The GS earnings report inspired a big gap open, resulting in another pop-and-drop pattern as the indexes struggled with overhead resistance and a short-term overbought condition. Bond yields relaxed slightly, and the dollar dipped temporally after a coordinated effort by Chinese banks to bolster the Yuan. However, this morning bond yields rebounded as recession fears rise ahead of the pending housing data. As earnings work to inspire the bulls to rally, the worries over inflation, rising rates, recession, and slowing global economies are likely to keep the bears engaged and price action challenging.

Asian markets traded mixed but mostly lower overnight, with the tech-heavy HSI falling 2.38%. European markets trade flat to modestly bullish after the UK inflation climbed back above a 40-year high. Trying to draw inspiration from earnings reports, U.S. futures struggle to hold on to overnight lows ahead of housing data that may remind the market about recession. Plan carefully and prepare for the wild price volatility to continue.

Economic Calendar

Earnings Calendar

The earnings calendar is starting to heat with nearly 50 companies listed and about 40 confirmed reports for today. Notable reports include ABT, AA, ASML, CMA, CCI, EFX, IBM, KMI, LVS, PG, PPG, STLD, TSLA, TRV, & WGO.

News & Technicals’

Netflix beat third-quarter expectations on the top and bottom lines Tuesday. The company added 2.41 million net subscribers during the quarter, higher than the 1 million it had forecast. Netflix will begin to crack down on password sharing next year. ASML reported third-quarter revenue and earnings on Wednesday that topped analyst expectations, bucking the trend of a slowdown seen by other semiconductor firms. Shares of chip firms have been battered this year amid a slowdown in growth among companies like Samsung and Micron as the semiconductor boom hits a wall. But the strong results from ASML bucked the broader market slowdown, sending shares more than 6% higher in morning trade. ASML said that it expects the direct impact of the U.S.’s chip curbs on China to be “limited.”

DOE says the funding opportunity represents the “largest investment in tidal and river current energy technologies in the United States.” Over the past few years, a number of projects related to tidal power have taken big steps forward. While there is excitement about the potential of renewable technologies such as tidal power, there are significant challenges when it comes to scaling up. President Joe Biden will announce the release of up to 15 million more barrels of oil from the Strategic Petroleum Reserve, sources familiar with the plan told CNBC. The move aims to extend the current SPR delivery program through December. In addition, an EU embargo on Russian oil is scheduled to go into effect on Dec. 5.

U.K. inflation rose in September 2022 as the country’s cost-of-living crisis continues to hammer households and businesses ahead of a tough winter. However, inflation unexpectedly dipped to 9.9% in August, down from 10.1% in July, on the back of a fuel price decline. Treasury yields rose across the board on Wednesday as concerns over a recession spread among investors, and markets looked ahead to releasing housing market data. The 6-month bond rose to 4.35%, the 12-month to 4.46%, the 2-year to 4.48%, the 5-year to 4.28%, the 10-year to 4.07%, and the 30-year to 4.07%.

Tuesday served a pop-and-drop price move after a big gap up open inspired by the better-than-expected GS earnings. Chinese currency operations took some pressure off the dollar, lifting the Yuan slightly as bond yields modestly relaxed. Unfortunately, as we stare down the barrel of the Housing Starts and Permits number, fears of recession resurfaced this morning, with bond yields rising along with the dollar. While earnings have provided us with a relief rally, the indexes remain challenged by significant overhead resistance. I expect price volatility to remain high with overnight reversals and intraday whipsaws as inflation, rate increases, and the slowing global economy continue to weigh heavy on investors’ minds.

Markets gapped significantly higher at the open (+2.25% in SPY, +2.05% in DIA, and +2.70% in the QQQ) on Tuesday. However, this was a bull trap. All 3 major indices immediately sold off hard. The QQQ had more than faded the gap, while the SPY got within a quarter of one percent and the DIA got within one-third of one percent of doing so by 11:40 am. From there, we saw a modest rally that lasted until 2:30 pm, regaining about half of the original gap during that time. Then the bears stepped in to sell off all 3 major indices again at 2:30 pm, revisiting the lows of the day within 15 minutes. After a pause at the lows, the bulls stepped in for a rally to end the day. This action gave us large, black candles with a large lower wick in all major indices.

On the day, all 10 sectors were in the green with Communication (+0.50%) lagging and Industrials (+2.03%) leading the charge. The SPY and DIA both gained 1.13% and the QQQ gained 0.79% on the session. The VXX fell almost 2% to 20.44 while the T2122 (4-week New High/Low Ratio) jumped back up into the overbought territory at 87.68. 10-year bond yields fell back to 3.998% and Oil (WTI) was down 2.6% to $83.23/barrel. So, overall, it was a bull trap day with a “gap and crap” action perhaps with some short profit-taking at the end of the day.

In economic news, September Monthly Industrial Production came in much hotter than forecast at +0.4% (versus +0.1% expected and -0.1% in August). After the close, API reported Weekly Crude Oil Stocks fell 1.270 million barrels (versus an expected build of 1.551 million barrels and compared to last week’s 7.054-million-barrel build). Atlanta Fed Pres. Bostic spoke before the Urban Institute Tuesday, speaking to Main Street rather than Wall Street and explaining current problems and the potential upside of recession. He said the economy is still trying to deal with the turmoil caused by the wage and job trends that stemmed from the Pandemic. The basic problem is that large numbers of workers quit, retired, moved, or changed fields during the pandemic, which put real labor pressure on all companies. However, the large (deep-pocketed) companies were in the position to raise wages and move to a remote work model. In that way, they drew workers away from lower wages and less flexible jobs when the economy picked back up. The issue was aggravated this year by inflation, where again the large profitable companies were in a better place to raise wages. All of this has put small and medium-sized firms in serious trouble, unable to find workers at the lower wages they had been paying (and could afford) in the past. He did not say so, but he did imply that a recession cycle will help lessen the problem for the SMEs that survive.

In stock news, Bloomberg reported that CS will be working with MS and RBCI to increase capital. The details were not available, but previous reporting said CS needs at least $2 billion to shore up its balance sheet and to do restructuring. Meanwhile, the FAA told BA that some of the company’s documentation submissions for the “737 Max 7” are incomplete and others need reassessment by BA. It was reported Tuesday that AAPL has told its main phone manufacturer in China to halt production and the two main component makers to drastically reduce the production of the iPhone 14 Plus (the cheaper, $899 model) as AAPL reevaluates product demand. Elsewhere, TWTR froze its employee stock award accounts ahead of an anticipated closing of the Musk buyout will happen at $54.20 on or before Oct. 28. Finally, AMZN workers in NY have rejected unionization by a 2-to-1 margin.

In stock IPO and M&A news, for the second day in a row, INTC lowered its outlook for the IPO of its self-driving car division Mobileye. The April expectation was for $50 billion, on Monday it was $20 billion, and on Tuesday at the IPO roadshow, the company said it was now targeting a $16 billion valuation. Meanwhile, an activist fund (Third Point) announced it has taken a significant position in CL and has urged the company to spin off its Hills Pet Nutrition division via IPO. Third Point said in an open investor letter that it expects Hills to be worth $20 billion as a standalone company. Finally, the US Senate Judiciary Committee expressed concerns over the KR acquisition of ACI and said it will hold hearings on the deal next month.

