The bears overwhelmed the market worried about political infighting over a high court appointment, a possible government shutdown, a delayed or no 2nd stimulus package, an upcoming election, and rising coronavirus concerns. Even though the bulls fought back, leaving behind some hopeful candle patterns that a relief rally may soon begin, the market downtrend and substantial resistance levels above provide concern that the overall downtrend may not be over just yet.

Asian markets chopped in an uncertain session with rising pandemic concerns. European markets have found a bit more bullishness this morning, getting a modest relief rally after yesterday’s rout. US Futures at the time of writing this report suggest a mixed but relatively flat open with tech doing its best to lead a relief. Expect price volatility to remain high with the market sensitive to the news cycle.

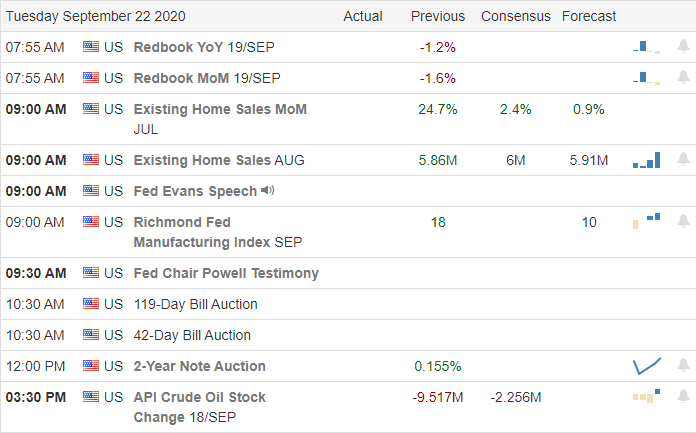

Economic Calendar

Earnings Calendar

On the Tuesday earnings calendar, we have 12 companies reporting quarterly results. Notable reports include NKE, AZO, KBH, SCS, & SFIX.

News and Technicals’

Worries about political infighting over a high court appointment, a possible government shutdown, a delayed or no 2nd stimulus package, an upcoming election, and rising coronavirus concerns had the bears working hard yesterday. The first 4-day string of selling since February has created technical damage and damaged to trader confidence in the path ahead. According to the T2122 indicator, the indexes are in a short-term oversold condition suggesting a relief rally may begin soon but having broken down below the 50-day averages and price support, the resistance above could stop any bullish attempt. Should we see a failure at or near the 5-day average, we can’t rule out the possibility of a 200-day average test in the weeks ahead. We should also consider the chance that we have seen the highs for the year, and the market could settle into a volatile sideways consolidation.

Technically speaking, the rally off of yesterday lows left behind hopeful candle patterns that a relief rally could soon begin. However, with the DIA, SPY, QQQ all below substantial resistance levels, a one day bounce while in a downtrend is nowhere near an all-clear signal to buy the dip. With so much uncertainty ahead, expect extreme sensitivity to the news cycle, overnight reversals, intraday head-fakes, and whipsaws, making price action very challenging to navigate. The silver lining in all of this is that stocks are on sale, and eventually, there will be some bargains when this is over.

Monday saw a brutal gap down on virus concerns, another big bank scandal, and the political news related to the replacement (or not) of Justice Bader-Ginsberg. Volatility continued all day with a later afternoon rally driving price back up into the gap. The result as a strong white candle (if you look past the gap down) in the QQQ, but big indecision in the DIA and a white Hammer in the SPY. On the day, QQQ gained 0.24%, SPY lost 1.04%, and DIA lost 1.84%. Oddly, VXX did not shoot higher, rising only to 25.16, but T2122 sank clear to the bottom of the oversold range at 2.28. 10-year bond yields fell to 0.672% and Oil (WTI) also fell 3.5% to $39.65/barrel.

During the day House Speaker Pelosi proposed the Democratic bill for additional stopgap funding to keep the government running past the September 30 deadline. However, Senate Majority Leader McConnell immediately criticized the bill because it did not contain the additional money for farm aid that the President wanted added. To be fair, many things were not in the bill, including extra funding for the Democrat favorite food assistance program. It was not mentioned, but another fundamental difference between the sides is that Republicans want the bill to include funding through January 2021 (when the next Congress is seated) while Democrats want funding only through the election. In this case, the Democratic bill offered a compromise of funding through December 20.

In the pre-release of Fed Chair Powell’s testimony for today he says “Many economic indicators show economic indicators show marked improvement…Both employment and overall economic activity, however, remain well below their pre-pandemic levels, and the path ahead continues to be highly uncertain,” He goes on to push for more virus control and stimulus as he also says “The path forward will depend on keeping the virus under control, and on policy actions taken at all levels of government.” Both he and Treasury Sec. Mnuchin are likely to face questions on the massively unused Fed Main Street Loan program (which stimulus legislation cannot be forgiven) as opposed to the PPP loan program many expect to be forgiven.

