With the NASDAQ setting a new record, and the SP-500 within striking distance, the index technicals’ improved through overhead resistance in the DIA, IWM, and SPY are still a concern. The Dow remains the most significant concern after rallying 670 points off Friday’s low; it must yet deal with its 50-day average as resistance. Despite antitrust probes and bipartisan-supported proposed antitrust legislation, the tech giants did the vast majority of the market recovery, with Microsoft briefly hitting a two trillion market cap. We’ve come a long way in just two trading days. Remember to take some profits!

Asian markets traded mixed overnight, but the HSI was on fire, surging 1.79% by the close. With a stronger than expected PMI and inflation worries creeping in, European markets trade primarily in the red this morning though the FTSE is clinging to modest gains. Ahead of earnings and housing data, the U.S. futures currently suggest a flat to modestly bullish open. As you plan your day, keep a close eye on overhead resistance levels that may harbor entrenched bears.

Economic Calendar

Earnings Calendar

On the hump day earnings calendar, we have nine companies listed on the calendar though some are unconfirmed. Notable reports include FUL, INFO, PDCO & WGO.

News & Technicals’

Although pressed several times pressed with hyperinflation questions, Jerome Powell stuck to his guns, suggesting the recent spike is likely temporary. All we can do is hope he’s right as the Fed continues to pump 120 billion a month into the system. The China crypto crackdown continues to impact Bitcoin prices falling below 30,000 once again. The new Delta variant of Covid is likely to become the dominant strain in the next couple of weeks, according to Dr. Fauchi. He has declared this strain as the greatest threat to the attempt to eliminate the virus. In the U.K., consumer price inflation came in 2.1%, and chief economist Andy Haldane urges policymakers to cut their quantitative easing program or risk what he calls the “tiger of Inflation” incoming. The Eurozone business activity surged to its highest levels in 15-years. However, as inflation worries crop up worldwide, U.S. Treasury yields saw little movement this morning, with the 10-year holding at 1.472% and the 30-year drifting slightly lower to 2.102%.

The index technicals improved substantially, with the tech giants doing the vast majority of the heavy lifting. The NASDAQ closed at a new record high, and the SPY is within striking distance of new records though the index has more stocks moving sideways to down than those moving up. The DOW remains the weakest of the indexes, still below its 50-day average though it has surged 670 points off Friday’s low in just two trading days. The VIX has calmed substantially but has not made a new low as one would expect, with new index records being set. That said, traders should remain vigilant as huge price volatility is possible with the DIA, SPY, and IWM still facing overhead resistance. Remember, when the market moves big, it’s a good idea to take some profits along the way.

Markets opened flat Tuesday and then rallied most of the day as bulls delivered some follow-through to Monday’s bullish reversal of last week’s action. However, a selloff the last half hour of the day took stocks out away from their highs. DIA was by far the least positive of the 3 major indices, printing a white-bodied Spinning Top candle. However, the SPY and QQQ put in stronger bullish candles. On the day, QQQ closed up 0.93% (to an all-time high close), SPY gained 0.53% (half a percent shy of a new all-time high), and DIA gained 0.20% and remains the laggard. The VXX fell 5% to 30.87 and T2122 rose 1%, but remains just outside the overbought territory at 78.79. 10-year bond yields fell slightly to 1.465% and Oil (WTI) was off eight-tenths of a percent to $73.08/barrel as the dollar fell again.

During the afternoon, Fed Chair Powell’s prepared remarks (for his House testimony) were released. In the prepared statement, Powell said the Fed will “soon begin discussing” the tapering of QE (bond buying). However, in questioning, he was very positive about the economic comeback and continues to maintain the position that the inflation being seen now is temporary in nature. Powell said it is “very, very unlikely” that the US will see 1970s-type inflation. He also repeatedly said that the pandemic remains a risk, specifically noting the slowing in the pace of vaccinations and the Delta variant of the virus.

Bloomberg reported that semiconductor order lead times increased another 7 days during May. The wait time on an average chip order (regardless of industry) is 18 weeks. However, the primary cause of the increase in wait time is phone chips, which saw an increase to almost 26 weeks lead-time. However, the report Bloomberg cited said that chipmakers like AVGO are cautioning against reading this as massive demand. The CEO of AVGO told Bloomberg this is more of a case of their customers coming to terms with a not-just-in-time supply chain. (Which means every link in the chain is just building inventory buffers now and that inventory will be worked back down in the future.)