After the close, UAL, NFLX, OMC, JBHT, ISRG, IBKR, and WTFC all reported beats on both the revenue and earnings lines. It is worth noting that NFLX crushed expectations and also reversed its subscriber losses, adding 2.41 million new subscribers during the quarter. However, the company did also lower its forward guidance. Meanwhile, UAL significantly raised its forward guidance on air travel trends. In less good news, FHN beat on the top line while missing on earnings.

So far this morning, ABT, ASML, PG, TRV, CFG, NDAQ, WGO, CMA, SC, and ELV have all reported beats on both the revenue and earnings lines. Meanwhile, BKR missed on revenue while beating on the earnings line. On the opposite side, MTB beat on the revenue side while coming in below analyst estimates on earnings. However, ALLY reported misses on both the top and bottom lines

Overnight, Asian markets were mixed but leaned to the downside. Hong Kong (-2.38%), Shenzhen (-1.43%), and Shanghai (-1.19%) paced the losses. Meanwhile, Malaysia (+1.05%), New Zealand (+0.64%), and Japan (+0.37%) led the gainers. In Europe, we see a similar picture taking shape at midday. Russia (-3.12%) is an outlier. However, the FTSE (-0.02%), DAX (+0.07%), and CAC (+0.17%) represent the middle ground with most smaller exchanges in the red, but also half a dozen of them modestly green in early afternoon trade. As of 7:30 am, US Futures are pointing toward a down start to the day. The DIA implies a -0.25% open, the SPY is implying a -0.30% open, and the QQQ implies a -0.26% open at this hour. 10-year bond yields are back up to 4.088% and Oil (WTI) is up 1.25% to $83.84/barrel in early trading.

The major economic news events scheduled for Wednesday include Sept. Building Permits and Sept. Housing Starts (both at 8:30 am), EIA Weekly Crude Oil Inventories (10:30 am), and Fed Beige Book (2 pm). We also have 2 Fed speakers scheduled, Kashkari at 1 pm and Bullard at 7:30 pm. The major earnings reports scheduled for the day include ABT, ALLY, ASML, BKR, CFG, CMA, ELV, LAD, MTB, NDAQ, NTRS, PG, PLD, SCL, TRV, UNF, and WGO before the open. Then, after the close, AA, CCI, EFX, IBM, KALU, KMI, KNX, LRCX, LSTR, LVS, LBRT, PPG, STLD, TSLA, and UMPQ report.

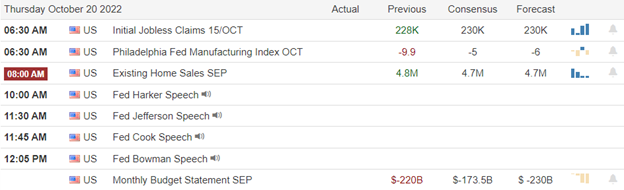

In economic news later this week, on Thursday, Weekly Jobless Claims, Philly Fed Mfg. Index, and Sept. Existing Home Sales are reported. Finally, on Friday, Fed member William speaks.

In earnings reports later this week, on Thursday, ABB, ALK, T, BX, DHR, DOV, DOW, EWBC, ERIC, FITB, FCX, GPC, HRI, KEY, MAN, MMC, MSM, NOK, NUE, PM, POOL, DGX, SNA, SNV, TSCO, UNP, WSO, WBS, SAM, CSX, RHI, SNAP, SIVB, UFPI, WAL, and WHR report. On Friday, we hear from AXP, ALV, EEFT, HCA, HBAN, IPG, RF, SLB, and VZ.

Last night’s big beat by NFLX had futures flying as traders read that turn-around as a sign for tech stocks in general. However, overnight trading soon came back to earth as the market continues to reset expectations for a recession. Another sign of that “recession fear” is that mortgage demand fell to a 25-year low last week as the average mortgage rate for a 30-year, fixed-rate loan rose to 6.94% (from 6.81%). So, it seems good earnings (in general) have only limited strength against a tide of economic pessimism.

With that backdrop, extension is not a factor, either in terms of the T-line or T2122. However, intraday reversals and daily chop are serious concerns. Remember that the downtrend remains intact in all the major indices. So, be cautious and demonstrate patience (wait for confirmation). With high volatility and less certainty, this may be the time to pursue more cautious trading strategies, including remaining hedged, quick, and/or small.

Don’t be stubborn. If you have a loss, just admit you were wrong and take it before it grows. And when price does move in your direction, always move your stops in your favor (remember the “Legend of the man in the green bathrobe“…it is NOT HOUSE MONEY, it’s all OUR MONEY!). Also, keep in mind that trading is not a hobby. It’s a job. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Lastly, remember that you get rich slowly and steadily in Trading…not by striking it rich on one or two trades. So, give up that lottery ticket mentality.

See you in the trading room.

Ed

Swing Trade Ideas for your consideration and watchlist: No trade ideas today (Rick is out). You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Markets gapped up strongly (+1.75% in the SPY, +1.40% in DIA, and up 2.40% in the QQQ) Monday. We then proceeded to get bullish follow-through the first 45 minutes of the day. However, at that point, it was like we hit a brick wall covered in Velcro and just got stuck right there as price traded sideways in a very tight range the entire rest of the day. This action gave us white, Harami candles in all 3 major indices, with DIA being a white, Spinning Top Harami. All 3 now sit on top of their T-line (8ema), but none of them has broken through local resistance or downtrend.

On the day, all 10 sectors are well into the green with Consumer Defensive (+1.37%) lagging and Technology (+3.52%) and Consumer Cyclical (+3.45%) leading the charge higher. The SPY gained 2.52%, DIA gained 1.77%, and QQQ gained 3.30%. The VXX was down 2.84% to 20.84 and T2122 has spiked up, but remains just outside the overbought territory at 75.56. 10-yr. bond yield also showed great volatility, recovering from an early plunge to recover up to 4.017%. And Oil (WTI) is just on the red side of flat at $85.50/barrel. So, overall, a gap-up then a dead flat day.

In economic news, the NY Fed Empire State Mfg. Index came in worse than expected at -9.10, compared to a forecast of -4.00 and September’s reading of -1.50. Meanwhile, Bloomberg Economics updated its model on Monday. The new forecast projects a 100% probability of a recession within the next 12 months. The previous update of the forecast had placed the probability at 65%.

In stock news, STLA said Monday it is seriously considering stopping all car production in China as the major carmakers (western) continue to lose Chinese market share to domestic car companies. Elsewhere, Bloomberg reports that CS has begun the sale of its US Asset Management unit. Sources told Bloomberg that several private equity firms are interested in the unit, which includes a platform for investing in collateralized loan obligations. Meanwhile, GOOGL’s YouTube platform announced new advertising methods to reach music and podcast listeners on Monday. Finally, the Wall Street Journal has reported that INTC has dramatically lowered the valuation of their Mobileye (self-driving car) unit, which the tech giant is in the process of spinning off and IPO. INTC originally expected an IPO price that would give a $50 billion valuation, but now the company is expecting only $20 billion (or less) from the spinoff. The IPO roadshow for that spinoff is set to kick off today and will eventually trade under the ticker MBLY.

