export Price Index, EIA Crude Oil Inventories, Fed Q4 Interest Rate Projections, Fed Economic Projections, FOMC Statement, Fed Interest Rate Decision, and FOMC Press Conference are reported. On Thursday, we get November Retail Sales, Weekly Initial Jobless Claims, NY Fed Empire State Mfg. Index, Philly fed Mfg. Index, Nov. Industrial Production, Oct. Business Inventories, and Oct. Retail Inventories are reported. Finally, on Friday, Mfg. PMI and Services PMI are reported.

In earnings later this week, on Wednesday we get reports from REVG, LEN, NDSN, and TCOM. On Thursday we get reports from JBL and ADBE. Finally, on Friday, we hear from CAN, DRI, and WGO.

Equity markets are looking for good CPI news this morning and especially looking for a softer tone and only 0.50% rate increase by the Fed on Wednesday. We may see a melt-up in anticipation with a general “wait to see” attitude by the big money. Meanwhile, the crypto world continues to reel as early today the SEC said that the head of the FTX exchange (Sam Bankman-Fried) defrauded investors to the tune of $1.8 billion and in the aftermath of the FTX collapse the Binance exchange (the world’s largest crypto exchange) halted outflows of the USDC stablecoin this morning. Bianance said the halt was temporary while it carries out a “token swap” (which just means swapping one digital currency for another electronically)…which on its own could cause more fear in the crypto world.

With that background, the short-term bearish downtrend line has now been broken in all three major indices and it looks like the bulls are looking to move even higher(at least in premarket trade). However, the big Nov. CPI report will have a lot to say about the open as well. Over-extension is still not a problem at all either in terms of the T-line (8ema) or the T2122 indicator. So, the bulls have room to run if traders want to move the market. Just bear in mind that the market risk is to the downside where a disappointing CPI (in this case too high) could crush the bull’s hopes and turn the bears loose.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

Swing Trade Ideas for your consideration and watchlist: NVDA, GSK, FDX, QCOM, SWKS, LEVI, and T. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Though the premarket pump will try to engage, the fear of missing out today will likely become the classic hurry-up and wait with CPI and FOMC events ahead. Friday’s close adds to the uncertainty, with indexes hovering just above critical price support levels. Will the coming data inspire the hoped-for Santa Clause rally, or will Powell be the Grinch that stole Christmas? While today may prove to be a chop fest, as we wait, anything is possible in the days ahead. Expect some sudden and substantial price reactions as Christmas hope battles recession worries.

Asian markets started the week lower, led by selling in Hong Kong down 2.20% as investors wait on U.S. data. European markets also traded primarily lower this morning on the uncertainty of the inflation and rate decisions ahead. However, in the U.S., premarket futures try to put on a brave face with modest bullishness with index prices posied near essential support levels. Plan for a choppy, light day as we wait.

Economic Calendar

Earnings Calendar

Although we have a few notables, it will be a very light week on the earnings calendar. Notables for Monday include COUP & ORCL.

News & Technicals”

Rivian said Monday it was pausing plans to manufacture commercial electric vans in Europe and would “no longer pursue” the agreement it made with Mercedes-Benz. However, the U.S.-based electric vehicle manufacturer said it remains open to exploring future work with Mercedes-Benz “at a more appropriate time.” Mercedes-Benz said Rivian’s decision would not impact the timeline of its electrification strategy or the planned ramp-up of its new electric vehicle manufacturing site in Jawor, Poland.

Inflation has already peaked, but it will remain above pre-Covid levels in 2023, said David Mann, chief economist for Asia-Pacific, Middle East, and Africa at the Mastercard Economics Institute. “Inflation has seen its peak this year, but it will still be above what we had been used to pre-pandemic next year,” Mann told CNBC’s “Squawk Box Asia” on Friday. He said it’ll take a few years to return to 2019 levels.

Before founding Crypto.com, Kris Marszalek was involved in multiple ventures that collapsed, including one where suppliers claimed they could not access their earnings. Over a decade ago, their manufacturing company paid Marszalek and his business partner millions of dollars months before it entered bankruptcy. In a tweet thread published ahead of this story, Marszalek wrote, “startups are hard” and “you will fail over and over again.”

