Jobless Claims and Virus News Lead

Markets started the day flat in the large-caps and a slight gap-down in the QQQ. After a sideways grind in the morning, there was a strong afternoon selloff. This left both large-cap indices printing large Bearish Engulfing candles and all 3 major indices closed at the lows to give us large black ugly candles. The VXX gained almost 3% to 18.84 and T2122 fell a little but remains well into the overbought territory at 87.22. 10-year bond yields were flat at 0.868% and Oil (was up half a percent to $41.66/barrel.

In miscellaneous news, LUV sent furlough warnings to about 15% of their mechanics as stalled talks continue with the pilot and flight attendant unions. The company is asking employees to take a 10% pay cut. Meanwhile, GOOG announced that their employee productivity is back above pre-pandemic levels, so they have adjusted well.

Wednesday the Business Roundtable called for more stimulus to save the economy. Jamie Dimon of JPM called the amounts involved “chump change” and at the same time said it was critical to avoid an economic crash. At the same time, the Institute for International Finance reported that the virus has pushed global debt to a record $277 trillion with “advanced nations” debt reaching 432% of GDP in Q3 (up 50% from 2019 Q3) and “emerging economies” only a bit worse at 248% of GDP. And all this comes as the US Senate also went on holiday recess until Nov. 30. It did this without a vote on another stimulus package. So, either the Senate is not concerned or they are too divided to decide.

The virus continues to rage as the US saw another 173,768 cases and 1,964 deaths on Wednesday. This surge has raised the US totals to 11,876,240 confirmed cases and 256,311 deaths. The 7-day average of new cases to 164,996 while the average number of deaths rose to 1,266/day. 47 states are have reported at least a 10% increase in cases since last week. 33 states have reported at least a 10% increase in covid-19 deaths since last week. New local and statewide restrictions continue to be implemented coast-to-coast mostly including mask mandates, curfews, and stay at home suggestions/requests. This comes as Admiral Giroir (White House Task Force) told reporters “this is not crying wolf, it is an absolutely dangerous situation…I lose sleep over where are right now.”

Overnight, Asian markets were mixed yet again but leaned to the red side. Malaysia (-1.31%) and India (-1.29%) led the losses while Indonesia (+0.66%) and Shenzhen (+0.63%) led gainers. However, in Europe, so far today we see red across the board. Smaller exchanges seem to be worse off, but the DAX (-0.87%), FTSE (-0.72%), and CAC (-0.70%) are indicative. As of 7:30 am, US futures are pointing to a flat to a modestly lower open. The DIA is implying a -0.17% open, the SPY implying a -0.11% open, and the QQQ implying a -0.28% modest gain at the open.

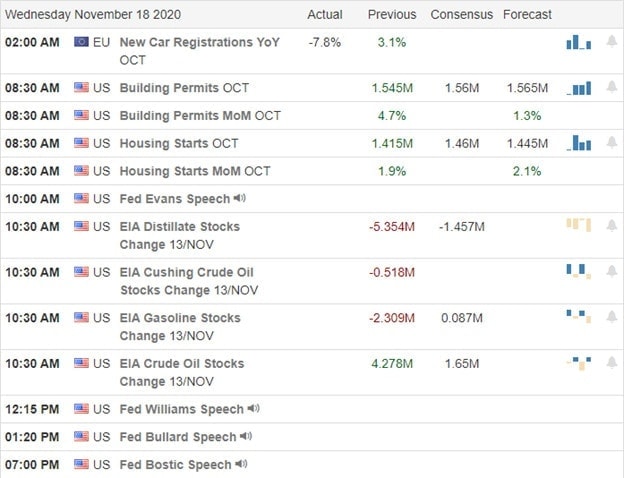

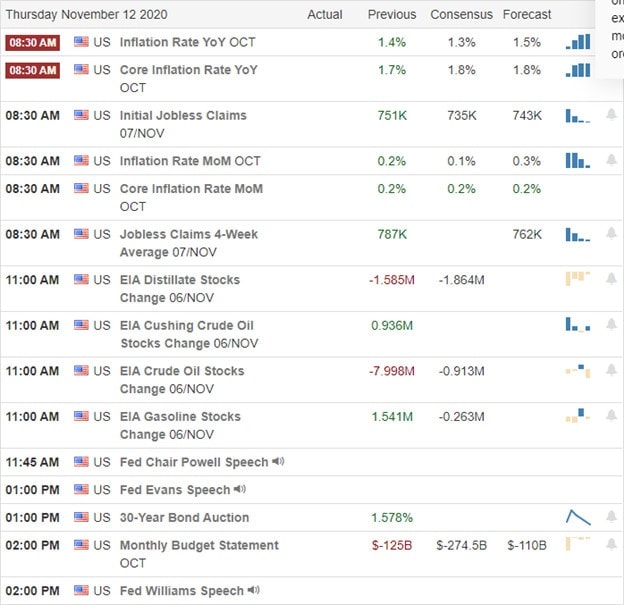

The major economic news for Thursday is limited to Nov. Philly Fed Mfg. Index and Weekly Initial Jobless Claims (both at 8:30 am), Oct. Existing Home Sales (10 am), and a Fed Speaker speaks twice (Mester at 8:30 am and 12:35 pm). Major earnings reports include BERY, BJ, M, and NTES before the open. Then after the close, BECN, BEST, INTU, POST, ROST, WSM, and WDAY report.

With no more major vaccine news, economic news may have the chance to move markets this morning. Just remember that for every push, there will be a reaction back the other way. So, don’t get caught up in FOMO (on either side). Remember there will be a chance for price to come to you soon. Stick to your discipline, keep taking profits (goals/targets) on the way, and work your trade plan. Consistency beats the occasional homerun every time. Focus on the trading rules you have built, follow the trend, and respect support and resistance. Good trading!

Ed

Swing Trade Ideas for your consideration and watchlist: SOLO, CRBP, JCI, NKLA, PLUG, DKNG, YUMC, QCOM. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service