DJIA Shakeup and New Fed Direction

Markets gapped higher on follow-through to last week’s rally. While there was some roller-coaster, markets essentially stayed where they gapped, closing near the highs. Once again, the SPY and QQQ both closed at new all-time highs. That said, the SPY and DIA could be seen as “gap up Hanging Man” candles, but we know that without follow-through candle signals mean nothing. Price gets the only vote that counts. On the day, SPY was up 1.01%, DIA up 1.39%, and QQQ up 0.62%. The VXX fell slightly to 24.52 and T2122 rose back near the overbought territory at 78.68. 10-year bond yields rose slightly to 0.656%, while Oil (WTI) was flat at $42.42/barrel.

After the close, CNBC reported that Fed Chair Powell’s Thursday video speech (virtual Jackson Hole Symposium) is expected to be historic. They say Powell will reverse the long-standing Fed inflation policy that goes back to former Chair Volcker’s policies to fight high inflation in the early 1980s. This speech is expected to outline a new policy designed to encourage inflation to “overshoot” (above the target rate of 2%) instead of trying to halt it at 2 percent. The idea appears to be they will look to hit the target level “on average.” This is all designed to emphasize full employment as the guide versus trying to meet dual mandates (employment and inflation) and is seen as an effort to jump start recovery. This will have the effect of forcing risk-seeking, which should point to a continued stock market rally.

In a major shakeup, 3 new companies were added to the Dow Jones “Industrial” Average last night. The new companies AMGN, CRM, and HON. Those 3 will replace PFE, XOM, and RTX. The XOM and PFE removals were a major unexpected move.

On the virus front, in the US, the numbers show we now have 5,915,911 confirmed cases and 181,117 deaths. The good news is that new cases continued their recent trend down from the July highs. However, the 7-day averages remain stubbornly above 43,300 new cases and 980 deaths per day.

Globally, the numbers rose to 23,836,657 confirmed cases and 817,606 deaths. Hong Kong reported a first case of reinfection (with 4 months between them). It appears the 33-year-old man was infected with two different strains of the virus. In Europe, France announced an increase in Covid-19 cases as Germany put both Paris and the French Riviera region on a travel warning. Meanwhile Spain tightened its restrictions again as cases rise. (All these European rises should be kept in context. Even combined, the number of new cases in Europe is dwarfed by those in the US.)

Overnight, Asian markets were mixed, but leaned heavily to the upside. Japan and South Korea led gainers. In Europe this morning again only Athens shows red. However, the bulls have not made a huge move either yet as the bourses all about +0.50% as of mid-day. In the US, at 6:30 am, the futures are pointing to a modestly higher open, with only the DIA looking at a +0.50% gap on the shakeup.

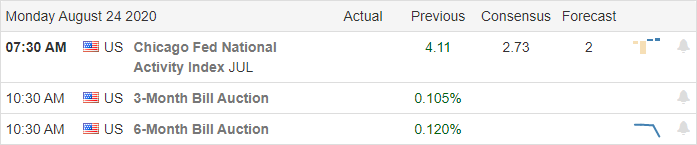

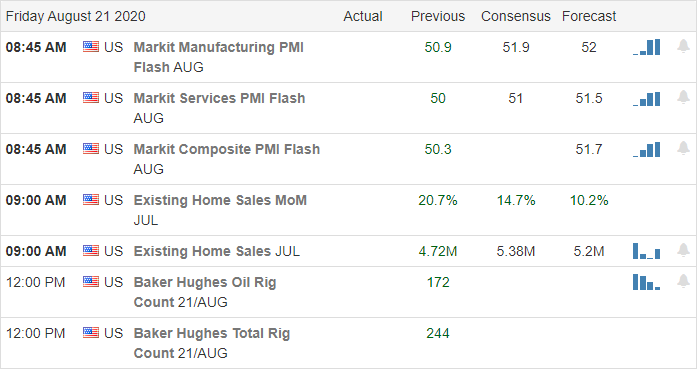

The major economic news for Tuesday is limited to Conf. Board Consumer Confidence and New Home Sales (both at 10 am) and a Fed Speaker (Daly at 3:25 pm). However, Tropical Storm Marco will be onshore with Hurricane Laura following soon. Major earnings reports on the day include BBY, BMO, BNS, HRL, MDT, and SJM before the open. Then after the close, ADSK, CRM, HPE, INTU, JWN, TOL, and URBN report.

Sorry folks but I am under the weather. This will have to suffice until tomorrow.

Ed

The Daily Swing Trade Ideas for today: . Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service