On the virus front, in the US, the numbers show we now have 7,046,444 confirmed cases and 204,515 deaths. The 7-day average of new cases is rising again, now over 41,000 per day. However, deaths dropped dramatically for some unknown reason to just 388 on Monday. This dropped the average to just under 800/day. Republicans in the Senate proposed $28 billion in aid for the airline industry ($3 billion more than asked) in an attempt to stave off 30,000 job cuts now planned in two weeks. This is likely a DOA proposal since the two parties have not agreed to an overall stimulus plan.

Globally, the numbers rose to 31,517,736 confirmed cases and 970,077 deaths. In the UK, there were ominous signs Monday. The country’s 2 top scientists addressed a presser where they said the UK is back to 10,000 new cases per day in a growth rate that may send them to 50,000/day by mid-October unless the spread is arrested (implied as a new national lock-down). The government then raised the alert level to 4 (transmission if high or rising exponentially). Level 5 is another national lockdown. PM Johnson is set to address an emergency meeting, Parliament, and the Public Tuesday where many expect additional measures to be announced. (JPM says that if another 2-week lockdown were to happen, it would knock another 2% off the UK’s 2020 GDP.) Elsewhere in Europe, Spain has reentered partial national lockdown (and full lockdown in Madrid) and France cases continue to spike in various cities

Overnight, Asian markets were mostly in the red again. Japan eked out a small gain while New Zealand and Malaysia managed slightly better, but still modest gains. However, China, Taiwan, and Hong Kong were all down over 1% and South Korea lost 2.4% on the day. In Europe, the picture is brighter as we find modest green numbers across the board as of mid-day. Again today, the DAX leads the way, up just under 1% so far. As of 7:30 am, US futures are mixed. The Large-Caps are on either side of flat, but the NASDAQ is pointing to a half-percent gap higher at the open.

The major economic news for Tuesday is limited to August Existing Home Sales (10 am) and, as mentioned, Fed Chair Powell testifies (10:30 am). On the earnings front, the only major announcements scheduled are AZO before the open and KBH and NKE after the close.

Markets may be looking to bounce back from Monday’s ugly start to the week. Possibly Fed Chair Powell’s soothing talk of “more stimulus as long as it’s needed” will do the trick. However, no more progress on the fiscal stimulus side and political rancor will not help. News of the expansion of virus-fighting measures in the UK (and the rest of Europe) is also going to be a damper.

Remember that we’ve seen “gap and fade” or “gap and indecision” for some time. So, be careful chasing unless you are fast or can take the heat. Follow the trend, which is clearly bearish now, don’t think you can pick bottoms, but also don’t chase moves that have gotten away. Stick to your rules, keep locking-in profits, and remember trading is a job for the long-haul…not a get rich quick scheme.

Ed

Swing Trade Ideas for your Consideration and Watchlist: PENN, NVTA, DDOG, FDX, PGR, LH, TGT, CZR, WHR, DGX, FSLY. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

A political battle royal has begun for the appointment of a Supreme Court Justice, and the aftershocks are creating market havoc this morning with the US Futures pointing to an ugly gap down open. The morning selling will make the lower low to confirm the downtrend in the DIA, SPY & QQQ. There is also significant pressure in the financial sector after leaked documents that show red-flagged transactions that amount to more than $2 trillion. Today could be a very painful day for the buy the dip buyers that loaded up on trades last week. Be careful as fear and possible margin calls could accelerate the selloff.

Asian markets closed mixed but mostly lower after the report that HSBC moved most of the suspicious money flagged in the leaked report. European markets are decidedly bearish this morning, with indexes trading more than 3% lower this morning. US Futures also point to a painful open that will create substantial damage to trader confidence and technical damage in the index charts. Prepare for a wild ride!

Economic Calendar

Earnings Calendar

On the Monday earnings calendar, we have 18 companies stepping up to report quarterly results, but there are not any particularly notable.

News & Technicals’

It seems the appointment of a new Supreme court justice will become a distraction political battle royal and possibly pulling attention away from completing an additional stimulus package. It’s such a hot topic that candidates received a record 90 million in campaign contributions as it fired up both political bases. Nancy Pelosi has gone as far as to threaten impeachment proceedings in an attempt to block a Trump appointment. This morning’s futures market sums up the intensity of the distraction, with Dow currently expecting a gap down of more than 500 points. According to reports, the President approved the Tiktok deal, and China has responded, saying they will blacklist some US tech firms raising uncertainty for foreign tech business. Leaked US government documents show that several big banks may have moved elicit funds. Germany’s largest bank, Deutsche Bank, tops the list and appears to have facilitated the more of the $2 trillion in suspicious transactions flagged by the US Government. JP Morgan is second on the list. Both banks indicate lower this morning, putting additional pressure on the markets.

