After hearing that the producer prices surged well past inflation expectations, the bulls ignored the news and pushed the SP-500 to its 47th record high for the year, with Dow leading the charge. I suspect there will be a time when we will suddenly care about inflation, but for now, stick with the bullish trends and enjoy the party as long as it lasts. With volume below average and a very week, Absolute Breadth Index may suggest market complacency is growing, so guard against overtrading and avoid chasing already extend stocks.

Asian markets struggled overnight, closing the session mostly lower with only ASX squeaking out a positive close. However, the Europiean markets see nothing but green this morning fueled on solid earnings data. With earnings numbers dwindling and U.S. futures trade mixed ahead import/export numbers and consumer sentiment.

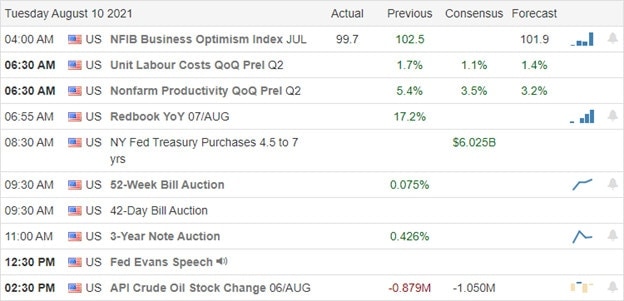

Economic Calendar

Earnings Calendar

We have a lighter day on the Friday earnings calendar with just 71 companies listed, but a significant number are unconfirmed. Notable reports include ARHVF, DSEY, FUJIY, SDPI, & VSTA.

New & Technicals’

The pandemic numbers back on the rise; the FDA recommends booster shots for people with compromised immune systems hoping to shield the most vulnerable. According to Fauci, everyone will likely need booster shots in the near future. In addition, pandemic restrictions are again on the rise, with indoor masking requirements and vaccine passports entering public buildings. A new black market business has emerged producing fake vaccination cards. As the U.S. withdraws troops, Al-Qaeda quickly regains power as they march across the country, taking city after city. The expectation is that Kabul will soon be recaptured, and the U.S. is now deploying 3000 American troops to help with the evacuation of Americans at the U.S. Embassy.

After hearing that Producer Prices came in much hotter than expected, the bulls quickly decided they don’t care, setting the 47th new record high in the SP-500 this year. The Dow also surged to new records while the QQQ recovered from early selling as the tech giants lifted the index. The VIX continues to march lower, nearing the June lows. It is, however, a bit concerning that volume remains below average as the market surges higher and the Absolute Breadth Index remains shocking low. That said, the bullish trends in the DIA, SPY, and QQQ are unmistakable, and the technicals show no signs the direction is about to change. Stay with the trends as long as this bullish party continues, but plan to protect your capital should the sentiment suddenly change.

July PPI came in much hotter than expected, but as expected Jobless claims kept falling. Markets shrugged off this news to open flat. Then after a fade the first hour, the bulls started a long, slow rally that lasted the rest of the day. This gave us strong candles in all 3 major indices, including a Dragonfly Doji in the DAI (to a new all-time high close), a strong bullish candle in the SPY (to another all-time high close), and a strong bullish candle in the QQQ. On the day, SPY gained 0.30%, DIA gained 0.08%, and QQQ gained 0.36%. The VXX fell another 2% to 26.24 and T2122 fell out of the overbought territory to 70.83. 10-year bond yields climbed to 1.361% and Oil (WTI) fell half a percent to $68.91/barrel.

After the close, DIS beat on both lines in its report. Despite its theme parks remaining unprofitable, the company managed to handily top estimates, delivering $17.02 billion in revenue and $0.80/share earnings for the quarter. One stand-out from the report was that the Disney+ streaming service added 1.5 million more subscribers than had been expected.

The delta variant is raising concerns in the logistics world. Which may have major follow-through impacts on the retail and manufacturing sectors in the fall. Chinese restrictions have caused the partial closure of the world’s third-largest port already. The Port of Los Angeles is already prepping for another dramatic decline in container volume. With container pricing up 220% already this year, the logjams that result from another set of port slowdown/shutdowns could have drastic impacts on shipping costs.

