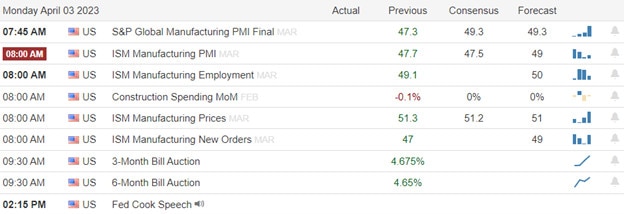

It took until Friday afternoon for the end-of-quarter window dressing activity to finally trigger s short squeeze surging indexes higher into the Friday close. The question now is can they follow through with the uncertainty of 2nd quarter earnings and a T2122 indicator showing an overbought index condition? Surging oil prices will be a help to the bulls after the surprise production cut decision from OPEC this weekend. However, PMI, ISM, and construction spending numbers have recently shown a very weak economic condition the bears may also find inspiration to fight back. Expect some big price moves, and watch for the possibility of quick intraday whips as a new quarter of trading begins.

During the night Asian markets mostly rallied with modest gains with surging oil prices rising costs. Though UBS falls 4% this morning and Europe worries about the rising oil prices their indexes continue to push upward across the board this morning. However, U.S. futures trade mixed this morning with Dow benefiting from the rising oil prices while tech indicates a bearish open with the SP-500 suck somewhere in the middle.

Economic Calendar

Earnings Calendar

We have a very light week on the earnings calendar as we wait for the official kick-off of the 2nd quarter with the big bank earnings beginning April 13th. Notable reports for Monday include AYI, LNN, MSM, RGP, & SGH.

News & Technicals’

Several OPEC+ members have announced intentions to voluntarily cut a further combined 1.16 million barrels per day of production. This move is independent of the broader bloc’s output strategy and will challenge consumer governments, such as the U.S., which are already tackling high inflation and volatility in the banking sector. A formal meeting of an OPEC+ technical committee takes place Monday to review the group’s existing strategy. It cannot change policy. Oil prices soared as much as 8% at the open after OPEC+ announced it was slashing output by 1.16 million barrels per day. The voluntary cuts will start from May to the end of 2023, Saudi Arabia announced, saying it was a “precautionary measure” targeted toward stabilizing the oil market.

Burger chain McDonald’s is temporarily closing its U.S. offices this week as it prepares to inform corporate employees about its layoffs as part of a broader company restructuring. “During the week of April 3, we will communicate key decisions related to roles and staffing levels across the organization,” the Chicago-based company said in the message viewed by The Wall Street Journal. McDonald’s also asked employees to cancel all in-person meetings with vendors and other outside parties at its headquarters. McDonald’s is expected to begin announcing key decisions by Monday.

The end of the quarter finally developed into a short squeeze on Friday afternoon with a strong buying push into the close of the day. At the same time, however, the T2122 indicator reached an overbought condition adding to the question if the bulls will have the energy to follow through with more buying in the Monday market. On the other hand, Goldman suggests this weekend that the institutional CTA’s are overly short and could begin a buying spree this week unless we see a substantial downside move. Adding additional upside pressure was the surprise OPEC decision to cut oil production substantially causing oil prices to surge this morning. That said we still face PMI, SIM, and Construction Spending data that have been very weak economic indicators of late. With lots of job data ending with the employment situation report on Friday traders should prepare for just about anything.

Friday was the bull’s day on Wall Street with a modest gap higher at the open from the large-cap indices. The SPY gapped up 0.22% and DIA gapped up 0.32%. Meanwhile, QQQ opened dead flat. However, after the open, a slow, steady rally took hold and kept going the entire day. We closed very near the highs in all three major indices. This action gave us large-bodied, white candles, with no lower wick and a tiny upper wick. So, nearly Marubozu (Shaved Head) candles in the SPY, DIA, and QQQ. DIA crossed up through its 50sma during the day and the SPY and QQQ are now getting extended above their T-lines (8ema). This happened on average volume in QQQ, a bit greater-than-average volume in the SPY but lower-than-average volume in the DIA.

On the day, all 10 sectors were in the green with Consumer Cyclical (+2.02%) leading the way higher while Communications Services (+0.29%) lagged behind other sectors. At the same time, the SPY gained 1.41%, the DIA gained 1.26%, and QQQ gained 1.66%. VXX fell slightly to 44.91 and T2122 climbed even further into the overbought territory to 95.39. 10-year bond yields fell again to 3.473% while Oil (WTI) rose 1.79% to $75.70 per barrel. So, Friday saw the bulls in charge all day long, even though there was not a large gap higher at the open.

In economic news, the February PCE Price Index came in a bit below expectation at +5.0% (year-on-year), compared to a forecast of +5.1% and the January reading of +5.3%. Meanwhile, February Personal Spending increased less than expected at +0.2%, versus a forecast of +0.3% and far below the January value of +2.0%. So, the Fed’s favorite measure of inflation fell three-tenths of a percent while consumer outlays also did not increase as much as expected. Both are what the Fed wants to see. Still, it is worth bearing in mind that inflation is still 3% above the Fed target of 2.0%. Later, the Chicago PMI came in above expectation at 43.8 (compared to a forecast of 43.4 and the February value of 43.6). Then the Michigan Consumer Sentiment came in below expectations at 62.0 (versus a forecast of 63.2 and the February reading of 63.4).

In stock news, STLA announced Friday that it will be spending $3.14 billion to launch eight brands of vehicles (43 total models) as of 2025. The company claims this to be a larger investment in that region than all competitors combined. Meanwhile, Chinese electric car maker XPEV announced it will upgrade and expand its Advanced Driver Assistance system to be available all across China by 2024. This might give XPEV an advantage over TSLA whose driver assist software only has limited availability in China. (Perhaps unrelated, TSLA CEO Musk announced Friday he will be making a trip to China.) Elsewhere, after the close, GM said it expects a number of its EV models (including Cadillac Lyriq, Chevy Equinox, and Chevy Blazer) to qualify for the full $7,500 tax credit. (TSLA had said on Wednesday that its Model-3 will only qualify for partial credit and F will provide more guidance on that matter soon.) On Sunday, TSLA announced they had delivered 422,875 cars in Q1. This was a 36% increase compared to Q1-2022 and a 4% growth compared to Q4 2022. However, this was almost 10,000 cars short of the average analyst estimate.

In stock legal and regulatory news, a CA judge ruled against AMZN in their bid to have a CA state antitrust lawsuit dismissed. The suit accuses AMZN of illegally forcing merchants to accept policies that caused consumers to pay artificially inflated prices. Meanwhile, a new racial bias lawsuit was filed against TSLA on Friday by a former worker who claims he was fired for pushing back against racist comments made by his supervisor. (This is a second suit filed making this claim. In the earlier case, TSLA lost, but the case is being reheard after the plaintiff rejected an appeals court reduction of the jury award.) Elsewhere, AAPL won its appeal against Britain’s antitrust regulator who wanted to launch an investigation of AAPL and GOOGL mobile browser market dominance. Late in the day Friday, the CA, MD, NJ, and NC state Attorneys General joined the US Dept. of Justice lawsuit to block the JBLU acquisition of SAVE for $3.8 billion. Separately, FL closed its probe into the deal aver JBLU and SAVE agreed to increase seat capacity in both Orlando and Ft. Lauderdale. At the same time, the National Labor Relations Board announced it has found ATVI violated US Labor Laws by illegally spying on employees and threatening to shut down internal communications channels (chat and email) as workers sought to organize. After the close, JNJ lost its bid to have its subsidiary stay in Bankruptcy (to avoid legal liability) while it waits on an appeal to the US Supreme Court. Finally, AAPL convinced a US Appeals court to throw out a $502 million verdict for patent infringement against VirnetX.