The question of whether the 50-day morning average of the Dow holding as price support has been answered this morning with a punishing gap down at the open. The lower low not confirms the downtrend of the DIA, SPY, and QQQ and creates substantial technical damage in the charts. I would not be at all surprised to hear about margin calls that have the potential to accelerate the selling. Today may prove to be one of those awful market days that test a trader’s tolerance to risk. Buckle up for a wild ride.

Markets saw a minor gap down Friday, but it was immediately followed up by a strong selloff that lasted until 1:30 pm. However, the bears called a week at that point and the bulls put in a relief rally into the close. On the day we still saw ugly black candles that failed the 50sma, including a Bearish Engulfing in the QQQ. At the close, DIA was down 1.09%, SPY down 1.55%, and QQQ down 1.28%. The VXX was flat at 24.37 and T2122 fell back to 34.91. 10-year bond yields were up slightly to 0.697% and Oil (WTI) was flat on the day at $40.98/barrel. This culminated a 3rd consecutive down week, in volatile trading.

On Saturday President Trump approved the ORCL / WMT and Byte Dance deal but did so while saying it includes a $5 billion fund to pay for an educational project. Byte Dance announced they were unaware that any such fund was part of the deal. So, that part of the announcement appears to be more gamesmanship by the President. The deal will also still need the approval of the Chinese government. However, Monday a Chinese state-backed media outlet called the deal “unfair but reasonable” in a possible preview of the official reaction.

To give that deal time to reach approvals, the President did extend the deadline for a ban on TikTok until next week. However, on Sunday a Federal judge blocked the Administration ban of TikTok and WeChat altogether. (Although a long back-and-forth legal battle is expected up through the tiers of courts.) So, momentarily it appeared that ORCL and WMT had gotten what they wanted (a toehold in the Social Media space) and they still may. However, that clarity was quickly replaced in favor of more political and legal limbo.

The big US banks are reportedly back in hot water (and reacting in pre-market). US Government files were leaked this morning showing that at least JPM and BK, had joined Germany’s Deutsche Bank and the UK’s Standard Chartered to launder $2 trillion in illicit funds over nearly 2 decades.

On the virus front, in the US, the numbers show we now have 7,004,990 confirmed cases and 204,118 deaths. The 7-day average of new cases is rising again at 41,330 per day. However, the average for deaths (which lags) is still trending down at 800 per day. Meanwhile, on Friday, the CDC reversed its caving to political pressure and changed its guidance for asymptomatic individuals. The new guidance says that anyone who is exposed to an infected person needs a be tested, regardless of whether or not they show symptoms. Bloomberg reported that this change was planned earlier, but delayed by a long “review and approval” by Administration outside the CDC. On Sunday we learned that 31 states have more new cases this week than last and 25 of those states have a higher test result positivity than the previous week. The fear is that this is another example of a holiday-caused surge as too many Americans ignore guidelines or have relaxed their adherence

Globally, the numbers rose to 31,263,651 confirmed cases and 965,398 deaths. Even with the new lock-down in the Northeast of their country, UK cases are rising. Sunday talk was that London is the next potential “local” mini-lockdown (2 weeks) as the Mayor met with the City Council in private session Sunday while UK PM Johnson is expected to address the country again as soon as Tuesday. In Germany, mandatory mask use has been reintroduced in areas (Munich region). Elsewhere, the recent Australian whole state lockdown has been vindicated as restrictions are beginning to ease and the new case count has dropped by a factor of 60.

Overnight, Asian markets were back to being mixed, but the largest economies leaned positive. China was up 1.5-2%, while Japan and South Korea were on the green side of flat. Europe has seen a similar situation so far this morning. However, European moves have been more modest and lean more to the red side at this point. The FTSE and CAC are on the red side of flat while the DAX is up a third of a percent at mid-day. As of 7:30 am, US futures are mixed with the large-caps split modestly on either side of break-even and the NASDAQ pointing toward a half percent gap higher.

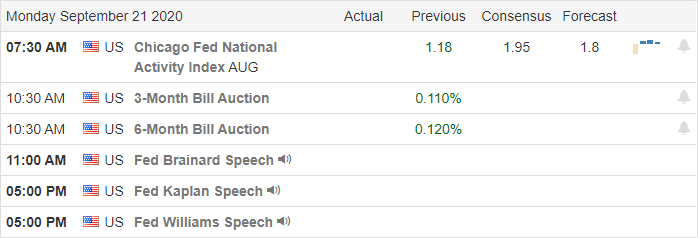

The major economic news for Monday is limited to 3 Fed speakers (Chair Powell at 10 am, Brainard at noon, Williams at 2 pm). Once again there are no major earnings reports on the day.

Coming off the first 3-week losing streak since March, markets look set to gap lower at the open Monday. However, “gap and rebound” volatility has been the norm in volatile markets recently. So, be careful, but, as always, stick to your plans. Follow the trend, but don’t chase moves you have missed. (There is always another trade coming soon…no need to suffer FOMO.) Hang in there with your rules and keep locking-in profits.