Although we see a little premarket bullish blustering today is likely to be nothing more than a classic hurry-up and wait for the Tuesday CPI and the Wednesday FOMC. I would expect some early price gyrations that will devolve into an understandable choppy price day with the uncertainty ahead. Technically speaking, there is a lot at stake as the major indexes, with the indexes closing very near critical support levels last Friday. If the CPI and FOMC decision inspires the bulls, we could see a Santa rally begin. However, if the reports inspire the bears and support levels break under the pressure, Powell may be seen as the Grinch that stole Christmas. Anything is possible, so position yourself carefully, avoiding overtrading your bias because the price moves are likely to be sudden and substantial in reaction to the coming data.

Markets gapped down very modestly on Friday. They then spent most of the day in waves and “dead flat” periods grinding sideways that lasted until 3:15 pm. At that point, all three major indices sold off hard in the last 45 minutes of the day, closing very near the lows. This left all of them as some form of a black-bodied inverted hammer candle. All three also failed a retest of their T-line (8ema). The QQQ also closed right at its major support level. So, overall, it was a blah day, punctuated by profit-taking or a bearish selling spree during the last hour.

On the day, all ten sectors ended in the red with Energy (-1.76%) leading us lower and the Financial Services (-0.22%) and Utilities (-0.23%) sectors holding up the best. In the meantime, the SPY was down 0.75%, the DIA was down 0.91%, and the QQQ was down 0.64%. All of this action took place on less than average volume. However, it was close to average than the last few days. The VXX climbed by 2.14% to 15.30 and T2122 fell back just inside of the oversold territory at 19.67. 10-year bond yields were up sharply to 3.586% and Oil (WTI) was flat at $71.59 per barrel.

In economic news, the market was disappointed by November PPI (Wholesale-level inflation) which came in at +0.3% (versus the forecasted +0.2% and the October value of +0.3%). So, traders had expected more evidence that inflation was starting to come down (in order to give the Fed cover to do a smaller rate hike this week) and were then disappointed. As a result, premarket action went from implying a modest gap higher to actually delivering a modest gap lower at the open. Later in the morning, Michigan Consumer Sentiment came in higher than expected at 59.1 (compared to the forecast of 56.9 and the previous value of 56.8).

In stock news, Reuters (which obtained an internal memo) reported Friday that TSLA is suspending production of its “Model Y” in China from at least Dec. 25 through year-end. It’s unclear if “Model 3” production will also be halted. The unplanned shutdown is a response to upticks in covid labor losses (related to the recent relaxation of zero-covid policies in Shanghai as well as parts supply (reduced for the same reason). In other auto news, STLA announced Friday that in February it will indefinitely shut down a Jeep Cherokee production plant in IL (1,350 employees). The UAW told Reuters that internal company documents show the company is moving Cherokee production to its Mexican plant. Elsewhere, ERIC and AAPL have reached a global patent license deal which ended a legal fight over royalty payments for 5G technology used in iPhones. Meanwhile, on Monday, MSFT announced a 10-year cloud services deal with the London Stock Exchange, part of which was MSFT acquiring a 4% stake in the exchange. Finally, it was announced today that AMGN has agreed to buy HZNP for $26.4 billion (or $116.50/share cash, a 20% premium on Friday’s closing price).

In index news, the QQQ (Nasdaq 100) will rebalance as of the opening bell on Dec. 19. Changes include the addition of RIVN, WBD, CSGP, GFS, BKR, and FANG. The tickers being removed are VRSN, SWKS, SPLK, BIDU, MTCH, DOCU, and NTES. So, the index will remain tech-heavy, even as it diversifies, and will be reduced from 102 to 101 tickers. Many exchange-traded funds and actively managed mutual and hedge funds are bound by rules stating they must own all of the “current members” of that index.