Early today the FDA authorized a vaccination booster shot for immunocompromised people. While the FDA said that fully-vaccinated healthy people are adequately protected, the debate continues on whether to expand booster shots or continue to apply the doses that would be required toward getting the unvaccinated population their first rounds of vaccine. However, Thursday afternoon Dr. Fauci (NIH) told a press briefing that it is likely that everyone will need a booster shot at some point.

Overnight, Asian markets were mostly in the red. Taiwan (-1.38%) was an outlier, but Shenzhen (-0.69%) and Singapore (-0.54%) paced the losses on global logistics concerns. However, India (+1.01%) and Australia (+0.54%) were among the few green exchanges in the region. In Europe, markets are mixed but lean to the green side so far on Friday. The FTSE (+0.33%), DAX (+0.43%), and CAC (+0.38%) are leading the continent higher at mid-day. As of 7:30 am, US Futures are pointing toward a flat open. The DIA is implying a +0.13% open, the SPY implying a +0.04% open, and the QQQ is implying a -0.02% open at this hour. 10-year bond yields are down a bit as the dollar is down so far today.

The major economic news scheduled for release on Friday is limited to July Imports and July Exports (both at 8:30 am) and Michigan Consumer Sentiment (10 am). The major earnings reports scheduled for the day are limited to DSEY and ERJ before the open. There are no earnings reports scheduled for after the close.

With no major news planned this morning and the twin fears of covid impacts and inflation-caused Fed tightening, the bears have the wind at their back this morning. However, the bulls have been impossible to deny regardless of news for months. It seems like a classic case of “climbing the wall of worry” in recent days. Gaps, fades, and long periods of tight-range sideways grind have been a spot-on description of market action this summer. However, trends remain bullish (if flattened in the QQQ). So, while caution is required, predicting trend change is not a strategy for long-term success.

Keep your losses small by managing stops and consistently take profits when you have them. Never chase price on an entry. If you missed a move, admit it and move on to the next trade. Above all, maintain your discipline to your trading rules. Stick with the trend until the trend is broken. As mentioned, reversal predictors don’t tend to last long in the trading business. Focus on the process and managing what you can control. Discipline will see you through.

Ed

Swing Trade Ideas for your consideration and watchlist: AAPL, MSFT, SOLO, MIME, ORCL, ASAN, PSA, CROX, TRGP, HUBS, EBON. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Traders shrugged off inflation numbers as they once again pushed the Dow and SP-500 to new records. When good news is a reason to buy, and bad news is a reason to keep buying, it makes me concerned about the damaging effects of complacency in the longer term. There is no doubt the DIA, SPY, and QQQ trends are bullish. So stay with them as long as they last, but never forget this wild bullishness will not last forever. Avoid chasing already extended stocks and guard against overtrading as this bull party continues.

Overnight Asian markets traded lower as currencies due to the weaker dollar. European markets trade mixed with modest gains or losses as pandemic concerns weighs on investors. Ahead of a dwindling number of earnings reports and the latest reading on Jobless Claims and PPI U.S. currently point to modest gains but new records at the open.

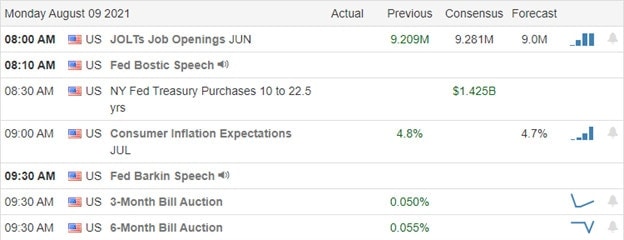

Economic Calendar

Earnings Calendar

On the Thursday earnings calendar, we have a busy day with more than 260 companies listed, but a significant number of them have not confirmed. Notable reports include DIS, ABNB, BIDU, BAM, CSIQ, TAST, BAP, CYBR, DASH, FRGI, GDRX, IQ< LZ, LAZR, MDP, MIDD, PLTR, PTE, & WPM.

News & Technicals’

The Competition and Markets Authority said it the purchase of Giphy by Facebook will harm competition. They warned the deal would remove a potential challenger in the display advertising market. In addition, a U.S. bipartisan bill aims to shake up how Apple and Google run their mobile app stores in similar news. App developers have claimed unfair practices from the tech giants, and the bill hopes to allow more competition into the app markets. According to Professor Sir Andrew Pollard, the head of the Oxford Vaccine Group said with the highly infectious delta variant achieving herd immunity is not possible.