Ed

Swing Trade ideas for your Consideration and Watchlist: No trade ideas for Monday. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

There was considerable price movement yesterday as the bulls and bears battled for control with MSFT and AAPL leading the QQQ its first close below its 50-day average since April. With the weekend approaching, a light day of earnings and economic news, as well as September options expiration, expect price volatility to continue. Plan your risk carefully as you consider the uncertainty of the weekend ahead.

Asian markets seesawed overnight but ultimately find the inspiration to rally, closing green across the board. With a significant spike in coronavirus and new shutdown measures taking place, European markets trade cautiously mixed but mostly lower this morning. US Futures traders flat to mostly lower overnight, but as the morning pump begins, they have rallied off overnight lows with the tech sector leading the way.

Economic Calendar

Earnings Calendar

On the Friday earnings calendar, we have a very light day with just one company expected to report today. That stock is TC and not at all notable unless you happen to one the sub-$1.00 equity.

News & Technicals’

With MSFT and AAPL under selling pressure, the indexes struggled yesterday with punishing intra-day whipsaws that kept traders on edge. The QQQ attempted to recover its 50-day moving average but ended the day closing below this psychological support. With US Futures mixed this morning, it’s understandable that there may be a little apprehension as we slide into the uncertainty of the weekend. Today is the last day trading for September options, so as traders unwind positions would may see and an extra dose of price volatility. Should the bears find the inspiration to rally, keep the resistance above with the downtrend created by this week’s lower high. Head fakes and intra-day are pretty common on options expiration day, and with the VIX still hovering above a 26 handle, traders must prepare for anything.

With just one small-cap stock reporting and a light day on the economic calendar, there won’t be much to react to except election news and political spin. I would not be at all surprised to see a choppy consolidation day. I wish you all a profitable Friday and a Fantastic Weekend!

Thursday saw a strong gap lower (about 1.6%). This was met with a strong rally that faded most of that gap by 11:15 am, but then the bears stepped back in and sold back off back to the lows by 12:30 pm. The rest of the day was smaller waves in the roller coaster ride. The 50sma held as support in the SPY, but the QQQ has given up the 50sma and the DIA has not reached it yet. On the day, QQQ lost 1.56%, SPY lost 0.87%, and DIA lost 0.52%. All closed up off the lows, but far from the highs as well. The VXX closed down again to 24.38 and T2122 was back down to 46.63. 10-year bond yields were up slightly to 0.689% and Oil (WTI) rose again to $41.04/barrel.

White House Chief of Staff Meadows met with Airline executives during the day and after the meeting told the press that the President supports $25 billion of “narrow” relief for the industry. (The industry, led by UAL, AAL, and unions have been seeking that amount in additional relief funds for the last month or so. The threat has been that if they cannot get the additional bailout funds, on top of the recent buyouts, retirements and furloughs, a major wave of new layoffs would come as soon as this fall.) No word on plans to execute on a bailout or of specific legislation offered. However, they did get the President’s public support of the additional $25 billion (although it did not come directly from the President and the term “narrow” was not defined).

After the close, the Fed announced it will decide by the end of the month if it will continue capping Big Bank dividends. (For reference WFC was one of the big banks to reduce dividends when the cap was announced in June.) This news comes as another stress test will be started soon. However, in a change from the previous protocol, this time around the Fed says it will publish company-specific stress findings for each of the 34 institutions it tests. The Fed announcement went on to outline two severe recession scenarios it will use in the stress testing of reserves this time around.

On Thursday ORCL and Byte Dance both agreed to a Treasury Dept. change of terms for their partnership deal. The changes were aimed at heading off the White House national security concerns (oddly that Byte Dance cannot access to user-tracking information the same way that AMZN, GOOG, AAPL, FB, MSFT, other App makers and every Internet Service Provider already use and track the same customer usage/tracking data). The two other main provisions are ORCL getting complete access to TikTok source code and the entire board of the new company being made up of American citizens regardless of new the company being a foreign entity or what the ownership shares will be. In a potential twist, WMT is now expected to partner with ORCL on the deal. (In last-second news, it was just announced the White House will block downloads of TikTok and WeChat as of Sunday. No word on the approval/disapproval of the Treasury-revised deal.)

On the virus front, in the US, the numbers show we now have 6,875,103 confirmed cases and 202,219 deaths. We saw another uptick to 46,295 new cases (well above the 7-day average), but new deaths dropped off a bit to 879 (still just above the 7-day average). In good news, TX moved forward to the next step in their reopening. They now allow all retail stores, office buildings, restaurants, factories, gyms, and museums to reopen immediately at 75% capacity as long as the hospitals in their region stay below capacity thresholds.

