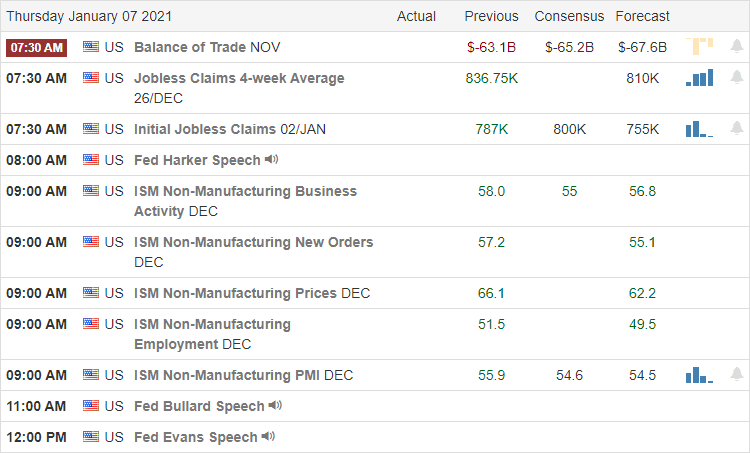

After a hideous and disgraceful display of politically fueled violence, Congress went back to work to certify the election for our Joe Biden. Let’s hope this country can now begin to heal. The bulls are clearly in control with hopes that more government stimulus is on the way under the new administration. Futures point to a modestly bullish open ahead of our biggest day of earnings this week and an economic calendar that includes a reading on Jobless Claims.

Asian markets closed mixed but mostly higher while China telecom shares plunged after the flip-flopping NYSE delisting decision. European markets are mostly higher this morning, and the U.S. futures indicate new market records at the open. Keep in mind before the bell tomorrow; we will get the latest reading Employment situation number, so plan your risk accordingly.

Economic Calendar

Earnings Calendar

On the Thursday earnings calendar, we have our most significant day with 21 confirmed reports. Before the bell, we will hear results from ANGO, AYI, BBBY, CAG, CSVI, HELE, LNN, LW, NTIC, PKE, REVG, SCHN, STZ, WBA, & WEI. After the bell, ACCD, AEHR, DCT, FC, MU, PSMT, & WDFC.

News & Technicals’

In my opinion, yesterday’s attack on the U.S., the capital, was one of the most shocking and disappointing events as our countrymen disgraced our republic. As a former military officer, I will pick up my M16 and defend the people’s right to protest. However, no matter your cause, there is no excuse for violence that puts our fellow countrymen in harm’s way. There is no excuse for this kind of behavior! After a very long night session, Congress certified the election for president-elect Joe Biden. Let’s hope the healing can now begin.

The bulls were out in force yesterday as it became evident that the Senate would flip after the runoff elections in Georgia, with the market celebrating a hopefulness of more government stimulus. The DIA and IWM closed at new record highs while the SPY pullback late in the day, losing its hold on an intraday record high. Trends remain bullish in the DIA, SPY & IWM while the QQQ displays a bit of weakness breaking its short-term uptrend. This morning, futures point to modest gains, ahead of International trade numbers and the weekly Jobless Claims report. As you plan forward, keep in mind that we will get the Employment Situation number before the bell on Friday, which is often a market mover.

As has been the case each day this year, markets gapped one way and then charged the other direction immediately. Wednesday saw the gap down followed by a strong morning rally. About 11:30 markets started to grind sideway, even drifting a bit higher until shortly after 2 pm. Then our deluded President’s conspiracy theory lies believing followers were incited to riot and storm the US Capitol building. Markets sold off as the seat of government was under siege for hours, but still managed to hold on to some of the morning gains. The DIA even closed at another all-time high close. On the day, DIA gained 1.44%, SPY gained 0.60%, and QQQ lost 1.39%. The VXX actually lost half a percent to 17.55 and T2122 jumped up into the overbought territory at 92.48. 10-year bond yield shot higher again to 1.039% and Oil (WTI) gained another percent to $50.52/barrel.