In energy news, on Friday the Biden Administration auctioned off 73 million acres of drilling rights in the Gulf of Mexico. On Sunday, first came some good news, as Iraq and its Kurdish Regional Government agreed in principle to resume oil exports through Turkey. This will increase global supply by one-half or one percent. However, then in a surprise announcement, OPEC+ announced production cuts of about 1.2 million barrels per day (around 3.7% of global daily consumption). The oil cartel expects to maintain this additional level of production cuts (3.2 million barrels per day in total) through the end of 2023. The new cuts will begin in May and analysts predict it will cause a $10/barrel increase in oil prices. All of this comes after oil posted a good week, but a bad month and a terrible quarter. WTI was up 1.8% on the day Friday, up 9.2% for the week but was down 5% for the month of March and down 7.3% in Q1. For its part, Natural Gas also had a strong day Friday, surging 5.3% on the day. Still, it fell 6% on the week, lost 19% in March, and posted a historic record 50% loss in the first quarter.

Overnight, Asian markets were mixed but leaned toward the green side. Thailand (-0.55% paced the three losing exchanges while Shenzhen (+1.39%), Malaysia (+0.76%), and Shanghai (+0.72%) led the gainers. Meanwhile, in Europe, a similar story is taking shape at midday. The CAC (+0.40%), DAX (-0.04%), and FTSE (+0.73%) are typical and lead the region modestly higher in early afternoon trade. As of 7:30 am, US Futures are pointing toward a mixed start to the day. The DIA implies a +0.36% open, the SPY is implying a -0.09% open, and the QQQ implies a -0.66% open at this hour. At the same time, 10-year bond yields are up to 3.505% and Oil (WTI) is skyrocketing (+0.608%) on the OPEC+ news to $80.27/barrel.

The major economic news events scheduled for Monday include Manufacturing PMI (9:45 am) and ISM Mfg. PMI (10 am). The major earnings reports scheduled for the day include SAIC before the open. Then after the close, there are no earnings reports scheduled.

In economic news later this week, on Tuesday we get February Factory Orders, Feb. JOLTs Job Openings, and the API Weekly Crude Oil Stocks Report. Then Wednesday, ADP March Nonfarm Employment Change, Feb. Imports/Exports, Feb. Trade Balance, March Service PMI, S&P March Global Composite PMI, March ISM Non-Mfg. PMI, and EIA Weekly Crude Oil Inventories are reported. On Thursday, we get Weekly Initial Jobless Claims and Bank Reserve Balances with Federal Reserve Bank. Finally, on Friday, US markets are closed but March Avg. Hourly Earnings, March Nonfarm Payrolls, March Participation Rate, March Private Nonfarm Payrolls, and the March Unemployment Rate are reported.

In terms of earnings, on Tuesday, AYI and MSM report. Then Wednesday, we hear from CAG and SCHN. On Thursday, LW, STZ, RPM, and LEVI report. There are no reports scheduled for Friday.

On Sunday CNBC reported that EDR (the parent of the UFC) is very near a deal to acquire WWE (“professional wrestling”). A deal may be announced as soon as Monday. However, this morning, the deal is being characterized as a merger with EDR as the senior partner and its leader remaining CEO, while the current leader of UFC (Dana White) would continue to run UFC and the CEO of WWE (Vince McMahon) would continue to run WWE. Elsewhere, a Swiss newspaper (Tages-Anzeiger) reported Sunday that the new bank created by the UBS acquisition of CS is set to cut 20%-30% if its workforce (11,000 jobs in Switzerland). US jobs will also be affected, but no details were available. Meanwhile, China urged Japan not to support the US chip and chip-making equipment embargo on China after Tokyo announced new restrictions Friday. The new restrictions would prohibit Japanese companies from selling 23 types of chip-making equipment (but avoided naming China specifically).

The short week ahead contains three stories of major note on the political front. Ex-President Trump will be arraigned on 30 charges related to fraudulent bookkeeping on Tuesday. I’m sure there’s no chance that will be turned into a circus but, given what Trump has said/written pre-arraignment, there is always hope for a gag order from the judge. In addition, there are two elections of note Tuesday. The most important is the election of the swing vote to the Wisconsin Supreme Court. At stake will be redistricting and potential future “election was stolen” decisions in that purple (swing) state. It is worth noting that the two sides of this election have spent $40 million total…for the election of a state judge. The other election is the runoff for the new Chicago Mayoral race after the incumbent was defeated during the initial round of voting.

With that background, it looks like the markets are still digesting the OPEC+ surprise production cut (pseudo inflation hike). Tech holders seem nervous (and most impacted), the market-leading SPY appears unsure how that news shakes out, and the mega-cap DIA (secure in the ability to pass on price increases) look unimpressed by the new threat. Remember, today is the first day of the new quarter/month after what could easily be seen as a “Window Dressing” run the last three days of last week. So, it would be natural (and maybe even expected) that we see a pullback or at least consolidation to start April. Bullish overextension was also an issue as of Friday’s close. As a result, we should keep an eye open for bearish action this week.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Markets gapped higher at the open Thursday (up 0.66% in the SPY, up 0.54% in the DIA, and up 0.77% in the QQQ). However, for the large-cap indices, this was a bull trap as the DIA immediately began selling and the SPY waited an hour and then began selling off. Both maintained a steady bearish pace once the selling began. For its part, the QQQ ground sideways and even had a slightly bullish trend until 11:15 am. At that point, it too began a steady selloff. DIA reached its low of the day (back below the Wednesday close) at 12:50 pm. Meanwhile, SPY and QQQ reached their low (still in the gap) at 1:50 pm. From that point, the bulls stepped in for a slow steady rally that lasted into the close. This action gave us gap-up candles with the SPY and QQQ both printing Doji and the DIA printing a black-bodied Hanging Man candle. DIA is also testing a resistance level.

On the day, nine of the 10 sectors were in the green with Consumer Cyclical (+0.97%) leading the way higher while Financial Services (-0.18%) lagged behind other sectors. At the same time, the SPY gained 0.59%, the DIA gained 0.44%, and QQQ gained 0.95%. VXX was dead flat at 45.11 and T2122 was also flat, staying in the overbought territory at 88.03. 10-year bond yields fell slightly to 3.553% while Oil (WTI) rose almost 2% to $74.39 per barrel. So, on Thursday we saw signs of indecision with all three major indices giving us candles with a lot of wick and very little body. We did move a little further from the T-line (8ema) and there are signs that the bulls are a little tired or at least tepid going into Friday (the last day of the month and quarter). We also saw a divergence in volumes as DIA had very low volume, QQQ was close to average and SPY was in between the other two major indices.

In economic news, the Final Revision of Q4 GDP came in just shy of forecast at +2.6% (compared to a forecast of +2.7% and a Q3 reading of +3.2%). At the same time, the Final Revision of Q4 GDP Price Index came in just as expected at +3.9% (versus the forecast of +3.9% and down from the Q3 reading of +4.4%). So, this confirms that economic growth was slowing in Q4…especially when you consider the inflation factor was above the growth rate. However, that inflation was also declining. Both of these are what the Fed hopes to hear and wants to occur. The only argument, then, is over how fast the slowing of growth and decreasing of inflation are happening. Elsewhere, the Weekly Initial Jobless Claims were slightly above the forecasted value at 198k (versus an expected 196k and also above the prior week’s 191k reading). Still, those layoffs are not high enough to significantly impact the labor market.