Globally, the numbers rose to 30,380,035 confirmed cases and 951,150 deaths. In the UK, the Northeast region of England has re-entered lockdown in an effort to stop a new surge in cases. Other areas of the country are implementing partial measures such as limiting gatherings to single-family and stopping counter restaurant and bar service (so-called table service only). This comes as testing demand is over 1 million per day, but capacity is only 230,000 tests/day. In Parliament, Government Ministers blamed the public for the problem, saying that only people told by a health professional should attempt to be tested.

Overnight, Asian markets were back to being mixed, but the largest economies leaned positive. China was up 1.5-2%, while Japan and South Korea were on the green side of flat. Europe has seen a similar situation so far this morning. However, European moves have been more modest and lean more to the red side at this point. The FTSE and CAC are on the red side of flat while the DAX is up a third of a percent at mid-day. As of 7:30 am, US futures are mixed with the large-caps split modestly on either side of break-even and the NASDAQ pointing toward a half percent gap higher.

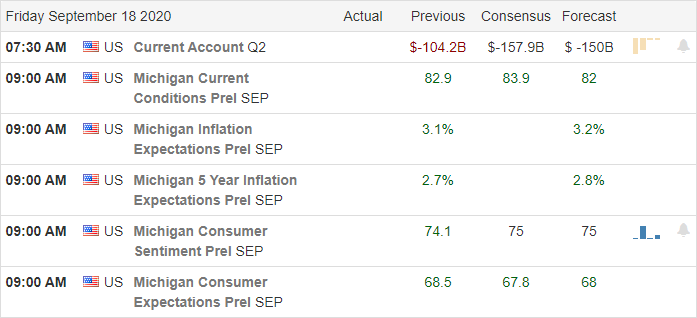

The major economic news for Friday is limited to Michigan Consumer Sentiment (10 am). Once again there are no major earnings reports on the day. However, this is Options Expiration Friday.

Gap and fade or indecision seems to be the standard operating procedure in markets recently. So, be careful of volatility. Also, don’t get caught off-guard by any pinning related to options expiration today. (There are a lot of inexperienced options traders out there right now that Mr. Market has to introduce to the pinning trick.) As always, stick to your plans, follow the trend, and don’t chase moves you have missed. (There is always another trade coming soon…no need to suffer FOMO.) Hang in there with your rules and keep locking-in profits. Also remember that Friday is payday. So, take a paycheck and consider whether you want to lighten up or hedge going into the weekend news cycles.

Ed

Swing Trade ideas for your Consideration and Watchlist: NIO, DOW, DFS, GPC, COF, MMM, KSS, TRUE. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

The celebration of the FOMC’s commitment to hold rates at historic lows for years lasted about an hour before the bears reemerged, seemly gaining the upper hand by the close. The price action left behind some troubling candle patterns and set the stage for possible index lower highs at price resistance. With futures pointing to a nasty gap down open, the question now is, will recent lows and the 50-day moving averages hold as support?

Asian markets closed in the red across the board overnight. European markets are also decidedly bearish this morning despite the Bank of England’s’ decision to keep rates low. Ahead of potentially market-moving economic reports, US Futures point to a substantial gap down at the open. Expect another wildly volatile day.

Economic Calendar

Earnings Calendar

On the Thursday earnings calendar, we have a light day with less than 10 confirmed reports. Notable reports include APOG & CMD.

News & Technicals’

After the FOMC committed to keeping interest rates at historic lows, we experienced a nasty intraday reversal with the bears surging into the close. During the Jerome Powells press conference, he noted that the economy looking forward remains uncertain and may take an extended time for employment to recover. Snowflake, ticker (SNOW) doubled yesterday to become the most significant software IPO in market history. The shares priced at $120 per share for the initial offering soared to over $253 in yesterday’s trading. OPEC and its allies are meeting today to discuss production limits. Analysts at this time don’t believe there will further production cuts but do expect the then to renew their commitment to the deep cuts they’ve already made.

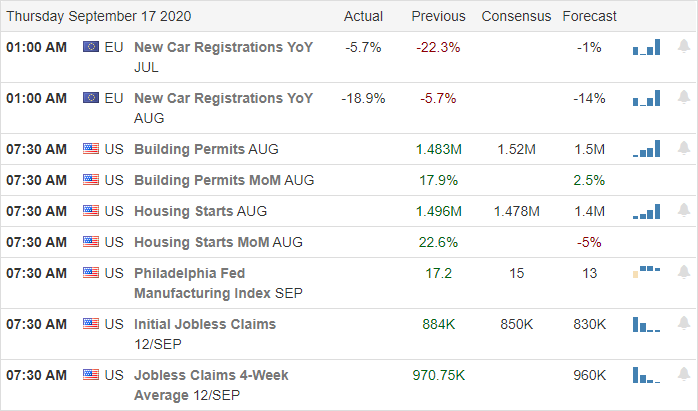

The last hour selloff in the indexes left behind some worrisome candle patterns at or very near price resistance levels, possibly setting the stage for lower high price patterns. Early rallies in the financial and oil sectors struggled to hold onto gains as the bears once again seem to gain the upper hand. Unfortunately, the US Futures currently point to a substantial gap down this morning. A painful reminder that buying stocks near price resistance levels is a practice that retail traders should avoid. The question to be answered now is whether the recent lows at or near the 50-day moving averages will hold as price support or will an official downtrend be established? Today we have a light day on the earnings calendar, but before the bell, we will get the latest reading on Housing Starts, Jobless Claims, and the Philly Fed MFG Index. Prepare for another volatile day.