In miscellaneous news, on Friday the WTO ruled that steel and aluminum import tariffs levied by the US (former President Trump) violate global trade rules. However, in a nod to US steelmakers and unions, President Biden has appealed the ruling to the WTO Appeals Court. This makes the ruling null because the Appeals Court is shut down since the US has been blocking the appointment of WTO “judges”. (US Aluminum and Steel firms: ARNC, SCTM, KALU, AA, CLF, CRS, CMC, NUE, STLD, X) Elsewhere, over the weekend, the Keystone oil pipeline leak in Kansas is the largest spill in the US for more than a decade. As of Sunday, TRP (the pipeline operator) said they have not found the cause of the 14,000+ barrel spill and have no plans on restarting operations with various investigations ongoing. Finally, on Sunday, the NASA Orion capsule splashed down after completing its 25-day mission to and week of orbiting the moon. Hours before it did so, a SpaceX rocket took off carrying a lunar lander made by the Japanese company iSpace. If they land successfully, it would be the first company (non-governmental entity) to reach the moon. (To date, only the US, Russia, and China have been able to successfully land missions on the moon.)

Overnight, Asian markets were almost exclusively red on generally modest moves. Thailand (+0.16%) was the only green while Hong Kong (-2.20%) was the only move greater than 0.90% in the region. In Europe, a similar story is taking shape at midday. The FTSE (-0.19%), DAX (-0.29%), and CAC (-0.38%) lead the region and are typical with only the FTSE MIB (+0.05%) in the green in early afternoon trade. As of 7:30 am, US Futures are pointing toward a modest gap higher to start the day. The DIA implies a +0.19% open, the SPY is implying a +0.28% open, and the QQQ implies a +0.32% open at this hour. Meanwhile, 10-year bond yields are falling to 3.536% and Oil (WTI) is off 0.69% to $70.53/barrel in early trading.

The major economic news events scheduled for Monday are limited to the November Federal Budget Balance (2 pm). There are no major earnings reports scheduled for before the open. Then after the close, JOAN, report.

In economic news later this week, on Tuesday we get November CPI and API Weekly Crude Oil Stocks. Then Wednesday, November Import/Export Price Index, EIA Crude Oil Inventories, Fed Q4 Interest Rate Projections, Fed Economic Projections, FOMC Statement, Fed Interest Rate Decision, and FOMC Press Conference are reported. On Thursday, we get November Retail Sales, Weekly Initial Jobless Claims, NY Fed Empire State Mfg. Index, Philly fed Mfg. Index, Nov. Industrial Production, Oct. Business Inventories, and Oct. Retail Inventories are reported. Finally, on Friday, Mfg. PMI and Services PMI are reported.

In earnings later this week, on Tuesday, we hear from CNM and ABM. Then Wed. we get reports from REVG, LEN, NDSN, and TCOM. On Thursday we get reports from JBL and ADBE. Finally, on Friday, we hear from CAN, DRI, and WGO.

All eyes (globally as well as in the US) seem to be looking toward the Fed. As of this moment, Fed Futures are showing that a 75% probability of a 0.50% rate hike and less than a 25% probability of a 0.75% rate hike has been priced into the market. The CPI data on Tuesday may give us a clue, but suffice it to say the market is expecting a slowing of the increases and no matter what the Fed does, it will have plenty of critics.

With that background, the short-term trend remains bearish. However, it looks like all three major indices are holding ground in premarket trading. In fact, the SPY and QQQ look as if they could be trying to form a short-term bottom for their pullbacks. Either way, over-extension is not a problem in terms of the T-line (8ema) or the T2122 indicator (where we are just barely inside oversold territory). So, they have room to run if traders want to move the market.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

Swing Trade Ideas for your consideration and watchlist: COUP, CLX, BDX, NVDA, OGN, KHC, GSK, MOMO, and PUMP. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

On Thursday, stocks gapped modestly higher at the open (up 0.5% in the SPY, 0.4% in the DIA, and up 0.5% in the QQQ). Then after a 15-minute fade of the gap (except in the DIA), a rally took us to the highs by 10:30 am. From there, we saw a pullback to the open level in slow narrow-range trading until 1 pm. At that point, the bulls stepped in for a renewed rally that took us to new highs by 1:45 pm. However, another selloff took us back to the lows by 2:15 pm. Finally, price ground along the low end of the day’s range within a tight range. This action gave us gap-up, white-body, indecisive Spinning Top candles that failed a retest of the T-line (8ema) from below. None of the 3 major indices has been able to break their short-term downtrend.