Traders and investors shrugged off inflation numbers yesterday, pushing the Dow and SP-500 up, setting more new records. When bad news becomes a reason to buy up the market, and good news inflates it, even more, we must become concerned about market complacency. That said, the trends are very bullish in the DIA, SPY, and QQQ, and the premarket pump suggests more records at the open. We have one potential stumbling block with the weekly jobless claims, but we have seen missing on that number can also be ignored. So stay with the trend and party like its 1999 as long as it lasts but, please guard yourself against complacency and the desire to overtrade these very lofty valuations.

The July CPI number came in exactly as expected and markets gapped up slightly after having feared seeing a hot number. The QQQ faded that gap immediately, but the entire market ground sideways in a very tight range from mid-morning on. This left us with a nice white candle in the DIA, a Dragonfly Doji type candle in the SPY and a black Spinning Top type candle in the QQQ. On the day, SPY gained 0.24% (a new all-time high close), DIA gained 0.63% (a new all-time high close), and QQQ lost 0.17%. The VXX fell 2.65% to 26.80 and T2122 rose back into the overbought territory at 83.16. 10-year bond yields fell slightly to 1.334% and Oil (WTI) rose 1.5% to $69.32/barrel.

During the afternoon, a bipartisan bill was introduced in the Senate that could have dramatic impacts on AAPL and GOOG. The bill, as introduced, would prevent the two behemoths from requiring App developers to use the app store payment system. It would also prevent AAPL and GOOG from limiting app developers from directly contacting app users with offers. Finally, it would prevent AAPL and GOOG from punishing app developers for offering better pricing anywhere outside of the app store. Although the impacts have not been quantified, if this were to become law both companies (and any other app store with 50 million users) would take a huge hit to a major cash cow division.

Also during the day, Dallas Fed President Kaplan said that the Fed should announce they are tapering bond-buying and should then begin tapering in October. It is worth noting that Kaplan has always been known as a “hawk” and that he is not a voting member at this time. However, this is the first FOMC member to put a firm timeline out in the public. KC Fed President George also said that she believes the Fed should move out of “extraordinary policy” and into a “neutral monetary policy” as the recovery continues. However, once again, George is not a voting member this year.

In another sign that the economy has recovered, US freight volumes (truck and rail) have returned to pre-pandemic levels. The Cass Freight Index for July showed volumes higher than July 2019. However, the numbers were down a bit from June. Interestingly (related to inflation), shipping prices fell faster than volumes in July (shipments declined 3% while costs came down 5%). The full index will be released later this morning.

Overnight, Asian markets were mostly in the red on modest trading. Shenzhen (-0.79%), Thailand (-0.64%), and Hong Kong (-0.53%) led the moves lower. Indonesia (+0.84%) was the only appreciable gainer. In Europe, markets are showing modest moves, but are mostly green at mid-day. The FTSE (-0.15%), DAX (+0.38%), and CAC (+0.25%) are typical of the continent. As of 7:30 am, US Futures are pointing to a flat open. The DIA is implying a 0.14% gain, the SPY implying a 0.07% gain, and the QQQ implying a 0.04% gain at this hour. The dollar is flat, but 10-year bond yields are up to 1.357% in early morning trading.

The major economic news scheduled for release on Thursday includes July PPI and Weekly Initial Jobless Claims (both at 8:30 am) and the WASDE (World Ag Supply and Demand Estimate) at noon. The major earnings reports scheduled for the day include ARKO, BIDU, BR, BAM, CSIQ, DDS, ESLT, IQ, KELYA, MDP, MIDD, EYE, and OGN before the open. Then, after the close, ABNB, WISH, BAP, DASH, FLO, RKT, and DIS report.

This morning markets will look to July Producer Prices for another clue as to how soon the Fed might start taking away stimulus. Europe and Asia showed some caution as fears over Delta variant impact increase. However, the US Markets love new highs, and a drift higher continues. Beware of volatility as markets have been gapping and resting the rest of the day for a while now. So, even the new highs feel like they are range-bound.