In stock legal news, the US Dept. of Justice has moved to dismiss its antitrust indictment against two former PPC executives after other prosecutions on the price-fixing charges failed to secure a conviction. On the other side, the Wall Street Journal reports that the FTC has launched an investigation of V and MA over whether they are using their security token standards to limit debit-card routing competition for online payments. The agency has already been investigating whether the two firms are stopping merchants from routing payments over other debit card networks. Meanwhile, the US DOJ has filed suit against CI, charging that the company over-charged the Medicare Advantage program by submitting false diagnoses (without the tests that would prove the ailments) in order to increase charges between 2012 and 2019. Finally, CS paid $495 million to settle a case related to mortgage-backed securities that had been brought by the state of New Jersey. The NJ Attorney General had claimed $3 billion in damages when the case originated in 2013 and the underlying crime had taken place in 2008.

In energy news, the US EIA said on Monday that oil output from the Texas and New Mexico Permian (shale oil) Basin is forecasted to reach a record in November. The region’s output is forecast to rise by 50,000 barrels per day to 5.453 million barrels per day. This is part of a nationwide increase of 104,000 bpd forecast to come from all US shale basins in the month. Elsewhere, XOM said Monday it has now exited Russia completely after Putin expropriated the company’s Russian properties. XOM values its losses from that expropriation at $4 billion. Finally, Bloomberg reports that the Biden Administration is moving toward releasing another 10-15 million barrels of oil from the strategic petroleum reserve in a bid to keep gas prices under control.

So far this morning, JNJ, GS, and SBNY all reported beats on the top and bottom lines. Meanwhile, TFC, MLI, and CBSH all reported beating on the revenue line while also missing on the earnings line. On the other side, LMT missed slightly on revenue while beating on earnings. However, HAS missed on both the earnings and revenue lines. STT reports later, at 8:50 am.

Overnight, Asian markets were green with only Shanghai (-0.13%) below break-even. At the same time, Hong Kong (+1.82%), Australia (+1.72%), and Japan (+1.42%) led the region higher with most exchanges gaining over one percent. In Europe, we see a similar story taking shape at midday. Portugal (-0.53%) is the only red in the region while the FTSE (+1.00%), DAX (+1.30%), and CAC (+0.83%) lead the continent higher. As of 7:30 am, US Futures are pointing toward another gap higher to start the day. The DIA implies a +1.36% open, the SPY is implying a +1.59% open, and the QQQ implies a +1.84% open at this hour. 10-year bond yields are back down to 3.998% and Oil (WTI) is off a quarter of a percent to $85.22/barrel in early trading.

The major economic news events scheduled for Tuesday are limited to Sept. Industrial Production (9:15 am) and API Weekly Crude Oil Stocks Report (4:30 pm). The major earnings reports scheduled for the day include ACI, GS, HAS, JNJ, LMT, SBNY, STT, and TFC before the open. Then, after the close, AMX, FHN, IBKR, ISRG, JBHT, NFLX, OMC, UAL, and WTFC report.

In economic news later this week, on Wednesday, we see Sept. Building Permits, Sept. Housing Starts, EIA Weekly Crude Oil Inventories, Fed Beige Book, Fed member Bullard speak. On Thursday, Weekly Jobless Claims, Philly Fed Mfg. Index, and Sept. Existing Home Sales are reported. Finally, on Friday, Fed member William speaks.

In earnings reports later this week, on Wednesday, we hear from ABT, ALLY, ASML, BKR, CFG, CMA, ELV, LAD, MTB, NDAQ, NTRS, PG, PLD, SCL, TRV, UNF, WGO, AA, CCI, EFX, IBM, KALU, KMI, KNX, LRCX, LSTR, LVS, LBRT, PPG, STLD, TSLA, and UMPQ. On Thursday, ABB, ALK, T, BX, DHR, DOV, DOW, EWBC, ERIC, FITB, FCX, GPC, HRI, KEY, MAN, MMC, MSM, NOK, NUE, PM, POOL, DGX, SNA, SNV, TSCO, UNP, WSO, WBS, SAM, CSX, RHI, SNAP, SIVB, UFPI, WAL, and WHR report. On Friday, we hear from AXP, ALV, EEFT, HCA, HBAN, IPG, RF, SLB, and VZ.

Overnight gaps seem to be all the rage lately, perhaps revealing a clue to big fund action (manipulation?) in the shadows. And although Monday was a dead tape after 10 am, volatility is still a major concern given the intraday action we saw last week. The premarket seems to indicate we want to test a recent resistance level and has us there now. Don’t get caught up in emotions, especially FOMO. Remember the bull trap on Friday and the bear trap on Thursday that ripped the face off those who chased the gap on those days. Once again, the prudent trader will let things settle out for a while before adding any new positions.

Market extension still is not a factor, either in terms of the T-line or T2122. However, chop and intraday reversal are serious concerns. This will be a big earnings week (see above) and Fed speakers are also likely to cause gyrations as traders keep trying to outguess the FOMC. Remember that the downtrend remains intact in all the major indices. So, be cautious and demonstrate patience (wait for confirmation).

Don’t be stubborn. If you have a loss, just admit you were wrong and take it before it grows. And when price does move in your direction, always move your stops in your favor (remember the “Legend of the man in the green bathrobe“…it is NOT HOUSE MONEY, it’s all OUR MONEY!). Also, keep in mind that trading is not a hobby. It’s a job. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Lastly, remember that you get rich slowly and steadily in Trading…not by striking it rich on one or two trades. So, give up that lottery ticket mentality.

See you in the trading room.

Ed

Swing Trade Ideas for your consideration and watchlist: No trade ideas today (Rick is out). You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

The stage is set for an epic week of price action as the 4th quarter earnings ramp up amid geopolitical and economic uncertainty. Despite the considerable danger, retail speculation remains remarkably high, so plan for big point whipsaws, overnight reversals, and short squeezes to challenge the talents of even the most experienced traders. We remain overdue for a relief rally, but if it begins, be wary of thinking it’s a market bottom. Earnings guidance and stock buybacks will be far more critical than the company hitting the vastly lowered estimates, so be patient jumping right after the headline report.

Asian markets traded mixed overnight as recession weighs on investors despite China holding firm on medium-term rates. European markets trade cautiously higher, waiting on UK fiscal statements and hoping they calm the currency fluctuations and repair some of the ECB credibility. Premarket futures are again pumping up a bullish open on earnings speculation but will the big banks inspire the bulls or the bears after reporting? Of course, anything is possible, so plan carefully.

Economic Calendar

Earnings Calendar

We begin the week relatively light on the earnings calendar, but we have some potential market-moving big bank reports in focus. Notable reports include BAC, BK, SCHW & ELS.

News & Technicals’

The UK’s new finance minister plan to scrap almost all planned tax cuts hoping to calm the markets. However, markets are uncertain by various factors, such as the prospect of much higher government debt. The worries include the enormous subsidies for consumer and business energy bills, the BOE’s current monetary tightening, and the government’s stimulus package. In addition, European solidarity is being tested as Russia’s war in Ukraine continues to cause energy turmoil for countries across the bloc. Paolo Gentiloni, the EU’s economics commissioner, has called for a “united approach,” while Pascal Donohoe, President at Eurogroup, says he “understands” why individual countries are bringing forward their monetary policies.