On the day, eight of the ten sectors were in the green with the Technology sector (+1.62%) leading the way higher while Energy (-0.74%) and Communications Services (-0.75%) were the weakest sectors. In the meantime, the SPY was up 0.79%, the DIA was up 0.59%, and the QQQ was down 1.18%. The VXX fell by more than 2% to 14.98 and T2122 has climbed a bit to 34.91. 10-year bond yields were up to 3.489% and Oil (WTI) was off a half of a percent to $71.68 per barrel. So, Thursday saw a modest gap higher followed by indecision on very low volumes.

In economic news, Weekly Initial Jobless Claims came in exactly on forecast at 230k. This was 4k higher than last week. However, continuing claims reached an 11-month high. Later, Freddie Mac reported that the average 30-year, fixed-rate mortgage fell again this week to 6.33% (down from 6.49% the prior week). Gasoline prices are also lower than they have been in a year this week, with EIA analysts saying they expect the national average to dip below $3/gallon in the near future.

In stock news, Reuters reported that CS has been able to raise $2.39 billion in new capital to help finance its turnaround plan. Elsewhere, AVY told a conference that it is experiencing a “challenging finish to the year.” AVY shares plunged on the news. In other news, Bloomberg reported that the financers behind $13 billion of the money that Elon Musk used to buy Twitter are in discussions to restructure the debt, with Musk putting up TSLA stock as collateral. In banking news, Reuters reports that multiple sources have confirmed that GS is slashing yearly bonuses for senior employees. In more hopeful news, the CEO of GM said she expects car sales to rebound by more than 9% in 2023 (15 million units versus 13.7 million in 2022).

In government news, the House overwhelmingly approved (by 350-80) a record $858 billion Defense spending bill for 2023 ($45 billion more than requested by President Biden). Meanwhile, the FTC voted 3-1 to officially block the MSFT acquisition of ATVI. Later in the day, the FTC announced plans to sue to enforce their decision. Elsewhere, the SEC warned public firms to study and report their exposure to cryptocurrency risks, which have been unreported to this point in general. Finally, overnight the short-lived Democratic majority in the Senate slipped as AZ Senator Sinema announced she is leaving the Democratic party to become an independent.

In energy news, oil majors XOM and CVX both announced Thursday that they will be significantly expanding CAPEX investments in the US and Canada in 2023. Finally, oil closed lower for the fifth straight day on Thursday despite the closure of the major Canada-to-US Keystone pipeline (which delivers 622k barrels per day to the US and is operated by TRP).

After the close, AVGO, CHWY, LULU, RH, and DOCU all reported beats on both the revenue and earnings lines. Meanwhile, COO beat on revenue while missing on the earnings line. Unfortunately, COST missed on both the top and bottom lines. It is worth noting that RH and AVGO raised their forward guidance while COO lowered its own guidance. Then this morning, LI reported misses on both the top and bottom lines. LI also lowered its forward guidance.

Overnight, Asian markets were mostly green as Chinese covid-easing and a $108 billion Chinese bond sale (to be used for economic stimulus) boosted the region. Hong Kong (+2.32%), Japan (+1.18%), and Taiwan (+1.05%) led the region higher. Then in Europe, we see a mixed and modest market at midday. The FTSE (-0.12%) lags while the DAX +0.32%) and CAC (+0.02%) indicate the mood of the continent in early afternoon trade. As of 7:30 am, US Futures are pointing toward a modestly green start to the day. The DIA implies a +0.18% open, the SPY is implying a +0.32% open, and the QQQ implies a +0.43% open at this hour. At the same time, 10-year bond yields are down just a tick to 3.485% and Oil (WTI) is up eight-tenths of a percent to $72.07 per barrel in early trading.