Stick with the trend until the trend is broken. Reversal predictors don’t tend to last long in trading. Also, keep in mind that you don’t need to call market turns to be successful. Just keep your losses small by managing stops and consistently take profits when you have them. Never chase price on an entry. If you missed a move, admit it and move on to the next trade. Above all, stick to your trading rules. Focus on the process and managing what you can control. Discipline will see you through.

Ed

Swing Trade Ideas for your consideration and watchlist: FOLD, FAST, AMD, NET, DOCU, KBH, PLTR, DDD. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Focus this morning will turn to the consumer inflation numbers that economists expect to come once again come in hot. However, the hope is prices have peaked, and the increases will be temporary, as the Fed has suggested. I must admit to skepticism on that point, but time will tell. As earnings continue to roll out positively, the DIA and SPY printed more new records while, at the same time, the absolute breadth index fell near a 2-year low. The 10-year Treasury yields rose three basis points, and the 30-year rallied close to 3 basis points in year morning trading ahead of the CPI report.

Asian markets ended the day with modest gains after a choppy session of trading. European markets trade green across the board this morning, but gains are modest ahead of the U.S. opening bell. With a substantial consumer inflation number pending, the U.S. futures suggest a flat mixed open, but that is likely to change dramatically market reacts to the CPI number before the bell. So expect an extra dose of price volatility at the open as traders and investors digest the results.

Economic Calendar

Earnings Calendar

We have 140 companies listed on the Wednesday earnings calendar, with quite a few that are unconfirmed. Notable reports include AIT, ARRY, BLNK, BMBL, CLOV, EBAY, XONE, FOSL, RIDE, MNKD, NGMS, NIO, PRGO, RXT, RGLD, RPRX, STAF, VRM, & WEN.

News and Technicals’

After passing a 1.2 trillion dollar plan on infrastructure, the Senate passed the framework for another 3.5 trillion spending plan before leaving on summer break. However, both plans could take weeks, if not months, to make their way through the house. Then, in what is likely the largest cryptocurrency thefts to date, more than $600 million was stolen by hackers. According to reports, Poly Network disclosed the attack on Twitter, asking them to return the hacked assets. Yeah, that should work, LOL. Poly Network is a platform that looks to connect different blockchains so that they work together. Finally, as gas prices rise, the White House will call on OPEC to raise its oil production. The national average is up about a dollar per gallon on Tuesday at $3.18.

Today the market will turn its focus to consumer inflation with the latest CPI reading before the bell. Economists expect the number to come in hot, climbing 0.5% for the month and 5.3% yearly. Although they expect the prices to have peaked, the big question is whether it’s elevated temporarily as the Fed has suggested. Unfortunately, economists expect to see continued increases. While setting new records in the DIA and SPY yesterday, the absolute breadth index registered its lowest low in nearly 2-years. That said, the index trends remain strongly bullish, with futures mixed as we wait on the CPI number.

Markets opened flat Tuesday before diverging. The DIA put in a nice little rally the first hour of the day and then ground sideways in a tight range the rest of the day. However, SPY wobbled sideways all day long and QQQ sold off the first two hours before starting a sideways grind that lasted into the close. This left us with a nice white candle (and new all-time high close) in the DIA, a Doji (and new all-time high close by pennies) in the SPY, and a Bearish Engulfing of a Doji (that bounced up off trendline support in the QQQ. On the day, SPY gained 0.12%, DIA gained 0.45%, and QQQ lost 0.51%. The VXX fell almost 2% to 27.53 and T2122 remains in the mid-range at 68.28. 10-year bond yields rose to 1.354% and Oil (WTI) spiked almost 3% to $68.45/barrel.

During the day, the Senate passed the $1 trillion Infrastructure bill with bipartisan support (69-30). Among other winners, steel industry names such as NUE, X, STLD, etc. all rallied hard on the news as did many in the construction industry. However, this Senate vote was not the last step and it sends the bill back to the House, where the next hurdle will be whether the “progressive wing” of the Democratic party will hold the bill hostage. That said, the more liberal wing is not expected to demand large changes since the Senate also introduced (and passed) a $3.5 trillion budget bill immediately after the Infrastructure bill passed. This Budget bill includes most of the liberal wing wish-list items.