Stellantis’ electric vehicle plans to compete with firms such as Elon Musk’s Tesla and companies like Volkswagen, Ford, and GM. According to the International Energy Agency, electric vehicle sales are on course to hit an all-time high this year.

After two years of port congestions and container shortages, disruptions are now easing as Chinese exports slow in light of waning demand from Western economies and softer global economic conditions, logistics data shows. “The retailers and the bigger buyers or shippers are more cautious about the demand outlook and are ordering less,” logistics platform Container xChange CEO Christian Roeloffs said in an update on Wednesday. “On the other hand, the congestion is easing with vessel waiting times reducing, ports operating at less capacity, and the container turnaround times decreasing, which ultimately frees up the capacity in the market.”

The ramp-up of 4th quarter earnings, the volatility of last week, and the massive willingness to speculate despite the danger set the stage for an epic week of wild price action. Earnings have the potential to trigger a short squeeze, punishing reversals, and huge intraday whipsaws. Keep an eye on bond yields, and currency fluctuations as the quantitive tightening threaten a banking currency crisis. Company guidance and stock buyback news will be more important than the actual earnings because of the massively lowered estimated targets. We are overdue for a relief rally, and perhaps a bear market rally is possible but be careful thinking it’s a market bottom until we finally see a higher low in the charts. Day traders will likely have the upper hand due to volatility, but they will likely have challenges due to the speed of the potential price swings.

US markets gapped higher at the Friday (+0.70% in the SPY, +0.65% in the DIA, and +0.95% in the QQQ) on solid big bank earnings reports. However, within 10 minutes, the reversal kicked in to see all 3 major indices sell off hard the first hour. Then a long, slow, grinding bear trend took over to drive us to the lows of the day within a couple of minutes of the close. This action gave us a Bear Dark Cloud Cover signal in the SPY and QQQ, with a similar candle in the DIA (just support from the T-line prevented it from reaching the right size to be a true Dark Cloud Cover). The SPY and QQQ also both failed to find support at their T-lines (8ema).

On the day, all 10 sectors were in the red, with Basic Material (-3.75%) leading the market lower while Healthcare (-1.33%) and Communication Services (-1.36%) held up the best. Meanwhile, SPY was down 2.28%, DIA was down 1.24%, and QQQ was down 3.01%. The VXX was up 2.24% to 21.45 and T2122 fell but remains in the mid-range at 34.78. 10-year bond yields have reversed an early loss to jump to 4.022% while Oil (WTI) is down 3.92% to $85.61/barrel. Overall, Friday was a big “bull trap” bearish reversal day which also partially reversed Thursday’s wild bullish ride.

In economic news Friday, September Retail Sales came in dead flat (compared to a forecast of +0.2% and an August reading of +0.4%). The September Export Price Index was -0.8% (which was better than the -1.0% forecast and the August -1.7%) while the Sept. Import Price Index was -1.2% (which was lower than the forecast -1.1% as well as the August -1.1%). August Business Inventories grew less than expected at +0.8% (versus the +0.9% forecast and July’s +0.5%). The Michigan Consumer Sentiment reading was better than expected a 59.8 (versus the 59.0 forecast and last month’s 58.6 number). On the Fed front, in a speech at Harvard, Fed Governor Waller said that a digital dollar would not offer material benefits over current US-dollar-denominated payments. He said this is especially true since a central bank digital currency would introduce additional threats, such as cybersecurity threats. Finally, Atlanta Fed President Bostic announced late Friday that he had “accidentally” broken Fed trading rules over recent years by doing personal trading during the Fed blackout (pre-announcement) periods, had filed “incomplete” disclosure documents, and had owned more than the permissible limit of US Treasury Bonds last year. He went on to say that despite these revelations, he had never traded on non-public information. However, the Fed has begun an investigation and the same type of activity has led to two Fed resignations in the last year.

In stock news, ABT recalled some of its liquid Similac brand baby formula (due to a bottle defect) on Friday. Meanwhile, Reuters reported that CS is in talks with several of its peer big banks about underwriting a potential stock offering to raise capital. The bank said it would prefer not to sell more shares at the current depressed price, but is making plans in case it becomes unavoidable. The Wall Street Journal reported that Rupert Murdoch is considering combining FOX (and FOXA) with NWSA. Elsewhere, SLB is getting backlash from 9,000 Russian employees after the company began cooperating with Russian authorities to carry out military conscription orders at work. On Saturday, a second AAPL store (in OK this time) voted to unionize.

In international news, on Friday, UK Prime Minister Truss fired her finance minister (Chancellor of the Exchequer). She also reversed course on the corporate tax cuts she had promised and dug her heels in to defend as late as Thursday. However, calls for her to resign (just 38 days into the job) continued this weekend. Meanwhile, markets in the UK are in crisis due to contradictory, unworkable, and unpopular messaging and policies coming out of the PM and her cabinet. Meanwhile, in China, Xi Jinping opened the Communist Party Congress and is expected to be reelected to an unprecedented third term as the head of the Chinese Communist Party later this week. In his opening speech, Xi doubled down on his “Zero Covid” policy (which still has several major cities locked down and has quarantines in place for some intracity travel) as well as calling for more competition with the US, including the semiconductor arena.

In dividend news, on Sunday, Investing.com reported last week’s largest dividend hikes. CMC raised its quarterly dividend by 14.3% to $0.16/share (which amounts to an annual yield of 1.6%). LOCO declared a special dividend of $1.50/share (for holders of record on 10/24) to be payable on Nov. 9. MCD increased its dividend by over 10% to reach a 2.5% annual yield of $6.08/share. Meanwhile, SKT increased its annual dividend by 10% to $0.22/share, which is a 1.5% annual yield.

So far this morning, BAC and BK both reported beats on the revenue and earnings lines. In particular, BAC beat revenue estimates by nearly $7 billion. (SCHW reports at 8:45 am). In other bank news, the Wall Street Journal reports that GS implemented a sweeping reorganization, splitting its largest unit into three divisions while also combining its asset management and wealth management businesses into a single unit.

Overnight, Asian markets were mixed with Australia (-1.40%), Taiwan (-1.23%), and Japan (-1.16%) leading the losses. Meanwhile, India (+0.73%), Thailand (+0.68%), and Shanghai (+0.42%) paced the gains. However, in Europe, the exchanges are green across the board. The FTSE (+0.72%), DAX (+0.91%), and CAC (+0.93%) are leading the region higher partially on the good news that Germany has no filled 95% of their natural gas storage (ahead of winter) and partially on a nearly total reversal by the UK government on it unfunded tax cuts and freeze of cost-of-living adjustments. As of 7:30 am, US Futures are pointing to a significant gap up to start the week. The DIA implies a +1.03% open, the SPY is implying a +1.24% open, and the QQQ implies a +1.49% open at this hour. 10-year bond yields continue being volatile as they have plunged back down to 3.947% and Oil (WTI) is flat at 85.61/barrel in early trading.