The major economic news events scheduled for Friday are limited to November PPI (8:30 am) and Michigan Consumer Sentiment (10 am). The major earnings reports scheduled for the day include Thursday, we hear from LI before the open. There are no earnings reports after the close.

With that background (and remembering that we have Wholesale Inflation data at 8:30 am), it looks like all three major indices are retesting their T-lines (8ema) in premarket trading. Therefore, obviously, over-extension is not a problem either in terms of the T-line (8ema) or the T2122 indicator. The short-term trend does remain bearish (despite yesterday’s green day) within the mid-term bullish trend now broken. However, all three major indices look like they will be testing that short-term downtrend with their open this morning. The QQQ was able to climb back up above its support level (despite a significant test on Wednesday and Thursday). And if the bulls cannot put in a strong rally today, we are headed toward a down week (the first in the DIA in a month). Lastly, remember that its Friday with a weekend news cycle ahead and a Fed meeting next week.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

Swing Trade Ideas for your consideration and watchlist: No trade ideas today. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Markets gapped down modestly (a half of a percent in the QQQ and a quarter percent in the large-cap indices) on Wednesday. Price then proceeded to meander sideways all day on low volume except for the DIA (which is looking like it will achieve average volume). This action is giving us black-bodied indecisive Doji candles in all three major indices. The QQQ managed to retest and fail resistance while the SPY and DIA did not get down to the level of testing support again.

On the day, nine of the ten sectors were in the red with Healthcare (+0.55%) by far the strongest and Energy (-0.65%) and Consumer Cyclical (-0.68%) the weakest sectors. In the meantime, the SPY was down 0.17%, the DIA was up 0.01%, and the QQQ was down 0.42%. The VXX was up by more than 1.45% to 15.29 and T2122 has climbed back out of the oversold territory to 20.52. 10-year bond yields were down a bit to 3.42% and Oil (WTI) was off 2.55% to $72.36 per barrel. So, Wednesday was an indecisive day that amounted to a fifth straight down day in the SPY and a fourth straight in the DIA.

In economic news, Q3 Unit Labor Costs rose far less than expected at +2.4% (versus a forecast of +3.1% and the Q2 increase of 3.5%). Q3 Nonfarm Productivity was also up more than expected at +0.8% (compared to a forecast of +0.6% and the Q2 value of +0.3%). This caused a small gap lower as traders interpreted modestly good economic data as not pushing the Fed in either direction. Later in the morning, we saw EIA Weekly Oil Inventories fall more than expected at -5.187 million barrels (versus the forecast of -3.305 million barrels but still nowhere near as much of a drawdown as the prior week’s 12.580 million barrels).

In stock news, LUV reinstated its dividend Wednesday after a three-year suspension. The CEO of the company cited a strong return of travel demand as he announced the company will pay $0.18/share to shareholders of record on January 31. Later, Reuters reported that AMZN was offline mid-morning. No details on the cause of the outage were given. In other AMZN news, Washington DC has sued the company for diverting tips intended for delivery drivers to its own coffers. Elsewhere, the CEO of C said she expects trading revenue to rise 10% in the current quarter while investment banking fees will fall 60% (in line with industry norms this quarter). In “you don’t say” news, the CEO of COIN said he expects the revenue of their cryptocurrency trading platform to be down 50% for 2022 compared to 2021. This comes after their competitor FTX and Celsius Network both filed for bankruptcy as well as the massive crash of crypto prices. In legal news, CVNA is meeting with lawyers and bankers to discuss ways to restructure its debt load with the risk of bankruptcy rising.

In government news, US lawmakers declined to exempt BA from a looming deadline for a new safety standard related to its “737 Max” jets. This loss will mean BA will need to rework safety systems on new planes before they can be certified by the FAA. Meanwhile, after hours, GOOGL, ORCL, AMZN, and MSFT were awarded $9 billion in contracts by the Dept. of Defense related to “Cloud services.” This comes a year after an AMZN lawsuit killed the previous awarding of these contracts to MSFT (based on bias introduced into the procurement process by former-President Trump).