Bitcoin briefly fell below $30,000 on Tuesday before rallying back to close just under $33,000. The pullback put fear into crypto markets as a Death Cross set up and weak hands ran for the doors. Bitcoin-related stocks (like MSTR and GBTC) suffered great volatility and/or losses on the day. Overnight Bitcoin continued its rebound rally and is trading near $34,000 in the premarket.

Related to the virus, new US infections are flat. The totals rose to 34,434,803 confirmed cases and deaths are now at 617,875. These numbers are now under-reported again as some (mostly Southern) states have decided to stop reporting data on a daily basis. Nonetheless, on the data we do have, the number of new cases is flat and at an average of 11,775 new cases per day (the lowest number since March 2020). Deaths continue to fall and are now down to 306 per day (again, the lowest number since March 2020). The White House said Tuesday that the country will not meet its stated goal of 70% of American adults having received at least one vaccine shot by July 4. They went on to say we are now on pace to be at 67% of adults in that state by the holiday. We will also come up short on the goal of 160 million Americans being fully vaccinated by that date, now being on a pace to be at 151 million as of Independence Day.

Overnight, Asian markets were mixed, on mixed trading. For example, Japan was dead flat, but Hong Kong (+1.79%), Taiwan (+1.53%), and Shenzhen (+1.00%) made nice gains. Meanwhile, Indonesia (-0.88%), Australia (-0.60%), and India (-0.54%) were down a bit. In Europe, markets are mostly in the red so far today. The FTSE (+0.23%) is an outlier, but the DAX (-0.67%) and CAC (-0.59%) are typical of the continent at this point in their day. As of 7:30 am, US Futures are pointing to a dead flat open. The DIA is implying a +0.04% open, the SPY is implying a -0.02% open, and the QQQ is implying a -0.04% open at this hour. Commodities are largely higher overnight with the Dollar down slightly.

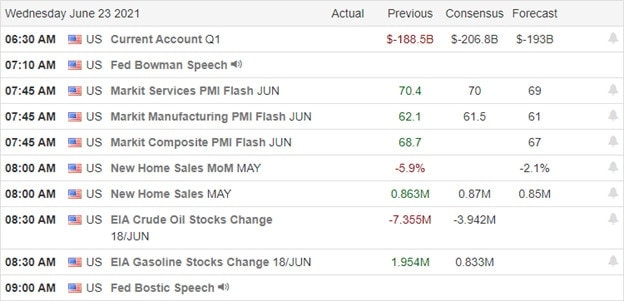

The major economic news scheduled for Wednesday includes Q1 Current Account (8:30 am), Manufacturing PMI (9:45 am), Services PMI and May New Home Sales (both at 10 am), Crude Oil Inventories (10:30 am), and multiple Fed speakers (Bowman at 9:10 am and Bostic at 11 am). Major earnings reports on the day include INFO, PDCO, and WGO all before the open. Then after the close CNXC, FUL, KBH, and SCS all report.

Inflation and the fear of Fed tightening continue to be the main talking points for the market. This comes despite some glaring examples in the other direction. For example, Lumber prices are down almost 50% and Corn is down 27% from the peaks in early May. Meanwhile, companies that use lumber and corn have pricing power…and their prices are not falling. So, they are reaping greater profits. In a perfectly efficient market, you might expect a huge rally in Housing and Food sectors, but that has not been the case since early May. The point is that it is not news, but the fear and rumor related to news that is drives markets. So, focus on the reaction and not the news itself in your trading.

The odds still favor following the trend and respecting support and resistance levels. That doesn’t really help in terms of the large caps, but the QQQ is still holding the bullish trend. Still, all trends reverse at some point and every S/R level is breached eventually. So, don’t just assume trend, support, or resistance will always hold. Keep locking in profits, moving your stops, and maintaining discipline. Follow your trading rules, don’t chase, and stick to the trade plan. Remember that consistency is the key to long-term trading success.

Ed

Swing Trade Ideas for your consideration and watchlist: AMSC, RIOT, MRO, NKLA, FANG, PTON, RUN, EXPR, PLUG. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Monday was a risk-on day across the market. The large-caps gapped up about half a percent and then all three major indices followed-through to the upside all morning. The afternoon saw a grind sideways in a tight range. This left us with strong white candles in both large-cap indices and a Bullish Engulfing Hammer-type candle in the QQQ. On the day, SPY gained 1.40%, DIA gained 1.75%, and QQQ gained 0.48%. The VXX fell 6% to 32.58 and T2122 shot higher to just outside the edge of the overbought territory at 77.88. 10-year bond yields spiked, but remain lower, at 1.492% and Oil (WTI) spiked 2.76% to $73.62/barrel. This came as the dollar fell which caused commodity price rises as a result.