The major economic news events scheduled for Monday are limited to NY Empire State Mfg. Index (8:30 am) and Federal Budget Balance (2pm tentative). The major earnings reports scheduled for the day include BAC, SCHW, and BK before the open. There are no major reports scheduled for after the close.

In earnings reports later this week, on Tuesday, ACI, GS, HAS, JNJ, LMT, SBNY, STT, and TFC report. Then Wednesday, we hear from ABT, ALLY, ASML, BKR, CFG, CMA, ELV, LAD, MTB, NDAQ, NTRS, PG, PLD, SCL, TRV, UNF, WGO, AA, CCI, EFX, IBM, KALU, KMI, KNX, LRCX, LSTR, LVS, LBRT, PPG, STLD, TSLA, and UMPQ. On Thursday, ABB, ALK, T, BX, DHR, DOV, DOW, EWBC, ERIC, FITB, FCX, GPC, HRI, KEY, MAN, MMC, MSM, NOK, NUE, PM, POOL, DGX, SNA, SNV, TSCO, UNP, WSO, WBS, SAM, CSX, RHI, SNAP, SIVB, UFPI, WAL, and WHR report. On Friday, we hear from AXP, ALV, EEFT, HCA, HBAN, IPG, RF, SLB, and VZ.

Volatility seems to want to continue to be the rule, as premarket futures indicate we will be popping back inside Friday’s big, ugly black candle. However, do not get caught up in emotions. Remember the bull trap on Friday and the bear trap on Thursday that ripped the face off those who chased the gap those days. So, just let things settle out for a while before you go adding any new positions.

Extension isn’t a factor today, either in terms of the T-line or T2122. However, volatility and intraday reversal are valid and serious concerns. This will be a big earnings week (see above) and Fed speakers are also likely to cause gyrations as traders keep trying to outguess the FOMC. Remember that the downtrend remains intact in all the major indices and, for what it is worth, we also had a bearish candle signal on Friday. So, be cautious and demonstrate patience (wait for confirmation).

Don’t be stubborn. If you have a loss, just admit you were wrong and take it before it grows. And when price does move in your direction, always move your stops in your favor (remember the “Legend of the man in the green bathrobe“…it is NOT HOUSE MONEY, it’s all OUR MONEY!). Also, keep in mind that trading is not a hobby. It’s a job. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Lastly, remember that you get rich slowly and steadily in Trading…not by striking it rich on one or two trades. So, give up that lottery ticket mentality.

See you in the trading room.

Ed

Swing Trade Ideas for your consideration and watchlist: DHC, WFC, JPM, BA, LUV, SB, NWL, EA, IGT. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

Yesterday’s CPI number triggered a rollercoaster ride of market emotions ranging from despair to euphoria, swinging the Dow more than 1400 points from low to high. The big question for today is can it continue facing higher rates, rising inflation, recession, and slowing world economies? With a busy day of potentially market-moving earnings and economic reports, will the rally continue or come to a screeching halt as quickly as it began? The one thing we can say for sure is the wild price volatility makes for a dangerous trading environment that could whipsaw or reverse suddenly, so plan your risk carefully heading into the uncertainty of the weekend.

Asian markets surged higher overnight in reaction to the vast U.S. short-squeeze reversal. This morning, European markets trade green across the board, hoping for a U.K. fiscal policy reversal. As earnings results roll out with a pending retail sales report, U.S. futures point to a bullish open but be prepared for just about anything with market emotions so high. Buckle up; it will likely be another very hectic day of price gyrations.

Economic Calendar

Earnings Calendar

The earnings ramp-up begins with several more reports that are potentially market-moving today. Notable reports include C, JPM , MS, PNC, USB, UNH & WFC.

News & Technicals’

Kwarteng’s abrupt departure from a series of international finance meetings in Washington, D.C., comes amid a growing political backlash against the Conservative government’s proposed tax cuts. The debt-funded measures announced on Sept. 23 and estimated to total £43 billion ($48.7 billion) sent financial markets into a tailspin. As a result, Prime Minister Liz Truss is under immense pressure to rethink her economic policies as opinion polls show support for her government has collapsed.

People are increasingly using their social networking “feeds” to discover compelling content as opposed to viewing the media shared by the friends that they follow. Zuckerberg referred to TikTok as a “very effective competitor.” Therefore, it’s important for Meta to develop AI that can recommend a range of content, including photos and text, to users besides just short videos. Twitter said in a court filing that it’s been trying since July to obtain materials related to a federal investigation into his effort to buy the company. “This game of ‘hide the ball’ must end,” Twitter lawyers said in the filing.

President Joe Biden recently claimed the “pandemic is over,” but the extension of the public health emergency indicates the administration does not believe the U.S. is out of the woods yet. The public health emergency, first declared in January 2020 by the Trump administration, has been renewed every 90 days since the pandemic began. The powers activated by the emergency declaration have greatly impacted the U.S. healthcare system and social safety net.

Thursday was a rollercoaster ride, with the Dow futures falling as much as 600 points after the much hotter-than-expected CPI. However, after the open, they trigger a massive short squeeze, recovering the early losses and surging up more than 800 points. The dollar pulled back, and the bond yields eased, helping the bulls to relieve the selling pressure. But, with the hard-to-face economic facts of slowing economies, inflation, and recession, can the rally continue? This morning we will get several potential market-moving earnings and economic reports that could keep the rally going or bring it to a screeching halt. There is a lot at stake, and the potential amlitude of these huge point moves makes for a very dangerous trading environment.

Huge volatility was the rule Thursday. Stocks gapped sharply lower at the open (-2% in the SPY, -1.8% in the DIA, and -2.9% in the QQQ) after a hot September CPI number. However, as I had warned in the morning blog, whiplash immediately kicked in as the bulls led a huge rally until 11:45 am. Over those 2.25 hours, the SPY gained a massive 5%, DIA gained a staggering 4.5%, and QQQ gained an incredible 6%. However, that was not the end of the huge volatility. The rest of the afternoon, we saw a couple more big moves to the downside (and the resulting even larger whips back to the upside). Still, it is important to note that the volume on those later swings began to fade as the day ground on. In the end, we closed not too far from the highs of the day.

This action gave us huge, heavy volume, Bullish Engulfing candles (with small wicks on both ends) in all 3 major indices. The SPY and DIA managed to cross and close above their T-lines (8ema), but the QQQ failed that test (at least for the day). All 10 sectors are green with Energy (+3.67%) leading the charge and the Consumer Cyclical sector (+1.22%) lagging. The SPY gained 2.61%, DIA gained 2,84%, and QQQ up 2.32%. Meanwhile, the VXX fell 2.6% to 20.98 and T2122 has jumped from oversold up into the mid-range at 65.15. 10-year bond yields have spiked to 3.96% and Oil (WTI) was up 2.13% to $89.13/barrel.