In stock news, on Thursday, VLCN announced it has launched two new models of electric motorcycle, one designed for on road and one for off-road driving. In other electric vehicle news, F reopened order reservations for its F-150 Lightning trucks at a new $4,000 higher price ($20,000 higher than when the truck was launched in April 2022). Meanwhile, a bi-partisan group of US Senators introduced a bill aimed at META, GOOGL, AMZN, and AAPL. The bill would restrict companies selling more than $20 billion in digital advertising from owning more than one part of the stack of services that connect advertisers with the companies who have digital ad space for sale. After the close, Reuters reported that BA will increase production of its 737 MAX to exceed the current 31 planes per month. Elsewhere, JD announced after the close that it will spin off its property and industrial units and list those entities on the Hong Kong Stock Exchange. This appeared to be a counter move to BABA (JD rival) plans to split into six businesses. After the close, Reuters reported that TSLA “solar roof” installation target were only 2% of CEO Elon Musk’s goals. (Musk’s 2021 forecast was for an average of 1,000 installations/week in 2021. However, the 2022 average was only 21 installations per week.) This miss was due to competitors getting the business. Finally, after the close it was reported that VORB has failed to secure funding. As a result, it will cease operations “for the foreseeable future” and will eliminate 85% (675) of the company’s positions.

In stock legal and regulatory news, META announced that beginning next Wednesday, it will allow European users to opt-out of targeted ads on its Facebook and Instagram services. The move comes in the wake of the December EU privacy order that began fining META $423 million. Elsewhere, a tech ethics group has asked the US FTC to stop OpenAI from issuing new commercial releases of its ChatGPT-4. MSFT, which has closely integrated OpenAI into its product offerings, as well as other companies are expected to fight any such move by the FTC. (A similar request is likely to follow for GOOGL’s Bard and other AI platforms.) At the same time, the US Consumer Financial Protection Bureau has ruled that lenders must begin collecting demographic and geographic data on loans to small businesses. The loan census data will be used to identify patterns of discrimination. Meanwhile, WFC will pay another $98 million for poor oversight and failing to comply with US sanctions against Iran, Syria, and Sudan. Late in the day, F withdrew its petition to the NHTSA which had sought approval to deploy 2,500 self-driving vehicles annually. A similar petition from GM is still pending approval. After the close, President Biden urged the Supreme Court to hear a case after the US Court of Appeals ruled TEVA had infringed a GSK patent by using a so-called “skinny label.” If the case were heard and the ruling was in TEVA’s favor, generic drugs would likely be more widely available.

In energy news, Natural Gas continues its historic slide. The front-month natty fell another 4% Thursday with the low of the day coming at $2.082/mmBtu. This leaves natural gas at the lowest price since mid-July 2020. And, unless there is a strong rally Friday, the first quarter will book more than a 50% decline in natural gas prices, which would be the largest quarterly drop in history. Thursday’s move came after the EIA reported a weaker-than-forecasted drawdown of inventories. The report cited a withdrawal of 47 billion cubic feet for the week (compared to a forecasted drawdown of 54 billion cubic feet). This leaves inventories 31% higher than the same time in 2022 and up 21% from the 5-year average inventory. Obviously, UNG reflects the same story, down 53% for the quarter as of Thursday’s close.

In miscellaneous news, the big story for Friday is likely to be ex-President Trump’s indictment by a New York Grand Jury. This Grand Jury found Trump should stand trial on multiple charges, including at least one felony, related to fraudulent reporting of a hush money payment and it then being claimed as a legitimate business expense for tax purposes. Apparently, surrender and arraignment has been negotiated to happen next week. The other big non-economic news is also political but does involve a major corporation. This one is the story of how DIS outwitted Florida Governor DeSantis’ (and that state’s GOP legislators’) move to punish the company for opposing Florida cultural issue legislation. DIS, legitimately and in public session, made a minimum 30-year contract (which could actually extend more than 100 years) with the (old) board that governs the Reedy Creek district. (That district board has jurisdiction over Disney World and related properties.) The contract gives DIS the exclusive right to decide on building high-density projects or buildings of any height or size or to assign those rights to anyone else DIS chooses. It also bans the new board from using the Disney name or characters in any way (like advertising). This contract was approved prior to the state taking over the district and DeSantis appointing his own new board. As a result, the move takes away most of the power of the new board and makes the DeSantis power move largely irrelevant. Obviously, DeSantis and the Florida GOP are furious and threaten action. However, multiple legal experts have reported that the contract is legal and binding.

Overnight, Asian markets were heavily green. Only New Zealand (-0.41%) and Malaysia (-0.14%) were in the red. Meanwhile, India (+1.63%), South Korea (+0.97%), and Japan (+0.93%) led the rest of the region higher. In Europe, we see the same picture taking shape at midday. Only Russia (-1.37%) and Denmark (-0.19%) are in the red. Meanwhile, the CAC (+0.56%), DAX (+0.42%), and FTSE (+0.20%) lead the region higher in early afternoon trade. In the US, as of 7:30 am, Futures are pointing toward a start to the day just on the green side of flat. The DIA implies a +0.21% open, the SPY is implying a +0.18% open, while the QQQ implies a dead flat open at this point. At the same time, 10-year bond yields are lower to 3.543% and Oil (WTI) is up more than three-quarters of a percent to $74.96 in early trading.

The major economic news events scheduled for Friday include Feb. PCE Price Index, and Feb. Personal Spending (bot hat 8:30 am), Chicago PMI (9:45 am), and Michigan Consumer Sentiment (10 am). We’ll also hear from Fed Member Williams at 3:05 pm. There are no major earnings reports scheduled for the day.

With that background, it looks like the markets are waiting on the Fed’s favorite inflation measure at 8:30 am. As of now, all three major indices are just on the bullish side of flat with 100 minutes left before the open. With today being month and quarter end, there may be some more window dressing activity. Also bear in mind that next week is a short week (Markets are closed Friday for “Good Friday”). Overextension is not a huge issue, but we are getting a little far from the T-line (8ema) and T2122 also shows markets a bit stretched. With the big legal news and so many people who feel they will need to weigh in on the topics, we might see a sleepy day in the market. However, that PCE Inflation gauge and quarter end are likely to call the market tune today.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

With the quarter coming to an end keep an eye out for the possibility of institutional window dressing over the next couple of trading days. Index charts improved on Wednesday helped in large part by the rally of the big tech giants. However, volume remained suspiciously low as the indexes stretch upward to test significant overhead resistance levels. With a reading on GDP and Jobless claims before the bell anything is possible at the opening of the day to be prepared for some early session price volatility.

Overnight Asian markets mainly rallied but with modest upside results despite the easing of banking fears. European markets are also pushing higher this morning decidedly bullish across the board. Ahead of market-moving economic data U.S. futures indicate a bullish open but expect some price volatility as the market reacts to the data. Will it inspire the bulls or the bears? We will soon find out of plan your risk carefully!

Economic Calendar

Earnings Calendar

Notable reports for Thursday include ANGO, BB, LAC, NEOG & MDRX.