In the afternoon, there was a report out of China that should have impacted TSLA, but which in fact had no impact on the stock Tuesday. The report, from a Chinese Auto Industry trade group, said that TSLA’s sales in China plummeted 70% in July. TSLA sold 8,600 cars in China during the month compared to about 14,700 in June. This is important because industry analysts expect China to account for 40% of all TSLA sales by 2022. However, the export of Chinese-made TSLA cars also increased during July.

In other news, the semiconductor shortage continues to grow. The average lead time for chip orders has increased again to 21 weeks. Despite certain bright spots, the bottom line is that this shortage will not ease anytime soon. (The problem is that it takes from 12-24 months to materially increase production capacity. Even then there will be a ramp-up process during which production speeds will be slower than existing capacity and QA failure rates much higher. On top of this, none of the major chipmakers want to be stuck with excess capacity once “reopening demand” wanes.) So, for the foreseeable future, markets need to get used to things like auto-industry plant shutdowns, computer component shortages, cellphone delays, and generally higher prices for everything that contains a chip. That will eventually hurt the bottom lines across the economy.

Overnight, Asian markets were mixed again. Japan (+0.65%) and Malaysia (+0.52%) led gainers while Singapore (-0.85%), Thailand (-0.64%), and Indonesia (-0.64%) paced the losses. In Europe, markets are mostly green at mid-day. The FTSE (+0.50%), CAC (+0.29%), and DAX (+0.03%) are typical of the spread across the continent, but there are 3 smaller exchanges slightly in the red. As of 7:30 am, US Futures are pointing to a flat open ahead of inflation data. The DIA is implying a +0.05% open, the SPY implying a -0.08% open, and the QQQ implying a -0.20% open at this hour. It is also worth noting that 10-year bond yields are up to 1.366%, the dollar stronger and Oil down 1.2% ahead of CPI data.

The major economic news scheduled for release on Wednesday includes July CPI (8:30 am), Crude Oil Inventories (10:30 am), July Federal Budget Balance (2 pm), and 2 Fed speakers (Bostic at 10:30 am and George at noon). 10-year Treasury notes are also auctioned at 1 pm. The major earnings reports scheduled for the day include APG, ARCO, CAE, and RPRX before the open. Then, after the close, APP, AVT, CACI, CPNG, EBAY, ENS, BEKE, NIO, OPEN, and RXT report.

All eyes will be on July Consumer inflation data this morning (which is expected to be hot as it was in June). However, the White House calling on OPEC to expand oil production in the face of rising fuel prices also is also a wildcard and is having an early morning impact on WTI. Beware of volatility as markets have been gapping and resting in a tight range to have gone “nowhere but sideways” over the slightly longer-term look.

Keep in mind, you don’t need to call the market turn to be successful. In fact, reversal predictors don’t tend to last long in trading. So, stick with the trend until the trend is broken. Also remember, you don’t have to trade every day. If the market action is too whippy or sideways lately, take some time off and enjoy the summer. However, if you do trade keep your losses small and consistently take profits when you have them. Never chase price. If you missed a move, admit it and move on to the next trade. Above all, stick to your trading rules. Focus on the process and managing what you can control. Discipline will see you through.

Ed

Swing Trade Ideas for your consideration and watchlist: FOLD, INO, GSK, PLUG, SNOW, JNJ, CARR. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

While bullish trends dominate in the DIA, SPY, & QQQ, traders and investors appear to be taking a wait-and-see approach. As a result, there is a noticeable decline in volume, and the absolute breadth index continues to diverge, yet the VIX is in decline. So are we waiting on the massive congressional spending bills, or could it be a wait to see if the CPI number on Wednesday is inflationary? We seem to be building up for a substantial move, but the question is will it be bullish or bearish? So plan your risk carefully as we wait for the decision.

Asian markets mostly rallied overnight, led by the HIS gaining 1.23% even as more pandemic restrictions occur in China. European markets trade mostly higher with modest gains as pandemic caution lingers and worries of tapering grow. Finally, as earnings results roll out, U.S. futures trade mixed and relatively flat as bulls and bears look for inspiration to break the index consolidation.

Economic Calendar

Earnings Calendar

We have about 140 companies listed on the Tuesday earnings calendar, but there is a considerable number unconfirmed. Notable reports include COIN, ARMK, XAIR, CSPR, FTEK, GO, JMIA, MCFE, PAAS, POSH, PSTL, PUBM, SIEN, SGFY, SMCI, SYY, TDG, U, UPST, & WW.