Lost amongst the coverage of insurrection was that the Democrats won both of the GA Senate runoff elections. So, President-elect Biden’s party will also control both Houses of the Congress (through VP Harris’ tie-breaking vote). Some had said an expectation of that outcome was the reason for the gap down. However, then markets immediately rallied, so it is hard to divine what Markets think about that change in governance. Still, it makes the increase to a $2,000/person direct payment much more likely.

The other story lost in the wash was that the riots helped to accelerate the weakness in the dollar. It has now fallen to the levels not seen since 2017. This has helped drive the Euro to a level that currency has not seen since 2014. Obviously, as the dollar falls, dollar-denominated commodity prices rise. This partially explains the gains in Gold and Oil. It also increases the pressure on the Fed and fiscal stimulus, which goes less far as each dollar of stimulus buys less. Overseas, it makes it harder for Central Banks and Governments to repay their own debt and to sell goods to the US. As a result, Bloomberg reports that some analysts are expecting the ECB and China to take action to lower the value of their own currencies to offset dollar weakness.

It’s hard to believe, but on a day with 4,100 virus deaths in the US, COVID-19 took a back seat. Related to the virus itself, US infections continue to rage as the US. The totals have risen to 21,857,616 confirmed cases and 369,990 deaths. As mentioned, we did hit another national record high in deaths, but also in new cases at 260,973 on Wednesday. However, the 7-day daily average remains at 228,891 new cases and 2,742 deaths per day.

Globally, the numbers rose to 87,763,513 confirmed cases and the confirmed deaths are now at 1,893,873 deaths. As a reference, the world is averaging 645,896 new cases and 11,250 new deaths per day. In Japan, the PM has declared a state of emergency in Tokyo and surrounding areas as they also reported a record number of new cases. Travel bans from international travel, especially from the UK and South Africa continue to be added. In Europe, the EU approved the MRNA vaccine, which means it will begin rollout across the EU by next week.

Overnight, Asian markets were mostly in the green. South Korea (+2.14%), Japan (+1.60%), and Australia (+1.59%) led the gainers. The only appreciable loss was in Hong Kong (-0.52%) with a couple other exchanges just on the red side of flat. In Europe we see a similar story so far today. The FTSE (-0.47%) is one of the notable red spots with the DAX (+0.41%) and CAC (+0.31%) being more typical of the continent. As of 7:30 am, despite the deluded riots that left 4 dead and the seat of Government battered, US Futures are moderately green this morning. The QQQ is strongest, implying a +0.74% gap up open, while the SPY (+0.40%) is implying a positive, but not gappy open and the DIA (+0.28%) is implying a modest gain at the open.

The major economic news for Thursday includes Import/Exports, Nov. Trade Balance, and Weekly Initial Jobless Claims (all at 8:30 am.), Dec. ISM Non-Mfg. PMI (10 am), and a pair of Fed speakers (Harker at 9 am and Bullard at Noon). Major earnings reports include AYI, BBBY, CAG, HELE, LW, REVG, STZ, and WBA before the open. Then after the close MU reports.

Volatility continues early in 2021. However, it would be hard to predict anything as volatile as Wednesday’s riots happening again. Even though the Cabinet apparently hasn’t had the courage to invoke Article 25, we can expect impeachment proceedings soon unless the GOP is willing to make massive concessions to buy off Democrats. At any rate, with the immediate threat behind us and President Biden’s election now certified, hopefully, we can return to the virus being the main threat for days to come. It would still be wise to remain cautious and not chase. Be ready for the market switch-backs we’ve seen each of the first several days of the year.

As always, lock in profits (base hits are better than long fly-outs) and stick with your discipline. Follow the trend, respect both support and resistance, and don’t chase the moves you have missed. There will be another opportunity and we don’t need to trade every day. Focus on the chart and your trading process. Remember, trading is a marathon, not a sprint.