During the day Monday bitcoin made news several times. The cryptocurrency fell below $32,000, before settling at $32,300. This came as China extended its crackdown on crypto-mining operations both geographically and ordering AliPay (online payments company) to do no business with entities related to crypto. Jim Cramer also told his colleagues that he has sold “almost all” of his bitcoin holdings. In a case of either bad or good timing (depending on how you look at it), MSTR announced they bought over 13,000 more bitcoin and their bitcoin holdings to $3 billion. (However, their average cost for bitcoin purchase is $37,000…so they are underwater and averaged down today.)

In miscellaneous business news, after the close, XOM announced it will cut 10% of its white-collar staff annually, following the GE model from the Jack Welch years. Meanwhile, DAL announced it plans to hire 1,000 new pilots by next summer. RIDE is taking heat from many of the print and electronic media sources, because top executives sold off major chunks of their stock in February, prior to the release of the company’s terrible quarterly earnings in March. CNBC also reported that SAFM is exploring the sale of the company to private ag investment firm Continental Grain. The idea is to take advantage of the high price of chicken. Early Tuesday, the EU announced a new investigation into GOOG for antitrust behavior related to ad technology.

Related to the virus, new US infections continue to fall. The totals rose to 34,419,838 confirmed cases and deaths are now at 617,463. These numbers are now under-reported again as some states (mostly Southern) have decided to stop reporting data on a daily basis. Nonetheless, on the data we do have, the number of new cases is flat and at an average of 11,502 new cases per day (the lowest number since March 2020). Deaths continue to fall and are now down to 300 per day (again, the lowest number since March 2020). However, it appears we may have made the common mistake again of getting too complacent. The Delta (Indian) variant continues to surge. For example, Missouri has seen a six-fold increase in hospitalizations, due to the new variant and a lack of vaccinations coupled with ending restrictions. Where the Delta variant made up just 10% of cases, Delta now accounts for 90% of the cases and almost all those patients are unvaccinated.

Overnight, Asian markets were mixed but mostly green. The most notable move came as Japan (+3.12%) surged back from its Monday hammering. Indonesia (+1.53%) and Australia (+1.48%) were the other two notable movers. Hong Kong (-0.63%) was the leader of those in the red. In Europe, a similar story is shaping up as of midday. The FTSE (+0.38%), DAX (+0.10%), and CAC (+0.19%) are typical, but there are half a dozen exchanges in the red across the continent. At 7:30 am, US Futures are flat. The DIA is implying a +0.04% open, the SPY implying a +0.11% open, and the QQQ implying a +0.26% open.

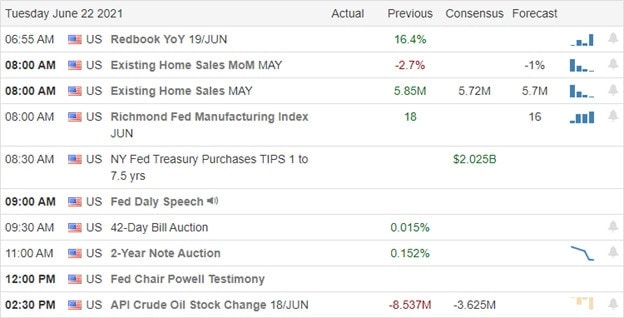

The limited major economic news scheduled for Tuesday includes May Existing Home Sales (10 am), Fed member Daly speaks (11 am), and Fed Chair Powell testifies at 2 pm (the first of two days of testimony). There are no major earnings reports scheduled for the day.

Interest rates are up slightly and Oil down two-thirds of a percent during premarket today. The dollar is also slightly stronger, which gives commodities in general a boost. With conflicting stories coming from different Fed members the last several days, don’t be surprised if markets bide their time until Chairman Powell testifies this afternoon. Undoubtedly he will be grilled from both sides of the aisle on exactly when tapering of bond-buying and then interest rate hikes may begin. Those are obviously keys to the market psyche.

The odds still favor following the trend and respecting support and resistance levels. That doesn’t really help in terms of the large caps, but the QQQ is still holding the bullish trend. Still, all trends reverse at some point and every S/R level is breached eventually. So, don’t just assume trend, support, or resistance will always hold. Keep locking in profits, moving your stops, and maintaining discipline. Follow your trading rules, don’t chase, and stick to the trade plan. Remember that consistency is the key to long-term trading success.