News & Technicals’

China has tightened measures the rapidly increasing infection rates, further dampening investor sentiment toward Chinese stocks. In addition, disruptions in the Chinese economy could also affect global growth. The Senate plans to vote on the 2700 page trillion-dollar infrastructure bill today and immediately begin efforts to pass another 3.5 trillion dollar package with no Republican support. The popular by now pay later offerings for online shopping is causing consumer debit and credit card balances to spike, especially for younger consumers. Analysts warn this trend could be the next hidden source of consumer debt. While the embattled Governor of New York fights to stay in office, Governor Newsome of Calfornia faces an upcoming Sept. 14th recall election. The rollout of new pandemic health orders and the massive exodus from to state may pose a real threat to Newsom’s chances of survival. All the political disruptions could have substantial market impacts as the political theater plays out.

Though trends in the DIA, SPY, and QQQ are very bullish, there seems to be a building uncertainty and a wait-and-see attitude among investors and traders. Perhaps they are waiting to see if the massive spending bill will pass through congress? Or maybe, it’s a wait on the inflationary reading on CPI coming out on Wednesday? As a result, the volume has become noticeably lighter, and the Absolute Breadth Index continues to diverge rather dramatically from the index charts. Technically speaking, the bullish trends look solid, yet a growing number of talking heads warn of a 10 to 20 percent pullback on the way. In addition, the VIX suggests fear is in decline, yet one must wonder if it is displaying some complacency? As for me, I will stay with the trend, but I continue to reduce my bullish aggressiveness and am ready to act should prices begin to slide south.

Markets opened flat and then oscillated sideways all-day Monday. This left us with Doji-like candles in all 3 major indices. On the day, SPY lost 0.07%, DIA lost 0.26%, and QQQ gained 0.18%, with all 3 being within a quarter of a percent of all-time highs. The VXX fell 1% to 28.01 and T2122 dropped back to 45.03 as the consolidation grind continues. 10-year bond yield jumped significantly to 1.329% and Oil (WTI) “rallied” to close down only 2.17% at $66.80/barrel (after having been down over 4.5% during early morning trading). In fact, the vast majority of commodities were down on the day as the dollar rose and Delta variant news stoked demand fears globally.

During the afternoon, it became clear that the long-awaited Infrastructure bill will receive its final Senate vote on Tuesday morning. (Since this bill has bipartisan support, with at least 19 Republicans on board, they have delayed the vote until daytime to give Senators plenty of television airtime.) From there the bill goes to reconciliation between the House and Senate before final passage. The Senate and Treasury Dept. also reach agreement on an amendment to the bill that would tighten cryptocurrency regulation, while not requiring individual reporting, but forcing that reporting onto trading/brokerage platforms. Again, this was a bipartisan-negotiated amendment.

Vaccine makers MRNA, BNTX, and PFE continue to extend a strong rally from recent weeks. This comes even in front of potential catalysts such as approval of booster shot plans and as new (higher in the case of Europe) pricing for vaccine doses is being negotiated for deliveries out past 2021.

Overnight, Asian markets were mostly green today. Hong Kong (+1.23%), Shanghai (+1.01%), and Singapore (+0.95%) led the gainers. Taiwan (-0.92%), Indonesia (-0.64%), and South Korea (-0.53%) were the lone red exchanges on the day. In Europe, markets are strongly leaning toward the green, with only two modest red numbers at this point. The FTSE (-0.02%) is one of the two, but the DAX (+0.23%) and CAC (+0.14%) are more indicative of the broader continent. As of 7:30 am, US Futures are pointing to a flat open. The DIA is pointing to a -0.03% open, the SPY is implying a +0.01% open, and the QQQ is implying a +0.12% open. 10-year bond yields are flat, but Oil is up almost 2% at this hour.

The only major economic news scheduled for release on Tuesday is Q2 Nonfarm Productivity and Q2 Unit Labor Costs (both at 8:30 am). The major earnings reports scheduled for the day include ARMK, DFH, IIVI, PRGO, SYY, and TDG before the open. Then, after the close, COIN, DAR, GO, and SMCI report.

