Powell calms the waters with more transitory inflation talk in Congress while at the same time the Social Security Office prepares for the highest cost of living adjustment in decades due to inflation. Hmm, you can’t make this stuff up, folks! Beginning today, up to 36 million families will begin receiving more stimulus checks from the IRS each month through the end of the year, and the FOMC will continue to print $120 billion per month to keep the party going. Markets will have a lot to digest this morning, with several economic reports as the number of earnings events ramp up.

Overnight Asian markets closed the day mixed with the NIKKEI down 1.15%, while the SHANGHAI rose 1.02% after China reports its economy grew in the second quarter. However, across the pond, European markets see red across the board this morning. Ahead of a big day of earnings and economic data, U.S. futures currently point to mixed open with the Dow looking lower and Tech Sector trying to hold on to some green. So buckle up; it could be a bumpy ride as we react to all the data from this extended market condition.

Economic Calendar

Earnings Calendar

On the Thursday earnings calendar, we have our biggest day of the week of reports with 35 companies listed. Notable reports include AA, AOUT, BK, CTAS, MS, PBCT, PGR, TSM, THC, USB, UNH, & WIT.

News & Technicals’

Seniors could receive the highest cost of living adjustment in decades. Based on estimates from the Consumer Price index data, the increase could be as high as 6.1%. Hmm, how can that be when Jerome Powell told us yesterday that inflation is transitory and that the Fed will continue printing $120 billion per month. About 36 million families will start receiving monthly IRS checks starting today through the end of 2021! The Biden Rescue Plan increases the payments up to $3600 per child. General Motors warns Bolt EV owners not to park the vehicle inside or to charge them unattended overnight due to a fire risk. Approximately 69,000 Bolt’s between 2017-2019 are involved in the recall. Treasury yields fell this morning after the Jerome Powell testimony in Congress yesterday. The 10-year fell to 1.317% this morning, with the 30-year sliding 1.94%

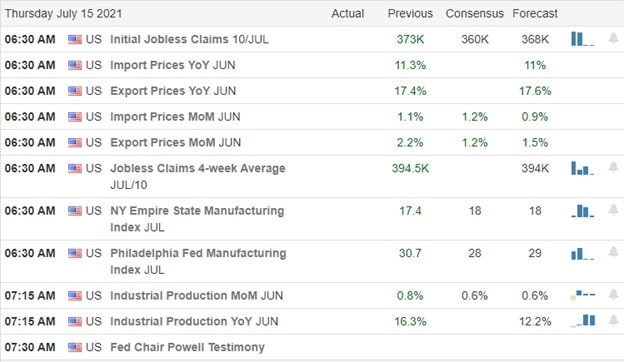

Markets bulls surged in early morning trading yesterday but could not hold onto the early gains pulling back by the close. As a result, the QQQ squeaked out a 0.16 cent gain while the DIA, SPY & QQQ ended the day with modest losses. However, the only index suffering technical damage was the IWM after failing its 50-day average, creating a lower high within a downtrend pattern. This morning we will get the latest reading on the Jobless Claims, Philly Fed MFG, Empire State MFG, Import/Export Prices, Industrial Production, and more Jerome Powell talk in Congress. If that’s not enough, we will also have a busy morning of potential market-moving earnings reports. So buckle up and expect anything to occur as the market sorts through the data in a very extended condition.

Despite much higher-than-expected producer prices (wholesale inflation), markets gapped up on Wednesday. However, the rest of the intraday action was a sideways grind with a slightly bearish trend. This left us with black Spinning Top type candles in all 3 major indices. In fact, the QQQ closed at another all-time high, despite the black body. On the day, SPY gained 0.18%, DIA gained 0.15%, and QQQ gained 0.18%. This all happened on very narrow breadth as a handful of FAANG stocks kept markets green on the day. (AAPL in particular had a tremendous day on heavy volume, closing at another new all-time high.) VXX fell over 2% to 28.91 and T2122 fell further into the oversold territory at 16.73. 10-year bond yields fell sharply to 1.351% and Oil (WTI) dropped 3.36% to $72.72 on news that OPEC+ had reached a deal that will raise their production quotas significantly.