Ed

Swing Trade Ideas for your consideration and watchlist: GOLD, KGC, GDX, WPM, NUGT, AGI. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

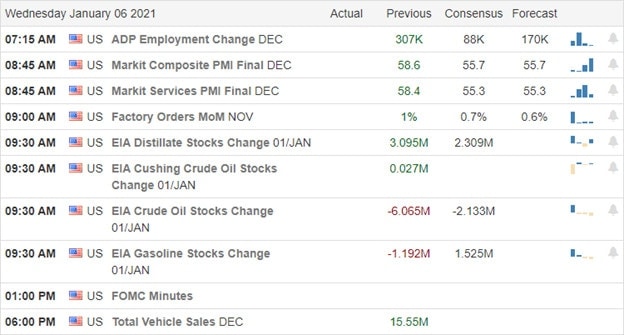

Political news out of the Georgia runoff election and the Congressional vote to certify the Biden presidency with efforts to block the process could set off price action fireworks in the market today. The bulls have defended support levels, but they fell just short of clearing the price resistance above at the close yesterday. With the VIX remaining elevated, be prepared for some news related price volatility, and don’t forget the FOMC minutes’ release this afternoon.

Overnight Asian markets closed mixed but mostly higher as energy stocks surged following the OPEC action. European markets see green across the board this morning, while the U.S. Futures offer up a mixed bag of results with the Dow higher and the other indexes modestly lower heading into the open. Stay focused and flexible as anything is possible on this very political new driven day.

Economic Calendar

Earnings Calendar

On the Hump Day earnings calendar, we have nine verified reports. Before the bell, we will hear from GBX, MSM, RPM, SMPL, & UNF. After the bell, LNDC, RELL, RGP, & SAR will report.

News & Technicals’

We face an interesting day in the market with a lot of political news that has the potential to move the market. First, we have the runoff elections that are drawing closer to flip the Senate raising concerns it will clear the deck for higher taxes. We also Congress try to certify the Biden election win, but a group also moves to block the effort, and protests have already begun. The 10-year Treasury yield rose above 1% for the first time since March in reaction to current Georgia runoff results, and Bitcoin surged above $35,000 for the first time. While politics preoccupy the market, the daily death toll hit new records as more than 3800 Americans succumb to the virus. Sadly, a grisly reminder we may have a long way to go to win this pandemic battle.

Yesterday’s bullish price action lifted the index charts just enough to challenge price resistance but failed to clear the level by the close. We should plan for the possibility of price volatility based on the political wrangling in Congress and Georgia. We also have some economic news to keep an eye on, such as releasing the FOMC minutes at 2:00 PM Eastern to create some price action fireworks. The VIX remains elevated as we attempt to rally, and the Absolute Breadth Index continues to show a concerning decline. Stay with the bullish trend but stay on your toes should the sentiment quickly shift.

Markets opened slightly lower on Tuesday. However, after a rollercoaster first hour, the bulls took control and led a sustained rally up until the last hour, which gave back just a touch of the gains. On the day the QQQ gained 0.82%, the SPY gained 0.69%, and the DAI gain 0.50%. VXX fell over 3% to 17.64 and T2122 shot back up to sit just below the overbought territory at 77.17. 10-year bond yields rose sharply to 0.955% and Oil (WTI) shot up over 4.5% buoyed by Saudi Arabia announcing production cuts, leaving it at $49.80/barrel after trading above $50 for the first time since last February.

Politics takes center stage again today without much real short-term impact. One of the two GA Senate races is projected to go to the Democrat challenger while the other election is too close to call, with the Democrat currently in the lead. If both Democrats win, the Senate becomes a stalemate for 2 years with Democratic VP Harris then being the deciding vote. If either seat remains Republican, current Majority Leader McConnell retains the power to obstruct all Democratic plans for 2 years. Meanwhile, the delusion of conspiracy theories comes to a crescendo as the President and some of his supporters will hold political theatre before accepting the Nov. election results.

Mortgage demand pulled back 0.80% in the last 2 weeks of December, despite record low interest rates (2.68% for 30-year conforming loans, which was way down from 2.90% in the previous reporting period). The volume of applications was up 3% above the same period a year prior, but the volume had been running at 20% or more higher than the previous year since the beginning of the pandemic. So, this may be signaling an end to the home buying surge.