Ed

Swing Trade Ideas for your consideration and watchlist: HES, SFIX, LLY, CNC, KR, SPGI, LYFT, PLTR, FSR, MRO, FUBO, BA, RIG, CDEV, ICPT, PACB, WISH. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

After Friday’s ugly selloff, the relief rally to fill the bearish gap was a nice reprieve. The SPY and IWM recovered nicely, closing above their 50-day averages, while the DIA remains the weakest index with substantial overhead resistance yet to overcome. Speculation and emotion are running high, as evidenced by the back-to-back 600 point swings. The wild price action favors day traders but makes it near to impossible to have an edge as a swing or position trader. Be very careful chasing buys as we test overhead price resistance levels that may have entrenched bears willing to defend.

Overnight Asian mostly rallied, with the NIKKEI leading the way, surging 3.12% through the HSI continued to drift south. European market trade mixed this morning with modest gains and losses as trade inflation and interest rate fluctuations. Ahead of a light earnings calendar and Housing numbers around the corner, U.S. futures have bounced off overnight lows but currently point to a flat open. After yesterday’s big relief rally, a little rest is not out of the question.

Economic Calendar

Earnings Calendar

On the Tuesday earnings calendar, we have just eight companies listed, with only half verified. Notable reports include KFY and PLUG.

News & Technical’s

The assault on the big tech’s continue with European Commission opened an antitrust investigation into Google. According to the report, the probe is looking into the advertising unit that has made it harder for rival online advertising services to compete. China’s illegalization of nongovernmental sanctioned cryptocurrencies has taken a toll on Bitcoin that has lost $300 billion in value since last Friday. Chinese authorities in the Sichuan province ordered crypto miners to shut down operations, and the Bank of China urged financial institutions not to provide crypto services. Fed Chairman Jerome Powell said in testimony prepared for delivery to Congress that the economy is growing, but faces continued threats from the Covid pandemic. He said inflation has risen “notably” but repeated his position that the price pressures are transitory. He has a story, and he’s sticking to it! The 10-year treasuries yields increased slightly this morning to 1.501%, and the 30-year advanced to 2.115%.

Yesterday’s relief rally filled the bearish gap left behind in Friday’s price action in the DIA, SPY, and IWM. The DIA remains the worst technical condition remaining below its 50-average with substantial overhead price resistance yet to overcome. However, the SPY and IWM recovered their 50-day averages but still have to price resistance levels above to yet to overcome. The SPY remains in a bullish trend even as semiconductor stocks suffered a pullback due to the China crypto mining crackdown. I wouldn’t call the 600 point swings in the last two days trading days healthy price action. In fact, it’s difficult to impossible for swing and position traders to have an edge in this kind of trading environment. Big price swings and high volatility favor the day trader. As the index charts approach price resistance levels, be prepared for the possibility of bearish pushback. Expect price volatility to remain high, with large intraday whipsaws and overnight reversals possible.

As the bears rode roughshod over the market to end the trading week, some significant technical damage was created in the index charts. With more economists warning of a possible 10 to 20 percent correction, price volatility can become quite extreme as emotions run high between those wanting to rush in and buy the dip and those welcoming the correction in prices. If this is the beginning of a correction, big daily price swings are possible with overnight reversals and intraday whipsaws to challenge trader skills. Observe price resistance levels as possible areas of bear attacks.

Asian markets had a rather rough night of trading with the Nikkei, leading the selling down 3.29%. However, European markets are trying to bounce off last week’s lows this morning, showing green across the board but modest gains thus far. Here in the U.S., we don’t do modest much anymore. We either rush in or run for the door, and this morning is no exception, with futures surging higher off of overnight lows. Watch for violent price action and big price swings as the bull and bears duke it out in early trading.

Economic Calendar

Earnings Calendar

We have another light day on the earnings calendar to begin a new week of trading with just five companies listed with the report from NPSNY as only one verified.

News & Technicals’

Bitcoin fell 7% Monday morning as the China crackdown on cryptocurrency mining extended to the southwestern provinces of Sichuan. Another economist Mark Zandi has joined the chorus of economists warning that inflation headwinds could create a 10 to 20 percent correction. Adding it may take a year to recover to just the break-even level. Staffing issues that are in turn creating maintenance issues have caused American Airlines to cancel hundreds of flights. According to the report, about half the cancellations were because of unavailable flight crews. Supply chain issues are likely to affect the Amazon Prime Day sales that began at midnight Monday. Businesses reported they are being hit hard by global shortages of shipping and semiconductors, while some worry they may run out of stock during the massive sales event. Treasury yields have fallen to a two-month low, with the 10-year trading at 1.438% this morning as the 30-year rose slightly to 2.043%.