As expected, Fed Chair Powell told Congress that the FOMC can wait before it starts to ease bond purchases, let alone taking rate action, despite surging inflation data. He stuck to the story that indications are that the inflationary surge will be transitory and that the economy is still a long way off from reaching the “substantial further progress” bar the committee has set before changing policy. Powell testifies again before the Senate this morning.

Last night China reported that its GDP grew 7.9% in Q2. This was lower than the expected 8.1% growth for the quarter. In other data released, Chinese retail sales jumped 12.1% in June (versus an 11% increase expected). And Chinese Industrial output also rose 8.3% year-on-year in June, versus the analyst estimates of a 7.8% increase. As mentioned yesterday, this would seem to indicate the Chinese recovery was losing steam in Q2, but came on strong in June, reacting to the newest Chinese stimulus policies.

US Consumer debt soared in Q1, reaching an all-time high of $14.64 trillion. The increase came despite average credit card balances have declined by the second-largest amount on record. (Only 5.63% of the total is credit card debt, which is the lowest percentage since records have been kept.) This paradox seems to be because there is a huge amount of student loan debt and increases in home-equity balances as consumers lock in ultra-low-rate debt and auto loans also soared (despite price increases). While most of the major banks have reported blowout quarters, BAC got hammered Wednesday after reporting it had lower than expected interest income.

Overnight, Asian markets were mixed but mostly green on the Chinese data. Shanghai (+1.02%), Taiwan (+1.06%), and Indonesia (+1.13%) led the gainers. Meanwhile, Japan (-1.15%) was an outlier to the downside, with the other three losses in the region being modest. However, in Europe, we are seeing significant losses across the board so far today. The FTSE (-0.84%), DAX (-1.08%), and CAC (-0.88%) are typical of the continent at mid-day. As of 7:30 am, US Futures are pointing to a red open as well. The DIA is implying a -0.59% open, the SPY implying a -0.45% open, and the QQQ implying a -0.09% open an hour in front of the data dump at 8:30 am. At this point, the dollar is slightly higher and 10-year bond yields are falling again at 1.327%. Commodities are mixed, with Oil down almost 2% and metals unchanged to slightly higher.

Major economic news scheduled for Thursday includes Import/Export Price Index, Weekly Jobless Claims, NY Empire State Mfg. Index, and Philly Fed Mfg. Index (all at 8:30 am), June Industrial Production (9:15 am), and Fed Chair Powell testifies again (9:30 am). The major earnings reports scheduled for the day include BK, CTAS, MS, PGR, TSM, TFC, USB, UNH, and WIT all before the open. Then, after the close, AA and WAL report.

It looks like the bears will make at least the first move today, trying to reverse the trend after yesterday’s indecisive Spinning Top candles. The Chinese data did not help, but Jobless Claims and Manufacturing indexes at 8:30 may well end up calling the tune early. Also, remember that earnings are underway with everything reporting so far this morning coming in as beats to the upside. Markets are still sitting near all-time highs, look extended, and are looking for direction. While it would be unlikely Fed Chair Powell would say anything new relative to his testimony to the other chamber yesterday, he does testify again this morning. So be aware of that potential driver as well.

Focus on your open positions first, don’t chase new ones, and remain nimble. The odds still favor sticking with the trend in terms of overall posture. And the long and mid-term trends remain bullish and have not been broken yet. So, stick to your trading rules, taking your profits, moving your stops, and maintaining your discipline. It is all about your decisions. Act with intention…don’t just react emotionally. Remember it is consistency that remains the key to long-term success.

Ed

Swing Trade Ideas for your consideration and watchlist: PM, LB, CEIX, TD, CLX, CSCO, WMT, DIS, CCRN. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

With the CPI coming in at its highest level since 1981, markets experienced some mild selling contrary to the frantic buying of late, leaving behind a bit of caution in the candle patterns. The most prominent being the potential shooting star pattern on the QQQ. I say possible because to be valid, the QQQ price must follow through to the downside today to confirm the signal, which may be a tall order with the recent big tech buying enthusiasm. That said, stay on your toes, avoiding complacency with another key inflation data point on its way this morning.