News & Technicals’

Anna Ashton, China director at the Eurasia Group, said that a meeting between Taiwan’s President Tsai Ing-wen and U.S. House Speaker Kevin McCarthy will provoke a strong reaction from China. Taiwan’s President Tsai Ing-wen will likely meet face-to-face with Kevin McCarthy when she makes a transit visit through Los Angeles next week. According to Ashton, “The reality is that McCarthy is third in line to the presidency. A meeting like this would be the senior-most U.S. official meeting with a sitting Taiwan president on U.S. soil ever,”

Elon Musk and other tech industry figures have urged artificial intelligence labs to stop training AI systems more powerful than GPT-4, OpenAI’s latest large language model. In an open letter signed by Musk and Apple co-founder Steve Wozniak, technology leaders urged for a six-month pause to the development of such advanced AI, saying it represents a risk to society. Musk, who is one of OpenAI’s co-founders, has criticized the organization a number of times recently, saying he believes it is diverging from its original purpose.

Big Tech stocks contributed to Wednesday’s advance. Amazon popped 3%, while Meta and Netflix each gained more than 2%. Regional banks, closely followed since Silicon Valley Bank’s collapse earlier this month, also finished the session higher, with the SPDR S&P Regional Banking ETF (KRE) adding around 1%. On Thursday, investors will watch for economic data on weekly jobless claims and the gross domestic product. Boston Federal Reserve President Susan Collins, Richmond Fed President Thomas Barkin, and Minneapolis Fed President Neel Kashkari are all slated to speak in the afternoon.

Technically speaking the index charts improved yesterday with QQQ leading the way. However, with significant overhead resistance, there is still a lot for the bulls to accomplish before an all-clear can be sounded. With the pending GDP and Jobless Claims reports before the bell anything is possible by the open depending on whether the bulls or the bears find inspiration in the data. Watch for whipsaws and big price moves as we push to test overhead resistance with the possibility of a short squeeze mixed in if end-of-quarter window dressing becomes a factor.

On Wednesday, the bulls were in charge from the opening bell, perhaps on upbeat guidance from LULU and MU. SPY gapped 1.05% higher, DIA gapped 0.85% higher, and QQQ gapped 1.23% higher at the open. From that point, SPY and QQQ ground sideways in a tight range until 2:30 pm. Meanwhile, DIA traded down (back into the gap) and then sideways until 2:30 pm. However, then a mild rally all the way into the close took all three major indices out on their highs. This action gave us Morning Star-type signals in the SPY and QQQ with both printing white, larger-body, smaller wick candles. However, the DIA printed a white-bodied, potential Hangman (or Hammer if viewed through bullish glasses). Once again this happened on lower-than-average volume (much lower in the DIA).

On the day, all 10 sectors were in the green with Technology (+2.10%) leading the way higher while Consumer Defensive (+0.64%) lagged behind other sectors. At the same time, the SPY gained 1.43%, the DIA gained 1.01%, and QQQ gained 1.82%. VXX fell 3.28% to 45.11 and T2122 climbed into the overbought territory at 88.12. 10-year bond yields fell slightly to 3.564% while Oil (WTI) fell 0.57% to $72.80 per barrel. So, hump day gave us a strong start to the day, probably on easing concerns over the banking sector. Then traders played the “wait and see” card until the afternoon when the last 90 minutes saw a modest but steady rally into the close. SPY did break its downtrend line (going back to the beginning of February) and crossed just above its 50sma. DIA also crossed just up through its downtrend (also going back to the start of February).

In economic news, February Pending Home Sales came in much better than expected at +0.8% (compared to a forecast of -2.3% but far below January’s blowout reading of +8.1%). Later in the morning, the EIA Weekly Crude Oil Inventories report gave us a significant drawdown versus the expectation. Oil inventories fell 7.489 million barrels (versus a forecasted build of 0.092 million barrels and the prior week’s build of 1.117 million barrels. On the gasoline front, inventories saw a 2.904-million-barrel drawdown (compared to the forecasted drop of 1.625 million barrels and the prior week’s 6.4-million-barrel decline). In terms of distillates (diesel and heating oil), there was a 281,000-barrel inventor build (versus a forecast of a 1.455-million-barrel decline and the prior week’s 3.313-million-barrel drawdown).

In stock news, Reuters reported that ICUI has teamed up with a private equity firm to bid against the GEHC and CG in an effort to acquire the medical technology business of MDT. Elsewhere, UAL CEO Kirby announced the airline had reached an agreement in principle with 30,000 union ground workers for a new two-year contract. At the same time, WMG announced it will lay off 4% of its workforce (only about 270 people) and will cut discretionary spending in the near future. Meanwhile, the US GSA announced it has awarded BLNK a “Multiple Award Schedule” contract which allows federal agencies to easily purchase BLNK equipment. At mid-afternoon, M announced it has named Tony Spring (of Bloomingdale’s) as its new President and “CEO in waiting” one day after current CEO Gennette said he would retire in February of next year. Later, Reuters reported that BAC’s digital personal finance tool (Life Plan) has attracted more than $55 billion in new accounts since it was launched in late 2020. Meanwhile, DIS announced it has laid off the Chairman of its Marvel Entertainment unit, Ike Perlmutter. (It is worth noting that Perlmutter had supported activist investor Nelson Peltz’s bid to get a DIS board seat and oppose the reinstatement of DIS CEO Iger.) In “taking the negotiations public” news, Ryanair confirmed that it is in negotiations with BA over an order of at least 100 jets with the option for 100 more…but that significant discounts needed to be brought to the table to clinch the order. (Ryanair is one of BA’s largest customers, alongside LUV, and can demand the best pricing.) Finally, after the close, EA announced it will cut approximately 6% of its workforce as part of a restructuring.

In stock legal and regulatory news, it was announced that FNF will pay the State of NY $3.5 million for anti-competitive agreements that the company had entered into with its competitors in order to avoid competition. FNF also agreed to end all such “no poach” agreements. (NY had already reached similar agreements with FNF competitors STC and ORI since late 2021.) Elsewhere, Britain announced it will “investigate in depth” the $61 billion acquisition of VMW by AVGO. The announcement said this was after AVGO failed to engage with the UK government after the Brits had published its concerns. The investigation can take up to six months. Meanwhile, Bloomberg reports that the FDIC is considering passing a greater share of the $23 billion bank failure costs onto the largest US banks. While the final decision will not be made until May, this could have significant impacts on BAC, C, JPM, and WFC (each of which may face a multi-billion charge). At the same time, the state of CA began regulating how much profit oil refiners in the state can make as of Wednesday. CVX is the largest refiner in that state and PBF has the largest exposure to CA refining with 32% of its refineries located in CA. After the close, a federal judge ruled that RMAX (as well as other real estate brokerages and the National Assn. of Realtors) must face a class action lawsuit over allegations of conspiring to inflate commission rates in Texas, Florida, New Jersey, Ohio, Pennsylvania, Virginia, North Carolina, and Colorado.

After the close, CNXC beat on revenue while missing on earnings. Unfortunately, RH and FUL missed on both the revenue and earnings lines. It is worth noting that RH also lowered its forward guidance.