Markets continue their sideways chop. Progress toward Infrastructure bill spending and the newly proposed Democratic $3.5 trillion budget plan (with a shifting of priorities from prior budgets) do not seem like major potential drivers. So, the summer doldrums on low breadth may continue as the bears have no immediate catalyst either. However, there are new Covid restrictions taking shape in China and this may be the foreshadowing of a tougher time for the global economy. Be careful of volatility and day-to-day chop as you plan your risk.

Remember, you don’t have to trade every day or even week. Trading success is about consistently winning more than you lose by following the trend and then keeping your losses small while consistently taking profits when you have them. You don’t need to call the turn or have all triple-digit gain trades. So, don’t try to predict the market. Neither should you chase price and, above all, stick to your trading rules. Focus on the process and managing what you can control. Discipline will see you through. Also, remember it’s Friday. Don’t forget to pay yourself and be ready for the weekend news cycle.

Ed

Swing Trade Ideas for your consideration and watchlist: BCRX, SNAP, STLD, TSLA, CHWY, PAVE, IDN, SKY. Rick is out but the RWO Room is open. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

After setting new records on Friday, we look to have mixed open as we wait for a vote in the Senate on the trillion-dollar infrastructure bill. Volume on Friday was below average, and the absolute breadth index decline to recent lows, but the VIX indicated declining fear falling below its 50-day average. With another busy week of earnings and a CPI reading on Wednesday, the recent price volatility will likely stick around, so plan your risk carefully. Though the IWM remains weak, the trends in the DIA, SPY, and QQQ are very bullish. So stay with the trend but have a plan should the bears decide to attack due to the lofty valuations.

Asian market kicked off the week with modest gains as oil prices fell 3%. European markets trade primarily in the red this morning, keeping an eye on earnings results. With more than 200 companies reporting and a JOLTS report later this morning, the U.S. futures suggest a mixed open with the Dow in retreat and the Nasdaq pointing to modest gains. Let the wild earnings rollercoaster ride continue!

Economic Calendar

Earnings Calendar

Although the bulk of market-moving reports are behind us, we still have a busy week of reports with more than 200 listed on the calendar. DDD, PLNT, APD, AMC, GOLD, BNTX, CBT, ELY, CF, CHGG, CXW, APPS, DISH, EBIX, ELAN, ENR, GLNG, KNDI, QLYS, SGMS, SDC, TTD, TSN, & WKHS.

News & Technicals’

According to reports, the Senate is inching closer to passing the trillion-dollar infrastructure bill. Debate is now closed, and there is the hopefulness that a vote is forthcoming. With more hyped-up deals turning into flops, lawsuits against the once-popular SPAC are running into suspect dealmaking questions. On Sunday, Larry Brilliant, a famed epidemiologist, said that the world is nowhere near the end of the pandemic, with only a small proportion of the world’s population vaccinated. He suggested that vaccinated people aged 65 with a weakened immune system should get a booster shot right away. If that’s not gloomy enough, a U.K. report delivered a stark warning on climate change, calling it a code red for humanity. Treasury yields start the week higher, with the 10-year trading up to 1.292% and 30-year rising to 1.942%

After gapping higher and setting new records in the DIA & SPY, the market mostly chopped the rest of the day as if most traders left for an early weekend after the jobs report. As a result, volume came in lower than average, and the Absolute Breadth Index fell to recent lows to close the week. However, on a positive note, the VIX finally broke down below its 50-day average. The bulls remain in control with positive trends in the DIA, SPY, and QQQ, with the IWM remaining the outlier still below its 50-day average. Though we’re over the hump with market-moving reports, we still have a busy week of earnings to keep the price volatility high. That said, stay with the trend but have a plan to protect your capital should the bears find a reason to attack. From these loft valuations, any pullback could be swift and painful.

The July Payrolls Data came in better-than-expected Friday, resulting in a slight gap up in the large-cap indices and a gap down in the QQQ. After that, all 3 major indices more or less ground sideways the remainder of the day. This left us with indecisive Spinning Top type candles in all major averages. On the day, SPY gained 0.17% (to a new all-time high close), DIA closed up 0.42% (to a new all-time high close), and QQQ closed down 0.44%. The VXX fell 2.5% to 28.30 and T2122 rose to just outside the overbought territory at 75.33. 10-year bond yields rose sharply to 1.304% and Oil (WTI) fell 1.4% to $68.11/barrel.