Asian markets traded mixed but mostly lower overnight due to inflation jitters of hot CPI numbers in the U.S. European markets trade modestly lower this morning as they cautiously monitor inflationary data. Ahead of the PPI numbers and big bank earnings, the U.S. futures are trying to put on a brave face pointing to flat to modest gains at the open. However, the PPI could easily inspire the bulls or bears, depending on the report. So stay focused and flexible and be ready for price volatility as the market reacts.

Economic Calendar

Earnings Calendar

On the Wednesday earnings calendar, we have about 20 companies listed that expect to report today. Notable reports include BAC, BLK, C, DAL, INFY, PNC, & WFC.

News & Technicals’

The CPI came in at the highest level since 1981 and slightly dampened buying enthusiasm with the worry the Fed may have to act sooner than expected. Today we will hear for BAC, C, WFC as the big investment banks report results. According to reports, hospitalizations are once again on the rise as the delta variant spreads throughout the country. In addition, Apple is reportedly ramping up production in anticipation of a big wave of phone upgrades to take advantage of 5g. Norwegian Cures Line is suing the Florida surgeon general to end the vaccine passport ban because they say it will force them to cancel cruises with its first sailing scheduled for August 15th.

Yesterday’s mild selling didn’t create much technical damage to the index charts, but it did offer a little caution by leaving behind some concerning candle patterns. The QQQ left behind a shooting star pattern that can sometimes signal a top, but it would require a bearish follow-through today for that to be valid. With the recent wild enthusiasm to buy big tech no matter the price, we will need a bit more proof of bearish price action to become worried. However, the IWM failing at its 50-day average creates some technical damage if it tries to lead the markets lower. We will get another reading on inflation this morning with the Producer Price Index, and if that were to come in higher than expected, it could overshadow the big bank earnings rolling out this morning. On the other hand, if the PPI comes in less than expected, I would not be surprised to see the market shrug-off inflation worries. Stay focused and flexible, prepared for price volatility as the market reacts to the data.

Markets gapped slightly lower Tuesday on a hotter than expected June CPI number. However, they rallied from there to new highs before giving back the gains in the afternoon and closing near the lows. This left us with Shooting Star-type candles in all 3 major indices. On the day SPY lost 0.34%, DIA lost 0.29%, and QQQ was dead flat. The VXX gained over a percent to 29.59 and T2122 fell all the way back to just inside the oversold territory at 19.30. 10-year bond yields spiked sharply to 1.42% and Oil (WTI) gained 1.6% to $75.30/barrel.

As mentioned, the Consumer Inflation numbers jumped the most in years. However, markets reacted very mildly to the news. Among the biggest movers by category, Car and Truck rental prices skyrocketed 88% year-on-year while gasoline and used cars both jumped 45% from a year ago.

This morning, weekly mortgage applications for new homes came in 8% above the prior week but were 29% lower than one year ago. However, refinancing applications spiked 20% on the week as buyers jumped on the recently falling interest rates.

In big bank news, after JPM’s blowout numbers Tuesday, this morning BAC missed expectations on revenue for Q2. BAC cited a drop in income due to lower interest rates over the quarter. However, the company did far exceed the earnings estimates of analysts ($1.03 actual vs $0.77 est.). On the other hand, C, WFC, BLK, and PNC all followed JPM’s lead in beating on both lines for the quarter…in some cases with blowout beats.

Overnight, Asian markets were red almost across the board. The only green came from Australia (+0.31%) and India (+0.26%). However, Shanghai (-1.07%), Shenzhen (-0.88%), and Hong Kong (-0.63%) were more representative of the region. Europe is following Asia’s lead so far today. While there are a few barely green exchanges, the FTSE (-0.52%), DAX (-0.17%), and CAC (-0.22%) are typical of the continent. As of 7:30 am, US Futures are pointing to a green, if mostly flat open. The DIA is implying a +0.02% open, the SPY implying a +0.10% open, and the QQQ implying a +0.36% open. 10-year bond yields and the dollar are also mildly lower in premarket, which should help commodities.

Major economic news scheduled for Wednesday is limited to June PPI (8:30 am), Crude Oil Inventories (10:30 am), Fed Beige Book (2 pm), and Fed Chair Powell testifies at noon. The major earnings reports scheduled for the day include BAC, BLK, C, DAL, INFY, PNC, and WFC. Then, after the close, there are no major reports.