Overnight, Asian markets leaned heavily to the green side. Japan (-0.36%), Thailand (-0.32%) and Singapore (-0.26%) were the only red in the region. Meanwhile, New Zealand (+1.67%), Australia (+1.02%) and Shanghai (+0.65%) led most of Asia higher. In Europe, we find green across the board at midday. The CAC (+1.37%), DAX (+1.27%), and FTSE (+0.94%) are leading the region higher in early afternoon trade. On this side of the pond, as of 7:30 am, US Futures are pointing toward another gap higher to start the day. The DIA implies a +0.64% open, the SPY is implying a +0.60% open, and the QQQ implies a +0.54% open at this hour. At the same time, 10-year bond yields are down a bit to 3.556% and Oil (WTI) is up 0.93% to $73.64/barrel in early trading.

The major economic news events scheduled for Thursday include Q4 GDP, Q4 GDP Price Index, and Weekly Initial Jobless Claims (all at 8:30 am) as well as Bank Reserve Balances with Fed (4:30 pm). However, Treasury Sec. Yellen also speaks at 3:45 pm. There are no major earnings reports scheduled for the day.

In economic news later this week, on Friday, Feb. PCE Price Index, Feb. Personal Spending, Chicago PMI, and Michigan Consumer Sentiment are reported as well as Fed Member Williams speaking. In terms of earnings, there are no major earnings reports scheduled for Friday.

In late-breaking news, Russia has detained a journalist from the Wall Street Journal, alleging suspicion of espionage. This is undoubtedly just another Russian negotiating tactic as with the American women’s basketball player (Griner) arrested last year. Still, the move will ratchet up tensions between the US and the former superpower Russia. Elsewhere, AAPL announced its Worldwide Developer’s Conference (where it usually unveils new products) is set for June 5-9. This year, in addition to new phones, etc. the tech giant is expected to also unveil a new augmented reality headset. In oil news, Bloomberg reports that slowly disappearing supplies of Brent has forced S&P to make a huge change. As of June, the world benchmark oil price will be a combination of oil contracts that will include West Texas Intermediate at Midland TX (Permian Basin oil). Finally, various sources report that, after another failed test, the $1.1 billion LMT hypersonic missile program will be shut down in favor of a program from RTX.

With that background, it looks like the bulls will be gapping markets higher again at the open. (At least it does ahead of the morning data dump.) We should also look out for potential window dressing as we come into the end of the quarter Friday. In fact, some would explain Wednesday’s rally as just part of that dressing. The SPY is looking to gap open above its 50sma after ending yesterday just above following an all-day retest from below. QQQ will be retesting a potential that can be seen dating back to at least late April ’22. DIA is not there yet but is getting closer to its 50sma from below. All three major indices are in an uptrend now having broken the mid-term downtrend lines and working on higher highs and higher lows. However, be careful insofar as price has not put in a higher low or successful retest above those broken lines. Overextension is not an issue in any of the big indices in terms of the T-line (8ema), but T2122 indicates we are a bit stretched according to that indicator. Treasury Sec. Yellen speaks late in the day, but if her remarks are released early, they could impact markets (especially the banking sector). However, it is more likely that if markets are news-driven today it will come from the GDSP, GDP Price Index, and Jobless Claims data at 8:30 am. Be careful not to chase, don’t expect immediate follow-through, and make sure your stops and exits are planned before you enter.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Markets opened just on the red side of flat (down 0.15% in the SPY, down 0.12% in the DIA, and down 0.18% in the QQQ). From that point, we saw a divergence in the three major indices as immediately headed South, continuing its fall until 11 am, when it began to grind sideways along the lows until 1:30 pm. Meanwhile, the SPY meandered sideways from the open until noon, when it began a modest selloff that lasted until 2 pm. For its part, DIA actually rallied from the open until 10:15 am and then ground sideways (to slightly lower) at noon. At that point, it too began a modest selloff that lasted until 2 pm. From 2 pm into the close, all three major indices put in a very steady and modest rally. This action gave us indecisive candles in all three, with the SPY and DIA printing Doji that held above their T-lines and the QQQ printing a black-bodied Hammer candle that also held its T-line.

On the day, eight of the 10 sectors were in the green with Energy (+1.65%) once again leading the way higher while Technology (-0.58%) again lagged behind other sectors. At the same time, the SPY lost 0.22%, the DIA lost 0.15%, and QQQ lost 0.53%. VXX fell almost 3% to 46.64 and T2122 fell back some but remained in the mid-range at 60.24. 10-year bond yields climbed again to 3.571% as money left bonds while Oil (WTI) rose three-quarters of a percent to $73.36 per barrel. So, Tuesday gave us a mixed morning with the three major indices getting in step during the afternoon to basically go nowhere. Indecision abounded is about as much as you can say. This all happened on significantly lower-than-average volume.

In economic news, the February Goods Trade Balance came in just slightly worse than expected at -$91.63 billion (compared to a forecast of -$91.00 billion and a January value of -$91.09 billion). The primary cause for this was a decline in exports as Imports came in increased. At the same time, February Retail Inventories (ex-Auto) rose 0.4%, which was up from the January increase of +0.1%. Later in the morning, the Conference Board Consumer Confidence survey found a more optimistic consumer than had been expected. The reading came in at 104.2, compared to a forecast of 101.0 and a February reading of 103.4. Later, after the close, the API Weekly Crude Oil Stocks Report showed a much greater than expected drawdown of 6.076 million barrels (versus the forecast of an inventory build of 0.187 million barrels and the prior week’s 3.262-million-barrel build).

In stock news, AAPL announced its own “buy now, pay later” program imaginatively name “Pay Later.” The service is enabled through payments made via MA on loans of $50 – $1,000 which are paid in four installments. The main company in that “buy now, pay later” space (AFRM) fell 8% Tuesday on the news. Still, AAPL is not the only company reaching into the loan business as PYPL recently did the same thing. AAPL is not even the only retailer to do so as WMT launched the same type of program in December. Meanwhile, the incoming LYFT CEO Risher (who takes over April 17) said Tuesday that the company is not for sale, which runs contrary to Wall Street expectations. LYFT fell 7.6% on this news. Elsewhere, AMC shares jumped Tuesday on a report stating that AMZN is considering acquiring the theatre chain. At the same time, FCNCA shares hit an all-time high Tuesday in follow-through to the Monday acquisition of SIVB assets at a bargain price. Late in the afternoon, MSFT announced a new cybersecurity product named “Security Co-Pilot” that uses the OpenAI ChatGPT-4 to help identify breaches and potential vulnerabilities by analyzing data. After the close, LCID said it will lay off 18% of its workforce (about 1,300 employees) to cut costs as part of its restructuring plan.

In stock legal and regulatory news, the NHTSA opened an investigation into 50,000 TSLA 2022-2023 Model X vehicles after receiving complaints about seat belt failures. Meanwhile, in Europe, French and German authorities raided the offices of five banks (including HSBC, SCGLY, and BNPQY) over allegations of dividend stripping fraud where the banks and investors quickly trade shares of companies going ex-dividend in order to obscure ownership and allow them to avoid paying taxes on the dividends. (This was just the kind of headlines the banking sector needed, given the recent industry news.) Back on this side of the pond, the US EEOC sued WMT Tuesday claiming it had violated the Americans with Disabilities Act when it fired a North Carolina worker. In Nevada, lawyers for CZR, WYNN, and MGM asked a US judge to dismiss a case that included all the major Las Vegas hotels as well as their software providers and alleged the group was fixing prices on hotel rooms in the city. In Brazil, META and GOOGL defended (themselves and) a Brazilian law in front of that country’s Supreme Court. The law in question is very similar to the infamous Section 230 in the US in that it holds that internet platforms are not responsible for the content posted by their users. After the close, a federal judge ruled in favor of the US Dept. of Justice saying that GOOGL failed to preserve company chat messages related to an antitrust case and that this breach “merits sanctions.” Finally, CNBC reported that DG is in settlement talks with OSHA after the company was labeled a “severe violator” of workplace safety laws.

