Stocks to Gap Up As Short-Squeeze Fades

US markets followed the world’s lead Monday gapping higher about a percent, but after the open the major indices mostly ground sideways amidst volatility. This ended with the large-caps printing indecisive candles (DIA a Harami Doji and the SPY a Spinning Top) to start the new month. While also having significant wicks, the QQQ was much more decisively bullish, putting in the best gain in 10 weeks. On the day, DIA was up 0.74%, SPY up 1.62%, and QQQ up 2.50%. The VXX fell over 5% to 19.88 and T2122 shot back up into the mid-range at 67.07. 10-year bond yields were flat at 1.071% after a volatile day and Oil (WTI) rose almost 3% to $53.68/barrel.

The social media pushed price action continued Monday as many brokerages reported outages at the open. Silver jumped 8.2% (11% intraday) as the massive volume and volatility continued in names like GME (-30% on a 52% range day) and AMC (flat on a 33% range for the day). In response, the CME raised the margin requirements for silver purchases. However, some brokers continue to slightly loosen restrictions on those tickers with fallout including that Robinhood was forced to raise another $2.4 billion in capital to use as collateral for trades in the high-volatility names and may need to raise another billion Monday night. However, overnight these moves may have lost steam as GME is down another 30% and Silver and AMC are also both down big.

On the stimulus front, Democrats took the first step toward a passage of the $1.9 trillion relief bill that would not require Republican support by introducing a budget resolution. This came ahead of the two-hour evening meeting between the President and the 10 Republican Senators who had sent him a $600 billion alternative to his plan. Both sides said the meeting was productive and talks would continue.

Related to the virus itself, US infections continue to rage as the US. The totals have risen to 26,911,375 confirmed cases and 454,213 deaths. However, the number of new cases continues the recent trend of falling and is almost back down to the pre-election level as the average new cases are now 147,839 new cases per day. Still, deaths remain stubbornly high at 3,256 per day. Dr. Fauci told reporters Monday that even if you had the original strain of COVID-19, there is a high rate of reinfection from the new (UK, Brazilian and South African) variants now circulating. In addition, Democratic lawmakers from both Houses of Congress called on President Biden to increase the supply of N95 masks for the public and to distribute them at no cost via USPS and the local pick-up centers.

Globally, the numbers rose to 104,011,252 confirmed cases and the confirmed deaths are now at 2,249,880 deaths. In good news, the world’s average of new cases is down again to 522,508 per day, but mortality remains high at 13,869 new deaths per day. In the UK, the government has begun a door-to-door testing program in 3 of the hardest-hit regions of the country in an attempt to slow the surge from new variants. Meanwhile, in Asia, Japan has extended its state of emergency while simultaneously holding a press conference to say the Summer Olympics will be held as planned.

Overnight, Asian markets were strongly green again. India (+2.57%) led again, with Taiwan (+2.27%) not far behind, but strong gains were seen throughout the region. The same is true in Europe so far today. The CAC (+1.66%) and DAX (1.15%) are typical, but the FTSE (+0.42%) lags a bit. As of 7:30 am, US Futures seem to be following the rest of the world again and are pointing to a gap higher at the open. The DIA is implying +0.82%, the SPY implying +0.86%, and the QQQ implying +0.87% in an unusually consistent move at this point.

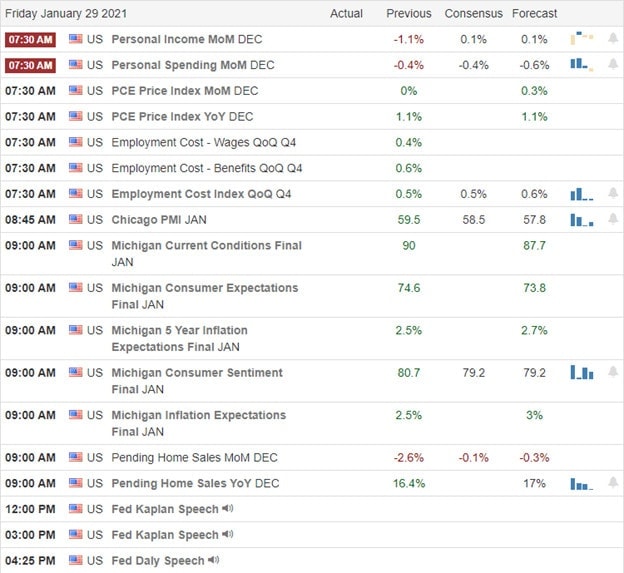

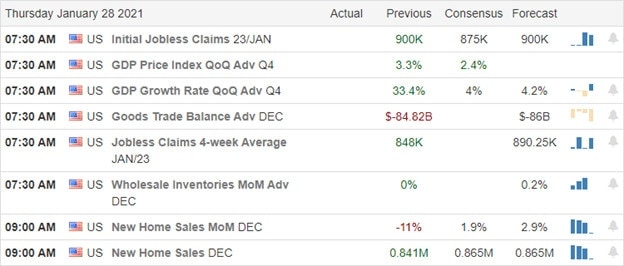

There is no major economic news for Tuesday, but there are 2 Fed speakers (Mester and Williams both at 2 pm). Major earnings reports for the day include BABA, ARCB, ABG, BP, BR, CTLT, COP, ETN, EMR, XOM, RACE, BEN, GPK, HOG, HCA, HUBB, IDXX, IMO, LII, MDC, MMP, MAN, MPC, MCK, MPLX, PFE, ST, SIRI, SYY, UPS, GWW, and WAT before the open. Then after the close, GOOGL, AMZN, AMCR, DOX, AMGN, ATO, CMG, CB, EA, FBHS, GOOG, LU, MHO, MTCH, PKI, SCSC, STE, SMCI, and VIAV all report.

It looks like the Bulls are off and running again this morning. It also appears the shine has come off the recent social-media short squeeze as GME, AMC, and Silver are all don big overnight. However, be very careful of volatility. Even with a strong day Monday, the market daily candles showed a lot of wick. In addition, heavy earnings reports before the open can still rock the boat. So, as tempting as it may be, we are not lottery ticket buyers or fad followers. We’re traders.

Remember to keep locking in your profits. Follow the trend, respect support and resistance levels, and don’t chase the moves you missed. It’s all about achieving trade goals and sticking to your discipline. Remember, our job is to produce consistent gains…not catch record-breaking one-day moves. So, stick with your plan, maintain discipline and work your process.

Ed

Swing Trade Ideas for your consideration and watchlist: UPWK, JMIA, XBI, VIAC, DQ, FUBO, ALT. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 Dick Carp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

Free YouTube Education • Subscription Plans • Private 2-Hour Coaching

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service