The rest of the world seemingly reacted poorly to yesterday’s hot CPI reading in the US. However, US markets mostly ignored the news or maybe gave more weight to the blowout earnings reports yesterday. So far today, earnings news is mostly positive in front of the PPI number. In this setting, markets are showing signs of weakness. If we get some follow-through on the Shooting Star-type candles, don’t be surprised by at least a short-term pullback. Markets are still sitting at all-time highs, look extended, and with the higher inflation numbers, we can expect more talk of Fed tapering. However, Bloomberg reported Fed Vice Chair Clarida told them the Fed would not have the new information they value most to adjust posture until year-end.

The odds still favor sticking with the trend in terms of overall posture. And the long and mid-term trends remain bullish. Focus on your open positions first, don’t chase new ones, and remain nimble. Stick to your trading rules, taking your profits, moving your stops, and maintaining your discipline. It is all about your decisions. So act mindfully and with intention…don’t just react emotionally. Consistency remains the key to long-term success.

Ed

Swing Trade Ideas for your consideration and watchlist: CLF, QCOM, BX, VALE, WMT, TZA. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

First out of the gate early this morning, PepsiCo kicked off the 3rd quarter earnings season by crushing the estimates and raising forecasts. Soon to follow will be the possible market-movers JPM & GS setting new high records in the DIA, SPY, and QQQ in anticipation. Let’s hope companies can produce the results that support these very lofty valuations! Except for considerable price volatility and possible morning gaps as traders and investors react to the data.

Overnight Asian markets mostly higher, with the HIS leading the way, advancing 1.63%. Europe markets are taking more of a wait-and-see stance with mixed and muted results this morning. Ahead of big bank reports and the latest reading on CPI, U.S. Futures trade mixed but primarily flat. There is a lot at stake this earnings season due to the high valuations so consider your risk carefully as the fireworks begin.

Economic Calendar

Earnings Calendar

Today we kick off the 3rd Quarter earnings season with 12 companies listed to report. Notable reports include CAG, FAST, GS, JPM, KRUS, & PEP.

News & Technicals’

Kicking off the 3rd quarter PepsiCo crushes estimates, and the company raises forecasts seeing a return of demand from foodservice customers. We will hear earnings results from both major market movers JPM and GS this morning. France, the Netherlands, Greece, and Spain all announced new restrictions on Monday in a bid to curb the rise in Covid infections. At the same time, the U.K. confirmed that it would lift its remaining restrictions on July 19th despite its infection rate remaining high. According to Husein Kanji, a partner at Hoxton Ventures, ‘this feels a lot like 1999,’ with tech venture investors writing bigger checks than ever before. A record 249 firms achieved $1 billion “unicorn” valuations in just the first half of 2021, doubling those produced last year. Treasury yields moved higher this morning, with the 10-year up four basis points to 1.368% and the 30-year climbing just one basis point to 1.994%.

The DIA, SPY, and QQQ continue to surge to higher highs with little regard to the inflated valuations as the frenzy of buying continues. New record highs have become so commonplace this year it’s barely newsworthy. However, the 3rd quarter earnings expectation energy is palpable with the big question can companies produce enough to support these lofty prices? Technically the T2122 4-week new high/new low ratio signals a possible over-bought condition, while the Absolute Breadth Index points to an extreme divergence with the index leaders. Though it’s become very redundant, I will continue to suggest we stay with the trend as long as it lasts but avoid over-trading and guard against complacency. We can expect some wild earnings fueled price volatility with substantial morning gaps, so plan your risk accordingly.

Monday saw a mixed but modest open followed by some trending the first hour. After that, the rest of the day was a sideways grind in a narrow range that closed near the highs. This left us with strong white candles in both of the large-cap indices and a Doji in the QQQ. All 3 indices closed at yet another new all-time high close. On the day, SPY gained 0.37%, DIA gained 0.37%, and QQQ gained 0.39%. The VXX lost two-thirds of a percent to 29.23 and T2122 remains in the overbought territory at 85.92. 10-year bond yields rose to 1.37% and Oil (WTI) fell half a percent to $74.14/barrel.