A rough week of selling left some significant technical damage in the index charts. The SPY, DIA, and IWM closed below their 50-day averages. The QQQ fends off the bears as the tech giants resisted the selling pressure holding onto price support levels as well as the current bullish trend. Fear spiked, closing the VIX above a 20 handle and well above its 50-day average while the Absolute Breadth Index registered a rise in momentum on the selling wave. If this is the beginning of a correction, we can expect the price action to become very volatile, with overnight reversals and intraday whipsaws becoming commonplace. This morning a short squeeze may be possible but be careful with rushing in to buy the dip if prices remain under resistance levels where the bears might be digging in defenses. Big daily price swings are possible, so plan your risk carefully and avoid complacency.

Friday was a kick in the teeth for Bulls as the large-caps gapped down well over one percent and then markets ground sideways all day up until a strong selloff the last 5 minutes of the day. This left the QQQ holding onto the uptrend by the skin of its teeth on a black spinning top and the large-cap indices printing ugly bottom-heavy black candles. On the day, SPY low 1.67%, DIA lost 1.68%, and QQQ lost 0.78%. The VXX shot almost 9% higher to 34.69 and T2122 dropped back to mid-range at 53.15. 10-year bond yield fell strongly again to 1.441% and Oil (WTI) rose almost three-quarters of a percent to $71.56. This closed out the worst week for markets since October for large-caps, especially the mega-cap DIA.

During the day Friday, Fed members issued dueling opinions in interviews. Non-voting Fed member Bullard said he could foresee a rate hike coming as soon as 2022 with both the economic gains and inflation running hotter than expected. However, shortly afterward, voting Fed member Kaskari told an interview that he wants to keep the short-term interest rate near zero through at least 2023 (another 2.5 years). He went on to say he believes the current inflation is being caused by supply chain constraints during the opening and will subside by year end. More importantly, he said that he hopes and expects any change in FOMC policy (including bond-buying tapering) will be slow and orderly. Fed Chain Powell gets his say later this week when he testifies before both houses of Congress.

In miscellaneous business news, AAL had to cancel 180 flights (about 6% of its normal schedule) this weekend due to maintenance issues and staffing shortages. Monday is the start of AMZN’s 2-day “Prime Day” event. However, supply chain issues (backlogs at ports in China and the US) that are adding 2-3 weeks to resupply timelines are likely to cause major headaches and limitations on what is available to sell. The same holds true for BBY, COST, WMT and other retailers who have set up competing sale events. Bitcoin is down 7% (just below $33,000) so far today as China intensified its crackdown on crypto mining operations. GOOG has closed its start-up incubator campus in London, announcing they will not reopen the facility closed during the pandemic.

Related to the virus, new US infections continue to fall. The totals rose to 34,406,001 confirmed cases and deaths are now at 617,166. These numbers are now under-reported again as some states (mostly Southern) have decided to stop reporting data on a daily basis. Nonetheless, on the data we do have, the number of new cases is falling again and are back down to an average of 11,158 new cases per day (the lowest number since March 2020). Deaths are also falling, just more slowly, but are now down to 291 per day (again, the lowest number since March 2020.

Globally, the numbers rose to 179,320,883 confirmed cases and the confirmed deaths are now at 3,883,427 deaths. The trends are better again as we have seen a slowing in the rate of increase now that India has passed its peaked. The world’s average new cases are falling quickly now, but remain at 360,464 new cases per day. Mortality, which lags, is also falling but remains at 8,186 new deaths per day.

Overnight, Asian markets were mostly in the red, some dramatically. Japan (-3.29%) was the main standout and was the down over 4% at one point. However, Australia (-1.81%), Taiwan (-1.48%) and Hong Kong (-1.08%) were among those that fell in sympathy. This came on no particular news as China’s Central Bank held rates steady as expected. In Europe, markets are mixed, but lean to the green side. The FTSE (+0.03%) and CAC (+0.16%) are flat, while the DAX (+0.55%) is modestly higher at this hour. As of 7:30 am, US Futures are pointing to a positive open. The DIA is implying a +0.51% open, the SPY implying a +0.34% open, and the QQQ implying a +0.33% open.

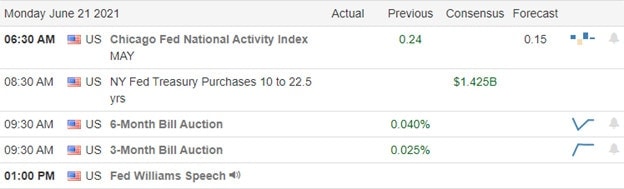

The only major economic news scheduled for Monday is Fed member Williams speaking at 3 pm. There are no major earnings reports scheduled for Monday.