Wednesday saw another gap higher (about 3 or 4 tenths of a percent) in spite of an August Retail Sales number that missed estimates by 40%. The roller coaster ride followed with the climax being a strong rally at 2pm (after the Fed said interest rates will remains near zero for at least 3 years) and an even stronger selloff at 3pm. On the day SPY was down 0.38%, DIA up 0.16%, and QQQ down 1.59% as the techs continued to get hammered. This gave us big bearish candles in the QQQ and SPY as well as an ugly high wick in the DIA. Oddly enough VXX also fell on the day, ending at 24.96 and T2122 climbed to 71.71. 10-year bond yield rose slightly to 0.697% and Oil (WTI) was up over 5% to $40.24/barrel.

As mentioned, the big news on the day was the Fed confirming what individual Fed voters have been saying for quite some time. The FOMC will hold rates essentially at zero percent for years to come, specifically at least through 2023. Nonetheless, they also improved their GDP forecast to a 3.7% contraction (when the last forecast was for a 6% contraction as recently as June). However, on the other side, they also reduced the 2021 GDP forecast from 5% growth to 4% growth. Chair Powell also said the Fed is working on changes to the Main Street Lending Program (which has been a flop with less than one-quarter of one percent of available funds being requested as loans as of now) to make it more widely accessed.

President Trump took a step back from his former position and called on the GOP to support a much larger stimulus package than either the Administration or the Senate Republicans had previously said they would accept. He didn’t mention a specific amount, but White House Chief of Staff Meadows later told the press that $1.5 trillion could be acceptable. (This number is halfway between the Republicans original $1 trillion and the Democrats most recent offer of $2 trillion. However, it’s a full trillion dollars over what Senate Republicans had wanted in their “Skinny Bill” as late as last week.) Both Meadows and House Speaker Pelosi said they are more hopeful of a deal now than they have been in 3 months. Senate Majority Leader McConnell refused to comment. For his part Fed Chair Powell reiterated that he still feels more fiscal support is likely needed with 11 million people out of work, small businesses struggling and local government revenues having dropped. In an unrelated story, House Republicans are moving to force a vote to re-issue the $138 billion of PPP program funds that went unrequested from the last stimulus bill. It’s unclear if there would be more demand now than earlier, but it is a sound political move and the market loves stimulus whether real or paper.

As for the ORCL- Byte Dance partnership deal for TikTok US operations, both Sec. of State Pompeo and President Trump said they don’t like what they have heard. While not an outright disapproval of the deal, it cannot be seen as a positive thing with just 3 days remaining until the White House-imposed deadline. On the positive side, the President did admit that he has given up on the government “getting a lot of money” for forcing the deal (government lawyers have explained to him that is not legal). Still, that was never a real obstacle to a deal. The crux of the issue is that the White House insists on a sale of the business and its technology assets while China has said it will not allow the sale of the technology (search and user interest tracking algorithms, etc.). On top of that, apparently no suitor has offered what Byte Dance feels is fair compensation for the entire business (the Oracle deal would leave Byte Dance with majority ownership in the new shell company).

On the virus front, in the US, the numbers show we now have 6,828,698 confirmed cases and 201,366 deaths. We saw another uptick to 40,154 new cases and 1,151 deaths. On Wednesday CDC Director Redfield told a Senate committee that masks are the most important tool we have and may well be more effective than a vaccine. In the same testimony, he said most people will not be able to access a vaccine until mid-2021 and the process would take 6-9 months to get enough people vaccinated twice to provide community herd immunity. (Beyond the supply issues, another hurdle will be the public. Two days ago, a non-partisan 1,200 respondent Kaiser Foundation poll found that only 42% of Americans will get vaccinated even when it is available.) In a different hearing, Dr. Fauci (NIH) told House lawmakers that while October data is theoretically possible, he expects data about the efficacy and safety of the early vaccine candidates to become available in November or December. (Oddly, he also said that US phase 3 trials are still only about two-thirds enrolled with approved healthy participants at this point.) However, as he often does, President Trump told reporters that the experts were wrong, large-scale vaccine distribution will begin about mid-October and 100 million vaccine doses will have already been distributed in the US by year-end.