Related to the virus itself, US infections continue to rage as the US. The totals have risen to 21,579,641 confirmed cases and 365,664 deaths. The post-holiday surge is still not fully upon us yet, but we did hit a national record of 3,775 deaths Tuesday. However, the 7-day daily average remains at 222,771 new cases and 2,678 deaths per day. As mentioned yesterday, the hospital capacity in the Los Angeles area is critical. Ambulance crews have told to perform 15 minutes of life-saving at any scene and then only transport patients that do not have a low likelihood of survival. Beyond that, each ambulance may experience an hour or more of wait time at the hospital before a patient can be seen and they freed up for another call. In addition, all non-essential (beyond just elective) surgeries have been canceled in the region.

Globally, the numbers rose to 86,959,936 confirmed cases and the confirmed deaths are now at 1,878,706 deaths. As a reference, the world is averaging about 637,000 new cases and 11,250 new deaths per day. As in the US, in Europe, delays in vaccinations are a major storyline. The Netherlands just gave its first vaccination on Wednesday as their National Health Ministry had bet on the wrong vaccine to be ready first. In France the pace is also far, far behind with just a few thousands of doses given. Italy also received 100,000 fewer doses than they expected. Meanwhile, for comparison the UK has vaccinated 1.3 million people and Germany almost 400,000. In China, over 100 cases were reported in one province and that region is being locked down with a negative test required to enter or leave the province as of today.

Overnight, Asian markets were mixed, but mostly red. Indonesia (-1.17%), Australia (-1.12%) and Malaysia (-1.02%) led the losses. Shanghai (+0.63%) was the only appreciable green exchange. In Europe, markets are mostly green so far today. Among the big 3 bourses, the FTSE (+2.75%) leads as an outlier, with the DAX (+1.02%) and CAC (+0.80%) more typical. As of 7:45 am, US Futures are mixed. The QQQ is implying a large -1.44% gap down while the DIA (+0.15%) is slightly green and the SPY is implying a -0.27% open at this point.

The major economic news for Wednesday includes Dec. ADP Nonfarm Employment (87:15 am), Dec. Services PMI (9:45 am), Nov. Factory Orders (10 am), Crude Oil Inventories (10:30 am), and Dec. FOMC Meeting Minutes (2 pm). Major earnings reports are limited to MSM and RPM before the open. There are no major earnings reports after the close.

Volatility continues early in 2021, with each day so far starting with markets going one direction only to slam back hard the other direction. Some pundits claim this is related to fear over the Senate, others that is it virus-related. Regardless of the cause, be cautious not to chase and be ready for market switch-backs. Safe is better than fast and nimble is better than slow…if that makes sense.

As always, lock in profits (base hits are better than long fly-outs) and stick with your discipline. Follow the trend, respect both support and resistance, and don’t chase the moves you have missed. There will be another opportunity and we don’t need to trade every day. Focus on the chart and your trading process. Remember, trading is a marathon, not a sprint.

Ed

Swing Trade Ideas for your consideration and watchlist: CX, X, GE, LTHM, TLRY, AMAT, REGI, XRT. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

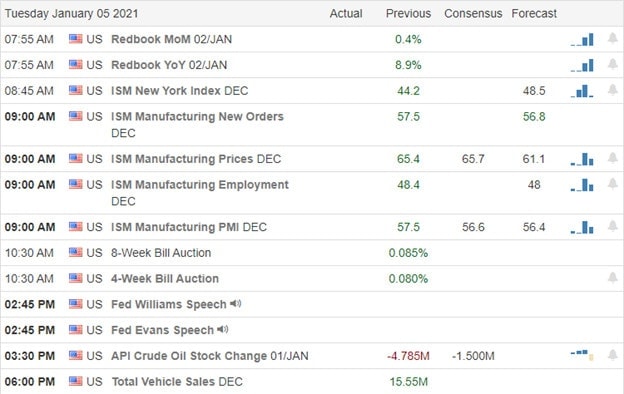

Yesterday selling us reminded us that bears still exist and that an overextended market condition can produce quick and painful selloffs. What happens next could be very important to the short-term future direction of the market. If the bulls are strong enough to defend yesterday’s lows over the next few days, Monday’s price action will be chalked up to volatility. However, if the bears show the ability to create a lower low in the next few days, they could gain the upper hand can create technical damage in the index charts. Expect the Georgia runoff election news to create pice sensitivity over the next 24 hours.