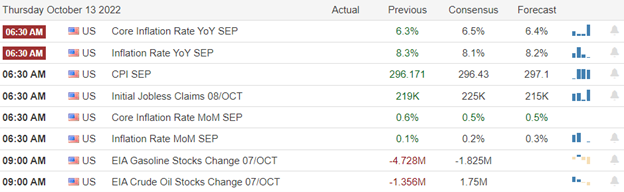

In economic news, as mentioned above, the September Month-on-month CPI reading came in at +0.4% (versus +0.2% forecast and +0.1% in August). That took the September Annualized CPI to +8.2% (versus +8.1% that had been forecast and +8.3% as of August). So, inflation fell slightly on an annual basis, but not as much as expected. The Weekly Initial Jobless Claims also came in slightly above expectations at 228k (versus 225k forecast and 219k last week). Finally, in the late morning, the EIA Crude Oil Inventory showed a massive 9.880 million barrel increase in stocks (versus a forecast 1.750 million barrel build forecast and a drawdown of 1.356million barrels last week).

In stock news, AAPL and GS launched a joint “high yield savings account” product for holders of the AAPL credit card. Bloomberg reported that KR is in talks to buy smaller rival ACI. ACI spiked 11.5% on the news and KR also closed up 1.15%. Elsewhere, NFLX announced its long-planned “with Ads” tier service for $6.99/mo. starting Nov. 3. Later, STLA (Dodge/Jeep parent) announced it is cutting one of its three shifts at its Warren MI plant due to a persistent shortage of chips. Meanwhile, the Chairman of C told a conference that higher capital requirements for big banks (as proposed for the banks entering into riskier cryptocurrency business) might curb lending and make the “potential coming recession” worse. Finally, a Brazilian court has fined AAPL $19 million and ordered that the iPhones the company sells in that country must come with chargers.

In trading news, on Thursday afternoon, Reuters reported that 24×7 stock trading is likely coming to the US within 5 years. The report cited sources at several brokers, electronic exchanges, as well as the CBOE exchange, all speaking at the Security Traders Assn. Annual Conference. There was no specific mention of Options, but one would assume that if the underlying assets were trading 24×7, the options on them would as well. So, traders may need to study the trading processes and approaches being used in the Forex and Cryptocurrency markets today for a heads-up on how we may be trading stocks in the not-too-distant future.

In Energy news, despite the overall large build in US oil inventories last week, there was a disturbing drawdown in Diesel and Heating Oil stock. The EIA reported that Distillates stocks, fell 4.9 million barrels for the week to the lowest level since May. With Winter fast approaching this should be upsetting news for consumers that appear will get the shaft as low inventories allow dealers to charge higher prices. This news was partially responsible for oil’s 2% rise on Thursday, despite a 10 million barrel increase in oil inventories and a 2 million barrel increase in gasoline stockpiles.

Overnight, Asian markets leaned heavily to the green side. Only Thailand (-0.12%) and Singapore (-0.03%) were in the red. Meanwhile, Japan (+3.25%), Shenzhen (+2.81%), and Taiwan (+2.48%) led the gainers. In Europe, we are seeing a similar push to the upside at midday. Only Russia (-0.79%) is showing red, while the FTSE (+1.25%), DAX (+1.21%), and CAC (+1.77%) lead the region higher in early afternoon trade. As of 7:30 am, US Futures are pointing toward a modestly green open after Thursday’s volatile, large gain. The DIA implies a +0.47% open, the SPY is implying a +0.32% open, and the QQQ implies a +0.08% open at this hour. 10-year bonds are showing their own volatility, plunging back down to 3.887% while Oil (WTI) is off just over 1% to $88.13/barrel in early trading.

The major economic news events scheduled for Friday include September Retail Sales and September Import/Export Price Indexes (both at 8:30 am), August Business Inventories, Mich. Consumer Sentiment, and August Retail Inventories (all at 10 am). The major earnings reports scheduled for the day include C, FRC, JPM, MS, PNC, USB, UNH, and WFC before the open. There are no major reports scheduled for after the close.

So far this morning, UNH, JPM, WFC, C, USB, PNC, and FRC all posted beats on both the top and bottom lines. JPM beat on revenue by almost $9 billion while the other large banks had significant revenue beats as well. However, MS reported a miss on both revenue and earnings, which they attributed to a collapse of its investment banking business. In addition, note that USB and FRC both lowered forward guidance after posting their beats. Finally, KR (second only to WMT among US grocers) announced it has reached the previously mentioned deal to buy ACI (the fourth largest US grocer) for $34.10/share or $24.6 billion.

After yesterday’s extreme volatility and bullish reaction to CPI, as well as a dose of great earnings this morning, the overall mood is likely to be bullish, but leery early in the day. It is less likely the data we get today will reverse markets from any move, but it could dampen or amplify what Mr. Market is doing at that time. With that said, volatility remains a very big concern unless you have the stomach to ride out big swings.

With this backdrop, the premarket action seems to show some modest optimism. Extension isn’t a factor today, either in terms of the T-line or T2122. However, that T-line (8ema) will be a level to watch as we see whether it can hold as support for the large caps or resistance for the QQQ. Today we know three things for sure. First, the strong bear trend is still in place. Second, volatility and huge intraday reversals were off the charts yesterday. And third, the weekend, when we can’t adjust while the market is closed, lies just ahead. So, consider whether you need to take some money off the table or add hedges today. (Remember, the first rule of making big money is to not lose big money.)

So, don’t be stubborn. If you have a loss, just admit you were wrong and take it before it grows. And when the price does move in your direction, always move your stops in your favor (remember the “Legend of the man in the green bathrobe“…it is NOT HOUSE MONEY, it’s all OUR MONEY!). Also, keep in mind that trading is a job. It’s not a hobby. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Demonstrate patience and wait for confirmation. Lastly, remember that you get rich slowly and steadily in Trading…not by striking it rich on one or two trades. So, give up that lottery ticket mentality.

See you in the trading room.

Ed

Swing Trade Ideas for your consideration and watchlist: No trade ideas today. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

If the choppy price action of late has been frustrating, the wait is over, and let the volatility begin. Not only do we have the CPI and Jobless Claims, but we also kick off the wild speculation and price manipulation of the 4th quarter earnings season. While companies may hit substantially lowered earnings estimates, the guidance forward and the commitment to stock buybacks will likely be most important for the future direction of the stock prices. Expect the challenging price action to continue with the path forward, which is looking so uncertain at this time.

Asian markets declined across the board as investors traded cautiously ahead of U.S. inflation data. European markets, however, show some willing bulls as they brace for the coming numbers. This morning looks like a repeat of yesterday’s premarket pump, pointing to a bullish open ahead of earning and economic report results. I guess the question to be answered is, with this pump-up speculation be successful, or will it result in another disappointing pop and drop? Buckle up; we’re about to find out!

Economic Calendar

Earnings Calendar

We’ve made it to the official kick-off day of the 4th quarter earnings. Notable reports include BLK, CMC, DAL, FAST, PGR, TSM & WBA.

News & Technicals’

Belgium’s central bank chief told CNBC that the European Central Bank needs to raise interest rates into positive territory when considering inflation, despite recession fears. “My bet would be it’s going to be over 2%, and I would not be surprised if we have to go to above 3% at some point,” said Pierre Wunsch, governor of the National Bank of Belgium. However, he said that September’s hike in the ECB’s benchmark deposit rate to 0.75% meant rates were still negative in real terms.

Cash, one of the most hated corners of the market for years, is getting some newfound love from money managers as the Federal Reserve’s firm commitment to rate hikes roiled nearly every other asset class. Global money market funds saw $89 billion of inflows for the week ending Oct 7, the largest weekly injection into cash since April 2020, according to Goldman Sachs’ trading desk data. Meanwhile, the data said that mutual fund managers also hold a record amount of cash.