During the day, the NY Fed released its June consumer survey. The survey found the median expectation of inflation for the next 12 months had jumped to 4.8%, the highest reading in the history of the survey. The survey also found consumers expect that unemployment will fall over the same time. Given this survey’s results, June CPI numbers are expected to come in hot this morning.

Also during the day, TSLA CEO Elon Musk testified in a shareholder lawsuit over the company’s purchase of SolarCity. The suit alleges the purchase amounted to a bailout that came at the expense of TSLA shareholders. Other TSLA board members had already settled their portion of the liability for $60 million. However, Musk refused. Early in his testimony Musk said he did not see a financial gain from the purchase, but it was part of his 2006 “master plan.”

Late in the day, the FDA announced a new warning will be added to the JNJ covid vaccine. The warning will inform the public that the vaccine has been linked to a rare, but serious, autoimmune disorder. However, regulators emphasized that the risk is tiny (100 cases found out of 12.8 million doses administered). JNJ stock fell sharply intraday on the news, but still ended flat on the day.

Overnight, Asian markets were mostly strongly green. Japan (+2.25%) and Shenzhen (+2.14%) were major outliers to the upside mixed. Nonetheless, the region was green with Taiwan (+0.87%), South Korea (+0.89%), and Australia (+0.83%) being typical. In Europe, we see a divergence. The 3 major bourses are all red. However, the entire rest of the continent is green at this point in the day. The FTSE (-0.61%), DAX (-0.10%), and CAC (-0.33%) all seem to be waiting on a cue from the US. As of 7:30 am, US Futures are mixed. The DIA is implying a -0.43% open, the SPY implying a -0.23% open, and the QQQ implying a +0.20% open.

Major economic news scheduled for Tuesday is limited to June CPI (8:30 am), Jun Federal Budget Balance (2 pm), and two Fed speakers (Bostic at noon and Bostic at 2:30). The major earnings reports scheduled for the day include CAG, FAST, FRC, GS, JPM, and PEP before the open. Then, after the close, AMX reports.

Early this morning, both GS and JPM posted strong beats for Q2. GS reported especially strong numbers based on banking around a very strong IPO market. BA also halted deliveries of its “787 Dreamliner” jets again when another flaw was found. This is the second halt to deliveries of the wide-body plane in the last year, with the previous stoppage lasting 5 months. Finally, France fined GOOG $593 million in a “news copyright” case where France found GOOG did not negotiate in good faith with the original publishers of news stories it reused.

Markets are still sitting at all-time highs, look extended, and at least the Nasdaq showed signs of indecision Monday. A little rest or even a small pullback should not be unexpected. However, the odds still favor sticking with the trend…and the trend remains strongly bullish. Focus on your open positions first, don’t chase new ones, and remain nimble. Keep following your trading rules, taking your profits, moving your stops, and maintaining your discipline. “Your” is the key word. It is all about your decisions. So act mindfully and with intention…don’t just react emotionally. Consistency remains the key to long-term success.

Ed

Swing Trade Ideas for your consideration and watchlist: No Tickers today. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Friday opened with a gap higher followed by a morning rally and then a sideways grind in a tight range all afternoon. This left strong bullish candles that closed near the highs in all 3 major indices. As a result, all 3 major averages also closed at new all-time high closes. On the day, SPY gained 1.07%, DIA gained 1.26%, and QQQ gain 0.62%. The VXX fell almost 7% to 29.43 and T2122 jumped from deep in the oversold area to deep in the overbought territory at 92.04. 10-year bond yields spiked back to 1.361% and Oil rose 2.4% to $74.69/barrel. These moves were helped by a weaker dollar that aided most commodity prices.

During the day, President Biden signed a wide-ranging executive order aimed at cracking down on anti-trust activities. The 72 clauses included recommendations to Federal agencies as well as actual prohibitions. Among the major points was the reversal of the Trump-era “ending of net neutrality.” This means that the telco, cable, and ISP companies cannot throttle specific websites unless they pay for a fast lane. (The classic example is NFLX traffic cannot be slowed and the customer cannot be charged more for NFLX usage than any other content.) Another major item is the “Right to repair,” where companies like AAPL must now allow customers to have their devices repaired wherever they like (as opposed to AAPL requiring you to just purchase new or only get repairs from AAPL itself). Another clause will allow the importation of cheaper Canadian prescription drugs. Many of the aspects of this executive order are sure to be taken to court.