After the close, LULU, JEF, CALM, and PLAY all reported beats on both the revenue and earnings lines. Meanwhile, MU missed on both the top and bottom lines. It is worth noting that MU lowered its forward guidance after a massive downside earnings surprise (-$2.03/share versus -0.80/share expected). However, LULU raised its own forward guidance.

Overnight, Asian markets were mostly green. Only New Zealand (-0.29%) and Shanghai (-0.16%) were in the red. Meanwhile, Hong Kong (+2.06%), Japan (+1.33%), and Malaysia (+0.80%) led the rest of the region higher. In Europe, we see green across the board at midday. The CAC (+1.24%), DAX (+0.91%), and FTSE (+0.82%) are leading the region higher in early afternoon trade. In the US, as of 7:30 am, the Futures are pointing toward a bullish start to the day. The DIA implies a +0.73% open, the SPY is implying a +0.85% open, and the QQQ implies a +0.84% open at this hour. At the same time, 10-year bond yields are down a bit to 3.558% and Oil (WTI) is up 1.04% to $73.96/barrel in early trading.

The major economic news events scheduled for Wednesday are limited to February Pending Home Sales (10 am) and EIA Weekly Crude Oil Inventories (10:30 am). Fed Vice Chair for Bank Supervision Barr also testifies again at 10 am. The major earnings reports scheduled for the day are limited to CTAS, PAYX, and UNF before the opening bell. Then after the close, CNXC, FUL, and RH report.

In economic news later this week, on Thursday, we get Q4 GDP, Q4 GDP Price Index, Weekly Initial Jobless Claims, and Treasury Sec. Yellen speaks. Finally, on Friday, Feb. PCE Price Index, Feb. Personal Spending, Chicago PMI, and Michigan Consumer Sentiment are reported as well as Fed Member Williams speaking.

In economic news later this week, on Wednesday, Feb. Pending Home Sales and EIA Weekly Crude Oil Inventories are reported. Thursday, we get Q4 GDP, Q4 GDP Price Index, Weekly Initial Jobless Claims, and Treasury Sec. Yellen speaks. Finally, on Friday, Feb. PCE Price Index, Feb. Personal Spending, Chicago PMI, and Michigan Consumer Sentiment are reported as well as Fed Member Williams speaking.

In earnings later this week, on Thursday and Friday, there are no major earnings reports scheduled.

So far this morning, there have been no major reports. UNF is scheduled to report at 8:10 am. Then, CTAS and PAYX are scheduled to report at 8:30 am.

In late-breaking news, the CEO of M, who has been leading the company’s turnaround effort, announced he will retire early next year. Elsewhere, whistleblowers from failed CS reported that prior to its failure, the bank was once again helping rich Americans dodge taxes. (In 2014, CS pleaded guilty to criminal charges for “knowingly and willfully” helping wealthy US clients hide assets offshore to avoid taxes.) The report, released by the US Senate, said the investigation took place over two years and that the illegal activity was still ongoing. CNBC reports that it is unclear at this point how much liability UBS will face for its newly acquired CS having violated its 2014 plea deal or current ongoing efforts to defraud the US government by hiding taxable assets for US clients.

With that background, it looks like the bulls will be gapping markets higher at the open. The SPY is starting to get closer to its 50sma from below and may move for a retest if there is some follow-through to the opening gap. DIA is also retesting the downtrend line stretching back to mid-February in premarket trading. All three of the major indices are above their T-line (8ema). However, overextension is not an issue in any of the big indices, nor does the T2122 indicator look stretched. Again, the economic news scheduled for today is not likely to be market-moving today. With that said, it is possible some news about the banking sector with another day of grilling for regulators (this time from the House) and the story on CS helping Americans cheat on taxes in the headlines this morning. Either way, the market remains very choppy with a bullish lean (over the last couple of weeks but certainly not a longer timeframe) in all three major indices (especially the QQQ).

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

On Monday, markets gapped higher at the open (up 0.60% in the SPY, up 0.69% in the DIA, but up only 0.21% in the QQQ). After 20 minutes of meandering sideways around the opening level, all three major indices began to selloff. DIA pulled back the least, stopping its descent at about 11:20 am. Meanwhile, the SPY reached its lows (at the Friday closing level) shortly after noon. At the same time, QQQ sold off the most reaching its lows at about 12:10 pm. From these lows, the SPY and QQQ have put in a very slow, almost sideways, climb, regaining a fraction of the ground lost during the morning selloff by the highs, which were reached at about 3 pm. For its part, DIA did the same very slow climb but having lost the least was able to regain its opening level. Again, DIA reached its highs of the day just after 3 pm. This action gave us indecisive candles across all three major indices. The SPY printed a black-bodied Spinning Top, the DIA printed a black-bodied Doji, and the QQQ printed a black-bodied Bearish Engulfing Candle with wicks on both ends.

On the day, nine of the 10 sectors were in the green with Energy (+2.33%) leading the way higher while Technology (-0.44%) lagged behind the other sectors. At the same time, the SPY gained 0.19%, the DIA gained 0.65%, and QQQ lost 0.69%. VXX fell more than 3.5% to 47.97 and T2122 climbed up to the top end of the mid-range (just outside of overbought territory) at 76.12. 10-year bond yields spiked to 3.541% on the day while Oil (WTI) skyrocketed 5.43% to $73.02 per barrel. Monday saw a gap higher as banking fears quieted down. However, after the open, action was very indecisive and even leaned bearish (especially in the tech-heavy QQQ that has led the market for some time now). This all happened on lower-than-average volume (much lower in the SPY and QQQ).

In stock news, CRM announced it has reached a deal with activist investor Elliott Management, which will avoid a proxy fight. The move came after CRM disbanded its mergers and acquisitions committee, reported stronger-than-expected results, said it will double buybacks and promised more headcount reductions. Then, at midday, DIS said it will begin the first of three rounds of layoffs (totaling 7,000 job cuts announced in February) this week. Meanwhile, LCID announced it is recalling 637 of its 2022-2023 vehicles due to electrical problems that could result in a loss of power while driving. (LCID delivered only 4,494 vehicles as of the end of last year. So, this is a significant portion of LCID production.) In other electric vehicle news, LICY announced it will open a new facility to break down (recycle Lithium) batteries in France in 2024. The project will be similar to plants LICY already has under construction in Germany and Norway. Meanwhile, CVS said late Monday that it expects to close its $8 billion acquisition of SGFY this week. (This likely means CVS has gotten past antitrust scrutiny and approvals.) Elsewhere, after hours, AMTI cut 57% of its workforce and has begun exploring strategic alternatives. At the same time, PINS announced a restructuring plan which includes the roughly a 4% workforce reduction announced in February. The announced plan includes subleasing leased office space in San Francisco. Finally, the Wall Street Journal reported that LYFT announced it has named David Risher (former AMZN and MSFT executive) as CEO beginning April 17.