Globally, the numbers rose to 30,073,744 confirmed cases and 945,817 deaths. The WHO came out against “Covid-19 passports” (passports that would allow test-free and quarantine-free travel for people with antibodies), because there are no studies on how universal immunity would be or how long immunity lasts. The renewed spread in Europe continues, but that is dwarfed by India, which reported a record high of 97,800 new cases today.

Overnight, Asian markets were red across the board, with the lone exception of Shenzhen which managed +0.08%. The biggest losers were Hong Kong, South Korea, and Australia which were all down over 1.2%. Europe has followed Asia so far today with red across the board. However, only the Netherlands is down more than a percent as of 7:30am. Speaking of that time, as of then the US futures are pointing to a gap lower. The Nasdaq implies a gap down of 1.63%, the SPY a dap down of 1.13%, and the DIA a gap down of 0.81%.

The major economic news for Thursday includes August Building Permits, August Housing Starts, Weekly Initial Jobless Claims, and Philly Fed Mfg. Index (all at 8:30 am). However, once again there are no major earnings reports on the day.

Be careful of volatility with gap and reverse being the norm recently in the mornings. Stick to your plans. Follow the trend and don’t chase moves you have missed…there will be another one soon. Hang in there with your rules and keep locking-in profits. Remember, trading is a job, not a lottery ticket.

Ed

Swing Trade ideas for your Consideration and Watchlist: TRUE, COF, MDB, MKC, HLT, ADSK, MMM, WFC, PYPL, AXP. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Yesterday ended with a mixed bag on index results heading into a big day of economic data that includes an FOMC statement and the chairman’s press conference. With the indexes closing at or very near price resistance levels, today’s data may well inspire the bulls higher or bring bears out of hiding depending on how investors digest the results. With an elevated VIX and futures pointing to gap up open, it seems an understatement to say anything is possible. Stay focused, and flexible.

Asian markets closed mixed in a rather falt session after Japan reported a disappointing plunge in exports. European markets trade mixed, cautiously awaiting the central bank decision. Overnight futures struggled to gain ground, but as the open near the pre-market pump up has begun suggesting another bullish morning gap. Buckle up.

Economic Calendar

Earnings Calendar

On the Hump Day earnings calendar, we have just 16 companies reporting quarterly results. Notable reports include BRC & MlHR.

News & Technicals’

Though there was a lot fo bullish energy at the open yesterday, we ended with a mixed bag of results. The SPY and IWM mostly chopped in a narrow range, with the DIA giving up early gains to close essentially flat. The QQQ and big tech struggled to hold the morning gap in the morning session, but the bulls fought back, closing the index with solid gains near price resistance levels. After the bell, FEX and ADBE produced strong earnings, with both stocks indicating substantial gains at the open today. However, during the night, US Futures seemed to struggle, often dipping into negative territory until early morning pump up began, which seems to have become the standard operating procedure for this year. Blackstone’s Tony James is warning this morning of a possible lost decade where market returns become anemic in a low-interest-rate environment but facing significant headwinds moving forward. During the night, Hurricane Sally strengthened to a Category 2 storm that made landfall at high tide, shutting down power and threatening widespread flooding. What a year! To much water in the south while the Pacific coast burns, suffering from drought.

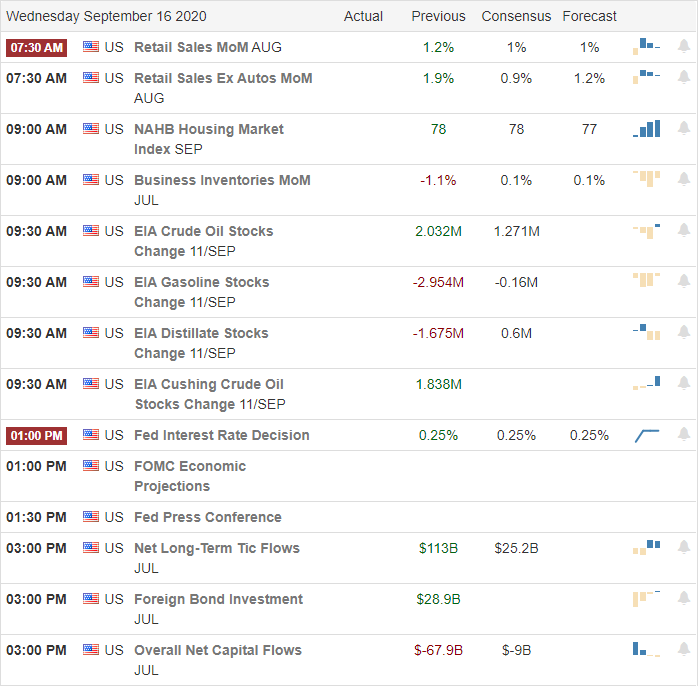

The FOMC will be in focus today as we wait for there interest rate decision, and of course, all eyes will be on the Jerome Powell at the press conference that follows. If that’s not enough, we keep investors guessing we also have Retail Sales, Business Inventories, Housing Market Index, and a Petroleum Statis report to digest before the 2 PM eastern statement release. Add to that index charts testing price resistance levels and an elevated VIX, and I think it’s safe to say anything is possible. As I write this report, futures point to a gap up open; however, I would not be at all surprised to see very anemic and choppy price action ahead of the FOMC decision. Becare not to chase with a fear of missing out if the morning gap does unfold.