In some potentially ominous news out of China, the PBOC cut the size of reserves that Chinese Banks must hold in reserve on loans. This move will inject $154 billion into their economy and is intended to stimulate more lending (and thus economic activity). This is both a sign the Chinese recovery might not be as robust as most assumed and that the Chinese government is reacting quickly. Late last week, Bloomberg reported an economist poll saying Chinese growth had fallen from over 18% (Q1) to 8% (Q2). Obviously, a slowing recovery means lower earnings potential and less consumer spending. China led the way going into and coming out of the pandemic recession. So, as a read-through, this may indicate that the US Administration and Fed are right to be concerned about removing stimulus too soon.

G-20 Finance Ministers and Central Bank Heads endorsed the global minimum corporate tax over the weekend. However, Sunday Treasury Sec. Yellen told reporters the mechanism to make it work may not be ready for Congressional approval until the Spring of 2022. She did say that she hoped to put the provisions into a budget reconciliation (which could be approved by a simple majority of Congress). The global minimum corporate tax initiative would also end unilateral taxes on digital services by individual countries (such as France and a few other European countries have imposed on major tech firms like FB, AAPL, and GOOG).

Overnight, Asian markets were mostly strongly green. Japan (+2.25%) and Shenzhen (+2.14%) were major outliers to the upside mixed. Nonetheless, the region was green with Taiwan (+0.87%), South Korea (+0.89%), and Australia (+0.83%) being typical. In Europe, we see a divergence. The 3 major bourses are all red. However, the entire rest of the continent is green at this point in the day. The FTSE (-0.61%), DAX (-0.10%), and CAC (-0.33%) all seem to be waiting on a cue from the US. As of 7:30 am, US Futures are mixed. The DIA is implying a -0.43% open, the SPY implying a -0.23% open, and he QQQ implying a +0.20% open.

Major economic news scheduled for Monday is limited to the WASDE Report (noon) and the 10-year bond auction (1 pm). (The former being the USDA estimates on world Ag production.) There are no major earnings reports scheduled for the day. However, we should note that earnings season starts up again Tuesday.

Richard Branson (SPCE) beat his billionaire rivals into space during a short ride Sunday. (Although Jeff Bezos (AMZN) and others argue over whether the SPCE flight went high enough to be considered in space. Either way, the news looks to be goosing the SPCE stock (albeit with big volatility) in the premarket. With Earnings season kicking off Tuesday, do not be surprised if there is some movement in financials as traders make pre-report bets on the banks as well as the overall economy.

Markets sit at all-time highs and are extended according to many measures. So, a little rest or pullback should not be unexpected. The odds still favor sticking with the trend. Focus on your open positions first and don’t chase. Remain nimble or hedged. Keep following your trading rules, taking your profits, moving your stops, and maintaining your discipline. Consistency remains the key to long-term success.

Ed

Swing Trade Ideas for your consideration and watchlist: No Tickers today. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Thursday was wild ride with all three major indices gapping down 1.3%, grinding sideways until 11 am, and then rallying for a couple of hours before fading late in the day. Support seemed to hold in all 3, but this left large-body candles with wicks at both ends in all the indices. So, while the bulls refused to roll over, you’d have to say that on balance it was the bears that were in control. On the day, SPY lost 0.80%, DIA lost 0.73%, and QQQ lost 0.58%. The VXX gained 6.5% to 31.54 and T2122 dropped all the way down deep into the oversold territory at 7.93. 10-year bond yields fell yet again to 1.293% (which was actually up significantly from the 1.25% it hit in premarket) and Oil (WTI) rose 1.29% to $73.13 on a falling dollar.

The White House announced that President Biden will sign an executive order that cracks down on anti-competitive practices in big tech, labor, and other sectors. This order directs a dozen federal agencies on how to approach corporate consolidation and antitrust. There are 72 specific actions outlined in the order, but details are not yet available. What is known is that the White House is calling the changes “sweeping.”