The Office for National Statistics estimated Wednesday the U.K. economy shrank by 0.3% in August, potentially beginning what economists expect will be a lengthy recession through the winter. In addition, postal workers, rail workers, and public barristers have all carried out strikes recently to protest pay and conditions, as wages fail to keep up with inflation running at around 10%. A worst-case scenario laid out by national electricity system operator the National Grid warned that households and businesses might face three-hour power outages over winter. Asia’s biggest economic problems next year will stem from rising interest rates. These will put increasing pressure on debt servicing in Asia and heighten capital flight from the region: IMF The U.K. bond crisis will have limited impact on Asian markets, although “anything that creates financial market turbulence will find a way” to upset other economies: IMF. As many Asian economies, such as Japan and Hong Kong, open up, increased human mobility will generate economic activity and stall a slowdown.

The wait is over, so let the volatility begin. After the disappointing PPI number, the dollar rose, the bond yields surged, and the FOMC minutes say the hawkishness is not yet over! That made for a choppy Wednesday as traders pondered the CPI, Jobless Claims, and what earnings reports might reveal. Once again, the overnight futures are working to pump up a bullish open but will it be just another pop and drop to punish those rushing in hoping to pick the bottom? We sure could use a rally with the indexes in a short-term oversold condition, but it may not be a tough sell if inflation remains resilient. As earnings number ramp up, expect wild speculation and price volatility to do the same. I think the company’s guidance and stock buyback levels will be more important this season than hitting the substantially lowered estimates. So be careful jumping in too soon and wait for the conference call before making your decision. Likely challenging times lie ahead, so plan your risk carefully.

Markets opened little changed Wednesday and then chopped sideways in a fairly small range. The only exception to this was the SPY which plunged the last 15 minutes of the day to get back near the lows. The DIA did retest its T-line (8ema), but failed, while the other 2 major indices didn’t even come close. This action is giving us Indecisive, Inside Day candles in all 3 of the major indices. The Spy printed more of an Inverted Hammer candle while the DIA gave us a Doji and the QQQ printed a Spinning Top. Overall, just a volatile, sideways day that seems to be coiling up as we wait for another shoe to fall.

On the day, seven of the 10 sectors are in the red with Utilities (-2.99%) being by far the biggest losing group. On the other side, Consumer Cyclical (+0.27%), Consumer Defensive (+0.24%), and Energy (+0.20%) were the gaining sectors. Meanwhile, SPY was down 0.32%, DIA was down 0.04%, and QQQ was down 0.03%. The VXX was off 1.01% to 21.54 and T2122 remains oversold at 15.81. 10-year bond yields backed off to 3.898% and Oil (WTI) was down 2.5% to $87.12/barrel.

In economic news, September PPI came in twice as hot as expected at +0.4% (versus +0.2% forecasted and actual in August). For what it is worth, the September Core PPI (with food and energy prices stripped out) came in as expected at +0.3%, which was also the same as August. In the afternoon, the September FOMC Meeting Minutes did not give us any new information. Just as Fed speakers have been telling us since the meeting, the FOMC expects rate hikes to continue at a higher pace and a higher final interest rate level for a longer period than originally expected since inflation is showing little sign of abating yet. After the close the API reported a 7.054-million-barrel crude oil inventory increase this week, dramatically reversing last week’s 1.770-million-barrel drawdown. Finally, Treasury Sec. Yellen expressed concerns about liquidity in the bond market as many of the largest buyers have gone away. Sovereigns, Japanese and European insurance and pension funds, etc. all have their own financial problems and are not looking to add US bonds. As a result, as the supply of Treasuries has climbed, a lack of liquidity has driven average yields higher and caused outsized volatility. (I’m not sure that is news, because that is how I was taught that free markets work…when supply goes up and demand goes down, the price falls, meaning in this case the yield rises. Nonetheless, she said it, and the financial media all thought it was newsworthy enough to report.)

In stock news, Wednesday afternoon, it was announced that CCJ (a uranium supplier) and BEP (a utility) are teaming up to acquire Westinghouse from BBU (a holding company affiliated with BEP). The $7.9 billion deal will give CCJ a 49% ownership interest in the Westinghouse venture as nuclear power becomes more popular again. Across the pond, the EU approved the deal where CE will buy DD’s “Mobility and Materials” business unit for $11 billion. After the close, CLF announced the USW union had ratified a new 4-year labor contract covering 12,000 of its employees. At the same time, AMAT announced it was cutting its Q4 revenue estimate, citing new export regulations as a headwind. Meanwhile, the NRLB cited SBUX for having called the police to disperse employees that were pro-union at a Kansas store. Finally, AMZN announced that it is switching rockets for the upcoming launch of its prototype satellites (intended to compete with Elon Musk’s Starlink of satellite-based high-speed internet system). The new rocket is from UAL (a joint venture by BA and LMT).

In Energy news, Oil was down in great part to a very strong dollar. (The Euro fell further below parity to $0.97 while the Dollar rose to a 24-year high of 146.91 Yen.) In company-related news, XOM announced that its new carbon emissions reduction business, called Low Carbon Solutions unit, had signed CF (the world’s largest ammonia manufacturer) as its first client. At the same time, they signed a second deal with ENLC (an oil pipeline network). After he close the EIA (US Energy Information Administration) said that consumers can expect to pay 28% more (compared to last year) to heat their homes this coming winter. This is based on Natural Gas (half of all homes) prices up 28% year-over-year, Electricity (40% of homes) up 10% over last year, and Heating Oil (9% of homes) up 27% on the year.

So far this morning, WBA, TSM, and FAST all beat on both the revenue and earnings lines. (As mentioned above, even though TSM beat, it also drastically cut new capital spending for the rest of the year…even while raising guidance.) Meanwhile, BLK and CMC missed on revenue while beating on earnings. On the other side, DAL beat on revenue while missing on earnings. However, DAL did raise guidance after reporting a major surge in summer travel. Finally, DPZ missed on both lines.

Overnight, Asian markets were red across the board. Taiwan (-2.07%), Hong Kong (-1.87%), and South Korea (-1.80%) led the red tide, perhaps aided by TSM (the world’s largest chipmaker) cutting 2022 capital spending by 10% in a major warning shot fired across the bow of tech companies. Meanwhile, in Europe, stock exchanges are mixed but lean to the green side at midday. The FTSE (+0.04%), DAX (+0.87%), and CAC (+0.40%) are leading the move with four of the smaller exchanges lagging and still red in early afternoon trade. As of 7:30 am, US Futures are pointing toward a modestly green open ahead of consumer inflation data. The DIA implies a +0.58% open, the SPY is implying a +0.55% open, and the QQQ implies a +0.30% open at this hour. 10-year bond yields remain at 3.89% and Oil (WTI) is also little moved at $87.40/barrel in early trading.

The major economic news events scheduled for Thursday include September CPI and Weekly Initial Jobless Claims (both at 8:30 am), EIA Weekly Crude Oil Inventories (11 am), and the Federal Budget Balance (2 pm tentative). The major earnings reports scheduled for the day include BLK, CMC, DAL, DPZ, FAST, INFY, PGR, TSM, and WBA before the open. There are no major reports scheduled for after the close.