In energy news, crude oil (WTI) fell again Wednesday in volatile trading, reaching close to the lowest level in a year. The causes this time were the EIA report that showed an unexpected inventory build of 6.2 million barrels of distillates (like diesel fuel). This post-refining inventory glut more than outweighed the crude oil inventory drawdown of 5.2 million barrels and the fall came in spite of news that Chinese oil imports reached the highest level in 10 months in November. In other energy news, PSX announced that was one fatality and another contract employee injured in a crane accident at its Wood River IL refinery.

After the close, GEF and GME reported misses on both the revenue and earnings lines. So far this morning, GMS, CIEN, KFY, and MOMO all reported beats on both the top and bottom lines. (HOV reports at 9:15 am.)

Overnight, Asian markets were mixed but leaned bearish with Hong Kong (+3.38%) and outlier on the post-Covid China opening news. Australia (-0.75%), Taiwan (-0.53%), and South Korea (-0.49%) led the region lower. Meanwhile, in Europe, the exchanges are mostly in the red at midday. The FTSE (-0.05%), DAX (-0.34%), and CAC (-0.26%) are typical of the continent with only three smaller exchanges in the green in early afternoon trade. As of 7:30 am, US Futures are pointing toward a modest green opening ahead of Jobless Claims. The DIA implies a +0.13% open, the SPY is implying a +0.20%) open, and the DIA implies a +0.20% open at this hour. 10-year bond yields are up to 3.447% and Oil (WTI) is up 2.19% to $73.55/barrel in early trading.

The major economic news events scheduled for Thursday are limited to Weekly Initial Jobless Claims (8:30 am). The major earnings reports scheduled for the day include Thursday, we hear from CIEN, GMS, HOV, and KFY before the open. Then after the close, AVGO, CHWY, COO, COST, DOCU, LULU, and RH report.

In economic news later this week, on Friday, November PPI and Michigan Consumer Sentiment are reported. In earnings later this week, on Friday, we hear from LI.

As stated above, Hong Kong skyrocketed overnight on the China opening story. Specifically, local Hong Kong media reported that the city is considering the outdoor mask requirement and reducing the isolation period for those who test positive for Covid-19. In addition, the Hong Kong government is considering replacing the need for two negative PCR tests with one rapid-antigen test for inbound travelers. Elsewhere, the Netherlands (home of ASML) appears to be falling in line with President Biden’s recently expanded chip sanctions for China (which restrict the sale of equipment used in the production of chip Fab facilities and which ASML is one of the world leaders in producing).

With that background, it looks like markets are setting up for a small gap higher, moving against the recent downtrend. Just remember Monday, when a similar gap-up turned into a slow all-day rout by the Bears. Over-extension is not yet a problem either in terms of the T-line (8ema) or the T2122 indicator. The short-term trend remains bearish within the mid-term bullish trend now broken. Only the large-caps indices still have support close below with the QQQ now not far below resistance (broken support). So, if the bulls cannot rally to hold those support levels we could see a bearish run for several percent in the near future.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

Swing Trade Ideas for your consideration and watchlist: CLX, PUMP, BK, PAAS, ANF. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

With a growing number of major financial institutions and company CEOs dominating the news cycle, warning of a 2023 recession, the bears extended their attack Tuesday. Though the selling raised some uncertainty for a Santa rally, critical support levels in the index charts held. However, we will need the bulls to step up and defend now, or the bears could quickly create some technical damage that may be difficult to recover. Earnings and economic reports could provide some inspiration, but recession worries, pending PPI and FOMC decisions, will likely keep uncertainty high for the near future.

While we slept, Asian markets sold off, with Hong Kong leading the way, down 3.22% as trade data disappointed. European markets also trade in the red this morning as the bear market rally sentiment diminishes with worries of a looming recession. U.S. futures reversed modest overnight bullishness to suggest a slightly bearish opening ahead of earnings and economic data. Uncertainty is high so prepare for news driving price volatility to continue.

Economic Calendar

Earnings Calendar

We have more activity on the Wednesday earnings calendar, but unlikely market-moving reports. Notable reports include AI, BF.B, CPB, GME, KFY, LOVE, OLLI, SPWH, THO, UNFI, & VRNT.