Late Friday afternoon it was reported that US consumer borrowing surged in June by the largest on record. This amounted to a 10.6% ($37.7 billion) increase compared to May. A large portion of the increase came from credit card balances and non-revolving loans such as motor vehicle purchase loans.

On Saturday, BRK.B reported operating earnings that were up 21% year-on-year while overall earnings (which reflect the value of Berkshire equity investments) were up 6.8%. The company has continued to buy back shares rather than make acquisitions, but the pace of buybacks has slowed, both from a year ago and from Q1. As of June 30, the company had well over $144 billion in cash on hand.

In miscellaneous weekend news, a federal judge ruled that NCLH can require proof of vaccination prior to boarding, granting the company an injunction from Florida’s law that had barred any demand of vaccination proof by businesses. The first NCLH cruise since before the Pandemic left Florida Sunday after the ruling cleared the way. The Infrastructure bill made some progress over the weekend, but there is still a lot of vote-wrangling to do. However, a Senate vote one way or the other seems likely this week. Elsewhere, the UN published a report, approved by all 195 member states on Friday, delivering a stark warning of the “irrefutable and unequivocal evidence” that climate change is real, has had a major human influence and is very close to being irreversible. The effects impact billions of people (consumers), business operations, and distribution around the globe. As will the mitigation efforts such as converting huge swaths of industry and public consumption from fossil fuels and petroleum-based goods (such as plastics). The economic transformation will likely be massive.

Overnight, Asian markets were mixed, but leaned to the green side. Thailand (+1.21%) and Shanghai (+1.05%) were the clear leaders among gainers. Meanwhile, Indonesia (-1.22%) was by far the largest loser Monday as Oil prices were down over 4.5%. The remainder of Asian exchanges saw more modest moves in either direction. In Europe, prices are also mixed, with most of the smaller exchanges modestly higher so far today, but the “big 3” exchanges all on the red side of the ledger. This may be due to the impact of data out of China showing that Chinese Exports unexpectedly slowed in July. Regardless, the FTSE (-0.32%), DAX (-0.08%), and CAC (-0.02%) are all down at mid-day. As of 7:30 am, US Futures are pointing to a mixed and flat open. The DIA is implying a -0.27% open, the SPY implying a -0.12% open, but the QQQ is implying a +0.15% open at this point. As mentioned, commodities are widely down with Oil leading the way as WTI is 4.44% lower early today. The 10-year bond yield is also down significantly to 1.275% in early trading.

The only major economic news scheduled for release on Monday is June JOLTs (10 am). The major earnings reports scheduled for the day include APD, AMRX, AVYA, GOLD, BNTX, DISH, ELAN, ENR, GTES, SGMS, SYNH, TGNA, TSN, USFD, VRTV, and VTRS before the open. Then, after the close, ADV, ACM, CBT, ELY, CF, COMP, CAPL, HE, LU, DOOR, NGL, NTR, STE, and WES report.

Markets seem mixed and unsettled early Monday. The Delta variant continued to run, with the average daily new cases back above 100,000 and deaths beginning to slowly increase. This comes in the face of evidence the recovery may be slowing even as fiscal stimulus and the will for monetary easing is starting to wane. In short, the bear case has control of the conversation to start the week. Beware of volatility as the futures have changed directions a couple of times this morning already. So, the indices have not broken free of the consolidation of the past few weeks and day-to-day chop may continue to be the order of the day.

Remember, you don’t have to trade every day or even week. Trading success is about consistently winning more than you lose by following the trend and then keeping your losses small while consistently taking profits when you have them. You don’t need to call the turn or have all triple-digit gain trades. So, don’t try to predict the market. Neither should you chase price and, above all, stick to your trading rules. Focus on the process and managing what you can control. Discipline will see you through. Also, remember it’s Friday. Don’t forget to pay yourself and be ready for the weekend news cycle.

Ed

Swing Trade Ideas for your consideration and watchlist: MSI, FOXA, ARKK, QCOM, DEN, DHI, OTIS, VIAC, X, MU, RF, STLD, CLF, NUE, NOK, AA, MT, DVN, NVTA. Rick is out but the RWO Room is open. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

|607% in just 24 months |

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service