In economic news later this week, on Friday we get September Retail Sales, September Import/Exports, August Business Inventories, Mich. Consumer Sentiment, and August Retail Inventories.

In earnings reports later this week, on Friday, the big banks really kick off earnings season as C, FRC, JPM, MS, PNC, USB, UNH, and WFC all report.

Markets will be focused on CPI data in at least the pre-market this morning, even though we have had some generally good earnings reports. For what it is worth, Moody’s Chief Economist said overnight that his analysis leads him to expect a significant inflation reduction within 6 months. However, just from a read-through of the PPI data, we should expect a very hot inflation number today. Don’t be surprised if we see more whiplash as markets overreact early, rethink and whip back in the other direction. However, at the moment we appear stuck between this week’s low and the T-line.

With this backdrop, the premarket action seems to show some optimism ahead of the CPI data. The market remains a bit extended in terms of T2122, but not extremely so. Watch the T-line levels for resistance if we bounce on the CPI data. Once again, the one thing we know is that the strong bear trend is still in place and markets have been indecisive the last two days…as if waiting. So, don’t predict a bottom, but keep a watchful eye on market price action.

Don’t be stubborn. If you have a loss, just admit you were wrong, respect your stop, and take the loss before it grows. When price does move in your direction, always move your stops in your favor (remember the “Legend of the man in the green bathrobe“…it is NOT HOUSE MONEY, it’s all OUR MONEY!). Also, keep in mind that trading is a job. It’s not a hobby. So, treat it that way. Do the work and follow the process. Stick to your trading rules, trade with the trend, and take those profits when you have them. Demonstrate patience and wait for confirmation. Lastly, remember that you get rich slowly and steadily in Trading…not by striking it rich on one or two trades. So, give up that lottery ticket mentality.

See you in the trading room.

Ed

Swing Trade Ideas for your consideration and watchlist: WBA, APA, HALO, BA, RCL, MO, UPST. You can find Rick’s review of tickers on his YouTube Channel here. Trade your plan, take profits along the way, and smart. Also, remember to check for impending earnings reports. Finally, remember that any tickers we mention and talk about in the trading room are not recommendations to buy or sell.

🎯 Mike Probst: Rick, Got CTL off the scanner today. Already up 30%. Love it.

🎯 DickCarp: the scanner paid for the year with HES-thank you

🎯 Arnoldo Bolanos: LTA scanner really works $$, thanks Ed.

🎯 Bob S: LTA is incredible…. I use it … would not trade without it

🎯 Malcolm .: Posted in room 2, @Rick… I used the LTA Scanner to go through hundreds of stocks this weekend and picked out three to trade: PYPL, TGT, and ZS. Quality patterns and with my trading, up 24%, 7% and 12%…. this program is gold.

🎯 Friday 6/21/19 (10:09 am) Aaron B: Today, my account is at +190% since January. Thanks, RWO HRC Flash Malcolm Thomas Steve Ed Bob S Bob C Mike P and everyone that contributes every day. I love our job.

Hit and Run Candlesticks / Road To Wealth Youtube videos

Disclosure: We do not act on all trades we mention, and not all mentions acted on the day of the mention. All trades we mention are for your consideration only.

DISCLAIMER: Investing / Trading involves significant financial risk and is not suitable for everyone. No communication from Hit and Run Candlesticks Inc, its affiliates or representatives is not financial or trading advice. All information provided by Hit and Run Candlesticks Inc, its affiliates and representatives are intended for educational purposes only. You are advised to test any new trading approach before implementing it. Past performance does not guarantee future results. Terms of Service

The bulls tried to get upside price action going, but all at once, the bears returned with a vengeance producing a nasty whipsaw to punish the dip buyers. As a result, the QQQ closed at a new 2022 low, while the other indexes managed to hold Monday’s low. Before the bell today, we will get the Producer price report and then deal with the FOMC minutes this afternoon. In addition, we will have to keep a close on rising bond yields and fluctuating currency after the BOE deadline warning to pension plans. Finally, no matter the market reaction, keep in mind the CPI numbers come out before the bell Thursday, so plan your risk carefully!

Asian markets traded mixed as the Yen continued to weaken to 146 to 1 against the dollar. European market trade mixed in a choppy session, waiting for U.S. inflation data. However, the U.S. futures push for a bullish open ahead of the PPI number. How the market reacts after the number is anyone’s guess. Perhaps the futures premarket pump will signal a relief rally, or perhaps they are just trying to put lipstick on a pig.

Economic Calendar

Earnings Calendar

With the official kickoff of 4th quarter earnings beginning tomorrow, we have another light day of reports. Notable reports include PEP & DCT.

News & Technicals’

Tobias Adrian, director of monetary and capital markets at the International Monetary Fund, told CNBC Jamie Diamon’s call that U.S. stocks could tumble another 20% was “certainly possible.” He said sentiment had so far held up relatively well, but a shift in this could spark a further downturn. Adrian also warned financial stability risks are very elevated, with the global economy in a “very, very stressed moment.” Sridhar Ramaswamy, who led Google’s advertising business from 2013 to 2018, has launched a Web3 company called nxyz. Nxyz trawls blockchains and their associated applications for data on things like NFTs and crypto wallets and then streams it to developers in real time. The company raised $40 million in a funding round led by crypto-focused venture fund Paradigm, with additional backing from Coinbase, Sequoia, and Greylock.

The U.S. Department of Commerce introduced sweeping rules to prevent China from obtaining or manufacturing key chips and components for supercomputers. Analysts said that this is likely to hobble China’s domestic chip industry. In addition, Washington’s export rules could touch other parts of the supply chain that use American technology, highlighting the wide-ranging nature of the latest restrictions.

Unbelievable

“I don’t think there will be a recession. If it is, it’ll be a very slight recession. That is, we’ll move down slightly,” Biden told CNN’s Jake Tapper in a Tuesday interview. On Monday, JPMorgan Chase CEO Jamie Dimon told CNBC there would likely be a recession in six to nine months. In September, the U.S. central bank raised benchmark interest rates by three-quarters of a percentage point —the Fed’s third consecutive hike. Treasury Secretary Janet Yellen said the U.S. is doing well amid global economic uncertainty. Yellen said the U.S. economy has slowed after a strong recovery, but job reports indicate a resilient economy. The Treasury Secretary reiterated that lowering inflation is a priority of the Biden administration.

Yesterday proved to be another choppy day as the bulls finally pushed off the lows only to have the bears produce a nasty whipsaw, driving indexes down in a quick move. The QQQ made a fresh 2022 low after the BOE set a deadline for pension plans to make adjustments as central bank interventions end. Today we face the latest reading on Producer Prices, more Fed speak, and we will get the minutes of the last FOMC meeting. I think the market is looking for any hope to relieve the short-term oversold condition of the indexes. Still, traders must remain aware of the currency liquidity issues and bond yield gyrations. As you make trading decisions, remember we get the CPI number before the bell on Thursday and begin the 4th quarter earnings with the big bank reports. Plan for a heavy dose of price volatility.