News & Technicals’

CEOs from JPMorgan, General Motors, Walmart, United, and Union Pacific are preparing for an economic slowdown. Rising interest rates, inflation, and geopolitical concerns are among the issues cited. The companies are taking a conservative approach to 2023. Goldman Sachs and Morgan Stanley have cut workers ahead of a possible economic downturn, but Bank of America CEO Brian Moynihan and his CFO have said they don’t see the need for layoffs. That doesn’t mean Bank of America’s headcount won’t shrink as it looks to cut expenses. “We’re up to about 215,000 [employees]; we need to run that backdown,” he said Tuesday.

Fink has become an outspoken proponent of “stakeholder capitalism” and, in his annual letter to CEOs earlier this year, pushed back against accusations that the giant asset manager was using its size to push a political agenda. Bluebell — an activist fund with around $250 million in assets under management that holds a tiny stake in BlackRock — has previously targeted the likes of Richemont and Solvay and had a hand in successfully forcing management to restructure at Danone.

With a growing number of banks and company CEOs warning about a 2023 recession, the bears found the inspiration to matain their attack on Tuesday. However, on the good news side of the selling, it has substantially relieved the frothy overbought condition of the Dow and key support levels held at yesterday’s close. The bad news is that recession worries continue to grow and wouldn’t take much to push the SPY, QQQ, and IWM below support to possibly spoil the hoped-for Santa rally. Today we have a few more earnings reports, Mortgage Apps, Productivity and Costs, and Petroleum Status numbers to inspire the bulls and bears. With a PPI number this Fraidy and an FOMC decision next week, understandably, making traders question the uber-bullish stance of late. With the big financial institutions battening down the hatches and layoff projections rising, plan for a volatile end to 2022.

On Tuesday markets opened flat only for all three major indices to start a long, steady selloff that lasted until 3:30 pm. However, the shorts took profits the last 30 minutes of the day to take us out up off the lows. The SPY and QQQ both also failed their uptrend lines during the day. This action gave us big black candles with small wicks at both ends. All three major indices also retested and failed their T-lines (8ema) on the day. This action took place on a larger-than-average volume in the DIA with a bit less than average volume in the SPY and QQQ.

On the day, nine of the ten sectors were in the red with only the Utilities (+0.11%) able to stay in the green while Technology (-2.23%) led the way lower. In the meantime, the SPY was down 1.45%, the DIA was down 1.05%, and the QQQ was down 2.07%. The VXX was up by more than 3% to 15.07 and T2122 has dropped into the oversold territory at 15.85. 10-year bond yields were down a bit to 3.531% and Oil (WTI) was off 3.38% to $74.35 per barrel. So, Tuesday was slow melt which saw the large caps close down a fourth straight day and the QQQ close lower for the third straight session.

In economic news, October Imports were up about $3.5 billion while October Exports fell just under $2.5 billion. This gave us an October Trade Balance deficit that was a bit less than expected at -$78.20 billion (compared to a forecast of -$80 billion) but also above the prior month’s actual of -$74.10 billion. Then after the close, the API Weekly Crude Oil Stock Report saw a larger-than-expected drawdown at -6.426 million barrels (versus a forecasted drawdown of 3.884 million barrels and last week’s drawdown of 7.850 million barrels).

In stock news, the EU Privacy Watchdog group ruled that META can no longer run ads based on users’ personal data without the users’ explicit consent. On this side of the pond, the CEO of BAC told Bloomberg that the company will be slowing hiring as fewer than expected employees are leaving the company, but continues to seek talent. This stands in contrast to MS, which let 2% of its workforce (1,600 people) go on Tuesday. In other news, Bloomberg reported AAPL has scaled back and delayed (until 2026) its plans to offer self-driving car software for electric vehicles. Meanwhile, a US District Judge ruled in favor of GSK, PFE, and SNY throwing out 50 thousand of US lawsuits that had claimed the heartburn drug Zantac caused cancer. However, about 10,000 similar cases in state and local courts remain intact. Finally, Reuters reports that MOS says that it is cutting potash production at its Saskatchewan Canada mine citing slower-than-expected demand.