PFE also made post-market news, saying that immunity provided by their vaccine has begun to wane and announcing they will seek FDA approval for clinical trials of a new Covid Booster Shot. The company also said it believes that immunity will require an additional booster 6-12mo. following completion of their 2-dose original regimen. The booster they have been developing specifically targets the highly contagious Delta variant and trials could start in August if approved. However, the CDC, FDA, and NIH commented that the waning of immunity has not yet been demonstrated and they will analyze the data as it comes in.

In banking news, yesterday WFC closed its “personal line of credit” business, angering thousands of customers. The reported reason is so that the bank can focus on credit card and personal loan lines of business. Meanwhile, overnight MS reported that there was a breach of customer data from one of the stock-plan businesses they operate. The company said they have already contacted the customers who were impacted.

Overnight, Asian markets were mixed but leaned to the red side. Taiwan (-1.15%), South Korea (-1.07%), and Australia (-0.93%) paced the losses. In Europe, markets are green across the board so far today. The region is seeing significant rebounds from Thursday as the FTSE (+0.69%), DAX (+0.92%), and CAC (+1.73%) are indicative of the continent. As of 7:30 am, US Futures are looking to rebound as well, but in a mixed fashion. The DIA is implying a +0.67% open, the SPY implying a +0.41% open, and the QQQ implying a flat -0.02% open. 10-year bond yields are also up sharply to 1.341% overnight.

Major economic news scheduled for Friday is limited to the Fed Economic Policy Report (11 am). The only major earnings report scheduled for the day is GBX before the open.

Markets seemed to have found a little support Thursday after the nasty gap down. The bulls refused to roll over, but the bears were also not done fighting as of day end. It looks like the day will start with the bulls attempting to follow through on their rally off the lows yesterday. That said, a single gap down did not do a lot to relieve what many consider too long of a run without a pullback. So, be careful. As mentioned yesterday, one candle does not indicate a trend change. However, it also does not take out all the sellers who have been waiting to pounce.

The odds still favor sticking with the trend. However, at some point, all trends fail. Those points of indecision are a good place to step back and wait on things to shake out. You DO NOT have to trade every day. So, consider whether this is your market condition or not. If you do trade, focus on your open positions first and be more nimble or hedged. Keep following your trading rules, taking your profits, moving your stops, and maintaining your discipline. And remember it’s Friday…payday. And maybe a time to lighten up for the weekend.

Ed

Swing Trade Ideas for your consideration and watchlist: AGEN, AKAM, FUBO, CLRE, SNOW, UNG, TGT, NET, CUBE, IT, LE, MDLZ, NSA, CLX, WFG, SPCE. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Large caps opened flat while the Nasdaq gapped higher again on Wednesday. All 3 major indices then waffled sideways the rest of the day. This left the QQQ and SPY as Hanging Man type candles at new all-time high closes and the DIA as a Bullish Harami candle in a consolidation. On the day, SPY gained 0.35%, DIA gained 0.32%, and QQQ gained 0.21%. VXX ended flat at 29.63 and T2122 rose but remains on the Southside of the mid-point at 39.31. 10-year bond yields continued to fall significantly to 1.321% and Oil (WTI) fell 1.75% to $72.09/barrel.

During the afternoon, the June Fed Meeting Minutes were released. The minutes showed the Fed kept a very patient tone in their discussions about tightening policy or even tapering bond purchases. While a couple of members noted faster economic progress than expected, the consensus was that “substantial further progress” was needed before any tightening started. Meanwhile, in Europe, the ECB came into alignment with the Fed in that they have adopted 2% inflation as their goal and will allow over-shoots.

After-hours it was reported by Bloomberg that many states will file suit against GOOG. The antitrust lawsuit, being worked on by several states Attorneys General, alleges the GOOG illegally abused its power over developers in their App Store. The suit will supposedly be filed in CA by end of day. This is a separate suit to the one filed by DOJ and a few states (which was dismissed by a Federal Judge on appeal) over similar antitrust issues.

The dollar slid a quarter of a percent last night as 10-year bond yields also fell again (6 basis points), touching 1.25% at one point. The purported causes were concerns over economic growth and the new Delta variant of Covid-19 (coupled with low vaccination rates across the South and within certain demographics). However, it’s unclear what growth this would relate to given economic projections…and so far the only significant resurgence of Covid is in southern MO.