Interest rates are starting the week lower as the 10-year bond yield fell to a 2-month low in overnight trading. This comes as Oil is flat. Jitters seem to be the order of the day without a good explanation for the Japanese market collapse today. Europe recovered nicely from the Asian weakness, but the bears have the trend in their favor in the US.

All trends reverse at some point and every S/R level is breached eventually. So, don’t assume trend, support, or resistance are always going to hold. Still, the odds favor following the trend and respecting support and resistance levels. Just keep locking in profits, moving your stops, and maintaining discipline. Follow those trading rules and stick to the trade plan. Remember that consistency is the key to long-term trading success.

Ed

Swing Trade Ideas for your consideration and watchlist: INSG, SNAP, BNGO, AAPL, NNOX, TQQQ, FSLY, FTNT, ARKF. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

The tech giants almost single handily lifted the QQQ to new record highs while China’s plan to release reserves toppled trends in inflationary stocks and commodities. At the same time, the DIA suffered technical damage in a wild price action day with a substantial whipsaw intraday. With price volatility so high, day traders likely have the upper hand, while swing and position traders may find the whips in price action challenging to downright unsavory.

While we slept, Asian markets closed mixed through the HIS rallied 0.85%. European markets are decidedly bearish this morning as the tumble in commodities continues. The U.S. futures currently point to a lower open with a very light day of earnings and economic data to provide inspiration as we slide into the weekend. Should the tech titans happen to turn south, it could be a painful day.

Economic Calendar

Earnings Calendar

We have a very light day on the Friday earnings calendar with just 3-companies listed and only one verified report coming from GLBS, which is not particularly notable.

News & Technicals’

Commodities plunged yesterday as China announced a plan to release reserves of metals that included Copper, Aluminum, palladium, and platinum. The move caused a spike in the U.S. dollar, also affecting Gold and Silver, as well as oil and grain futures. That said, we can expect most of the prices to recover due to the rising inflation. Morgan Stanley has upgraded Occidental due to higher prices suggesting a 40% increase in the stock. Exon Mobil received a similar upgrade earlier this week. Remarkably with inflation on the rise, the 10-year Treasury note fell this morning to 1.477%, and the 30-year dipped to 2.067%, likely giving the Fed a sigh of relief. The Covid-19 delta variant initially discovered in India is now spreading around the world, becoming the dominant strain in some countries, such as the U.K., and likely to become so in others, like the U.S. The variant now makes up 10% of all new cases in the United States, up from 6% last week. Studies have shown the variant is even more transmissible than other variants.

Yesterday’s price action saw traders rushing into the tech giants lifting the QQQ to new record highs. At the same time, the DIA suffered some technical damage following through to the downside after failing its 50-day average on Wednesday. With 40% of the SPY weighted by the tech giants held its ground but fell just short of breaking back above price resistance, and though the IWM recovered substantially, it has the uncertainty of a lower high followed by a lower low. China’s action tossed a monkey wrench into inflation-related stocks breaking established trends adding another layer of uncertainty as to what happens next. One thing for sure is that price volatility and huge intraday whipsaw will keep us all guessing. Stay focused and flexible as we slide into the weekend. Happy Father’s day!

Jobless Claims were unexpectedly high before the open and markets were a little manic on Thursday. The SPY waffled sideways all day, while the QQQ surged from open to close, and the DIA drifted lower all day. This left both large-cap indices in indecisive candles with the SPY printing a Doji that did not break through resistance and the DIA printing a Spinning Top, which may have found support. However, the QQQ printed a big white candle that closed at another all-time high. On the day, SPY lost 0.03%, DIA lost 0.62%, and QQQ gained 1.27%. The VXX fell to 31.88 and T2122 dropped down just above the edge of the oversold territory at 21.13. 10-year bond yields fell to 1.514% and Oil (WTI) dropped over 1.5% to $71.03/barrel.

As mentioned yesterday, the Chinese have begun flooding markets with their metals stockpiles in an effort to combat commodity inflation. That move, plus a stronger dollar, hammered metal prices on the day as shown by Copper (-4.83%), Silver (-6.52%), and Gold (-4.72%). However, the good news on the inflation front wasn’t limited to metals. Soybean (-8.5%) have fallen 20% since May while Corn, Wheat, Sugar, and even Lumber (-9%) also fell sharply. CNBC’s Jim Cramer went so far as to say that “commodity inflation is pretty much over” (not that his opinion is worth more than anybody else’s). Still, on the other side of inflation news, related to Fed action, mortgage rates shot higher Thursday to an average of 3.25% (30-year fixed), up half a percent from February levels.