In energy news, Oil (WTI) closed very near a one-year low on Tuesday. This comes as Fed and recession fears have overcome last month’s OPEC+ production cuts. Earlier in the day, the EIA released projections that US oil production for the year would rise marginally more than their previous estimates to 11.87 million barrels per day average (compared to the previous estimate of 11.83 million barrels per day). They also now estimate that 2023 production in the US will reach 12.34 million barrels per day. Still, they expect US oil consumption to be 20.36 million barrels per day and forecast that will rise to 20.51 million barrels per day in 2023.

After the close, PLAY and TOL reported beats on both the revenue and earnings lines. Meanwhile, CASY missed on revenue while beating on earnings. Unfortunately, SFIX missed on both the top and bottom lines. It is also worth noting that TOL and SFIX have both reduced their forward guidance.

Overnight, Asian markets leaned to the downside. Hong Kong (-3.22%) was an outlier while Australia (-0.85%), Singapore (-0.83%), and Japan (-0.72%) paced the losses. Only Shenzhen (+0.17%) managed to stay green. Meanwhile, in Europe, we see a similar picture taking shape at midday. Only the FTSE MIB (+0.01%) and Greece (+0.15%) are in the green while the FTSE (-0.05%), DAX (-0.39%), and CAC (-0.41%) lead the way lower in early afternoon trade. As of 7:30 am, US Futures are pointing toward a red start to the morning. The DIA implies a -0.29% open, the SPY is implying a -0.45% open, and the QQQ implies a -0.70% open at this hour. 10-year bond yields are up slightly to 3.54% and Oil (WTI) is on the green side of flat at $74.35/barrel in early trading.

So far this morning, THO and CPB reported beats on the revenue and earnings lines. Meanwhile, UNFI beat on revenue while missing on earnings. (ASO, BF.B, and OLLI all report later but before the opening bell.)

The major economic news events scheduled for Wednesday include Q3 Labor Cost and Q3 Nonfarm Productivity (both at 8:30 am), and EIA Crude Oil Inventories (10:30 am). The major earnings reports scheduled for the day include ASO, CPB, WLY, THO, and UNFI before the open. Then after the close, GME and GEF report.

In economic news later this week, on Thursday we get Weekly Initial Jobless Claims. Then on Friday, November PPI and Michigan Consumer Sentiment are reported. In earnings later this week, on Thursday, we hear from CIEN, GMS, HOV, KFY, AVGO, CHWY, COO, COST, DOCU, LULU, and RH. Finally, on Friday, we hear from LI.

Overnight the Democrats expanded their tiny majority in the US Senate as Senator Warnock won the GA runoff election. Elsewhere, the first electric vehicle maker unionization vote is taking place in Ohio today and Thursday as the UAW seeks to unionize the GM battery plant in Northeastern Ohio. In non-election news, the large banks warned of recession yesterday and are preemptively cutting jobs to preserve profitability. For their part, WMT says the consumer is strong and we actually need a recession to tame inflation. This all came as the demand for mortgages fell again last week, even as mortgage interest rates fell from 6.49% to 6.41% for a 30-year, fixed-rate, conforming loan. The Mortgage Bankers Assn. said demand fell by 1.9% last week (but were 86% lower than the same week of 2021).

With that background, it looks like premarkets are down again as the QQQ test support and the SPY is reaching to do the same. DIA has not gotten there yet, but could do so on a bad day. The short-term trend remains bearish within the mid-term bullish trend no broken. Note that we have no extension from the T-line is only potentially a problem in the QQQ at the moment. However, we did dip into the oversold area of the T2122 indicator yesterday. Of course, we do have Q3 Productivity and Labor Cost data at 8:30 am, but those are not usually huge market movers. So, overall, if the bulls cannot rally to hold support levels we could see a bearish run for several percent in the QQQ and SPY (with the DIA holding up better on the rotation to the safety of the mega-cap names).

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

Swing Trade Ideas for your consideration and watchlist: No trade ideas today. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service