Tuesday saw another significant gap higher followed by an afternoon selloff that left us with indecisive black candles. None of the 3 major indices were able to break out of their consolidation range of the last week. However, 8 of the 10 major sectors were up on the day, with Financial Services and Energies being the outliers. On the day SPY gained 0.49%, DIA was flat at +0.02%, and QQQ gained 1.42%. The VXX was also flat at 25.02 and T2122 (4-week New High/Low Ratio) fell back to mid-point at 51.83. 10-year bond yields rose slightly to 0.682% and Oil (WTI) was up almost 3% to $38.32/barrel.

During the day AAPL announced a slew of product refreshes but added a long-awaited bundle of AAPL services (subscription to music, TV, arcade and cloud storage) for $15/mo. Wall Street had been pushing the company to offer a subscription bundle revenue stream. AAPL also announced a fitness line aimed to compete with PTON. On the day AAPL was flat and PTON initially dropped but recovered for a 4.19% gain.

Hurricane Sally made landfall in AL overnight. As a Category 2 storm, the fear appears to be more about torrential rain and wind damage than major storm surge or large-scale inundation. However, AL, and FL businesses could see disruptions from the storm. It appears that in most measures, the West Coast fires and smoke are still the worst natural disasters impacting the country.

On the virus front, in the US, the numbers show we now have 6,788,471 confirmed cases and we have now had over 200k deaths at 200,197. This comes after a small uptick yesterday in a still (by US standards) “mild day” of 38,286 cases and 1,197 deaths. In a related story, the political operator placed as head of communications of HHS (the one who has changed reported numbers to fit Admin. narrative) publicly apologized for his most recent “deep state,” “sedition,” and related unfounded conspiracy theories that he has used to justify massaging the numbers provided by career scientists. Meanwhile, FDX reported a continued demand surge in the last quarter from pandemic-related orders. And SBUX reports same-store sales were down only 11% in August versus 2019 as the recovery continues.

Globally, the numbers rose to 29,764,825 confirmed cases and 939,962 deaths. The OECD now estimates the global economic contraction to be just 4.5% for the year. While this is still an unparalleled drop in global GDP, that is much better than their mid-year forecast of -6%. In Ireland, the entire cabinet is self-isolating and Parliament has been suspended following infections and a recent test. Meanwhile, Germany’s Education and Research Minister told a news briefing that she does not expect a vaccine to be widely available until mid-2021. At the same presser, the Health Minister said between 55% and 65% of the population would need to have already been vaccinated for it to control the virus in the population. In the neighboring Czech Republic they saw a record number of new cases and in France, dozens of schools have been closed in the last week as their own cases are increasing again. Spain has also brought on new restrictions to fight its own increase.

Overnight, Asian markets were mixed again, but leaned a touch more to the red side Wednesday. The NIKKEI and Hong Kong were flat with China and South Korea down. The remainder (smaller markets) were mostly green. Europe is also mixed this morning with the big 3 bourses all just on the red side of flat as traders wait on hints about the Fed statement (which comes after the European closes). In the US, at 7:45 am, the futures are pointing to another green open. The large-caps are implying an open up 0.40% with the NASDAQ implying a green but flat open.

Wednesday is a big day for major economic news with August Retail Sales (8:30 am), July Business Inventories (10 am), Crude Oil Inventories (10:30 am), FOMC Interest Rate Decision and Q3 Interest Rate Projection (both at 2 pm), and FOMC Press Conf. (2:30 pm). However, there are no major earnings reports on Wednesday.

We remain range-bound with gaps being the main move of the day. There is not a bullish trend yet, but the bearish trend has been broken. So be careful of volatility with gaps and indecisive swings controlling the market. That said, the market seems to be waiting on the Fed today. This is a bit odd since nobody expects a rate change and Fed officials (including the chair) have already often and repeatedly said rates will remain at essentially zero for years to come. So, I do not know what markets want or expect to hear…let alone what they might hear this afternoon.

Regardless, beware of the volatility. Stick to your plans. Follow the trend and don’t chase moves you have missed…there will be another one soon. Hang in there with your rules and keep locking-in profits. Remember, trading is a job, not a lottery ticket.

Ed

Swing Trade ideas for your Consideration and Watchlist: CWH, DRI, PYPL, TSM, LYV, FSM, BBY, ALLY, KSS, ETFC. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service