In stock legal and regulatory news, RACE hailed a deal, between Germany and the EU, which will allow small-volume manufacturers like RACE to continue producing internal combustion engine vehicles beyond 2035 as long as they can be run on “carbon-neutral e-fuels.” (Exactly what constitutes a “carbon-neutral e-fuel” was not explained.) Elsewhere, the US Supreme Court declined to hear an appeal that was a challenge on US steel import tariffs. This leaves the 25% tariffs on European steel in place and was a loss for DORM and several other Turkish steel importers who were the plaintiffs. Meanwhile, AMZN lost its bid to avoid a class-action consumer lawsuit (damages are estimated between $55 billion and $172 billion) filed by residents of 18 states over pricing policies. Later in the day, it came out that the FDIC will backstop the deal whereby FCNCA will acquire much of SIVB assets. The FDIC will provide FCNCA with a line of credit. At the same time, the former TSLA employee who had their $137 million racial bias verdict reduced by an appeals court has filed suit again rather than accept the $15 million reduced amount. The new trial begins this week. In other legal news, the newly-fired FOX News producer is recanting her testimony supporting FOX in the $1.6 billion defamation case filed against FOX by Dominion Voting Systems. That same former employee filed amended discrimination and retaliation lawsuits against FOX as well.

In cryptocurrency news, COIN is waiting on the filing of a lawsuit and charges by the SEC (claiming the company sold unregistered securities) which were announced via the receipt of a Wells Notice letter last week. However, Binance (the world’s largest cryptocurrency exchange) and its CEO Changpeng Zhao will be the first crypto exchange to be tested by the US government. The US Commodity Futures Trading Commission (CFTC) filed suit against Binance over regulatory violations on Monday. (Binance recently made news when its due diligence prior to a proposed white knight acquisition turned up the fraud and mismanagement at now-defunct FTX.

In energy news, the major cause behind Oil’s huge rise Monday came from a halt to exports from Iraq’s Kurdistan region. Turkey stopped pumping Iraqi oil following its loss of an arbitration case confirming that Bagdad’s approval was required for the shipping of Kurdish oil. This instantly dropped global oil supplies by 450,000 barrels per day. Adding to the pain, Russia was quick to announce “it is close to achieving its goal of cutting production 500,000 barrels per day (down to 9.5 million barrels per day produced).

After the close, PVH and EE reported beats on both the revenue and earnings lines. PVH also raised its forward guidance.

Overnight, Asian markets were mostly green. New Zealand (+1.36%), Hong Kong (+1.11%), and South Korea (+1.07%) led the broad-based rally. Meanwhile, Taiwan (-0.81%), Shenzhen (-0.72%), and India (-0.20%) paced the losses. In Europe, we see a similar picture taking shape at midday with an even split of red and green among the bourses. The CAC (+0.01%), DAX (+0.06%), and FTSE (+0.07%) lead as always on market size. However, Greece (-1.22%), Denmark (-0.39%), and Belgium (-0.36%) pace the losses. On this side of the pond, US Futures are pointing toward a start to the day just on the red side of flat. The DIA implies a -0.02% open, the SPY is implying a -0.10% open, and the QQQ implies a -0.15% open at this hour. At the same time, 10-year bond yields are rising again to 3.568% as money leave bonds early and Oil (WTI) is on the green side of flat at $72.89/barrel in early trading.

The major economic news events scheduled for Tuesday include Feb. Trade Goods Balance and Feb. Retail Inventories (both at 8:30 am), Conference Board Consumer Confidence (10 am), and the API Weekly Crude Oil Stocks report (4:30 pm). Fed Vice Chair for Bank Supervision Barr, FDIC Chair Gruenberg, and Treasury Department Undersecretary Liang are also scheduled to testify to (be grilled by) the House at 10 am. The major earnings reports scheduled for the day are limited to CNM, ESLT, IHS, MKC, SNX, and WBA before the opening bell. Then after the close, CALM, PLAY, JEF, LULU, and MU report.

In economic news later this week, on Wednesday, Feb. Pending Home Sales and EIA Weekly Crude Oil Inventories are reported. Thursday, we get Q4 GDP, Q4 GDP Price Index, Weekly Initial Jobless Claims, and Treasury Sec. Yellen speaks. Finally, on Friday, Feb. PCE Price Index, Feb. Personal Spending, Chicago PMI, and Michigan Consumer Sentiment are reported as well as Fed Member Williams speaking.

In earnings later this week, on Wednesday, we hear from CTAS, PAYX, UNF, CNXC, FUL, and RH. On Thursday and Friday, there are no major earnings reports scheduled.

So far this morning, WBA, MKC, and HIS have reported beats on the revenue and earnings lines. Meanwhile, ESLT beat on revenue while missing on earnings. On the other side, CNM reported inline on revenue while missing on earnings. (SNX reports later in the premarket). It is worth noting that HIS raised its forward guidance.

In late-breaking news, BABA founder Jack Ma returned to China Monday (after more than a year abroad) in what many saw as a potential sign that President Jinping may be softening his stance on the technology sector. Then overnight it was announced that BABA will split into six different business units, each with its own CEO and board as well as its own ability to raise outside funding and go public. Ma will not be CEO of any of the units, but his return to China is perceived as the blessing of the move by the government. BABA shares were up almost 9% in premarket on the news. Elsewhere, Bloomberg reports SCHW has more than $29 billion in unrealized, long-dated bond losses on its books (as of year-end). In addition, the report said higher interest rates are starting to cause its customers to move money out of SCHW and into money-market vehicles.

With that background, it looks like the markets are in a “wait and see” mood this morning. All three of the major indices sit just above their T-line (8ema) with DIA and SPY also sitting just above the 17ema. DIA also sits just atop its 200sma. So, overextension is not an issue in any of the big indices, nor does the T2122 indicator look stretched. The economic news scheduled is not likely to be market-moving today. However, it is possible some news about the banking sector will come from the (mostly political) grilling of regulators by the House today. The market remains very choppy with a bullish lean in the SPY, a full-blown bullish trend in the QQQ, and much more of an undecided feel to the DIA.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Markets gapped down modestly on Friday (down 0.34% in the SPY, down 0.43% in the DIA, and down 0.21% in the QQQ). This came as DB had put a shock into markets globally on default risks. After that open, all three major indices wandered around the open level for 90 minutes. However, about 11:15 am, the bulls stepped in to lead a long, steady rally that lasted the rest of the day, closing very near the highs. This action gave us white-bodied candles with larger lower wicks, including a Hammer in the QQQ. This happened on slightly less than average volume on SPY and QQQ as well as a bit heavier than average volume in the DIA.

On the day, eight of the 10 sectors were in the green with Utilities (+2.83%) leading the way higher while Technology (-0.26%) lagging behind the other sectors. At the same time, the SPY gained 0.64%, the DIA gained 0.44%, and QQQ gained 0.37%. VXX fell more than 4% to 49.74 and T2122 climbed up out of the oversold territory into the mid-range at 31.67. 10-year bond yields dropped again to 3.374% while Oil (WTI) fell 1% to $69.20 per barrel. So, Friday saw a gap down, about 1.5 hours of reconsideration, and then a modest rally that lasted the entire rest of the day.