Overnight Asian markets recovered from early losses after the NYSE reversed its Chinese telecom delisting decision. European markets see modest losses across the board this morning as England goes into a nationwide lockdown. U.S. futures lose overnight gains turning modestly bearish as we head toward the open with ISM Mfg. Data in focus at 10 AM Eastern.

Economic Calendar

Earnings Calendar

On the Tuesday earnings calendar, we have twelve companies listed but only one verified report. Keep an eye on SGH reporting after the bell today.

News & Technicals’

A late afternoon decision by the NYSE reversed their decision to delist three Chinese telecom giants helping the overnight futures trade higher. Yesterday’s pop and drop price action left behind bearish candle patterns as the market reacted to Iranian military action, the pending Georga Senate runoff election, and surging pandemic concerns. Although there is a reason for caution heading into the Tuesday open, the bulls fought back, holding on to essential supports such as the psychological Dow 30,000. Remember, one day does not make a trend, so what happens next will be very important to the market’s short-term direction. Should the bulls prove strong enough to defend and recover broken trends, yesterday’s selloff could prove to be nothing more than volatility. However, if the bears can produce a follow-through, lower low in the next few days, they could gain the upper hand.

News out of Georgia may well create some price sensitivity and volatility today and into tomorrow open. Plan your risk carefully. Also, more news such as England going into another pandemic triggered, countrywide lockdown, New York considering making it a crime to avoid vaccination, or the possible addition of more public restrictions could add to the price volatility. Stay on your toes and be careful not to overtrade in this environment.

Markets gapped higher between 0.3% and 0.5% at the open Monday. However, this was met by a face-ripping selloff that lasted until about 12:30 pm on fears over the holiday surge and the new, more contagious virus strain. The rest of the day was a sideways grind with a slight bullish bent to i. However, stocks closed closer to their lows than to the Open. This left us with large Bearish Engulfing candles in all 3 major indices, albeit with lower wicks. On the day, SPY lost 1.36%, DIA lost 1.13%, and QQQ lost 1.41%. The VXX gained almost 9% to 18.25 and T2122 fell sharply and now sits at 31.19. 10-year bond yields were flat at 0.915% and Oil (WTI) fell over 2% to $47.36/barrel.

In a bizarre turnaround, the NYSE announced it will not delist the 3 Chinese telecom companies in order to comply with a Presidential Executive Order. So, China Telecom, China Mobile and China Unicom will all remain listed for now.

An interesting tidbit out of the UK. Since the first of the year, the cost of moving freight to the UK from Europe has quadrupled due to extra turmoil from Brexit. This was also complicated by the extra testing requirements at the border around the new virus strain. This news came as the UK enters its third national lockdown.

Related to the virus itself, US infections continue to rage as the US. The totals have risen to 21,353,051 confirmed cases and 362,123 deaths. The post-holiday surge is still not fully upon us. However, the 7-day daily average remains high at 218,967 new cases and 2,702 deaths per day. So far, the US has vaccinated only 4.5 million people (less than 25% of 2020 goal), but has distributed well over 15 million doses. So, the hold-up is the logistics of administering the shots. Due to the extreme requirements for storage temperatures, relatively few locations in each state have the vaccine and this added to a system strain of all the new cases has slowed vaccinations. As an example of system load, Los Angeles ambulance crews were told to make triage decisions and not transport patients with little chance of survival, because the hospitals have no capacity left for such patients.

Globally, the numbers rose to 86,197,384 confirmed cases and the confirmed deaths are now at 1,863,113 deaths. As a reference, the world is averaging about 622,939 new cases and 11,170 new deaths per day. As mentioned, the UK imposed another national lockdown to fight the strain on their NHS caused by the new virus variant. A Cabinet Minister went further to say that UK citizens should not be traveling under any circumstances. Elsewhere in Europe, Italy has decided to extend its own lockdown measures at least another two weeks and Germany is discussing an extension of their own quarantine with regional leaders.