Related to corporate taxes, Ireland has said “they want a compromise” and will fight against the Global 15% Minimum tax plan that has already been agreed by the G-7 and discussed by the G-20. Essentially, the Irish Finance Minister Donohoe said that undercutting other country’s tax rates in order to get multi-nationals to hide/park their profits in Ireland is legitimate market competition. As such, his country intends to fight hard at the OECD with the help of AAPL, GOOG, and others companies who currently stash their profits in Ireland.

Related to the virus, new US infections continue to fall. The totals rose to 34,377,592 confirmed cases and deaths are now at 616,440. These numbers are now under-reported again as some states (mostly Southern) have decided to stop reporting data on a daily basis. Nonetheless, on the data we do have, the number of new cases is falling again and are back down to an average of 12,697 new cases per day (the lowest number since March 2020). Deaths are also falling, just more slowly, but are now down to 316 per day (again, the lowest number since March 2020. BAC joined the parade of Wall Street Banks that are demanding workers return to the office.

Overnight, Asian markets were mixed. Malaysia (+1.16%), Hong Kong (+0.85%), and Shenzhen (+0.77%) led the gainers. The losses were moderate, if wider-spread, but only Indonesia (-1.01%) showed a significant loss. In Europe, markets lean heavily to the red side so far today. The FTSE (-1.17%), DAX (-0.95%), and CAC (-0.62%) are typical of the spread as of mid-day. As of 7:30 am, US Futures are pointing to a lower open. The DIA is implying a -0.35% open, the SPY implying a -0.25% open, and the QQQ implying a dead flat open.

There is no major economic news or earnings reports scheduled for Friday.

Interest rates and commodity prices continued lower overnight, with some notable exceptions. However, the fall was less than Thursday, even if the trend continues. What is unknown is whether this is just a reaction to China going all-in to fight inflation, whether the market believes the Fed, or maybe something unknown is at work. All we can really say is that Thursday was a reflation trade (tech up, value down) and it seems to be setting up for something similar early today.

All trends reverse at some point and every S/R level is breached eventually. So, don’t assume trend, support, or resistance are always going to hold. Still, the odds favor following the trend and respecting support and resistance levels. Just keep locking in profits, moving your stops, and maintaining discipline. Follow those trading rules and stick to the trade plan. Remember that consistency is the key to long-term trading success.

Ed

Swing Trade Ideas for your consideration and watchlist: No trade ideas today. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

The Fed decided to stay the course, continuing to buy $120 Billion in debt per month as the FOMC acknowledged rising inflation is more substantial than expected. Though the initial reaction to the statement brought out the bears, the bulls charged back in a late afternoon rally. The only index suffering some technical damage was the DIA which closed below its 50-day average. Long story short, stay with the trend because the market no longer cares about debt or inflation.

Asian markets traded mixed overnight, with the Nikkei slipping nearly 1% while the HIS rallied. European markets are pulling back modestly this morning across the board. Ahead of earnings, Jobless claims, and manufacturing data, U.S. futures point to a modestly bearish open after rallying well off the overnight lows. Stay focused and watch for whipsaw moves as the bulls and bears sort out dominance issues with overhead resistance levels as the battleground.

Economic Calendar

Earnings Calendar

We have a slightly busier day on the Thursday earnings calendar, with eight companies reporting. Notable reports include ADBE, JBL, KR, & SWBI.

News & Technicals’

Eleven Republican senators now support a bipartisan infrastructure framework, which would give a bill enough votes to pass the Senate if all Democrats get on board. However, several liberal senators have signaled they could oppose the bipartisan plan, saying it does not go far enough to fight climate change or income inequality. China launched the first astronauts into space on Thursday as China challenges the U.S. in several technology areas. The bill to make Juneteenth the 12th federal holiday sailed through Congress, passing the Senate by unanimous consent with the House passing the bill just one day later sending it on to the President to sign into law. After spiking yesterday, U.S. Treasury yields drifted lower Thursday morning, with the 10-year coming in a 1.56% and the 30-year dipping to 2.179%.