Overnight, Asian markets leaned heavily to the downside with the only green coming from a couple exchanges that barely broke even. Hong Kong (-2.89%), Thailand (-2.09%), Malaysia (-1.40%), and Singapore (-1.08%) paced the losses. Part of the reasoning is that there may be serious risk to investors on Chinese companies listed in Hong Kong and the US due to a regulatory crackdown. In Europe, markets are following Asia, as losses are widespread and significant at mid-day. The FTSE is showing -1.88%, The DAX -1.91%, and the CAC -2.37% at this hour. As of 7:30 am, US Futures are pointing to American exchanges following Europe and Asia. The DIA is implying a 1.29% gap down, the SPY implying a 1.22% gap lower, and the QQQ implying a 1.25% gap down at the open.

Major economic news scheduled for Thursday is limited to Weekly Initial Jobless Claims (8:30 am) and Crude Oil Inventories (11 am). The only major earnings report scheduled for the day is LEVI after the close.

Markets have looked toppy the last couple of days, but the bulls refused to give an inch. It seems the bears have found some real energy this morning following up on global weakness and deflationary moves. So, the fickle Mr. Market has swung from fear the economy would be too hot (and the Fed would take away stimulus) to fear the economy is not hot enough. These manic swings over things that will take months (at a minimum) to work out are a clear sign of indecision and volatility. So, the bears may push today, but don’t be too certain one candle indicates a major market shift.

All trends reverse at some point and that’s exactly what we will see this morning as the short-term strong bull trendlines are broken. However, a trend break or even a pullback does not necessarily mean a shift to a bear market. It doesn’t even necessarily mean long-term technical damage. Bearish moves tend to be fast and short. So, be very careful trading in a volatile, broken-trend market until things shake out. You do not have to trade every day. If you do trade, focus on your open positions first and be more nimble or hedged. Follow your trading rules, keep taking your profits, moving your stops, and maintaining your discipline.

Ed

Swing Trade Ideas for your consideration and watchlist: No Tickers today. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Yesterday we were reminded that bears are still around and hungry. It was all big tech holding up the market yesterday as most everything else slipped sideways or south. Their market dominance is clear, but one must wonder how much longer tech can maintain this buying pressure as valuations soar and P/E ratios hit new record highs. If nothing else occurred yesterday, the bears gave us a warning not to become complacent. Stay with the trend but stay focused and flexible because bear attacks and price volatility could signal a top is near.

Asian markets closed mixed overnight in a choppy market session. European markets are primarily bullish this morning, keeping an eye on the muted global sentiment. Ahead of the JOLTS number and the FOMC minutes, U.S. futures are trying to shake off yesterdays selling as the QQQ gaps to yet another record high as the big tech party continues.

Economic Calendar

Earnings Calendar

On the Wednesday earnings calendar, we have just eight companies listed and only four verified reports. Notable reports include MSM, SAR & WDFC.

News & Technicals’

With mass pandemic vaccinations continuing across the country, health officials warn we could see a harsh flu season this winter due to the minor season in 2020. Biden is now suggesting door-to-door efforts to increase the number of vaccinations in areas where there are low acceptance rates. At the same time, France is preparing a new law to make the Covid vaccination compulsory for those in the health care industry. The European Central Bank is now raising its forecast to a 4.8% growth rate this year with 4.5% in 2022, raising some inflationary concerns. China’s crypto-crackdown called for the shutdown of a company “suspected” of providing software services for virtual currency transactions. With the FOMC minutes just around the corner, the 10-year Treasury yield dipped this morning to 1.338%, and the 30-year fell to 1.967%.

The bears reminded us yesterday that they are still around and hungry, with the IWM testing its 50-day average and the DIA suggesting a possible test. However, trends remain bullish, and the rally back yesterday afternoon raises the question if the bears have the energy to follow through on yesterday’s threat. That said, the VIX indicated a modest increase in fear, and the Absolute Market Breadth Index saw its first increase in days on the selling wave. So there may be a reason some caution but no reason to run for the door just yet. Instead, consider this a warning shot over the bow not to overtrade or become complacent with valuations so elevated. We know a correction is way overdue and could begin at any time but stay with the trend until then.