Overnight, Asian markets were mostly green again. Thailand (+2.62%), South Korea (+1.57%), and Shenzhen (+1.50%) were the strong outliers with most exchanges moving much more modestly and mostly to the upside. However, in Europe, markets are mostly red with only a few clinging to the green side of flat. Among the 3 major European bourses, the FTSE (-0.09%) is just red, while the DA (-0.64%) and CAC (-0.71%) are more typical of the continent at mid-day. As of 7:30 am, US Futures are just on the red side of flat. The DIA is implying a -0.17% open, the SPY implying a -0.15% open, and the QQQ implying a -0.10% open at this point.

The major economic news for Tuesday is limited to Dec. ISM Mfg. PMI and Dec. ISM Mfg. Employment (both at 10 am) and a Fed speaker (Williams at 3:45 pm). There are no major earnings reports on the day.

After a rough start to 2021, markets seem to be pausing to check the wind direction. This may be due to waiting on the GA Senate elections, the Republican theatre to placate conspiracy theories, or even waiting to see the depths of post-holiday virus impacts. Regardless, there is no strong direction in pre-market this morning.

Lock in those base hit profits where you can and stick to your discipline. Follow the trend, respect support and resistance, and don’t chase moves you have missed. Focus on the chart and your trading process. Remember that trading is a marathon, not a sprint. So, don’t feel like you need to trade every day.

Ed

Swing Trade Ideas for your consideration and watchlist: WMT, AUY, LMNX, UTHR, TPR, KL. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

The afternoon New Year’s eve record-setting rally looks to extend this morning as the bulls step on the gas on this first trading day of 2021. Trends remain bullish as vaccine results will produce a much better year for business. That said, hospitalizations hit new records as well over the holiday shutdown. One has to wonder what kind of restrictions will businesses have to face under a new administration should the surge continue. Long story short, have a plan of action to protect your capital should the market stumble.

Asian markets closed mixed but mostly higher overnight, and European markets are decidedly bullish this morning. U.S. futures point to bullish open ahead of PMI Mfg. and Construction Spending numbers with a very light day on the earnings calendar. Expect possible political news sensitivity as the tenuous transition of power begins.

Economic Calendar

Earnings Calendar

Although we have several small-cap stocks listed on the earnings calendar, their reports are unconfirmed, and thus no notable earnings.

News & Technicals’

On the first trading day of 2021, the U.S. Futures look to extend the late New Year’s eve record-setting rally. With an accommodative Fed, more Governmental stimulus rolling out, and high hopes that vaccines will put the pandemic behind us, there is a reason for all the bullishness. However, with indexes already at record highs, high unemployment, and substantial economic damage to businesses, traders will have to remain focused and ready to act should the market stumble. Market P/E valuations are very high as we enter the new year, and with economic restrictions still in place, will companies be able to produce healthy enough earnings to sustain current prices? Hospitalizations hit new records highs over the holiday and did post-pandemic travel. How will the new administration respond if infection rates continue to surge? A lot to ponder as we kick-off the new year.

One thing for sure at the moment is that the index trends remain bullish, and there seems to be a relentless willingness to buy up stocks no matter the valuation. Some suggest we are in a growing bubble, and while that may be true, bubbles can continue to extend for months. As traders, all we can do is stay with the trend as long as it lasts, follow our rules, and avoid overtrading. Always have a prepared plan should the bears suddenly have reason to come back to work. Trust me, they will, and it will likely occur very suddenly. With this morning gap up to new records, the T2122 indicator will once again show a short-term extended condition. The Absolute Breadth Index remains in a concerning decline, and keep in mind the VIX-X remains above a 20 handle as we set new records in the indexes.

Markets opened relatively flat on New Year’s Eve. However, after some normal volatility, the bulls won out. All 3 major indices closed at new all-time high Closes (but not above prior intraday highs). The large-caps both printed “Morning Star type” candle patterns and the QQQ printed a Bullish Harami (of the Spinning Top variety). On the day, the DIA gained 0.55%, the SPY gained 0.51%, and the QQQ gained 0.25%. VXX was flat at 16.79 and T2122 (4-week New High/Low Ratio) inched up just outside of the overbought territory at 79.59. 10-year bond yields were flat at 0.916% and Oil (WTI) was also flat at $48.42/barrel.