In economic news, February Durable Goods Orders came in lower than expectations at -1.0% month-on-month (compared to a forecast of +0.6% but far better than the January reading of -5.0%). Later in the morning, Manufacturing PMI was reported to be above the forecast at 49.3 (versus an expected 47.0 and February’s 47.3 value). The Services PMI also beat expectations at 53.8 (compared to a forecast of 50.5 and even compared to the February reading of 50.6). At the same time, the S&P Global Composite PMI also beat expectations with a value of 53.3 (versus the forecast of 47.5 and the February value of 50.1). In Fed talk, St. Louis Fed Pres. Bullard (uber hawk) largely stuck to his guns, telling reporters that the Fed policy rate will likely need to continue rising to higher-than-expected levels once the banking sector stress eases. (Bullard’s terminal rate forecast is a half percent higher than most Fed members at 5.50% – 5.75%.) Later, Richmond Fed President Barkin (also a hawk) told CNN that he had no second thoughts on the Fed’s 25-basis-point hike Wednesday. He went on to say that by the time the FOMC voted, the banking system “felt very stable…So, the conditions were right to do monetary policy the way we want to…” Meanwhile, Atlanta Fed President Bostic (neutral to dovish) told NPR that “There was a lot of debate. This wasn’t a straightforward decision, but at the end of the day, we decided there were clear signs that the banking system is sound…(and) inflation is still too high.”

In stock news, TSLA rolled out version 2.0 of its Full Self-Driving software that makes the feature only available to drivers who achieve a 100/100 safety score (as scored by TSLA sensors and other proprietary factors). In other auto news, F announced its new Tennessee factory (BlueOval City) is scheduled to build 500k electric vehicles per year. This is part of the F plan to be producing 2 million electric vehicles per year by 2026. The BlueOval plant will begin production in the fall of 2025. Elsewhere, the Wall Street Journal reported that MO is considering expansion of its non-nicotine product lines over the next 12 months. At the same time, AAL said it would suspend its Philadelphia to Madrid route for about a month (in May to June) due to delivery delays of BA 787 Dreamliner jets. Over the weekend, according to the Financial Times, the CEOs from PG, PFE, and AAPL are among the very few US-listed company leaders to attend the Chinese Development Forum in Beijing.

In stock legal and regulatory news, late in the day Friday, the US FDA approved a PHAR treatment for weakened immune systems. (PHAR jumped 22% on the news.) Meanwhile, Reuters reported that the US Dept. of Justice (and outside lawyers) are investigating TSN over the antitrust law aspects of its announced closure of a Virginia Chicken processing plant. TSN gave suppliers two months’ notice while antitrust and the Packers and Stockyards Act laws require 90 days’ notice. Elsewhere, FRBK said Friday that it expects to file its annual report with the SEC much later than the March 30 deadline. The bank hopes to report by May 1. The US Dept. of Transportation has rejected an application from JBLU and SAVE that the two be allowed to operate under common ownership. The DOT cited the pending US Dept. of Justice lawsuit seeking to block the acquisition.

Overnight, Asian markets were mixed. Hong Kong (-1.75%) was by far the biggest mover with Taiwan (-0.53%) and Shanghai (-0.44%) rounding out the group that paced the losers. Meanwhile, Singapore (+0.82%), Japan (+0.33%), and New Zealand (+0.28%) led the gainers. However, in Europe, the bourses are strongly green across the board at midday. The DAX (+1.40%), CAC (+1.17%), and FTSE (+0.98%) are leading the region higher in early afternoon trade. As of 7:45 am, US Futures are pointing toward a gap higher to start the day. The DIA implies a +0.66% open, the SPY is implying a +0.67% open, and the QQQ implies a +0.39% open at this hour. At the same time, 10-year bond yields are higher to 3.466% and Oil (WTI) is up 1.3% to $70.15/barrel in early trading.

There are no major economic news events scheduled for Monday. The major earnings reports scheduled for the day are limited to BTNX and CCL before the opening bell. Then after the close, PVH reports.

In economic news later this week, on Tuesday, we get Feb. Trade Goods Balance, Feb. Retail Inventories, Conf. Board Consumer Confidence, and the API Weekly Crude Oil Stocks report. Then Wednesday, Feb. Pending Home Sales and EIA Weekly Crude Oil Inventories are reported. Thursday, we get Q4 GDP, Q4 GDP Price Index, Weekly Initial Jobless Claims, and Treasury Sec. Yellen speaks. Finally, on Friday, Feb. PCE Price Index, Feb. Personal Spending, Chicago PMI, and Michigan Consumer Sentiment are reported as well as Fed Member Williams speaking.

In earnings later this week, on Tuesday, CNM, ESLT, IHS, MKC, SNX, WBA, CALM, PLAY, JEF, LULU, and MU report. Then Wednesday, we hear from CTAS, PAYX, UNF, CNXC, FUL, and RH. On Thursday and Friday, there are no major earnings reports scheduled.

In late-breaking news, the fallout from the banking crisis continues. In the US, FCNCA announced it has reached a deal to acquire the deposits and loans of SIVB from the FDIC. The deal includes $72 billion in assets acquired at a discounted price of $16.5 billion. In Europe, the top managers of CS are facing an investigation and potential disciplinary action from the Swiss Banking Regulator. Meanwhile, in the Persian Gulf, the head of the Saudi National Bank (whose public refusal to buy more of CS caused that bank’s depositor run) has resigned “for personal reasons.” Elsewhere, the UAW has elected a reformer as union President. This may mean trouble for automakers as the new President ran on promises to take tougher negotiating stances in upcoming negotiations.

With that background, it looks like the bulls are going to gap the major indices (large caps) back up above their T-line (8ema). The DIA will also be retesting its 200sma from below at the open. Overextension from the T-line is not an issue in any of the big indices, nor is the T2122 which is back in its mid-range. With no economic news scheduled, the FOMC decision off the table, and banking problems somewhat subsiding, I suspect that the bulls will have a little room to run this morning. This doesn’t necessarily mean any market trend change. It just means the bulls have momentum in the premarket and there is no known obstacle to them stretching their legs in the short-term.

As always, be deliberate and disciplined…but don’t be stubborn. If you have a loss, admit you were wrong and take that loss before it gets out of hand. And when the price does move in your direction, always move your stops in your favor and take a little profit off the table. You have to keep the “Legend of the man in the green bathrobe” in mind. In a winning situation, it is NOT HOUSE MONEY you’re betting, it’s YOUR MONEY! There is absolutely no reason to keep raising your bet (risk) size just because you’ve had a win. Finally, remember that trading is not a hobby. It’s a job. The money is real and so is the risk. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Do the work!

See you in the trading room.

Ed

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

On Thursday, markets gapped higher to differing degrees (up 0.74% in the SPY, up only 0.37% in the DIA, and up 1.24% in the QQQ). All three major indices then went on a bullish run, reaching the highs of the day at about 11:10 am. However, then the bears took over selling off the SPY, DIA and QQQ at an increasing tempo that reached the lows of the day at 3 pm. The last hour saw a volatile bounce up off the lows that took all three back up to the opening level by the close. This action gave us gap-up indecisive candles (Doji in the QQQ and DIA as well as a black-bodied Spinning Top in the SPY). This happened on greater-than-average volume in all three of the indices.

On the day, six of the 10 sectors were in the red with Energy (-1.51%) leading the way lower while Technology (+1.50%) fairing much better than the other sectors. At the same time, the SPY gained 0.26%, the DIA gained 0.21%, and QQQ gained 1.19%. VXX climbed 2.67% to 51.89 and T2122 remained well into the oversold territory at 7.94. 10-year bond yields dropped again to 3.412% while Oil (WTI) fell 2.3% to $69.26 per barrel. So, Thursday saw a major divergence with much money chasing the safety of bonds while at the other end of the spectrum high tech names like NFLX, MU, MRVL, and others leading the QQQ higher.