The FOMC acknowledged rising inflation suggesting a rate increase is possible sometime in 2023 while at the same time continuing to buy debt at $120 billion per month. The initial negative reaction whipsawed yesterday afternoon as buyers rushed back in after the press conference. Though the SPY, QQQ, and IWM recovered substantially, the DIA suffered some technical damage closing below its 50-day average. If the highest PPI on record is of no consequence to the market and the Fed continues to grow their more than 7 Trillion balance sheet, I guess the new normal is no financial metric matters anymore! Stay focused on price action and stay with the trend as long as it lasts.

Markets ground sideways in a nothing burger until the Fed news at 2 pm. From there, we saw a knee-jerk dive to the downside, followed by a sharp whiplash rally at 3pm that ended up fading again the last 15 minutes of the day. This left us with wicks on the downside and black bodies on the candles of the 3 major indices. However, it is fair to say the bears were more-or-less in control Wednesday. On the day, SPY lost 0.56%, DIA lost 0.77%, and QQQ lost 0.37%. The VXX rose to 32.07 and T2122 fell to 41.85. 10-year bond yields rose significantly to 1.579% and Oil (WTI) fell two-thirds of a percent to $71.66/barrel.

The big news for the day was the Fed data points and words. While the Fed left rates unchanged (near zero) and continues to say there will be no rate hikes the rest of this year or next, the new “dot-plot” forecasts 2 rate hikes during 2023. However, Chair Powell told reporters that the dot-plot “needs to be taken with a big grain of salt.” In other words, he warned against taking the projection of two rate hikes in 2023 wasn’t an indication that the Fed would definitely raise rates then. Powell also told reporters that the FOMC has not made any decisions about when to start tapering their bond-buying, which many had suspected would be announced at this meeting.

In global news that impacts trading, Chinese efforts to curb commodity prices kicked into overdrive. All Chinese state-owned companies were ordered to report their futures positions (to curb speculation) and the state-owned stockpiles of metals have also started to be released to the Chinese markets. This can’t help but to have a global impact since China is one of the importers of every commodity. In an unrelated story, early today there was another major internet outage (the second in 10 days), This one, reportedly caused by a failure in the network of AKAM, took out airline websites (LUV, UAL, ULCC), a broad number of Australian Banks, the Hong Kong stock exchange, and major financial platforms like Vanguard, E-Trade, and ADP briefly.

Related to the virus, new US infections continue to fall. The totals rose to 34,365,985 confirmed cases and deaths are now at 616,150. These numbers are now under-reported again as some states (mostly Southern) have decided to stop reporting data on a daily basis. Nonetheless, on the data we do have, the number of new cases is falling again and are back down to an average of 13,360 new cases per day (the lowest number since March 2020). Deaths are also falling, just more slowly, but are now down to 344 per day (again, the lowest number since March 2020). In an interesting move, the CEO of MS told all employees they must return to the office by September. This lies in contrast to other companies that have decided some jobs and some work by most positions can be performed remotely even after restrictions are all lifted.

Overnight, Asian markets were mostly in the red on modest moves. Japan (-0.93%) was by far the biggest loser with Shenzhen (+1.23%) by far the biggest gainer. However, the bulk of the region moved well less than half a percent and mostly to the downside. In Europe, with the exception of Greece (+0.21%), the entire continent is trading modestly lower at this point in the day. The FTSE (-0.40%), CAC (-0.02%) and DAX (unchanged) are typical. As of 7:30 am, US Futures are pointing toward a modestly lower open. The DIA is implying a -0.14% open, the SPY implying a -0.20% open, and the QQQ implying a -0.35% open.

The major economic news for Thursday is limited to Initial Jobless Claims and Philly Fed Mfg. Index (both at 8:30 am) and Treasury Sec. Yellen testifies at 10 am. Major earnings reports on the day include CMC, JBL, and KR before the open. Then after the close ADBE reports.

The market is still digesting and figuring out what to do with the Fed news from yesterday. The FOMC continues to say they are “staying the course” and no changes are foreseen for the next 18 months. They did forecast interest rates rising a couple of times in 2023, but Chair Powell immediately went out of his way to say, in effect, “that’s not a given, it may not happen.” So, the market sees inflation now that the Fed says will lessen in early 2022, a booming economy that isn’t quite as hot as some would like, and a Fed that says “Don’t worry, we got this.” …What is a trader to do?

As always, follow the trend and respect support and resistance levels. However, don’t just assume those levels will hold. All trends reverse at some point and every S/R level is breached eventually. Keep moving your stops, locking in profits, and maintaining discipline. Follow those trading rules and stick to the trade plan. Remember that consistency is the key to long-term trading success.

Ed

Swing Trade Ideas for your consideration and watchlist: No trade ideas today. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service