In business news over the long weekend, TSLA reported they just missed its goal of shipping 500,000 cars in 2020, coming up just 450 cars short of the milestone. Bitcoin also rallied above $34,000 for the first time. And the NYSE delisted 3 Chinese telecom companies as required by President Trumps November executive order. China vowed some unspecified retaliation on Saturday. In early Monday news, 226 GOOG employees have formed a union after ongoing disputes with management.

On the political front, the new Congress was sworn in. The Senate also completed the process by voting to override the President’s veto of the $740 billion Defense Spending bill (now law). The same leadership was re-elected on either side of the aisle in both Houses, while the President continues to pressure and plot ways to overthrown his election defeat. This runs against the backdrop of the GA Senate runoff elections that are likely to leave the Republicans in control of the Senate but are very close races according to most pundits. No legislative agenda (such as a vote on raising stimulus payments to $2,000) is likely to take place until after those results.

Related to the virus itself, US infections continue to rage as the US. The totals have risen to 21,113,528 confirmed cases and 360,078 deaths. The post-holiday surge is still not fully upon us. However, the 7-day daily average remains high at 216,886 new cases and 2,696 deaths per day. Three more states have identified cases of the new strain of COVID-19 over the weekend. Most experts have been saying they believe the new strain is already everywhere. On Sunday, the federal government said it is in talks with the FDA to possibly speed up the rate of vaccinations by giving half doses of the MRNA vaccine to twice as many people.

Globally, the numbers rose to 85,579,769 confirmed cases and the confirmed deaths are now at 1,852,389 deaths. As a reference, the world is averaging about 613,548 new cases and 11,066 new deaths per day. The new strain first seen in the UK has now been found in 37 countries as well as Hong Kong and Taiwan. Parts of Japan are going back into lockdown. There is also now a different mutation out of South Africa. Oxford scientists say this strain has substantial changes in the structure of the virus and is therefore concerning related to current vaccine effectiveness. British Health Minister Hancock said it is too early to tell, but he is incredibly worried about the new variant. In an interesting story, Bloomberg says France is approaching vaccinations in a very cautious way, having only completed 500 of the first round of shots to date, despite starting the same day as all other European countries.

Overnight, Asian markets were mostly green. Malaysia (-1.51%) and Japan (-0.68%) were outliers. However, South Korea (+2.47%), Shenzhen (+2.45%), and Australia (+1.47%) led the rest of the Asian exchanges higher. This came despite Chinese Dec. Mfg. PMI data coming in below expectations. In Europe, markets are solidly green across the board so far on Monday. Among the big 3 bourses, FTSE (+2.59%) leads the way with the CAC (+1.52%) and DAX (+1.08%) more typical across the continent. As of 7:30 am, US Futures are pointing to a moderate gap higher at the open. The DIA is implying a +0.47% gap, the SPY a +0.43% gap, and the QQQ a 0.41% gap higher.

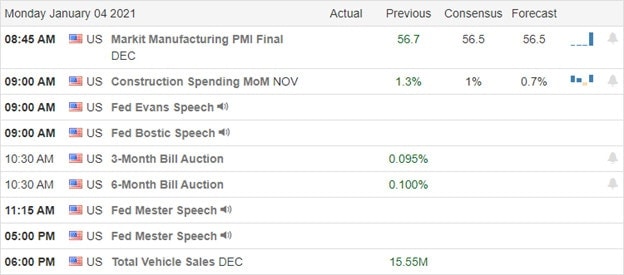

The major economic news for Monday is limited to Dec. Mfg. PMI (9:45 am) and a Fed speaker (Bostic at 10 am). There are no major earnings reports on the day.

The bulls seem to want to start off the new year on a small gap higher. With much of the big money expected to return to the office today, we may see some optimism coming off their vacation. For whatever reason, Bitcoin has taken a major Monday hit (down 10%) after having reached all-time highs.

Focus on the chart and your trading process. Lock in those base hit profits and maintain your discipline. Follow the trend, respect support and resistance, and don’t chase moves you have missed. Remember that trading is a marathon, not a sprint. So, don’t try to get rich quick. Do it in the long-run by hitting goals over and over again.

Ed

Swing Trade Ideas for your consideration and watchlist: COMM, TFC, TXN, SWCH, JNPR, HON, ORBC, AVTR, WFC. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service