Solid Start to the New Year

Though volume was incredibly light in the last week of 2021, the strong price action set the stage for a solid start to the new year. But, unfortunately, the big gap up open greatly increases the risk to retail traders trying to capitalize on the move. Remember, strong bullish moves premarket also create the possibility of a pop and drop pattern, so make sure you see some follow-through buying before jumping into the fray. That said, I want to wish you all a very successful 2022, and let us begin the new year with profits and wise trading decisions.

During the night, Asian markets traded mixed with Evergrande shares halted preparing to release information about the most indebted developer. This morning, European markets trade is mostly bullish, with only the FTSE showing a modest decline when writing this report. With reading on PMI and Construction Spending just around the corner, U.S. futures point to s substantial gap open that may set new record highs to begin the new year.

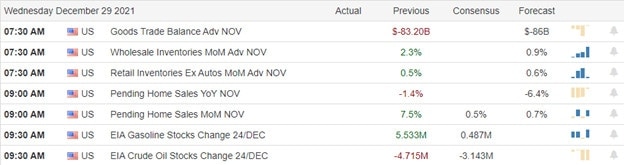

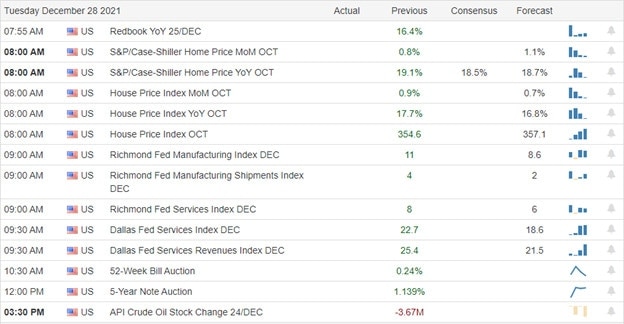

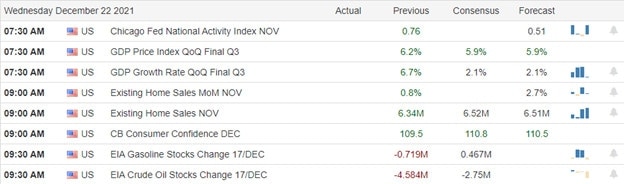

Economic Calendar

Earnings Calendar

To begin trading in the new year, we have just three unconfirmed reports on the earnings calendar with no notable events.

News & Technicals’

Airlines have canceled more than 15,000 U.S. flights since Christmas Eve. Bad weather worsened flight disruptions on the first day of the year. In addition, Omicron infections among crews have thinned staffing at some carriers. China Evergrande Group shares have been suspended from trading on Monday pending the release of “inside information,” the embattled property developer said without elaborating. Evergrande, the world’s most indebted developer, struggles to repay more than $300 billion in liabilities. These include nearly $20 billion of international market bonds deemed to be in cross-default by rating firms last month after they missed payments. China tightened its monetary policy, embarking on “aggressive deleveraging” as it sought to slash debt in the property sector. But China’s economy appears to be bouncing from a “mini-downturn” into an upswing as the country eases policy, says investment bank, Morgan Stanley. As a result, the bank is “more bullish than the consensus” and says it sees GDP growth in China accelerating to 5.5% in 2022. Finally, Tesla just published its fourth-quarter vehicle production and deliveries report for 2021, and it handily beat analysts’ expectations. In the fourth quarter, Tesla deliveries amounted to 308,600 electric cars, and full-year deliveries amounted to 936,172 vehicles. According to a consensus compiled by FactSet, Wall Street analysts had anticipated Tesla deliveries of 267,000 in the fourth quarter and 897,000 for all of 2021.

Although the indexes took a little rest last couple of trading days of the year, they maintained bullish technical patterns that set the stage for a solid start to the new year. The futures surged during the night, suggesting a substantial gap up at the open on the first trading day of 2022. That said, we still have to be careful remembering that stock valuations are exceptionally high, with bloated P/E ratios and market internals showing that 56% of stocks remain below their 200-day averages. The fact remains that the big price swings of late and big gap open market adds significant risk for the retail trader jumping into new positions. Trade with the upside trend but guard against overtrading and avoid complacency. We have several potential market moving reports coming our way this week, so plan your risk carefully. I wish you all a very successful 2022!

Trade Wisely,

Doug